Georgia's corporate income tax rate dropped again for 2026—and the change is more significant than many businesses have accounted for in their planning. Whether you're already operating in Georgia or evaluating it as an expansion location, the updated rate affects your actual tax liability, your apportionment calculations, and how you model your combined federal-state burden.

Here's what the 2026 rate is, how it was set, and what your business needs to do about it.

Key Takeaways

- Georgia's corporate income tax rate for 2026 is 4.99%, reduced from 5.19% in 2025 under HB 463, signed May 11, 2026

- The rate applies to C corporations on Georgia net taxable income, starting from federal taxable income with Georgia-specific modifications

- Georgia decouples from federal bonus depreciation and One Big Beautiful Budget Act (OBBBA) cost-recovery provisions; plan to model these separately

- Combined with the 21% federal rate, your total statutory burden stays below 26% once Georgia taxes are deducted federally

- Form 600 is due April 15 for calendar-year filers; estimated payments are required when net income is expected to exceed $25,000

Georgia's Corporate Income Tax Rate in 2026: What Changed and Why

The 2026 Rate: 4.99%

Georgia's corporate income tax rate for tax year 2026 is 4.99%—a flat rate applied to all Georgia-sourced net corporate income for C corporations.

Some earlier published tables, including a Tax Foundation data page, listed the 2026 rate as 5.19%. That figure reflected the 2025 rate established by HB 111, which reduced the rate from 5.39% to 5.19% for taxable years beginning on or after January 1, 2025.

Georgia HB 463, signed by Governor Kemp on May 11, 2026, further lowered the rate to 4.99% for taxable years beginning on or after January 1, 2026. Any source still showing 5.19% as the 2026 rate is outdated.

The Phasedown Mechanism

Georgia's rate reductions don't happen automatically. They trace back to HB 1437, the Tax Reduction and Reform Act of 2022, which created a conditional phasedown structure. A scheduled reduction can be delayed if:

- Revenue growth estimates don't meet required thresholds as of December 1

- Prior-year net revenue doesn't exceed the preceding five fiscal years

- The Revenue Shortfall Reserve is insufficient to cover the projected reduction

Businesses should check the Georgia Department of Revenue's annual rate confirmation — typically released before the start of each taxable year — rather than assuming reductions will continue on schedule.

What Didn't Change

HB 463 affected only the income tax rate. The following remain unchanged for 2026:

- No new corporate surcharges or alternative minimum taxes introduced

- No new gross receipts taxes applied to C corporations

- Corporate net worth tax unchanged — still capped at $5,000 for net worth exceeding $22 million

The net worth tax is a separate obligation from corporate income tax and was not modified by HB 463.

How Georgia's 2026 Rate Compares Nationally

Georgia's 4.99% rate positions it well below the national average. According to Tax Foundation 2026 data, among the 44 states levying a corporate income tax:

- Average top marginal rate: ~6.57%

- Median top rate: ~6.5%

Georgia's 4.99% sits roughly 1.5 percentage points below both benchmarks.

States That Cut Rates in 2026

Only four states reduced corporate income tax rates for 2026:

| State | 2026 Rate | Change |

|---|---|---|

| Georgia | 4.99% | Down from 5.19% |

| Nebraska | 4.55% | Reduced |

| North Carolina | 2.0% | Continued phasedown |

| Pennsylvania | 7.49% | Reduced |

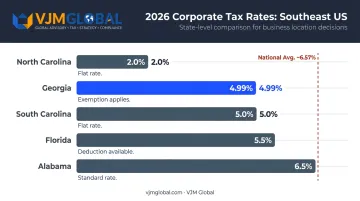

Southeastern State Comparison

For businesses evaluating the Southeast specifically:

| State | 2026 Corporate Rate | Notes |

|---|---|---|

| Georgia | 4.99% | Flat rate, HB 463 |

| North Carolina | 2.0% | Lowest in region |

| South Carolina | 5.0% | Plus corporate license fee |

| Florida | 5.5% | $50,000 exemption applies |

| Alabama | 6.5% | Federal tax deduction allowed |

Zooming out to the full national picture, Georgia's rate holds up well. South Dakota and Wyoming impose no corporate income tax at all, while Nevada, Ohio, Texas, and Washington use gross receipts taxes instead — a different model that taxes revenue rather than profit, meaning even unprofitable businesses owe a liability. For companies that carry losses or operate on thin margins, Georgia's income-based flat rate is often the more predictable option.

How Georgia Corporate Income Tax Is Calculated

Starting Point: Federal Taxable Income

Georgia corporate income tax starts with federal taxable income, then applies state-specific additions and subtractions.

Common additions to Georgia taxable income include:

- State and municipal bond interest (non-Georgia)

- Net income taxes paid to other jurisdictions

- Federal net operating loss (NOL) deducted federally

- Intangible expenses and related interest

- Captive REIT expenses

Common subtractions include:

- Interest on US government obligations

- Certain Georgia municipal bond interest

- Federally disallowed wages tied to federal jobs tax credits

Apportionment: How Georgia Taxes Multi-State Businesses

If your corporation operates in multiple states, you don't pay Georgia tax on all your income—only the portion apportioned to Georgia. Georgia uses a single-sales-factor apportionment formula for most businesses, meaning:

Georgia apportioned income = Total income × (Georgia sales ÷ Total sales)

Companies with heavy Georgia production or payroll but few in-state sales benefit most from this formula. A company generating $10 million of income but with only 20% of sales in Georgia would apportion $2 million to Georgia—resulting in roughly $99,800 of Georgia corporate income tax at 4.99%.

Nexus matters too. Your corporation must have sufficient connection with Georgia before state income tax applies. Physical presence—an employee, office, or property in Georgia—generally creates nexus. Economic nexus can also apply for companies without a physical footprint but with meaningful Georgia sales activity.

Public Law 86-272 provides limited protection for companies whose only Georgia activity is soliciting orders for tangible personal property. That protection doesn't extend to service businesses.

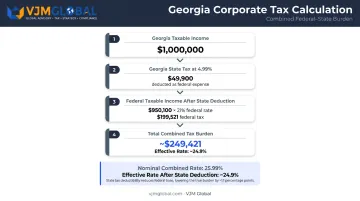

Calculating the Combined Federal-State Burden

Once you've determined Georgia apportioned income, the next step is understanding your true combined tax load. The federal corporate rate is 21% (established under TCJA; HB 463 and the One Big Beautiful Bill Act of 2025 did not change this). Stacking Georgia's 4.99% gives a nominal combined rate of 25.99%, but that's not your actual burden.

State income taxes are deductible for federal purposes, which reduces the effective combined rate. A simple illustration:

- $1,000,000 of Georgia taxable income

- Georgia tax: $49,900 (4.99%)

- Federal taxable income after state deduction: $950,100

- Federal tax at 21%: $199,521

- Total combined tax: ~$249,421, or ~24.9% effective rate

The actual number depends on your full tax profile. The true blended burden is noticeably lower than 25.99%.

Georgia's Decoupling from Federal Cost Recovery

This is where Georgia compliance gets complicated for 2026. HB 1199, signed March 20, 2026, updated Georgia's IRC conformity date to federal law enacted on or before January 1, 2026. Despite that updated conformity, Georgia explicitly decouples from:

- Federal bonus depreciation under IRC Section 168(k) and the new Section 168(n) created by OBBBA

- OBBBA's Section 174A R&E provisions (Georgia maintains pre-TCJA Section 174 treatment, allowing immediate deduction of research and experimental expenditures)

If your business claimed 100% bonus depreciation federally under OBBBA, you'll need to compute depreciation separately on your Georgia return. This creates a timing difference that can increase Georgia taxable income relative to federal taxable income. Model it before filing, not after.

Georgia Corporate Tax Filing Requirements and Deadlines

Form 600: Key Dates

C corporations file Form 600 (Georgia Corporation Tax Return). Critical dates for calendar-year filers:

| Obligation | Due Date |

|---|---|

| Annual return (Form 600) | April 15 |

| Extension (7-month, with federal Form 7004) | November 15 |

| Q1 estimated payment | April 15 |

| Q2 estimated payment | June 15 |

| Q3 estimated payment | September 15 |

| Q4 estimated payment | December 15 |

Important: An extension to file is not an extension to pay. Any tax owed must be paid by April 15 using Form IT-560C. Filing late without payment triggers a 5% penalty per month, up to 25% of unpaid tax; late payment separately carries a 0.5% monthly penalty, up to 25%.

Estimated Tax Threshold

Estimated quarterly payments are required when a corporation's net income is reasonably expected to exceed $25,000 for the year. Underpayment carries a 5% penalty plus a 9% per annum charge, making accurate quarterly estimates worth the effort.

Common Compliance Risks

- Incorrect sales factor calculations trigger apportionment audits more than any other filing issue

- Federal bonus depreciation add-backs are missed when businesses don't adjust for Georgia's decoupling rules

- Unexpected revenue growth mid-year leads to estimated tax shortfalls and automatic penalties

- Federal audit adjustments require amended Form 600 filings — a step many businesses overlook entirely

Multi-state and cross-border structures add another layer of complexity — Georgia obligations don't exist in isolation from federal returns or other state filings. VJM Global's CPAs support businesses with multi-jurisdiction compliance, including apportionment modeling and state filing coordination across all 50 states.

Tax Planning Considerations for Georgia Businesses

Entity Structure Matters

Georgia corporate income tax at 4.99% applies to C corporations only. Pass-through entities—S corporations, partnerships, and LLCs taxed as partnerships—generally don't pay Georgia corporate income tax at the entity level. Income flows to owners' individual returns instead.

When does a C-corp structure make sense despite the entity-level tax?

- When retaining earnings for reinvestment (avoiding immediate pass-through taxation on undistributed profits)

- When accessing corporate-level deductions and benefits unavailable to pass-throughs

- When institutional investors or equity structures require a C-corp

- When the business is headed toward an acquisition or IPO

OBBBA Federal Changes and Georgia Impact

Georgia's fixed-date conformity means businesses need to model two separate depreciation and R&E schedules for 2026:

| Treatment | Federal (OBBBA) | Georgia |

|---|---|---|

| Bonus Depreciation | 100% | Not allowed |

| R&E Expenditures | Section 174A (amortized) | Pre-TCJA Section 174 (immediate expensing) |

For R&E-heavy businesses, this split works in Georgia's favor. Georgia's immediate deduction of research expenditures can produce lower Georgia taxable income than the federal figure—worth modeling before filing.

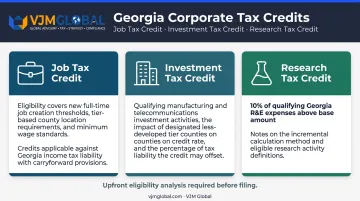

Georgia Tax Credits Worth Modeling

Beyond the depreciation and R&E adjustments, three credits can materially reduce your Georgia corporate income tax liability:

- Job Tax Credit — Available to businesses creating qualifying jobs in eligible industries and locations; credits can offset corporate income tax and, in some cases, withholding tax obligations

- Investment Tax Credit — For qualifying capital investment activities; eligibility varies by type of investment and location within Georgia

- Research Tax Credit — 10% of additional Georgia research expenses above a base amount; requires documented Georgia research spend and statutory eligibility review

These credits require upfront eligibility analysis—industry classification, job count, investment type, and Georgia-specific research spend all factor in. Running the numbers before filing, rather than after, is where the planning value lies.

Frequently Asked Questions

What is Georgia's corporate tax rate?

Georgia's corporate income tax rate for 2026 is 4.99%—a flat rate applied to all Georgia net taxable income for C corporations. This was reduced from 5.19% in 2025 under HB 463, signed May 11, 2026.

How much is $100,000 taxed in Georgia?

A C corporation with $100,000 of Georgia net taxable income owes approximately $4,990 in Georgia corporate income tax at the 2026 rate of 4.99%, before any applicable credits. Federal tax is calculated separately on the corporation's total taxable income.

What was Georgia's corporate tax rate in 2025?

Georgia's corporate income tax rate for tax year 2025 was 5.19%, set by HB 111. Prior to HB 111, the baseline rate was 5.39%—the 2026 reduction to 4.99% under HB 463 continues the legislatively triggered phasedown.

When is Georgia corporate tax due in 2026?

For calendar-year corporations, Form 600 is due April 15, 2026, with a 7-month extension available if a federal extension (Form 7004) is filed. Estimated quarterly payments are due April 15, June 15, September 15, and December 15.

Does Georgia have a combined federal and state corporate tax rate?

Georgia's 4.99% stacks on top of the federal 21% rate, but state taxes are deductible federally, so the true blended burden falls below the nominal 25.99% sum. The effective combined rate depends on your specific income profile and deductions. Model your effective rate before finalizing your tax provision.

Are pass-through businesses subject to Georgia corporate income tax?

Pass-through entities—S corporations, partnerships, and LLCs—don't pay Georgia corporate income tax at the entity level; that obligation falls on C corporations. Owners of pass-throughs pay Georgia individual income tax on their allocated share of business income.