Introduction

Many UK businesses misapply or completely miss reverse charge VAT obligations across their cross-border, construction, and domestic transactions. The reverse charge shifts VAT accounting from supplier to customer — a mechanism designed to combat fraud but one that catches out even experienced finance teams.

This guide is for UK VAT-registered businesses buying services from abroad, operating in construction, or dealing in specified goods such as mobile phones or wholesale energy.

Getting it wrong carries real consequences: HMRC penalties, interest charges, and in serious cases, loss of input tax recovery rights. For partially exempt businesses, it also creates cash flow problems that compound quickly.

Here's what this guide covers:

- What reverse charge VAT is and why it exists

- Where it applies in the UK (cross-border, construction, specified goods)

- How to account for it correctly on your VAT return

- Invoicing requirements for suppliers and customers

- The most common mistakes — and how to avoid them

Key Takeaways

- Reverse charge VAT shifts VAT responsibility from the supplier to the buyer, who calculates and reports it directly

- Applies in three UK contexts: imported services, specified domestic goods (mobile phones, wholesale electricity), and CIS construction supplies

- For VAT returns: enter output tax in Box 1 and reclaim it as input tax in Box 4, resulting in net zero for fully taxable businesses

- Suppliers must not charge VAT but must include "reverse charge" wording and state the VAT amount for customer self-accounting

- Misapplication risks penalties, interest, and loss of input tax recovery

What Is Reverse Charge VAT in the UK?

Reverse charge VAT flips the normal VAT accounting process. Instead of the supplier charging VAT and paying it to HMRC, the customer self-accounts — declaring it as output tax and (where eligible) reclaiming it as input tax on the same return.

HMRC describes it as requiring the customer to "act as if you are both the supplier and the recipient of the services." In practice: you calculate the VAT, report it in Box 1 of your VAT return, and reclaim it in Box 4 — subject to normal input tax rules.

Why Reverse Charge Exists

The reverse charge was introduced to close the missing trader (carousel) fraud loophole. Fraudulent suppliers would charge VAT to customers — who would reclaim it as input tax — but never remit that VAT to HMRC. Section 55A of the VAT Act 1994 explicitly authorizes reverse charge "to counter... missing trader fraud."

The scale made action unavoidable. MTIC fraud cost the UK exchequer between £1.1 billion and £1.9 billion in 2004-05 alone.

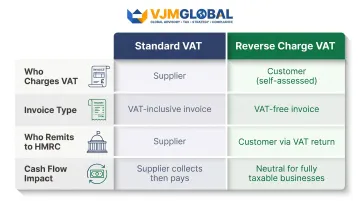

How It Differs from Standard VAT

| Standard VAT | Reverse Charge VAT | |

|---|---|---|

| Who charges VAT? | Supplier | Customer (self-assessed) |

| Invoice type | VAT-inclusive invoice | VAT-free invoice |

| Who remits to HMRC? | Supplier | Customer (via VAT return) |

| Cash flow impact | Supplier collects, then pays | Neutral for fully taxable businesses |

For fully taxable businesses, the net VAT position is zero — but the compliance obligation is strict.

Where Reverse Charge VAT Applies in the UK

Reverse charge VAT applies across three distinct UK scenarios, each governed by different rules with important thresholds and conditions.

Buying Services from Overseas Suppliers

When a UK VAT-registered business purchases services from an overseas supplier — software licences from Adobe or Google, consultancy, legal services, or marketing support — the overseas supplier typically does not charge UK VAT. The UK buyer must still account for it under the reverse charge, using the Place of Supply rules in VAT Notice 741A.

Under the B2B general rule, a supply is made where the customer belongs. If you're a UK business receiving services from abroad where the place of supply is the UK, you must apply the reverse charge.

Watch the registration threshold: The value of overseas services purchased counts toward the VAT registration threshold — currently £90,000 in any rolling 12-month period. Even if your own sales are exempt or below the threshold, large purchases of services from abroad can force you to register. This catches charities, education providers, and other exempt organisations off guard more often than expected.

Domestic Reverse Charge for Specified Goods and Services

The domestic reverse charge under VAT Notice 735 applies to B2B transactions involving:

- Mobile phones and computer chips — only when the VAT-exclusive invoice value is £5,000 or more

- Wholesale gas and electricity

- Wholesale telecommunications services

- Emission allowances

- Renewable energy certificates

For mobile phones and computer chips, the reverse charge only applies when the VAT-exclusive invoice value is £5,000 or more, calculated on a per-invoice basis. HMRC explicitly warns against disaggregation — splitting orders to fall below the threshold. Where a supplier has reasonable grounds to believe a customer is doing this, they should apply the reverse charge regardless.

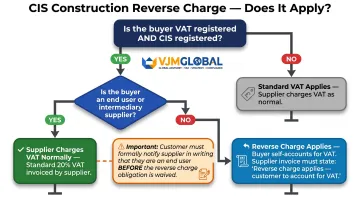

Reverse Charge for Construction Services

Since 1 March 2021, a domestic reverse charge applies to construction services within the scope of the Construction Industry Scheme (CIS). The buyer (main contractor), registered for both VAT and CIS, accounts for VAT instead of the subcontractor.

The reverse charge only applies when the buyer is not an "end user." End users are VAT and CIS-registered businesses that use the building for their own purposes — they don't make onward supplies of the construction services. Where the buyer qualifies as an end user, the supplier charges VAT normally.

The customer must notify the supplier in writing that they are an end user before the supplier can stop applying the reverse charge. Without that written notification in place, the customer remains liable for accounting for the VAT themselves.

How to Account for Reverse Charge VAT on Your UK VAT Return

Under reverse charge, the customer simultaneously records output tax (as if they had sold the supply) and input tax (as the buyer). For fully taxable businesses, the net effect is zero — but both entries are mandatory. Partial exemption rules can result in an actual VAT cost if the service is used for exempt activities.

VAT Return Box Entries

The exact boxes you complete depend on the type of reverse charge:

| Scenario | Box 1 | Box 4 | Box 6 | Box 7 |

|---|---|---|---|---|

| International services (customer) | Output VAT | Input VAT | Value of supply | Purchase value |

| Domestic goods/construction (customer) | Output VAT | Input VAT | — | Purchase value |

The key distinction: for overseas services, you complete Box 6 (value of the deemed supply, as you're stepping into the supplier's shoes). For domestic reverse charge and construction, Box 6 is left blank by the customer — the supplier reports that figure instead.

Worked Example: Overseas Software Purchase

A UK marketing agency receives a £10,000 invoice for software licences from a US provider. No UK VAT appears on the invoice.

Calculation:

- Net value: £10,000

- UK VAT at 20%: £2,000

VAT return entries:

- Box 1 (output tax): £2,000

- Box 4 (input tax): £2,000

- Box 6 (value of supply): £10,000

- Box 7 (purchase value): £10,000

Tax point: The invoice date, not the payment date — even if you use cash accounting. Reverse charge supplies are excluded from the Cash Accounting Scheme.

Postponed VAT Accounting for Imported Goods

Since 1 January 2021, UK importers can elect to use postponed VAT accounting (PVA) instead of paying import VAT at the border. This requires:

- UK VAT registration

- An EORI number

- Using the CHIEF or CDS customs system

The effect mirrors reverse charge accounting: VAT appears in Boxes 1 and 4, with the import value in Box 7. This avoids tying up cash at the border while waiting to reclaim it — see HMRC's guidance on postponed VAT accounting for eligibility details.

Interaction with Accounting Schemes

Reverse charge transactions sit outside the main VAT accounting schemes:

- Excluded from the Flat Rate Scheme — report them separately under standard rules

- Cannot use the Cash Accounting Scheme — the invoice date always applies

- Standard reverse charge rules apply regardless of which scheme your business otherwise uses

Reverse Charge VAT Invoice Requirements

A supplier must include on a reverse charge invoice:

- The net amount (no VAT charged)

- The VAT amount the customer must self-account for (shown separately, not in the total VAT charged box)

- A clear statutory reference

HMRC accepts any of the following phrasings:

- "Reverse charge: Customer to pay the VAT to HMRC"

- "VAT Act 1994 Section 55A applies"

- "S55A VATA 94 applies"

Buyer Responsibilities

Even if the supplier's invoice omits an explicit reverse charge reference, the buyer remains legally responsible for applying it when conditions are met. Ignorance of the supplier's omission is not a defence, so buyers should verify the supplier's VAT registration number before proceeding.

UK businesses with cross-border VAT exposure — particularly those also operating in or entering the Indian market — can benefit from specialist advisory support. VJM Global works with UK-based companies to manage international tax obligations, including the accounting and compliance implications that arise from operating across multiple jurisdictions.

Common Mistakes and Compliance Risks

Not Accounting for Overseas Services at All

The most common mistake: businesses purchasing services from overseas suppliers (SaaS platforms, consultants) simply don't account for the reverse charge. Either the supplier doesn't mention it or the business assumes no UK VAT applies when no VAT appears on the invoice.

HMRC can assess for the unclaimed output tax along with penalties and interest. The buyer cannot argue that they relied on the supplier's invoice silence.

End User Confusion in Construction

Subcontractors and main contractors frequently misidentify end user status. If a contractor treats a job as end-user when the reverse charge should apply (or vice versa), both parties risk incorrect VAT treatment.

Get written confirmation of end user status and keep it on file. HMRC's suggested wording is:

"We are an end user for the purposes of section 55A VAT Act 1994 reverse charge for building and construction services. Issue us with a normal VAT invoice."

Partial Exemption as a Hidden Cost

Businesses that use reverse-charged services partly for exempt activities cannot reclaim the full input tax. The VAT becomes a real cost that is often overlooked in budgeting.

A financial services firm buying overseas software for £50,000 (VAT £10,000) that is 60% exempt can only recover 40% of the input tax — £4,000. The remaining £6,000 is an unrecoverable cost. Before committing to a major overseas service contract, calculate your partial exemption recovery rate so this figure appears in your budget, not as a surprise after the fact.

Frequently Asked Questions

What is the reverse charge in the UK?

UK reverse charge VAT is a mechanism where the buyer rather than the supplier accounts for VAT on certain transactions — covering imported services, specified domestic goods and services, and construction under CIS. The supplier issues a VAT-free invoice while the buyer self-reports VAT on their return.

How to account for reverse charge?

The buyer enters the VAT amount as output tax in Box 1 of the VAT return and reclaims it as input tax in Box 4. The net purchase value goes in Box 7, and for overseas services, also in Box 6. The tax point is the invoice date, not the payment date, even under cash accounting.

Does reverse charge VAT affect my VAT registration threshold?

Yes — the value of overseas services subject to reverse charge counts towards the VAT registration threshold of £90,000. A business making only exempt sales could still be required to register for VAT because of those overseas purchases.

What should a reverse charge invoice include?

The invoice should show the net amount with no VAT charged and include a statutory reference such as "Reverse charge: Customer to pay VAT to HMRC." The buyer's VAT number must also appear on the invoice.

Does reverse charge VAT apply to all construction services?

It applies to CIS construction services where the buyer is VAT and CIS registered and is not the end user. Labour and materials are both covered across 5% and 20% rated supplies, with the rules in force since 1 March 2021.

Can I reclaim reverse charge VAT as input tax?

Fully taxable businesses can reclaim reverse charge VAT in full on the same return it is declared — resulting in net nil VAT. However, partially exempt businesses can only recover the proportion relating to taxable activities, making the unrecoverable portion a real cost.