Introduction

India runs one of the most aggressive transfer pricing regimes in the world. Under Section 92CB of the Income Tax Act, safe harbour rules give taxpayers a statutory mechanism where tax authorities must accept the declared transfer price without further scrutiny — a meaningful compliance guarantee in a jurisdiction where TP disputes are routine.

This guide is written for Singapore companies with Indian subsidiaries, captive service centers, or intercompany arrangements. Singapore is India's largest source of FDI, with USD 14.94 billion invested in FY2024-25 (30% of total inflows) — that scale of investment generates exactly the intercompany transaction volumes these rules are designed to cover.

That FDI exposure also means greater scrutiny. TP audits grew from roughly 1,000 to 4,290 between 2005-06 and 2014-15, with over 50% resulting in adjustments. Safe harbour rules offer a direct compliance shield against that audit intensity.

This article covers what the rules are, which Singapore-India transactions qualify, current margin thresholds, the opt-in process, and the significant changes introduced in March 2025 and proposed for 2026.

Key Takeaways

- Safe harbour lets eligible Indian entities declare a pre-approved transfer price that tax authorities must accept—no full arm's length benchmarking required

- Key categories include IT services, ITeS, KPO, contract R&D, intra-group loans, and low value-adding services—common in Singapore MNE India operations

- CBDT Notification 21/2025 extended safe harbour through FY2025-26, raising the threshold to INR 300 crore (~USD 32 million)

- Union Budget 2026 proposes a unified 15.5% IT services margin, a INR 2,000 crore (~USD 212 million) threshold, and five-year validity

- Electing safe harbour forfeits MAP rights under the India-Singapore DTAA for covered transactions—a trade-off that requires careful evaluation

What Are India's Transfer Pricing Safe Harbour Rules?

Under Section 92CB of the Income Tax Act, safe harbour refers to defined circumstances in which Indian tax authorities must accept the transfer price declared by a taxpayer. This is statutory protection — not a voluntary pricing guideline.

Introduced in September 2013, the rules aim to reduce transfer pricing audits and prolonged disputes by giving qualifying taxpayers a pre-approved margin. This eliminates the need for a full arm's length analysis on routine transactions. For Singapore companies with straightforward intercompany arrangements, the key question is whether safe harbour or an Advance Pricing Agreement (APA) is the right fit.

How Safe Harbour Differs from APAs

| Feature | Safe Harbour Rules | Advance Pricing Agreements |

|---|---|---|

| Structure | Standardized, rule-based | Individually negotiated |

| Process | Self-selectable via form filing | Bilateral negotiation with tax authority |

| Customization | None—fixed margins apply | Tailored to specific transactions |

| Timeline | Immediate (if eligible) | 2-3 years negotiation period |

| Cost | Minimal (form filing only) | INR 10-20 lakh plus professional fees |

| Validity | Annual (current) / 5 years (proposed 2026) | Up to 5 years plus 4-year rollback |

Safe harbour suits companies with standard, high-volume transactions that fall cleanly within the prescribed categories. APAs make more sense when pricing is complex, margins are atypical, or the transaction value justifies a tailored long-term arrangement.

Why Singapore Companies Operating in India Should Care

Why Singapore Companies Operating in India Should Care

Singapore-India Business Flow Scale

Singapore's position as India's top FDI source creates massive intercompany service flows. Cumulative FDI from Singapore stands at USD 174.88 billion, with bilateral trade totaling USD 35.6 billion in FY2024-25.

Many Singapore-headquartered MNEs operate India captives or shared service centers performing:

- Software development and IT services

- Back-office and ITeS operations

- KPO and analytics services

- Contract R&D

These are precisely the transaction types covered by safe harbour rules.

Compliance Burden Without Safe Harbour

Without electing safe harbour, the Indian entity must:

- Annually conduct full benchmarking studies against comparable companies

- Maintain prescribed transfer pricing documentation (local file, master file)

- Obtain Form 3CEB Accountant's Report

- Face transfer pricing audits where officers may recompute taxable income

- Defend pricing through lengthy litigation if adjustments occur

This creates substantial compliance costs and audit exposure.

India-Singapore DTAA Interaction

Safe harbour reduces that compliance burden significantly — but there is a treaty consequence to consider. The India-Singapore Double Taxation Avoidance Agreement provides MAP (Mutual Agreement Procedure) as a dispute resolution mechanism, yet electing safe harbour eliminates MAP access for those transactions.

For companies with straightforward, low-margin service operations, this trade-off typically favors safe harbour. Where transactions are complex or pricing is contestable, preserving MAP rights may be the more defensible position.

Eligible Transactions, Categories, and Margin Thresholds

Safe harbour applies only to specific "eligible international transactions" defined in the rules. Understanding which categories apply to your Indian subsidiary is the first step before electing safe harbour.

Primary Categories for Singapore Companies

Service Transactions:

- IT and software development services: Software development and related technology work performed by the Indian entity

- IT-enabled services (ITeS): Back-office, data processing, customer support exported to overseas parent

- Knowledge Process Outsourcing (KPO): Analytics, research, professional services with graded margin structure

- Contract R&D services: Related to software development or generic pharmaceutical drugs

Financial and Other Transactions:

- Intra-group loans: Foreign currency loans benchmarked to reference rates plus spread; INR loans benchmarked to SBI MCLR plus spread

- Low value-adding intra-group services: HR, finance support, and administration charges billed to the Indian subsidiary

Current Margin Thresholds (FY2024-25 and FY2025-26)

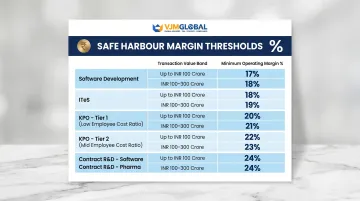

Under CBDT Notification 21/2025 (March 2025), the upper threshold for five service categories increased from INR 200 crore to INR 300 crore (approximately USD 32 million).

Service Transaction Thresholds:

| Category | Transaction Value | Minimum Margin on Operating Costs |

|---|---|---|

| Software Development (insignificant risks) | Up to INR 100 crore | 17% |

| Software Development (insignificant risks) | Above INR 100 crore to INR 300 crore | 18% |

| ITeS (insignificant risks) | Up to INR 100 crore | 17% |

| ITeS (insignificant risks) | Above INR 100 crore to INR 300 crore | 18% |

| KPO (employee cost ≥60% of operating costs) | Up to INR 300 crore | 24% |

| KPO (employee cost 40-60%) | Up to INR 300 crore | 21% |

| KPO (employee cost ≤40%) | Up to INR 300 crore | 18% |

| Contract R&D—Software | Up to INR 300 crore | 24% |

| Contract R&D—Generic Pharma | Up to INR 300 crore | 24% |

Intra-Group Loan Safe Harbour Rates:

| Loan Type | Credit Rating | Safe Harbour Rate |

|---|---|---|

| INR loans | AAA to A | SBI 1-year MCLR + 175 bps |

| INR loans | BBB-, BBB, BBB+ | SBI 1-year MCLR + 325 bps |

| INR loans | No rating (up to INR 100 crore) | SBI 1-year MCLR + 425 bps |

| Foreign currency (up to INR 250 crore) | AAA to A | Reference rate + 150 bps |

| Foreign currency (above INR 250 crore) | BB+ to B- | Reference rate + 450 bps |

Ineligibility Criteria

Even if your transaction falls into an eligible category, safe harbour is denied in the following situations:

- Notified Jurisdictional Areas: Transactions with entities in listed jurisdictions are excluded. No countries are currently listed — Singapore has never appeared on this list.

- Threshold breaches: Transactions exceeding the prescribed INR value limits for each category are ineligible.

- Risk conditions not met: The Indian entity must assume insignificant entrepreneurial risk; entities bearing significant risks do not qualify.

How to Opt Into India's Safe Harbour Rules: The Election Process

Who Makes the Election

The Indian entity (not the Singapore parent) must formally elect to be covered by filing the prescribed form with the assessing officer.

Current Process (AY 2025-26 and AY 2026-27)

Filing requirements:

- Form 3CEFA must be filed by the due date for filing the income tax return

- The taxpayer declares that transactions fall within eligible categories

- Operating margin meets minimum threshold

- Prescribed documentation confirming eligibility is submitted

- Form 3CEB Accountant's Report must be obtained and filed

Key conditions:

- Under Notification 21/2025, single-year elections are permitted (the previous 3-year continuity requirement under Rule 10TE(2) has been waived)

- If facts are misrepresented or information is inaccurate in Form 3CEFA, the election is void ab initio (invalid from the start)

Consequences of Accepted Safe Harbour Election

Once the transfer price is accepted under safe harbour:

- No adjustment can be made by the transfer pricing officer

- MAP is unavailable under the India-Singapore DTAA for those transactions

- No need to maintain comparable company data or justify margin independently

Because MAP is forfeited once safe harbour is elected, Singapore companies should carefully weigh this against APA and MAP alternatives before filing. VJM Global helps Singapore companies assess eligibility, prepare Form 3CEFA, and evaluate the trade-offs between safe harbour, APAs, and MAP across their full India tax position.

Compliance Simplification Benefits

Safe harbour removes much of the documentation overhead associated with full arm's length benchmarking. For Singapore companies managing multiple intercompany transactions, this directly reduces annual compliance costs and audit exposure.

Specific simplifications include:

- No comparable company searches required

- Pre-approved margins accepted by statutory definition

- Reduced documentation burden

- Audit certainty for covered transactions

Key Amendments: 2025 Extensions and the Upcoming 2026 Overhaul

March 2025 Amendment (CBDT Notification 21/2025)

Extension and expansion:

- Safe harbour rules extended to AY 2025-26 and AY 2026-27 (covering FY2024-25 and FY2025-26)

- Upper transaction threshold raised from INR 200 crore to INR 300 crore for five service categories:

- Software development services

- ITeS

- KPO services

- Contract R&D (software)

- Contract R&D (generic pharma)

New inclusion:

- "Core auto components" definition expanded to include lithium-ion batteries for electric/hybrid vehicles

Procedural change:

- Single-year election permitted (waiver of 3-year continuity requirement)

Union Budget 2026 Proposed Overhaul (Effective April 1, 2026)

The CBDT released draft Income-tax Rules, 2026 on February 11, 2026. As of May 2026, these rules have not been formally notified.

Major proposed changes:

Consolidation of IT Service Categories

| Current Structure | Proposed 2026 Structure |

|---|---|

| 4 separate categories (software dev, ITeS, KPO, contract R&D software) | Single "IT services" category |

| Margins ranging 17-24% | Unified 15.5% margin |

This represents a substantial reduction from current ranges, making safe harbour more commercially viable for Singapore entities operating India captive centers.

Transaction Threshold Increase

Current threshold: INR 300 crore (~USD 32 million)

Proposed 2026 threshold: INR 2,000 crore (~USD 212 million at INR 94.25/USD)

At roughly 6.5x the current threshold, this increase means larger Singapore captive operations previously excluded will now qualify — a meaningful shift for mid-to-large-scale entities.

Extended Validity Period

Current regime: Annual election (or multi-year with continuity requirements)

Proposed 2026 regime: 5-year block period with one-time Form 49 application

Singapore companies opting in from FY2026-27 would not need to re-elect annually for five years, removing a recurring compliance burden for India captive operations.

New Data Center Services Category

The 2026 draft introduces a new safe harbour for data center services at 15% margin on cost. This is particularly relevant for:

- Singapore companies investing in India's growing data center sector

- Cloud infrastructure providers

- AI infrastructure operations

With India projected to add over 1,500 MW of data center capacity by 2026, this new category gives Singapore operators clearer pricing certainty for cross-border cost allocations.

Form Changes

| Current Forms | Proposed 2026 Forms |

|---|---|

| Form 3CEFA, 3CEFB, 3CEFC (separate) | Form 49 (merged single form) |

| Form 3CEB (Accountant's Report) | Form 48 (Accountant's Report) |

Current Status of 2026 Rules

As of May 2026, the draft rules have NOT been formally notified. These proposals carry significant planning implications, so Singapore companies should track CBDT notifications closely rather than waiting until year-end.

In the interim, Singapore companies should:

- Monitor CBDT notifications for formal issuance

- Prepare for implementation if adopted as proposed

- Continue using current rules for FY2024-25 and FY2025-26

- Assess how the proposed threshold and margin changes affect existing transfer pricing strategies before FY2026-27 begins

VJM Global's international tax team works regularly with Singapore entities on India transfer pricing compliance. If the 2026 overhaul proceeds as drafted, early preparation — particularly for companies near the INR 300 crore threshold — will reduce both compliance risk and administrative cost.

When Safe Harbour Rules Are Not the Right Fit for Singapore Companies

Financially Irrational Scenarios

If your actual operating margin exceeds the safe harbour minimum, electing into the regime locks the Indian entity into a lower declared margin. This:

- Potentially understates taxable income in India

- Creates double taxation exposure for the Singapore parent

- Reduces overall tax efficiency

For example, if your Indian captive ITeS operation operates at a 22% margin but the safe harbour threshold is 18%, electing in would artificially lower your declared margin — and create a mismatch with the Singapore parent's books.

Structural Constraints

Transaction value thresholds:

- Entities whose transactions exceed INR 300 crore (current) or INR 2,000 crore (proposed) cannot use safe harbour

- Must proceed with full arm's length documentation

APA interaction:

- Safe harbour and APAs are alternative mechanisms

- Entities with signed APAs or those pursuing APAs cannot simultaneously apply safe harbour to the same transactions

Notified Jurisdictional Areas (NJAs):

- Safe harbour does not apply to transactions with entities in NJAs

- No country is currently listed as an NJA — Cyprus was the only country ever listed, from November 2013 to December 2016

- Singapore transactions face no exclusion on this ground

MAP Forfeiture Risk

For Singapore companies in any of these situations, the Mutual Agreement Procedure (MAP) under the India-Singapore DTAA is likely the better path:

- An active MAP process is already underway

- Pricing disputes are anticipated

- The Singapore parent's income is materially affected by Indian TP adjustments

Opting into safe harbour eliminates MAP access for those transactions — a trade-off that can prove costly if a dispute escalates.

Choosing between safe harbour, APA, and MAP depends on your specific situation. VJM Global helps Singapore companies and other foreign multinationals work through that decision based on:

- Transaction value and complexity

- Appetite for audit risk versus administrative cost

- Whether a bilateral APA or MAP treaty process is already in motion

- Long-term India tax strategy and repatriation planning

Frequently Asked Questions

What are the transfer pricing safe harbour rules in India for 2025?

As of March 2025, CBDT extended safe harbour rules to FY2024-25 and FY2025-26 via Notification 21/2025. Prescribed margins for IT, ITeS, and KPO remain 17-24%, with transaction thresholds for certain services raised from INR 200 crore to INR 300 crore.

What is the threshold for transfer pricing documentation in India?

All Indian entities with international transactions must maintain TP documentation annually and file Form 3CEB, regardless of transaction value. The specified domestic transaction threshold is INR 20 crore; master file and CbC reporting thresholds are INR 500 crore (group revenue) and INR 6,400 crore respectively.

What types of transactions are eligible for India's safe harbour rules?

Eligible categories include IT/software development services, ITeS, KPO, contract R&D (software and pharma), intra-group loans, and low value-adding intra-group services—all subject to transaction value thresholds and minimum margin conditions.

Can a Singapore company opt into India's safe harbour rules for its Indian subsidiary?

The election is made by the Indian entity (subsidiary), not the Singapore parent. The Indian entity must file Form 3CEFA, meet eligibility criteria, and confirm the operating margin meets the safe harbour threshold by the income tax return due date.

What is the difference between safe harbour rules and an Advance Pricing Agreement in India?

Safe harbour rules are standardized, self-selectable margins that apply to defined transaction types with no negotiation required. APAs are individually negotiated agreements offering greater pricing flexibility, but take 2-3 years and cost INR 10-20 lakh to conclude. A key distinction: MAP is unavailable once safe harbour is elected, while APAs can resolve disputes bilaterally.

What changes are coming to India's safe harbour rules in 2026?

Union Budget 2026 proposes consolidating IT service categories under a single 15.5% margin, raising the threshold to INR 2,000 crore (~USD 212 million), five-year validity lock-in, and a new data center services category at 15%—effective April 1, 2026, pending finalization of draft rules released February 2026.

For Singapore companies navigating India's transfer pricing landscape, safe harbour rules offer a practical compliance option—though the MAP forfeiture trade-off warrants close consideration within your broader tax strategy. The proposed 2026 reforms bring significant simplification and expanded eligibility thresholds.

VJM Global's international taxation practice supports Singapore MNEs with Indian operations through transfer pricing compliance, safe harbour eligibility assessment, Form 3CEFA filing, and advisory on safe harbour versus APA versus MAP alternatives. With 30+ years of experience in India's tax and regulatory environment, our team helps you select the right compliance path and manage your transfer pricing obligations accurately.

Contact VJM Global at info@vjmglobal.com or +91 98915 76441 to assess your eligibility and evaluate whether safe harbour rules align with your Singapore-India transfer pricing strategy.