Introduction

When a Singapore company transacts with its Indian subsidiary or associated enterprise (AE) — supplying goods, receiving services, or transferring semi-finished products — India's transfer pricing law requires these transactions to be priced at arm's length. The Cost Plus Method (CPM) is one of the most commonly applied methods to achieve this compliance under Section 92C of India's Income Tax Act.

This guide is written for Singapore-based CFOs, tax managers, and business owners with Indian operations. Many companies apply CPM — prescribed under Rule 10B(1)(c) of the Income Tax Rules — without fully understanding how the markup is calculated or which costs belong in the base.

That gap creates real exposure. Misapplication leads to tax adjustments, prolonged disputes with Indian authorities, and potential double taxation that could have been avoided with the right approach upfront.

Key Takeaways

- CPM determines arm's length pricing by adding a gross profit markup to the cost of production or service delivery in controlled (inter-company) transactions

- Governed by Section 92C of India's Income Tax Act; most suitable for routine manufacturing, service provision, semi-finished goods transfer, and long-term supply arrangements

- Follows a four-step process: identify costs → determine comparable markup → adjust for functional differences → compute the arm's length price

- Key pitfalls: wrong cost base selection, inappropriate markup percentages, and applying CPM where significant intangibles are involved

- Annual documentation is mandatory for international transactions exceeding INR 1 crore — Form 3CEB applies for AY 2024-25, with Form 48 replacing it from FY 2026-27, backed by independent benchmarking studies

What Is the Cost Plus Method in Transfer Pricing?

The Cost Plus Method (CPM) is a traditional transaction method under India's transfer pricing framework. It calculates the arm's length price (ALP) by adding a gross profit markup to the costs incurred by the supplier in a controlled transaction.

Core formula: ALP = Cost of Production + (Cost of Production × Appropriate Gross Profit Markup %)

When an Indian entity supplies goods or services to its Singapore associated enterprise (AE), CPM ensures the profit retained by the Indian entity matches what an independent party would have earned in a comparable deal. This directly addresses profit shifting and tax base erosion — the two concerns driving India's stringent transfer pricing rules.

How CPM differs from related methods:

- Comparable Uncontrolled Price (CUP) looks at the final transaction price; CPM focuses on the seller's cost and margin instead

- Transactional Net Margin Method (TNMM) works at the net operating margin level; CPM operates at gross profit, making it more sensitive to how costs are classified and recorded

The OECD Transfer Pricing Guidelines 2022 classify CPM as a traditional transaction method under Chapter II (paragraphs 2.45–2.61). For Singapore companies, this means a CPM-based structure in India is defensible not just under Indian tax law but also against any OECD-aligned challenge from the Singapore side.

Why Singapore Companies with Indian AEs Use CPM

Typical Transaction Patterns

Singapore companies commonly establish Indian subsidiaries to perform:

- Routine manufacturing or contract manufacturing

- IT and business process outsourcing (BPO) services

- Software development under cost-plus contracts

- Transfer of semi-finished goods for further processing

- Long-term supply arrangements with limited market risk

These functional profiles share common characteristics: the Indian entity operates with limited risk, does not own significant intangibles, and functions primarily as a service provider or routine manufacturer. Because the Indian AE's contribution is cost-driven rather than value-driven, CPM's markup-on-costs framework benchmarks the arrangement accurately.

Regulatory Alignment

That functional profile creates a direct compliance obligation. Under Section 92C, India requires every international transaction to be benchmarked against arm's length conditions — and CPM addresses this requirement effectively when:

- The Indian entity maintains reliable cost accounting data

- Comparable uncontrolled transactions exist (internal comparables with third-party customers or external comparables from databases)

- The transaction involves routine functions without unique value creation

CPM is recognised under both India's domestic rules and the OECD Guidelines, which allows Singapore companies to maintain consistent global TP policies without reconciling conflicting standards. India requires the Most Appropriate Method (MAM) to be selected based on six factors prescribed in Rule 10C — and CPM is the MAM most commonly applied to manufacturing and routine service transactions.

How CPM Works Under India's Transfer Pricing Rules

Conceptual Overview

CPM starts with the Indian AE's verifiable cost base for a controlled transaction, benchmarks the gross profit markup against comparable uncontrolled transactions, adjusts for functional or risk differences, and arrives at the ALP. The result is compared to the actual price charged; any shortfall triggers a transfer pricing adjustment and potential tax liability.

Internal vs. External Comparables:

- Internal comparables are the most reliable: the Indian subsidiary sells the same or similar goods/services to unrelated customers at a known margin

- External comparables are drawn from databases such as Prowess (CMIE) or Capitaline for Indian companies, where the functional profile must be closely matched

Under Rule 10B(1)(c), the markup is a gross profit markup — calculated on the cost base, not revenue. Consistency in cost accounting between the tested party and comparables is critical; even minor differences in overhead allocation can distort results.

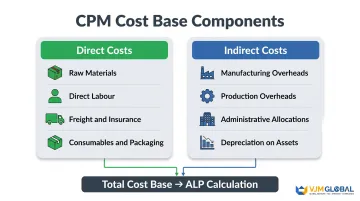

Step 1: Identify Direct and Indirect Costs of Production

Determine all costs incurred by the Indian AE for the controlled transaction:

Direct costs:

- Raw materials and components

- Direct labour (including provident fund, gratuity)

- Freight and insurance directly attributable to production

- Consumables and packaging materials

Indirect costs:

- Manufacturing overheads (factory rent, depreciation, utilities)

- Production overheads (quality control, indirect labour)

- Administrative allocations (management salaries, office expenses, IT costs)

- Depreciation on production assets

Costs should relate specifically to goods transferred or services provided to the Singapore AE. India's tax authorities scrutinise cost exclusions and unusual allocations closely: particularly headquarters allocation charges from Singapore, R&D expenses, and shared service costs.

Step 2: Determine the Normal Gross Profit Markup from Comparable Transactions

Identify a normal gross profit markup using:

- Internal comparables (preferred): The Indian entity's own transactions with unrelated parties for similar goods or services — these provide the strongest benchmark and are given priority by Indian tax authorities

- External comparables: Publicly available data from unrelated enterprises in similar industries, filtered for functional similarity (FAR analysis), turnover and employee cost thresholds, export intensity, related party transaction filters, and current year financial data

The markup must reflect functions performed, assets used, and risks assumed. The OECD Guidelines emphasise that comparability adjustments should account for material differences affecting gross profit margins.

Step 3: Adjust for Functional and Other Differences

Adjust the normal markup for differences between the controlled transaction and comparables that could materially affect the gross profit margin.

Common adjustments in Singapore-India contexts:

- Differences in payment terms or credit periods

- Volume discounts or rebate structures

- Additional services bundled into the transaction

- Technology support or training provided by the Singapore parent

- Geographic market differences

Adjustments should only be made where the difference is material and quantifiable. Each adjustment must be supported by documentation — financial statements, invoices, or third-party benchmarks — that survives TPO scrutiny during assessment proceedings.

Step 4: Compute the Arm's Length Price

Increase the cost base (Step 1) by the adjusted markup (Step 3) to arrive at the ALP. Compare this to the price actually charged.

Tolerance band (current regime):

- Wholesale trading: ±1% (where purchase cost ≥80% of total cost and inventory ≤10% of sales)

- All other transactions: ±3%

If the actual price falls within the tolerance band, no adjustment is made. If it falls outside, the difference represents taxable income that India's tax authorities may add back — triggering potential tax liability and penalties.

The tolerance band was confirmed by CBDT Notification No. 116/2024 for AY 2024-25 and maintained for FY 2025-26, providing stable planning parameters.

Key Factors Affecting CPM Application for Singapore-India Transactions

Cost Base Consistency

One of the biggest risks is using different cost accounting standards or allocation methodologies compared to external comparables. Indian entities prepare financial statements under Ind AS (Indian Accounting Standards). Mismatches in how overhead is allocated — or whether finance costs are included in the cost base — can distort markup comparisons.

Ensure the Indian AE maintains detailed cost accounting records that align with the methodology used in selecting external comparables.

Availability and Quality of Comparables

CPM's reliability depends on whether genuine comparable transactions exist.

Internal comparables (where the Indian AE sells the same product to both the Singapore parent and independent customers) are far stronger than external comparables. When using external databases like Prowess or Capitaline, ensure:

- Functional profiles match closely (routine manufacturing/services, limited risk)

- Financial data is current (Indian authorities prefer current year data)

- Quantitative filters are appropriate (turnover, employee cost ratios, export intensity)

- Loss-making companies are excluded with justification

No specific CBDT circular prescribes minimum comparability criteria; these are derived from ITAT jurisprudence and TPO practice.

Functional Analysis (FAR Analysis)

CPM is most defensible when the Indian entity performs routine functions with limited risk. If the Indian entity takes on significant market risk, holds valuable IP, or makes strategic decisions, the functional profile becomes too complex for CPM and a different method may be required.

TP documentation should include a detailed Functions, Assets, and Risks (FAR) analysis that demonstrates why the Indian entity is appropriately characterised as a routine service provider or manufacturer.

Transfer Pricing Documentation and Form 3CEB

Indian regulations require taxpayers with international transactions above INR 1 crore to maintain contemporaneous TP documentation and obtain Chartered Accountant certification.

| Regime | Form Required | Filing Deadline |

|---|---|---|

| Through AY 2025-26 | Form 3CEB | October 31 of the assessment year |

| From FY 2026-27 onwards | Form 48 (Income-tax Act, 2025) | One month prior to ITR due date |

VJM Global supports Singapore companies through the full TP documentation process, covering functional analysis, benchmarking studies, and Form 3CEB/Form 48 filing to reduce audit exposure.

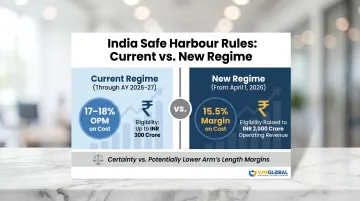

India's Safe Harbour Rules

India offers safe harbour rules that provide certainty without full-scale CPM benchmarking:

Current regime (through AY 2026-27):

- IT/ITES services: 17-18% operating profit margin (OPM) on cost, depending on turnover

- Eligible transactions up to INR 300 crore

New regime (effective April 1, 2026):

- IT/ITES services: uniform 15.5% margin on cost

- Eligibility threshold raised to INR 2,000 crore in operating revenue

Singapore companies receiving IT services from Indian AEs should evaluate whether the new reduced safe harbour margin offers compliance savings compared to full CPM benchmarking. The trade-off is certainty versus potentially lower arm's length margins.

Common Misconceptions, Limitations, and When CPM May Not Apply

Misconception: CPM Works for All Transaction Types

Many Singapore companies assume CPM applies across all inter-company transactions. CPM is inappropriate where:

- The Indian entity owns significant intangibles

- The entity performs non-routine functions (strategic decision-making, R&D ownership)

- The transaction involves unique products with no comparable

In such cases, the Profit Split Method or TNMM may be more appropriate.

Limitation: Subjectivity in Cost Determination

The cost base is not always straightforward. Disputes often arise between Singapore companies and India's Transfer Pricing Officer (TPO) over:

- Headquarters allocation charges from Singapore

- R&D costs (whether product-specific or general)

- Pre-production or setup costs

- Shared service costs

Example: A Singapore parent allocates global IT infrastructure costs to its Indian subsidiary at 8% of the subsidiary's revenue. The TPO may challenge this allocation if the methodology is not clearly documented or if comparable companies do not incur similar charges.

Misconception: The Highest Markup Is Safest

Some companies apply a conservative (high) markup to avoid adjustments. An inflated markup that does not reflect market norms can attract scrutiny from Indian tax authorities and create double taxation risk if Singapore's IRAS takes a different view.

When that happens, companies typically turn to the Mutual Agreement Procedure (MAP) under Article 27 of the India-Singapore DTAA — but MAP is not a quick fix. India had 337 TP MAP cases at the start of 2024, with an average resolution time of 45.73 months for post-2016 cases — nearly four years. Singapore companies are better served initiating an Advance Pricing Agreement (APA) or filing a MAP application proactively, before a dispute escalates, rather than treating it as a fallback.

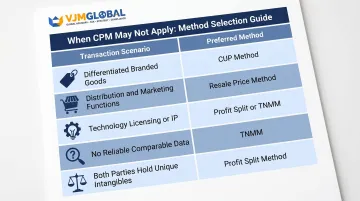

When CPM May Not Apply

| Scenario | Preferred Method |

|---|---|

| Highly differentiated or branded finished goods with unique selling prices | CUP Method |

| Indian entity performs significant distribution and marketing functions | Resale Price Method |

| Technology licensing or IP transfers | Profit Split or TNMM |

| No reliable comparable data exists, and gross margin comparisons would be distorted | TNMM (net margin approach) |

| Both parties contribute unique and valuable intangibles (OECD para 2.65) | Profit Split Method |

The OECD Guidelines (para 2.49) note that CPM breaks down when costs and market price are not meaningfully connected — for example, a pharmaceutical company that makes a high-value drug discovery with minimal R&D expenditure cannot use its low cost base to justify a low arm's length price.

Frequently Asked Questions

What is the Cost Plus Method in transfer pricing?

CPM determines arm's length price by adding a gross profit markup to the supplier's costs in a controlled transaction. It is one of five prescribed methods under Section 92C of India's Income Tax Act, most commonly applied to routine manufacturing and service transactions between associated enterprises.

When should a Singapore company use the Cost Plus Method for transactions with its Indian subsidiary?

CPM is most appropriate when the Indian subsidiary performs routine manufacturing, contract manufacturing, or service functions (such as IT or BPO) without owning significant intangibles or bearing substantial business risk. It also requires that comparable uncontrolled transactions are available to benchmark the markup.

What costs are included in the cost base under India's Cost Plus Method?

The cost base typically includes direct costs (raw materials, direct labour, freight) and indirect costs (manufacturing overheads, allocated administrative expenses, depreciation on production assets). Costs specific to the tested party's controlled transaction should be separately identified from those attributable to third-party sales.

How is the gross profit markup determined for CPM in India?

The markup is drawn from comparable uncontrolled transactions — either internal (the Indian entity's own third-party sales) or external (Prowess or Capitaline databases). These comparables must be adjusted for material functional or risk differences before being applied to the controlled transaction's cost base.

What is the difference between CPM and TNMM for Singapore-India transactions?

CPM benchmarks at the gross profit level using cost markups, making it sensitive to cost accounting consistency. TNMM benchmarks at the net operating margin level and is generally more tolerant of minor cost structure differences, making TNMM more widely used when gross-level comparables are difficult to find.

What documentation does a Singapore company need for transfer pricing compliance in India using CPM?

The Indian AE must maintain contemporaneous TP documentation — covering functional analysis, benchmarking study, and economic analysis — and obtain CA certification in Form 3CEB (through AY 2025-26) or Form 48 (from FY 2026-27 onwards). Documentation must be ready by October 31 (or one month prior to the ITR due date under the new regime).

Need expert assistance with India transfer pricing compliance? VJM Global's international tax team supports Singapore companies with end-to-end TP services: from FAR analysis and benchmarking studies using Prowess and Capitaline databases to Form 3CEB/Form 48 filing and TPO dispute representation. With 30+ years of experience and a dedicated team of Chartered Accountants, we handle India's TP requirements so you can focus on your business. Contact us at info@vjmglobal.com or +91 9213397070.