Introduction: Cost Audit in India — A Compliance Priority for Singapore Businesses

Imagine this scenario: A Singapore-headquartered manufacturing company establishes a subsidiary in India, scales operations successfully, crosses ₹50 crore in annual turnover — and suddenly finds itself subject to mandatory cost audit requirements. For Singapore finance teams used to straightforward statutory audits under the Companies Act (Cap. 50), there is no equivalent framework back home — and missing this obligation triggers fines, officer liability, and filing penalties.

Cost audit in India is mandated under Section 148 of the Companies Act, 2013, alongside the Companies (Cost Records and Audit) Rules, 2014. Foreign-owned entities incorporated in India — including wholly-owned Singapore subsidiaries, joint ventures, and private limited companies — are not exempt simply because their parent company is based overseas.

According to the Department for Promotion of Industry and Internal Trade (DPIIT), Singapore remains India's second-largest FDI source, with cumulative equity inflows of USD 171.92 billion (23.87% of total FDI) as of December 2024. A significant share of these investments sits in cost-audit-applicable sectors: telecommunications (5%), construction and infrastructure (8%), and manufacturing.

This guide covers what cost audit is, which Singapore businesses operating in India are affected, sector applicability, exemptions, the filing process, and penalties for missing deadlines — so Singapore parent companies can manage this India-specific obligation before it becomes a liability.

TLDR:

- Cost audit is a mandatory Indian compliance requirement separate from the standard financial audit

- Applies to Indian subsidiaries of Singapore companies once sector and turnover thresholds are met

- Only ICMAI-registered Cost Accountants can conduct cost audits — CAs are not eligible

- Non-compliance triggers company fines up to ₹5,00,000, officer fines up to ₹1,00,000, and ₹1,000/day in continuing penalties

- Telecommunications, electricity, pharmaceuticals, chemicals, and construction sectors are most commonly affected

What is Cost Audit in India — And How Is It Different from Singapore's Audit Requirements?

If your Singapore business has an Indian subsidiary in manufacturing, pharma, or infrastructure, Indian law may require more than a standard financial audit. Cost audit is a separate, mandatory examination of a company's cost accounting records (materials, labour, and overheads) to verify accuracy and compliance with cost accounting standards prescribed by the Ministry of Corporate Affairs (MCA).

The legal foundation rests on Section 148 of the Companies Act, 2013, which empowers the Central Government to mandate cost audits for specific classes of companies. This is separate from the statutory financial audit all companies undergo under Section 143.

For Singapore readers, here's the key distinction:

Singapore's Companies Act requires a standard financial/statutory audit for most companies. India's cost audit is an additional, industry-specific layer focused on production and service cost structures, not financial statement accuracy. This is a compliance dimension Singapore finance teams often miss when managing Indian subsidiaries remotely.

| Aspect | Financial Audit (Both Countries) | Cost Audit (India Only) |

|---|---|---|

| Focus | Accuracy of financial statements | Verification of cost accounting records (materials, labour, overheads) |

| Conducted By | Chartered Accountant | Cost Accountant (ICMAI member with Certificate of Practice) |

| Regulatory Authority | MCA / ACRA (Singapore) | Ministry of Corporate Affairs (India) |

| Forms Filed | Annual returns, director's report | CRA-2, CRA-3, CRA-4 |

| Applicability | Nearly all companies | Sector-specific with turnover thresholds |

One restriction Singapore finance teams frequently overlook: Section 148(3) bars any person appointed as statutory auditor under Section 139 from also serving as cost auditor. Your existing Chartered Accountant cannot fulfil both roles. Companies must separately engage a Cost Accountant in Practice registered with the Institute of Cost Accountants of India (ICMAI).

Why the Indian Government Mandates Cost Audits

Cost audits serve multiple policy purposes:

- Price monitoring in regulated industries: The government tracks pricing in pharmaceuticals, telecommunications, and electricity generation to protect consumers

- Tender integrity: Cost audits detect inflated cost claims in government contracts, ensuring fair pricing for public sector procurement

- Transparency in strategic sectors: Industries with significant public interest (fertilizers, petroleum) undergo cost scrutiny to prevent market manipulation

For Singapore businesses, these objectives have direct operational consequences. Cost audit findings can affect your Indian subsidiary's pricing in regulated markets, its eligibility for government tenders, and its exposure to regulatory review — all areas where non-compliance carries penalties beyond a simple filing fine.

Which Singapore-Owned Businesses in India Must Get a Cost Audit Done?

The obligation applies to companies incorporated in India — including wholly-owned subsidiaries, joint ventures, and private limited companies with Singapore parent companies — if they meet the applicability criteria under Rule 4 of the Companies (Cost Records and Audit) Rules, 2014.

Two-step test for cost audit applicability:

- The company's products or services must fall under the sectors listed in Table A (Regulated) or Table B (Non-Regulated) of the Rules

- The company must cross the relevant turnover thresholds based on its sector classification

Turnover threshold criteria:

For Regulated Sectors (Table A):

- Overall annual turnover ≥ ₹50 crore AND

- Aggregate turnover of the specific product/service requiring cost records ≥ ₹25 crore

For Non-Regulated Sectors (Table B):

- Overall annual turnover ≥ ₹100 crore AND

- Aggregate turnover of the specific product/service requiring cost records ≥ ₹35 crore

Before the cost audit threshold applies, there's a baseline obligation: companies in notified sectors with overall turnover of ₹35 crore or more in the immediately preceding financial year must begin maintaining cost records in CRA-1 format. Singapore businesses should set this up before turnover hits ₹35 crore — not after.

Timing matters: Both thresholds are assessed against the immediately preceding financial year's turnover. A Singapore-owned entity that scaled up quickly in India can cross into cost audit territory without any formal government notice. Track your India subsidiary's turnover against these thresholds at the close of each financial year — particularly as operations approach the ₹50–100 crore range.

Sectors That Trigger Cost Audit: Where Most Singapore Businesses in India Operate

Table A (Regulated Sectors)

Six regulated sectors commonly involve Singapore investments in India:

- Telecommunications services

- Generation, transmission, distribution, and supply of electricity

- Petroleum products

- Drugs and pharmaceuticals

- Fertilizers

- Sugar and industrial alcohol

Real-world example: Sembcorp Industries Ltd — Singapore-headquartered and SGX-listed — operates in India's electricity generation sector through subsidiaries including Sembcorp Green Infra Limited. With more than 7.6 GW of power assets across 13 Indian states as of May 2025, it falls squarely within Table A cost audit requirements.

Bharti Airtel (Telecommunications — Table A) is another example, receiving significant FDI from Singapore through major shareholder Singtel, placing it under the same obligations.

Table B (Non-Regulated Sectors)

Table A captures the most heavily regulated industries, but Table B casts a wider net. Thirty-three product and service categories fall within its scope, including those most relevant to Singapore manufacturers and service providers:

- Chemicals (inorganic, organic, precious metals)

- Plastics and polymers

- Electrical or electronic machinery

- Iron and steel

- Textiles

- Cement

- Construction industry

- Health services

- Education services

- Rubber and allied products

- Machinery and mechanical appliances

Two points from Table B are worth calling out for Singapore businesses specifically:

- Service industries now included — Health services, education, and infrastructure projects fall under cost audit rules. Singapore-based companies operating in healthcare, ed-tech, or consulting in India should review their exposure.

- Trading companies are excluded — Entities that only buy and sell goods (without manufacturing or notified services) are generally not covered. This is a common source of confusion for Singapore businesses running India trading subsidiaries.

Exemptions from Cost Audit: When Singapore Businesses May Not Need to Comply

The Companies (Cost Records and Audit) Rules, 2014 include four exemptions that can relieve eligible companies from mandatory cost audit. Understanding these matters early — the right structure can determine whether your India subsidiary faces this obligation at all.

The four exemption categories are:

Export Revenue (75%+ Rule): Entities whose foreign exchange export revenue exceeds 75% of total revenue are exempt. This applies directly to Singapore businesses running export-oriented units in India that primarily serve international markets.

Special Economic Zone (SEZ) Units: Operations conducted entirely within an SEZ are excluded from mandatory cost audit. Many Singapore investors structure their India entry through SEZ units to take advantage of this and related tax benefits.

Captive Power Generation: Entities generating electricity solely for their own consumption through a Captive Generating Plant are exempt — relevant for energy-intensive manufacturing subsidiaries.

MSME Classification (Micro or Small): Entities classified as micro or small enterprises under the MSME Development Act, 2006 are exempt from mandatory cost audit.

Revised MSME thresholds (effective April 2025):

According to the Union Budget 2025-26, the government doubled MSME turnover thresholds:

| Category | Previous Turnover Limit | New Turnover Limit (2025) |

|---|---|---|

| Micro Enterprise | Up to ₹5 crore | Up to ₹10 crore |

| Small Enterprise | Up to ₹50 crore | Up to ₹100 crore |

| Medium Enterprise | Up to ₹250 crore | Up to ₹500 crore |

Impact for Singapore businesses: More Indian subsidiaries may now qualify as micro or small enterprises and therefore be exempt from cost audit. Singapore-backed startups or smaller Indian entities should verify their MSME classification status at the start of each financial year.

Annual review is essential. Turnovers shift, export ratios fluctuate, and entity classifications can change — an exemption that applied last year may not apply this year. Singapore parent companies should build this eligibility check into their annual India compliance calendar. VJM Global supports foreign-owned businesses with exactly this kind of structured annual review as part of ongoing India compliance management.

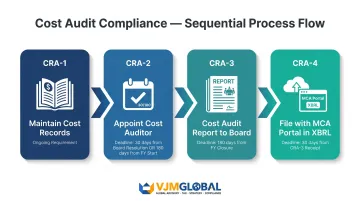

The Cost Audit Process: Key Forms and Deadlines Indian Subsidiaries Must Follow

Four key compliance forms must be filed in sequence:

1. CRA-1 (Cost Records Maintenance): Prescribed format for maintaining cost records in the company's books — an ongoing obligation, not a one-time filing.

2. CRA-2 (Appointment of Cost Auditor): Filed within 30 days of the Board resolution appointing the cost auditor OR within 180 days of the start of the financial year, whichever is earlier.

3. CRA-3 (Cost Audit Report): Cost auditor submits the audit report to the Board of Directors within 180 days from financial year closure.

4. CRA-4 (Filing with MCA): Company files the cost audit report with the MCA within 30 days of receiving the CRA-3 report. Must be filed via the MCA V3 portal in XBRL format.

| Form | Purpose | Deadline |

|---|---|---|

| CRA-2 | Intimation of cost auditor appointment | 30 days from Board resolution or 180 days from FY start (whichever earlier) |

| CRA-3 | Cost audit report to Board | 180 days from FY closure |

| CRA-4 | Filing cost audit report with MCA | 30 days from receipt of CRA-3 |

Auditor Qualification Requirement

Only a Cost Accountant in Practice — a member of the Institute of Cost Accountants of India (ICMAI) with a valid Certificate of Practice — can be appointed as cost auditor. A Chartered Accountant or Singapore-qualified auditor cannot fulfil this role under Section 2(28) of the Companies Act, 2013.

Technical Challenges for Remote Management

Singapore finance teams managing India subsidiaries remotely often encounter delays due to unfamiliarity with:

- The MCA V3 portal

- XBRL format requirements for CRA-4

- Digital Signature Certificate (DSC) procurement for authorized signatories

Working with an India-based compliance partner like VJM Global helps Singapore businesses stay on top of CRA-2 to CRA-4 deadlines — including coordination with ICMAI-qualified cost auditors and end-to-end MCA portal filing — without pulling focus from core operations.

Note that MCA General Circular No. 07/2025 (dated 27 October 2025) extended the CRA-4 filing deadline for FY 2024-25 to 31 December 2025, with no additional fees for timely filings.

Penalties for Non-Compliance: What Singapore Businesses Risk

Statutory penalty framework under Section 147:

| Defaulter | Provision | Fine Range |

|---|---|---|

| Company | Section 147(1) | ₹25,000 to ₹5,00,000 |

| Officer in default | Section 147(1) | ₹10,000 to ₹1,00,000 |

| Cost auditor | Section 147(2) | ₹25,000 to ₹5,00,000 (or 4x remuneration, whichever less) |

Continuing default penalties (Section 450):

- Initial penalty of ₹10,000 plus ₹1,000 per day after the first day of default

- Maximum: ₹2,00,000 for the company; ₹50,000 for an officer in default

Fines are the most visible consequence — but the business fallout can run deeper.

Operational consequences beyond statutory fines:

Tender eligibility at risk: No single law automatically bars non-compliant companies from government contracts, but bid documents increasingly make cost audit compliance a direct eligibility requirement. A GeM portal bid document (March 2026) explicitly required Section 148 compliance — meaning non-compliant subsidiaries may simply not qualify to bid.

MCA scrutiny that stalls growth: Non-compliance flags a company for regulatory review, which can delay approvals for fundraising rounds, IPOs, or expansion filings — creating timeline risks that Singapore parent companies rarely anticipate.

Personal exposure for Singapore-appointed directors: Individual directors and officers face personal fines and potential disqualification under Indian law. For Singapore executives sitting on Indian subsidiary boards, this is a direct personal liability — not just a company-level compliance gap.

If your Indian subsidiary triggers an MCA review during a capital raise or acquisition, the compliance gap becomes a deal risk. Address cost audit obligations before they surface in due diligence.

Frequently Asked Questions

Who can do a cost audit in India?

Only a Cost Accountant in Practice — an individual or firm holding a valid Certificate of Practice from the Institute of Cost Accountants of India (ICMAI) — can be appointed as a cost auditor. The company's existing statutory financial auditor (Chartered Accountant) cannot serve in this dual role.

Are MSMEs exempted from cost audit in India?

Yes. Companies classified as micro or small enterprises under the MSME Development Act, 2006 are exempt from mandatory cost audit requirements, even if their products/services fall under notified sectors. As of April 2025, small enterprises are defined as those with turnover up to ₹100 crore.

Does cost audit apply to foreign companies and their Indian subsidiaries?

Yes. Cost audit obligations apply to companies incorporated in India, which includes Indian subsidiaries of foreign companies (including Singapore businesses). The country of the parent company does not grant an exemption; applicability is determined by sector and turnover thresholds.

Is cost audit in India the same as the financial audit Singapore businesses are familiar with?

No. Financial audit examines financial statements for accuracy and is conducted by a Chartered Accountant. Cost audit examines cost accounting records (materials, labour, overheads) and must be conducted by a Cost Accountant. Both may be required simultaneously for eligible Indian companies.

What happens if a Singapore company's Indian subsidiary misses the cost audit deadline?

Late filing attracts daily penalties of ₹1,000 per day (capped at ₹2,00,000 for the company). Continued non-compliance can lead to fines on the company and its officers, director disqualification risks, and exclusion from government tenders..

Can a company operating in an Indian SEZ skip cost audit compliance?

Yes. Companies operating entirely within a Special Economic Zone are exempt from the mandatory cost audit requirement under the Companies (Cost Records and Audit) Rules, 2014 — so Singapore businesses that have structured their India presence through SEZ units are not subject to this requirement.

Need help with cost audit compliance for your Indian subsidiary? VJM Global specializes in helping Singapore businesses navigate India's cost audit requirements — from cost record maintenance and auditor appointment to CRA-4 filing and MCA compliance. With 30+ years of experience serving 1,000+ foreign-owned businesses across USA, UK, Australia, and beyond, we ensure your India operations stay compliant while you focus on growth. Contact us at info@vjmglobal.com or call +91-9213397070.