Introduction

Singapore ranks as India's #1 source of foreign direct investment in FY 2024-25, contributing INR 32,637 crore (24% of total FDI equity inflow), and has established itself as one of India's most active bilateral Advance Pricing Agreement (APA) partners with 11 BAPAs signed to date.

Yet many Singapore-based businesses operating in India encounter costly transfer pricing disputes because they assume India's regulatory framework resembles other jurisdictions. That assumption frequently triggers audit exposure and double taxation risk.

For Singapore companies with Indian subsidiaries, joint ventures, or service arrangements, transfer pricing is the set of rules that governs how those cross-border transactions are priced. India's Income Tax Act requires all such prices to reflect what independent parties would charge — the "arm's length principle" — to prevent profit shifting to lower-tax jurisdictions.

This guide explains when transfer pricing rules apply to Singapore companies in India, how arm's length pricing is determined, what documentation must be maintained, and which dispute avoidance tools — including the bilateral APA route — are available to Singapore-India structures.

Key Takeaways

- All Singapore-India related-party transactions must be priced at arm's length — no threshold exemptions apply

- TNMM benchmarked 357 transactions in FY 2024-25 APAs, making it the go-to method for IT/ITES structures

- Key filings: Form 3CEB (due October 31), Local File above INR 10 million, plus Master File and CbCR where applicable

- Penalties can reach 2% of transaction value plus up to 200% of tax on misreported income

- India signed 5 bilateral APAs with Singapore in FY 2024-25, giving companies a clear path to eliminate double taxation

- The Income Tax Act 2025 (effective April 1, 2026) introduces revised safe harbour margins (15.5% for IT services), block TP assessments, and expanded Form 48 disclosures

What Is Transfer Pricing in India?

Transfer pricing is the price set for transactions between entities within the same multinational group. These transactions can include:

- Sale of goods or raw materials

- Provision of services (management, IT, shared functions)

- Licensing of intellectual property

- Intra-group loans and guarantees

- Cost-sharing arrangements

When this price differs from what unrelated parties would agree to, income can shift to lower-tax jurisdictions — eroding the host country's tax base.

India introduced transfer pricing regulations in 2001 under Chapter X (Sections 92A–92F) of the Income Tax Act, 1961. The cornerstone is the arm's length principle (ALP), which requires income from international transactions to be computed as if the parties were unrelated. The framework has been reorganised under Chapter 10 of the new Income Tax Act 2025, effective April 1, 2026, while preserving core ALP principles.

These principles apply to two regulated categories:

- International transactions: All cross-border transactions between associated enterprises (AEs), with no minimum value threshold — even a single transaction triggers compliance

- Specified domestic transactions (SDTs): Domestic related-party transactions with aggregate value exceeding INR 200 million

For Singapore companies transacting with an Indian subsidiary or group entity, the international transactions category applies from day one — regardless of transaction size.

Why Transfer Pricing Rules Apply to Singapore Companies Operating in India

Associated Enterprise Definition

A Singapore entity qualifies as an "Associated Enterprise" of its Indian counterpart under Section 92A when:

- Direct or indirect shareholding of 26% or more

- Common management or board control (more than half of directors appointed by the other)

- Economic dependency on the other party's IP or supply

- Loan financing exceeding 51% of the Indian entity's total book assets

- Guarantee of 10% or more of total borrowings

A Singapore parent holding an Indian subsidiary almost always satisfies this definition. The Income Tax Act 2025 has broadened the AE definition further by combining the general and specific categories.

Common Singapore-India Transaction Types

The most common transaction structures that trigger TP scrutiny include:

- Indian IT/ITES subsidiaries providing software development or business process services to a Singapore parent

- Singapore holding companies charging management fees or royalties to Indian operating entities

- IP owned in Singapore licensed to India

- Intra-group loans from Singapore to Indian entities

- Cost-sharing arrangements for R&D or shared services

Tax Rate Context

Each of these transaction types carries heightened scrutiny precisely because of the tax rate differential between the two countries. Singapore's corporate tax rate (approximately 17%) is significantly lower than India's effective rate on domestic companies (approximately 25.17% under Section 115BAA). This 8 percentage point gap means Indian tax authorities are alert to structures where profits may be shifted toward Singapore, making thorough arm's length pricing documentation especially critical for Singapore-India group structures.

The FDI picture reinforces this focus. Singapore accounted for 23.87% of cumulative FDI into India (USD 171.92 billion as of December 31, 2024), making Singapore-routed transactions a natural priority area for India's transfer pricing enforcement.

How India Determines the Arm's Length Price

India prescribes six ALP methods and requires taxpayers to apply the Most Appropriate Method (MAM) — there is no statutory hierarchy. The MAM must be selected based on transaction nature, the functional and risk profile of both entities, data availability, and degree of comparability. The basis of selection must be documented and justified in the transfer pricing study.

A comparability analysis (FAR: Functions, Assets, Risks) is mandatory and forms the backbone of any transfer pricing study.

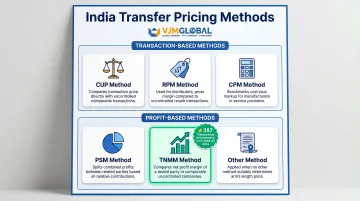

Transaction-Based Methods

Comparable Uncontrolled Price (CUP): Compares the controlled transaction price directly to an identical or similar uncontrolled transaction. Most reliable, but requires high comparability.

Resale Price Method (RPM): Works backward from the resale price charged to an unrelated customer, deducting an appropriate gross margin.

Cost Plus Method (CPM): Adds a market-level gross markup to the supplier's direct and indirect costs.

All three are preferred where reliable price or gross margin data on comparable transactions exists.

Profit-Based Methods

Profit Split Method (PSM): Divides the combined profit of the AEs in proportion to their relative functional contributions. Used primarily for transactions involving unique, hard-to-value intangibles (for example, where both Singapore and India entities contribute to R&D outcomes).

Transactional Net Margin Method (TNMM): Compares the net profit margin of the tested party, using a Profit Level Indicator such as operating profit/costs or operating profit/sales, against comparable independent companies.

TNMM is the most commonly used method for IT/ITES captive service providers in India. In FY 2024-25 APAs, 357 transactions were benchmarked using TNMM, far exceeding any other method.

Range Concept and Tolerance Band

Once the MAM is selected, India applies specific rules to determine whether a price adjustment is warranted.

When six or more external comparables are available and TNMM, RPM, or CPM is the MAM, India applies the interquartile range (35th to 65th percentile). If the taxpayer's margin falls within this range, no adjustment is made. If outside, India uses the median as the ALP.

The tolerance band applies even when a single ALP is determined. For AY 2025-26, the tolerance is:

- 1% for wholesale trading transactions

- 3% for all other transactions

If the variation between the declared price and computed ALP does not exceed the tolerance, the declared price is accepted.

Captive Service Provider Issue

Indian tax authorities do not accept losses or very low margins for limited-risk Indian entities providing services to a Singapore principal. The Indian entity's actual conduct, not merely the contract, determines its risk profile.

If the Indian entity controls day-to-day operations, employs senior staff, or manages client relationships, it may not be characterised as a low-risk captive. Singapore companies should ensure their Indian entity's contractual terms, FAR analysis, and actual business conduct are fully aligned.

In the landmark Netflix India ruling (ITAT Mumbai, October 2025), the tribunal rejected a Revenue attempt to recharacterise a limited-risk distributor as an entrepreneurial entity, deleting a proposed INR 445 crore adjustment. Key factors: the entity owned no IP, employed only 64 people, and operated under strict supervision.

Transfer Pricing Documentation and Compliance Requirements in India

India's three-tier documentation framework (aligned with OECD BEPS Action 13) consists of:

- Local File (Rule 10D documentation + Form 3CEB)

- Master File (Form 3CEAA)

- Country-by-Country Report or CbCR (Form 3CEAD)

Each tier has separate applicability thresholds and filing deadlines.

Local File and Form 3CEB

Form 3CEB (Accountant's Report certified by an independent Chartered Accountant) must be filed by every company that has entered into any international transaction with no minimum threshold exemption. Filing deadline is October 31 each year.

The Local File (Rule 10D) is required when aggregate international transactions exceed INR 10 million and must contain:

- Ownership structure and group profile

- Business description

- Nature and terms of each transaction

- FAR analysis

- Economic analysis

- Benchmarking study with comparables

- ALP computation

- Rationale for method selection

Documentation must be prepared contemporaneously and maintained for eight years.

Master File and CbCR

Master File (Form 3CEAA) is required when both of the following thresholds are met:

- The Indian entity's aggregate international transactions exceed INR 500 million (or INR 100 million for intangible transactions)

- The group's consolidated global turnover exceeds INR 5 billion

It covers group-level business overview, supply chain for top five products/services, intangibles strategy, financing arrangements, and FAR analysis for group entities contributing 10%+ of group revenue or assets. Due date: November 30.

CbCR (Form 3CEAD) is required when the group's consolidated revenue in the prior accounting year exceeds INR 64 billion, requiring country-level disclosure of revenues, profits, taxes paid, and employees. Singapore companies should confirm whether the Singapore parent or an Indian entity is the designated filing entity under India's exchange-of-information arrangement with Singapore.

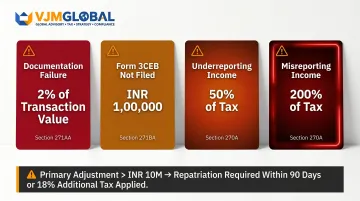

Penalty Structure

| Violation | Penalty | Section (1961 Act) |

|---|---|---|

| Failure to maintain documentation | 2% of transaction value | Section 271AA |

| Failure to file Form 3CEB | INR 100,000 | Section 271BA |

| Underreporting of income | 50% of tax | Section 270A |

| Misreporting of income | 200% of tax | Section 270A |

If a primary TP adjustment exceeds INR 10 million, a secondary adjustment is mandatory. The excess profit must be repatriated to India within 90 days; otherwise, the company pays an additional 18% tax on the unrepatriated amount (effectively approximately 20.97% including surcharge and cess).

Singapore companies managing these obligations across multiple entities often work with an India-based transfer pricing advisor — VJM Global, for instance, has supported foreign multinationals with India-specific documentation and audit defence for over 30 years.

Form 48: New Disclosure Requirements (Effective TY 2026-27)

Under the Income Tax Act 2025, Form 48 replaces Form 3CEB from FY 2026-27. Key enhancements include:

- Separate disclosure of total transaction amounts

- Details of royalty agreements, financing and guarantee agreements

- APA arrangements mapping

- ALP computation methodology including number and margins of comparables

- Expenses incurred by AEs on behalf of the taxpayer

Singapore companies should begin preparing systems to capture this transaction-level data ahead of the April 2026 effective date. Fresh benchmarking searches must be conducted annually ; rolling forward prior-year data without a new search is a documented compliance gap that TPOs actively target.

Safe Harbour Rules, APAs, and Dispute Avoidance for Singapore Companies

Safe Harbour Rules

Safe Harbour Rules (SHRs) under Section 92CB offer optional predefined operating profit margins that, if maintained, are accepted by Indian tax authorities without further scrutiny.

Revised Safe Harbour Margins (Effective TY 2026-27):

| Transaction Category | Margin | Revenue Cap |

|---|---|---|

| IT services (software development, ITeS, KPO) — turnover ≤ INR 200 crore | OPM ≥ 15.5% | INR 2,000 crore (INR 20 billion) |

| IT services — turnover > INR 200 crore | OPM ≥ 16.5% | INR 2,000 crore |

| Contract R&D services | OPM ≥ 21% | -- |

| Corporate guarantees | Commission ≥ 1% p.a. | -- |

| Intra-group loans | Reference rate + 1.5%–4.5% spread (by credit rating) | -- |

The new regime extends safe harbour validity to five consecutive years for IT service transactions starting FY 2026-27, reducing the annual refiling burden.

Critical limitation: Opting for SHR prevents invoking MAP for the same transaction. If a foreign tax authority makes a corresponding adjustment, India will not provide treaty-based relief.

APAs: The Bilateral Route for Singapore Companies

Advance Pricing Agreements (APAs) are binding agreements between the taxpayer and CBDT that pre-agree the TP methodology for up to five years (with a four-year rollback option).

Three types exist:

- Unilateral (UAPA) — India-taxpayer only

- Bilateral (BAPA) — between India and another country's tax authority

- Multilateral (MAPA) — involving multiple jurisdictions

Singapore companies benefit significantly because Singapore is one of India's bilateral APA partner countries. As of FY 2024-25:

- 31 BAPA applications filed by Singapore companies

- 11 BAPAs signed cumulatively

- 5 BAPAs signed in FY 2024-25

A BAPA eliminates double taxation entirely by binding both India's CBDT and Singapore's IRAS to the agreed methodology. For Singapore-India groups with high-value or complex transactions, this is the strongest certainty tool available. India signed a record 174 APAs in FY 2024-25 (65 BAPAs), suggesting CBDT has both the appetite and capacity to process new applications at pace.

MAP (Mutual Agreement Procedure)

MAP is the post-dispute resolution route available under the India-Singapore DTAA (Article 25). It applies when a TP adjustment has already been made by Indian authorities and the taxpayer faces double taxation.

India aims to resolve MAP cases within 24 months.

Strategic choice framework:

- SHR — for low-complexity IT/ITES transactions with stable margins above 15.5%

- BAPAs — for high-value or intangible-heavy Singapore-India structures

- MAP — for past disputes requiring treaty-based relief

Block TP Assessment

These three tools cover the dispute avoidance spectrum — but for groups with highly consistent transaction profiles, the 2025 IT Act introduced a fourth option. Block TP assessment allows the ALP determined in a lead year to apply to similar transactions in the following two years.

Conditions:

- Same AEs and international transactions

- Consistent methodology

- No material change in FAR profile

- Taxpayer-optional (requires filing Form 46)

This reduces the frequency of MAP triggers for stable business models but creates lock-in risk if the lead year is unfavourable.

Common Transfer Pricing Pitfalls Singapore Companies Make in India

Documentation Prepared After the Audit Notice

Indian TPOs frequently reject TP documentation that was not demonstrably in place before the filing deadline. Documentation must be contemporaneous, backed by invoices, agreements, and correspondence.

Benchmarking studies must use current-year (or immediately preceding year) data from recognised databases and be updated annually with a fresh comparables search — rolling forward without revision is one of the most commonly flagged deficiencies.

Mischaracterising the Indian Entity's Functional and Risk Profile

Singapore companies often structure contracts to make their Indian subsidiary appear as a low-risk, limited-function entity. If the Indian entity's actual conduct involves managing client relationships, retaining specialised talent, or controlling day-to-day operations, Indian tax authorities will recharacterise it as a higher-value participant.

Indian authorities now conduct detailed value chain analyses. Any mismatch between contractual risk allocation and economic reality sharply raises audit risk. Verify that the following are fully consistent with each other:

- Inter-company agreements and board resolutions

- Actual day-to-day operational conduct

- Functional and risk profile declared in TP documentation

Overlooking Secondary Adjustments and Thin Capitalisation Rules

Many Singapore companies that receive a primary TP adjustment (ALP adjustment by the TPO) are unaware that secondary adjustments are mandatory when the adjustment exceeds INR 10 million — requiring repatriation of excess funds within 90 days or payment of 18% additional tax.

India's thin capitalisation rules (Section 94B) add a second layer of exposure for Singapore entities providing intra-group loans. Key limits to know:

- Interest deductions capped at 30% of EBITDA where total interest to AEs exceeds INR 10 million

- Disallowed interest can be carried forward for up to eight years

Frequently Asked Questions

What is transfer pricing regulation in India?

India's transfer pricing regulations under Chapter X of the Income Tax Act (now Chapter 10 of the Income Tax Act 2025, effective April 2026) require all income from international transactions between associated enterprises to be computed at the arm's length price. The framework is administered by the Central Board of Direct Taxes (CBDT) and enforced through Transfer Pricing Officers (TPOs).

What are the different methods of transfer pricing in India?

India prescribes six methods — CUP, RPM, CPM, PSM, TNMM, and Other Method — with no statutory hierarchy. Taxpayers must apply the Most Appropriate Method based on transaction type, FAR analysis, and data availability. TNMM is the most commonly used method for IT/ITES transactions in India, benchmarking 357 transactions in FY 2024-25 APAs.

What are the transfer pricing thresholds and limits in India?

All international transactions (regardless of value) require Form 3CEB. The Local File documentation threshold is INR 10 million in aggregate international transactions. The Master File threshold is INR 500 million in international transactions with group turnover above INR 5 billion. CbCR applies when group consolidated revenue exceeds INR 64 billion. SDTs are subject to TP rules only above INR 200 million.

What documentation is required for transfer pricing in India?

Required documentation includes:

- Form 3CEB (Accountant's Report) — due October 31, mandatory for all international transactions

- Local File under Rule 10D — FAR analysis, ALP computation, benchmarking study, and comparables data

- Master File (Form 3CEAA) and CbCR (Form 3CEAD) where applicable

All records must be maintained for eight years from the end of the relevant assessment year.

Is a transfer pricing audit mandatory in India and when is it due?

Filing Form 3CEB is mandatory for every company with international transactions (due October 31), but not every company is referred to a Transfer Pricing Officer for audit. Referrals are risk-based under CASS parameters, triggered by high transaction values, prior TP adjustments exceeding INR 10 million, or non-filing of required reports. The income tax return for TP cases is due November 30.

What are the tax implications of transfer pricing in India?

Non-arm's length pricing can result in an upward adjustment to taxable income in India by the TPO. Penalties range from 2% of transaction value for documentation failures to 50–200% of tax for under-reported or misreported income. For Singapore companies, double taxation risk arises if India adjusts income already taxed in Singapore. This risk can be mitigated through the India-Singapore DTAA, Mutual Agreement Procedure (MAP), or a Bilateral APA.