Introduction

Indian businesses with Singapore subsidiaries, holding companies, or related-party transactions face a distinct compliance challenge: satisfying both IRAS (Singapore's Inland Revenue Authority) and India's CBDT transfer pricing norms simultaneously. Singapore's position as India's 2nd-largest cumulative FDI source at USD 171.92 billion (23.87% of total FDI from January 2000 to December 2024) underscores the scale of this exposure. Getting either jurisdiction wrong can trigger double taxation, a 5% surcharge on adjustments in Singapore, and significant penalties in India.

Many Indian groups use Singapore as a regional holding hub, treasury centre, or IP holding entity, generating significant intra-group transaction flows. Common transaction types include:

- Management fees and service charges

- Royalty and IP licensing payments

- Intercompany loans and treasury arrangements

- Cost allocations and shared services

Each of these must comply with Singapore's Sections 34D–34F of the Income Tax Act and India's Sections 92–92F simultaneously. That means reconciling two distinct sets of documentation standards, benchmarking norms, and methodologies — while defending consistent positions across both tax authorities.

This guide covers Singapore's TP legal framework, documentation obligations, penalties, exemptions, and how Indian businesses can use the India-Singapore DTAA to resolve disputes when both sides push back.

Key Takeaways

- Singapore's transfer pricing rules apply to all related-party transactions—the arm's length principle is mandatory, regardless of transaction size

- Indian companies must prepare TP documentation if annual gross revenue exceeds SGD 10 million or if documentation was required in the prior year

- Non-compliance results in fines up to SGD 10,000 plus a 5% surcharge on any TP adjustment, payable even if no additional tax is due

- Exemptions exist for specific transactions—such as loans under SGD 15 million using IRAS indicative margins—but audit risk remains regardless

Why Singapore's Transfer Pricing Rules Matter for Indian Businesses

The India-Singapore Business Corridor

Singapore ranked as the largest FDI source into India in FY 2024-25, with over USD 14 billion in investments. In Q2 FY 2024-25 alone, Singapore accounted for 50% of India's total FDI inflows. That capital flows primarily into services (18.19%), computer software and hardware (16.74%), trading (13.32%), and infrastructure (8.39%). Each sector generates related-party transaction networks that attract transfer pricing scrutiny.

Indian businesses increasingly use Singapore for:

- Regional holding companies consolidating ownership of Southeast Asian subsidiaries

- Treasury centres managing group liquidity and intercompany financing

- IP holding entities centralising royalty streams from India and APAC markets

- Shared service centres providing management, IT, or back-office support to Indian operations

Each of these structures generates intra-group transactions—royalty payments, management fees, intercompany loans, cost recharges—that trigger TP obligations in both jurisdictions.

The Dual Compliance Burden

Indian TP regulations under Sections 92-92F of the Income Tax Act, 1961 require arm's length pricing for all international transactions, enforced by the Transfer Pricing Officer (TPO) under Section 92CA. Simultaneously, Singapore's Sections 34D-34F of the Income Tax Act 1947 impose independent TP obligations, including:

- Mandatory contemporaneous documentation (Section 34F)

- A 5% surcharge on adjustments (Section 34E)

- IRAS's power to adjust profits to arm's length (Section 34D)

Indian businesses cannot prepare Indian TP documentation and assume it satisfies IRAS. Singapore applies its own standards for indicative loan margins, profit level indicators, and comparability analysis — each of which diverges from CBDT guidance in meaningful ways. Both filings must be prepared independently and then cross-checked for consistency.

Which Indian Business Structures Face Singapore TP Scrutiny

IRAS specifically targets:

- Indian companies with Singapore subsidiaries conducting related-party transactions

- Singapore branch offices of Indian companies, treated as Singapore taxpayers for TP purposes

- Joint ventures involving Indian and Singaporean entities

- Indian MNE groups using Singapore as a regional headquarters or IP hub

IRAS flags higher audit risk when structures show:

- Recurring losses in the Singapore entity

- Transactions routed through low-tax jurisdictions

- Significant use of intangibles without clear ownership documentation

- Operating results that don't match the entity's actual functions and risks

Singapore's Transfer Pricing Legal Framework: What Indian Businesses Must Know

Statutory Basis and IRAS Guidelines

Singapore's TP rules are codified in:

| Provision | Scope |

|---|---|

| Section 34D (ITA 1947) | Comptroller (tax authority) may adjust income or deductions to arm's length if related-party conditions differ from independent conditions |

| Section 34E (ITA 1947) | 5% surcharge on adjustment amount, payable regardless of tax liability |

| Section 34F (ITA 1947) | Mandatory TP documentation from YA 2019; penalties for non-compliance |

These are supplemented by the Income Tax (Transfer Pricing Documentation) Rules 2018 (S 93/2018) and the 2024 Amendment Rules (S 501/2024), which raised services exemption thresholds from SGD 1 million to SGD 2 million for YA 2026 onward.

The IRAS Transfer Pricing Guidelines (8th Edition, published 19 November 2025) provide practical guidance on applying these rules. While Singapore broadly aligns with OECD TP Guidelines, jurisdiction-specific rules take precedence. This includes IRAS's annually published indicative margins for related-party loans (applicable to loans not exceeding SGD 15 million) and specific guidance on profit level indicators.

The Arm's Length Principle and How to Apply It

The arm's length principle requires that transactions between related parties reflect what independent parties would agree to under comparable circumstances. IRAS is empowered under Section 34D to adjust profits where related-party pricing deviates from this standard.

IRAS recommends a three-step approach:

- Conduct a comparability analysis — identify economically relevant characteristics of the transaction (functions, assets, risks, contractual terms, economic circumstances)

- Identify the most appropriate TP method and tested party — select the method that best fits the transaction and determine which entity's profit should be tested

- Determine the arm's length result — apply the method using reliable comparable data, using local Singapore comparables where available

Indian businesses should structure intra-group agreements with Singapore entities following this framework. IRAS prefers local comparables over regional ones and does not permit the use of secret comparables for assessment purposes.

Accepted Transfer Pricing Methods

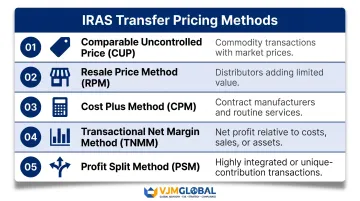

IRAS accepts all five OECD-recognised methods:

- Comparable Uncontrolled Price (CUP) — best suited for commodity transactions where market prices are readily available

- Resale Price Method (RPM) — applies to distributors that add limited value before resale

- Cost Plus Method — used for contract manufacturers or routine service providers

- Transactional Net Margin Method (TNMM) — measures net profit relative to an appropriate base (costs, sales, assets)

- Transactional Profit Split Method — reserved for highly integrated operations or transactions involving unique, hard-to-value contributions

Singapore follows the **"Most Appropriate Method" rule; there is no prescribed hierarchy. Taxpayers must select the method that provides the most reliable measure of an arm's length result for the specific transaction, supported by robust documentation.

Where Indian businesses already have a benchmarking approach in place, the following differences with IRAS's framework deserve close attention:

Key differences from Indian TP norms:

- Indian benchmarking often relies on Indian or regional comparables; IRAS expects Singapore local comparables and will scrutinise results built solely on regional data

- IRAS recommends the interquartile range (25th–75th percentile) to address comparability defects; the full range is accepted only when all data points are equally reliable

- Multi-year data is expected to account for business cycles and long-term pricing arrangements — a requirement less consistently applied under Indian TP practice

Transfer Pricing Documentation Requirements for Indian Businesses Operating in Singapore

Who Must Prepare TP Documentation

Under Section 34F(2), mandatory TP documentation applies if:

- Gross revenue from trade or business exceeds SGD 10 million for the relevant period; OR

- TP documentation was required for the immediately preceding basis period

This "stickiness" creates a persistent obligation. Once triggered, companies remain subject to documentation requirements until gross revenue falls below SGD 10 million for the current and two preceding basis periods.

Critical for Indian businesses: Singapore branches of Indian companies are treated as Singapore taxpayers for TP purposes. They cannot assume India-level TP documentation covers their IRAS obligations—separate Singapore-compliant documentation is required.

What the Documentation Must Include

Singapore follows a three-tiered structure aligned with OECD BEPS Action 13:

Tier 1: Group-Level Overview (Master File equivalent)

- Global business overview and organizational structure

- MNE group's overall TP policies relevant to Singapore operations

- Group intangibles and financial activities

Tier 2: Entity-Level Section (Local File equivalent)

- Singapore taxpayer's business details and financial information

- Functional analysis (FAR) – functions performed, assets employed, risks assumed

- Detailed TP analysis demonstrating arm's length pricing for each covered transaction

- Selection and application of the most appropriate TP method

Tier 3: Country-by-Country Report (CbCR)

- Required for ultimate parent entities with consolidated revenue ≥ SGD 1,125 million

The Second Schedule of the 2018 Rules prescribes detailed content requirements. Documentation must be in English and explicitly state the date it was completed.

Important for Indian businesses: Singapore does not mandate separate OECD-format Master File and Local File, but its content requirements broadly align with OECD Annexes I and II.

Indian businesses preparing Master File and Local File for CBDT requirements should not assume that filing also satisfies IRAS. Supplementation addressing Singapore-specific requirements — such as local comparables and IRAS-accepted methods — is required. VJM Global's cross-border tax advisory team helps Indian businesses prepare IRAS-compliant TP documentation that aligns with CBDT obligations, reducing the risk of inconsistent positions across both jurisdictions.

Timing, Retention, and RPT Reporting

Contemporaneous Preparation

- Documentation must be completed no later than the income tax return filing due date for the relevant year

- Must be retained for at least five years from the end of the basis period

- IRAS can request submission within 30 days of written request

Related Party Transactions (RPT) Reporting Form

Companies whose total RPT value in financial statements exceeds SGD 15 million for the financial year must complete the RPT Form as part of their corporate income tax return (Form C).

How the SGD 15 million threshold is calculated:

- Aggregate all amounts received/receivable and paid/payable to related parties per the income statement (excluding dividends and key management compensation)

- Add year-end balances of loans and non-trade amounts due from/to related parties

- Purchases and sales cannot be netted off

Required information:

- Transaction categories (sales/purchases of goods, services, royalties, interest, other income/expense)

- Ultimate Holding Company details

- Top 5 foreign related parties (by value), including entity names, countries, relationship types, and transaction amounts

Note: Completing the RPT Form does not replace the need for TP documentation. TP documentation should not be submitted with the RPT Form — it must be provided within 30 days only upon IRAS's request. Failure to complete the RPT Form renders the tax return incomplete.

Penalties, Surcharges, and Exemptions Under Singapore TP Rules

Penalties for Documentation Non-Compliance

Under Section 34F(8) of the Income Tax Act 1947, failure to comply with TP documentation requirements can result in a fine of up to SGD 10,000 per offence. Specific offences include:

- Failure to prepare TP documentation as required by Section 34F(3)

- Failure to retain documentation for the required five-year period

- Failure to submit documentation within 30 days of IRAS request

- Providing documentation that is false or misleading in a material particular

Each violation is treated as a separate offence with its own fine.

The 5% Surcharge on TP Adjustments

Section 34E imposes a 5% surcharge on the amount of any TP adjustment made by IRAS under Section 34D or voluntarily disclosed by the taxpayer:

- Even loss-making entities face cash outflows — the surcharge applies whether or not additional income tax is actually payable

- Payable within 30 days of the surcharge notice

- IRAS may remit the surcharge under Section 34E(3) for good cause, particularly for taxpayers with cooperative conduct and strong compliance records

Example: If IRAS adjusts a Singapore subsidiary's management fee from SGD 1 million to SGD 1.5 million (SGD 500,000 adjustment), the surcharge is SGD 25,000 (5% of SGD 500,000), payable even if the subsidiary remains in a tax loss position.

Exemptions from Documentation Requirements

General Exemption: Companies with gross revenue not exceeding SGD 10 million — and where documentation was not required in the prior year — are exempt from Section 34F obligations.

Transaction-Level Exemptions (most relevant to Indian businesses):

| Transaction Type | Exemption Threshold | Notes |

|---|---|---|

| Related-party loans | Principal ≤ SGD 15 million AND using IRAS indicative margins | IRAS publishes indicative margins annually |

| Routine support services | 5% cost mark-up for services in First Schedule (Annex C) | Covers HR, IT support, accounting, etc. |

| Goods (purchase/sale) | ≤ SGD 15 million per category | |

| Services | ≤ SGD 2 million per category (YA 2026 onward) | Raised from SGD 1 million by 2024 Amendment |

| Royalties/rentals/guarantees | ≤ SGD 2 million per category (YA 2026 onward) | Raised from SGD 1 million by 2024 Amendment |

| APA-covered transactions | Covered by an Advance Pricing Arrangement | Full exemption for APA scope |

CRITICAL WARNING: Qualifying for a documentation exemption under Section 34F does NOT shield a taxpayer from IRAS audit or Section 34D TP adjustment. IRAS advises that even exempt entities should prepare TP documentation to reduce audit risk. Section 34D — IRAS's power to make arm's length adjustments — operates entirely independently of Section 34F documentation requirements.

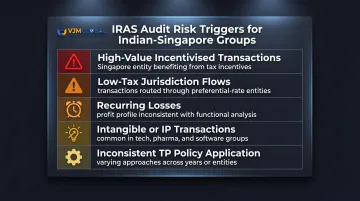

IRAS Audit Risk Triggers Indian Businesses Should Watch

Knowing where IRAS focuses attention is half the battle. The following risk factors are especially relevant for Indian-Singapore group structures:

- High-value related-party transactions where the Singapore entity benefits from preferential tax treatment or tax incentives

- Transactions with parties in low-tax jurisdictions (Singapore's 17% headline rate may be viewed as low-tax by Indian authorities)

- Recurring losses or unusual profit fluctuations inconsistent with the entity's risk profile and functional analysis

- Transactions involving intangibles or IP (common in Indian tech, pharma, and software groups using Singapore as an IP hub)

- Inconsistent application of stated TP policies across years or entities

Financial transactions — including loans, cash pooling, and guarantees — also draw scrutiny, as do headquarters cost allocations and cost contribution arrangements tied to intangibles development.

Dispute Resolution: Using the India-Singapore DTAA and APAs

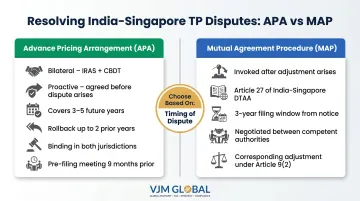

Advance Pricing Arrangements (APAs)

Singapore's APA programme allows Indian businesses to agree upfront on TP methodology for specific transactions, providing certainty and reducing audit risk:

Bilateral APAs (recommended):

- Joint agreement between IRAS and India's CBDT

- Cover 3 to 5 future financial years

- Rollback available for up to 2 prior years (if facts are consistent)

- Provide binding certainty in both jurisdictions, eliminating double taxation risk

- India's CBDT executed 95 APAs and 32 bilateral APAs in FY 2022-23 across all treaty partners

Unilateral APAs (discouraged):

- Agreement only with IRAS

- Lower certainty — non-binding on India's CBDT, creating residual double taxation risk

- IRAS will exchange information regarding cross-border unilateral APAs with the jurisdictions of related parties

- Generally not recommended for Indian businesses with significant India-side exposure

Pre-filing requirement: A pre-filing meeting must be initiated at least 9 months before the first day of the APA covered period.

When a TP dispute has already arisen — rather than preventing one — MAP under the India-Singapore DTAA becomes the primary tool.

Mutual Agreement Procedure Under the India-Singapore DTAA

The India-Singapore Double Taxation Avoidance Agreement (DTAA), signed 24 January 1994 and amended by three protocols, offers two key dispute resolution mechanisms:

Article 27 (Mutual Agreement Procedure):

- If a TP adjustment by IRAS results in double taxation (same income taxed in both India and Singapore), Indian businesses can invoke MAP

- A case must be presented to the competent authority within 3 years of receipt of the notice giving rise to taxation inconsistent with the Agreement

- Both competent authorities (IRAS and India's CBDT) shall endeavour to resolve the case by mutual agreement

Article 9(2) (Corresponding Adjustments):

- Inserted by the Third Protocol (signed 30 December 2016), enables corresponding adjustments

- When Singapore includes and taxes profits already taxed in India, India must make an appropriate adjustment to the tax charged on those profits, provided the conditions are arm's length

- Provides mechanism for eliminating economic double taxation from TP adjustments

Practical application: Consider a scenario where IRAS adjusts a Singapore subsidiary's management fee upward by SGD 500,000. If India has already taxed that same SGD 500,000 as arm's length income in the Indian parent's hands, the business faces double taxation on the same profits.

Invoking Article 27 MAP triggers negotiations between IRAS and India's CBDT, typically resulting in a corresponding downward adjustment in India to eliminate the overlap.

Deciding between an APA and MAP — and timing each correctly — is critical to avoiding unnecessary tax exposure. VJM Global's international tax advisory team has managed India-side procedural requirements for both mechanisms across India-Singapore structures, and can help determine which route fits your situation.

Frequently Asked Questions

What is the penalty for transfer pricing in Singapore?

Non-compliance with TP documentation requirements can result in a fine of up to SGD 10,000 per offence. Any TP adjustment — whether made by IRAS or voluntarily disclosed — also attracts a 5% surcharge on the adjustment amount under Section 34E, payable even if no additional tax is due.

When does an Indian company need to prepare transfer pricing documentation for Singapore?

Indian companies must prepare TP documentation when gross revenue from Singapore operations exceeds SGD 10 million, or when documentation was required in the immediately preceding year. Both Singapore subsidiaries and Singapore branches of Indian companies fall under these triggers.

Does Singapore follow the OECD Transfer Pricing Guidelines?

Singapore broadly aligns with the OECD TP Guidelines but has jurisdiction-specific rules that take precedence—including indicative margins for related-party loans, specific profit level indicator guidance, and preference for local Singapore comparables. The IRAS Transfer Pricing Guidelines (8th Edition, 2025) govern Singapore TP practice.

Are there exemptions from Singapore's transfer pricing documentation requirements?

Yes. The general exemption covers companies with gross revenue below SGD 10 million (where documentation wasn't required the prior year). Transaction-level exemptions apply to qualifying loans, routine support services at a 5% cost mark-up, and goods/services below category thresholds — but exemptions do not shield against IRAS audits or TP adjustments.

What is an Advance Pricing Arrangement (APA) and can Indian businesses apply for one in Singapore?

An APA is a formal arrangement between the taxpayer and IRAS on TP methodology for future transactions, typically covering 3–5 years. Indian businesses can pursue a bilateral APA involving both IRAS and India's CBDT, providing binding certainty and eliminating double taxation risk in both jurisdictions.

How does Singapore's transfer pricing framework interact with India's TP rules for cross-border transactions?

Both Singapore (Sections 34D–34F) and India (Sections 92–92F) require arm's length pricing, but their documentation requirements, accepted methods, and benchmarking standards differ. Indian businesses must comply on both ends and reconcile positions carefully — conflicting adjustments across jurisdictions remain a real risk without coordinated documentation.