Key Takeaways

- Arm's length pricing applies to all international transactions with Associated Enterprises — no minimum transaction value exempts you from compliance

- Arm's length price (ALP) must be determined using one of six prescribed methods, with TNMM most commonly applied for IT/ITeS services

- Documentation kicks in at INR 1 crore (Local File), INR 50 crore (Master File, if group turnover exceeds INR 500 crore), and INR 6,400 crore (CbCR)

- Penalties span 2% to 200% of tax, making proactive contemporaneous documentation essential

- India has signed 84 bilateral APAs with Singapore in FY 2025-26, offering pricing certainty for qualifying cross-border transactions

What Is Transfer Pricing in India and Why Singapore Businesses Must Pay Attention

Transfer pricing in India governs the pricing of cross-border transactions between Associated Enterprises (AEs). For Singapore holding companies, this applies directly to every transaction with their Indian subsidiary, including:

- Management fees and royalty payments

- Intercompany loans and capital financing

- Shared service charges and cost allocations

- Business restructuring arrangements

- Transfers of goods, services, and intangibles

The Associated Enterprise Trigger for Singapore Businesses

Two entities are AEs if one holds 26% or more voting power in the other, or if the same person controls both—a threshold commonly met by Singapore parent-Indian subsidiary structures. Section 92A of the Income Tax Act defines multiple additional deemed-AE criteria, including management control and economic dependency, covering most Singapore-India group structures.

Why India Is a High-Scrutiny Jurisdiction

India operates a Computer Assisted Scrutiny Selection (CASS) system that systematically flags TP risk cases for audit by specialized Transfer Pricing Officers (TPOs). Each TPO handles up to 50 complex cases annually, focusing on high-value international transactions.

Singapore's prominence as India's second-largest cumulative FDI source — USD 171.92 billion since 2000, representing 23.87% of total inflows — means Singapore-India transactions receive heightened scrutiny. Singapore is explicitly listed as a bilateral APA partner, making the India-Singapore DTAA directly relevant for resolving TP disputes through Mutual Agreement Procedure (MAP).

India's TP Legal Framework: Key Provisions Singapore Businesses Must Know

Governing Legislation

India's TP rules are governed by Sections 92A–92F of the Income Tax Act, 1961, contained in Chapter X. Effective April 1, 2026, the new Income Tax Act, 2025 reorganizes these provisions while expanding coverage to digital assets, platform economies, and innovative financing structures—particularly relevant to Singapore tech and fintech companies operating in India. Under the new Act, the Associated Enterprise definition is consolidated under Section 162.

Scope of International Transactions

The TP regime covers all major categories of cross-border intercompany transactions, including:

- Purchase, sale, or lease of tangible and intangible property

- Provision of services

- Lending or borrowing of money

- Capital financing arrangements

- Business restructuring

- Cost-sharing arrangements

Any cross-border flow between a Singapore parent and its Indian AE falls within this scope.

Specified Domestic Transactions (SDTs)

TP rules also apply to certain domestic transactions (for example, between two Indian entities under the same MNE group) if aggregate value exceeds INR 20 crore. Singapore businesses with multiple Indian group entities—such as a manufacturing subsidiary and a distribution affiliate—must evaluate SDT exposure.

Three-Tier Documentation Framework

India adopted the OECD BEPS Action 13 framework via Finance Act 2016, implementing:

- Local File – Annual TP documentation with FAR analysis and benchmarking

- Master File – Group-level information on MNE structure, intangibles, and financing (Form 3CEAA)

- Country-by-Country Report (CbCR) – Consolidated group reporting (Form 3CEAD, governed by Section 316 under the new Act)

Each tier has separate thresholds and deadlines (detailed below).

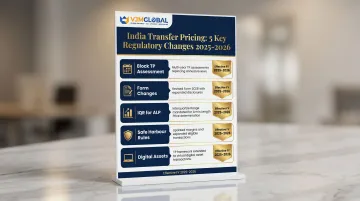

Key 2025–2026 Changes Impacting Singapore Businesses

| Change | Detail | Effective Date |

|---|---|---|

| Block TP Assessment | ALP determined for Year 1 applies to Years 2–3 if FAR analysis and methods unchanged; requires filing Form 46 | AY 2026-27 (Rule 82) |

| Form Changes | Form 3CEB replaced by Form 48; Form 46 for block assessment applications | April 1, 2026 |

| IQR for ALP | Transition from arithmetic mean to interquartile range (35th–65th percentile) | April 1, 2026 (Rule 10CA) |

| Safe Harbour Revisions | Uniform 15.5% margin for IT Services; threshold raised to INR 2,000 crore | April 1, 2026 |

| Digital Assets Coverage | Expanded scope to platform economies and Significant Economic Presence | April 1, 2026 |

The block assessment offers Singapore businesses multi-year pricing certainty, but requires upfront certification by a Chartered Accountant and submission by June 30 following the third tax year.

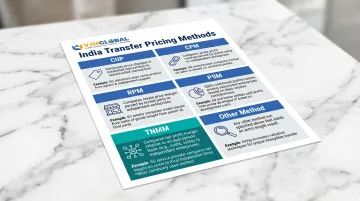

How Arm's Length Price Is Determined: The 6 Prescribed Methods

India prescribes six methods under Section 92C, requiring taxpayers to select the "most appropriate method" based on transaction nature, functions performed, assets employed, and risks assumed. There is no prescribed hierarchy.

The six methods with Singapore-relevant applications:

Comparable Uncontrolled Price (CUP) – Best for commodity transactions or where identical uncontrolled transactions exist. Example: A Singapore trader purchasing Indian textiles at market-referenced prices.

Resale Price Method (RPM) – Used when a Singapore entity buys goods from its Indian AE and resells to third parties. The gross margin on resale is benchmarked against comparable distributors.

Cost Plus Method (CPM) – Suited for Indian captive service providers billing their Singapore parent. The markup on operating costs is benchmarked against comparable service providers.

Profit Split Method (PSM) – For transactions involving unique intangibles shared between Singapore and Indian entities, where neither party is a routine service provider.

Transactional Net Margin Method (TNMM) – The most commonly used method in India for IT/ITeS services. Operating profit margin (e.g., EBIT/Operating Cost) is benchmarked against comparable companies.

Other Method – Catch-all for transactions without comparable uncontrolled transactions, including valuation-based approaches.

Once the appropriate method is selected, the transfer price is tested against an allowable range before any adjustment is triggered.

ALP Tolerance Band and Range

India applies a tolerance band: ±3% for most transactions; ±1% for wholesale trading. If the transfer price falls within this range, it is deemed arm's length with no adjustment.

When six or more comparable data points exist under TNMM, RPM, or CPM, the interquartile range (IQR) — 35th to 65th percentile — applies. If the transfer price falls outside the IQR, the median is used as the ALP.

Safe Harbour Margins for Singapore Businesses

Two Safe Harbour regimes currently apply:

For AY 2025-26 and AY 2026-27 (Notification 21/2025):

- IT Services: 17% on operating costs (up to INR 100 crore); 18% (INR 100-300 crore)

- ITeS: 17% (up to INR 100 crore); 18% (INR 100-300 crore)

- Transaction threshold: INR 300 crore (increased from INR 200 crore)

From April 1, 2026 (new Rules 2026):

- IT Services (consolidated category): 15.5% uniform margin

- Threshold raised to INR 2,000 crore (~US$218M)

- 5-year validity period

- Also covers KPO, contract R&D, intra-group loans (cost of funds +2-3%), corporate guarantees (1.75-2%), and data centre services (15% cost-plus)

The 2026 regime broadens eligibility, bringing more Singapore-owned GCCs and IT subsidiaries within reach. That said, opting for Safe Harbour permanently forfeits the right to invoke MAP (Rule 10TG), a trade-off that Singapore businesses must evaluate carefully before committing.

TP Documentation, Compliance Thresholds, and Filing Obligations

Documentation Tiers and Thresholds

| Documentation Tier | Threshold | Form/Rule |

|---|---|---|

| Local File | International transactions exceed INR 1 crore | Rule 10D |

| Master File | International transactions exceed INR 50 crore (INR 10 crore for intangibles) AND consolidated group turnover exceeds INR 500 crore | Form 3CEAA (Rule 10DA) |

| CbCR | Consolidated group revenue exceeds INR 6,400 crore | Form 3CEAD (Rule 10DB/Section 316) |

Local File: Core Components

- Ownership structure and MNE group profile

- Business description of taxpayer and AEs

- Nature, terms, and value of international transactions

- Functional, asset, and risk (FAR) analysis — the foundation of TP defense

- TP methods considered and most appropriate method selected

- Comparability analysis with external benchmarks

- Adjustments made to align transaction prices with ALP

Filing Obligations and Deadlines

| Obligation | Deadline | Notes |

|---|---|---|

| Form 3CEB (Accountant's Report) | October 31 of assessment year | Replaced by Form 48 from AY 2026-27 |

| Income Tax Return (TP entities) | November 30 | Mandatory for entities filing Form 3CEB/Form 48 |

| Master File (Form 3CEAA) | November 30 | Aligns with ITR due date |

| CbCR (Form 3CEAD) | 12 months from end of reporting year | Intimation (Form 3CEAB) due within 2 months |

Critical Compliance Notes

- Documentation must be prepared contemporaneously (during the financial year or before the ITR filing deadline)

- Records must be retained for eight years from the end of the relevant assessment year (Rule 10D(5))

- Annual updates are required even if the transaction continues unchanged, unless nature and terms remain materially the same

- Form 3CEB requires independent Chartered Accountant certification — the certifying CA must not have provided any other services to the entity that year

VJM Global's transfer pricing team helps Singapore businesses prepare Local Files, Master Files, and Form 3CEB filings — including benchmarking studies using databases such as TP Catalyst and Capitaline. With 30+ years in Indian tax compliance, the team ensures contemporaneous documentation is in place well ahead of filing deadlines, which matters most when TPO scrutiny occurs.

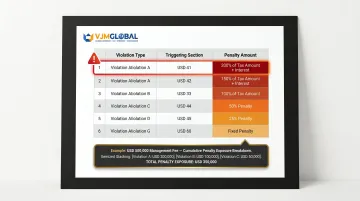

Penalties for TP Non-Compliance and Common Audit Triggers

India's TP penalty framework is among the world's strictest, with cumulative penalties possible for a single non-compliant transaction.

Penalty schedule for Singapore businesses:

| Section | Violation | Penalty |

|---|---|---|

| 271AA(1) / 271G | Failure to maintain TP documentation or furnishing incorrect information | 2% of value of each international transaction |

| 271BA | Failure to file Form 3CEB | INR 1,00,000 |

| 270A | Under-reporting of income | 50% of tax payable |

| 270A | Misreporting of income | 200% of tax payable |

| 271AA(2) | Failure to furnish Master File | INR 5,00,000 |

| 271GB | CbCR non-filing | INR 5,000/day (first 30 days); INR 15,000/day thereafter |

Example exposure: A Singapore parent charges its Indian subsidiary a management fee of USD 500,000. If the TPO determines the arm's length fee should have been USD 300,000, the excess USD 200,000 is treated as income. If this is deemed misreported (not just under-reported), the Indian entity faces a 200% penalty on the tax attributable to USD 200,000, plus the 2% documentation penalty if Form 3CEB was incomplete or incorrect.

Common TP audit triggers:

- CASS selection based on TP risk parameters (high-value transactions, volatile margins, prior adjustments)

- Prior year TP adjustments of INR 1 crore or more upheld by appellate authorities

- Non-filing or incomplete Form 3CEB—automatic referral to TPO

- Search or survey operations uncovering unreported international transactions

- Related-party transaction materiality in financial statements without corresponding TP documentation

Singapore businesses with large or complex India operations—particularly those in IT/ITeS, fintech, and shared services—are most at risk.

If an audit results in an upheld adjustment, secondary adjustment rules can compound the cost significantly.

Secondary adjustment consequences:

When a primary TP adjustment exceeds INR 1 crore and the excess is not repatriated to India within 90 days, the following consequences apply:

- The unrepatriated amount is treated as a deemed advance from the Indian taxpayer to the Singapore AE

- Imputed interest accrues at SBI one-year MCLR + 3.25%, adding to the Indian entity's taxable income each year

- As an alternative, the taxpayer can elect a one-time tax of 18% plus surcharge and cess (effective rate ~20.97%) on the unrepatriated amount for a clean exit

The cash-flow exposure is real: a SGD 1 million TP adjustment left unrepatriated triggers roughly SGD 210,000 in additional tax. Singapore groups should model repatriation windows at the deal-structuring stage and account for FEMA repatriation rules and withholding tax costs before an adjustment is ever raised.

Dispute Resolution: APAs, Safe Harbour Rules, and MAP

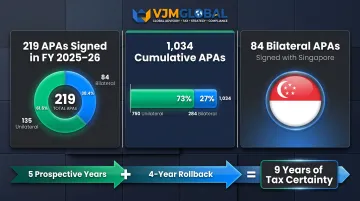

Advance Pricing Agreements (APAs)

India's APA program offers the strongest certainty for Singapore businesses. APAs cover 5 prospective years with a 4-year rollback option, providing up to 9 years of pricing certainty. Bilateral APAs (BAPAs) under the India-Singapore DTAA protect against double taxation in both jurisdictions.

India signed a record 219 APAs in FY 2025-26 (135 unilateral, 84 bilateral), with Singapore explicitly listed among 13 treaty partners. Cumulative totals now stand at 1,034 APAs (750 unilateral, 284 bilateral). Singapore businesses should pursue BAPAs early for material or recurring transactions—particularly those involving intangibles, cost-sharing, or multi-entity structures.

Eligibility requirements and filing fees include:

- Covers all international transactions and PE profit attribution

- Unilateral APA fee: INR 20,00,000 under new 2026 rules

- Rollback now applicable only if the return of income was filed by the original due date (not extended date)

- Proceedings may close if not concluded within 2-3 years

Safe Harbour Rules

For eligible Singapore businesses, Safe Harbour offers a lower-cost compliance path with reduced documentation requirements.

Covered transactions:

- IT/ITeS services (15.5% margin under 2026 rules)

- KPO and contract R&D

- Intra-group loans (cost of funds +2-3%)

- Corporate guarantees (1.75-2%)

- Low-value-adding intra-group services

Key considerations:

- 5-year validity once exercised (under 2026 rules)

- Two-year block confirmed for AY 2025-26 and AY 2026-27

- Threshold raised to INR 2,000 crore, making more Singapore GCCs eligible

- Forfeits MAP rights per Rule 10TG—cannot invoke bilateral dispute resolution for Safe Harbour transactions

Trade-off: Singapore businesses with routine service transactions and margins comfortably above Safe Harbour rates should consider opting in for certainty. Those with complex structures, unique intangibles, or margins near the threshold should preserve MAP access.

Mutual Agreement Procedure (MAP)

MAP enables the Competent Authorities of India and Singapore to resolve TP disputes bilaterally, targeting resolution within 24 months from acceptance (Rule 44G(4)). It is available under Article 25 of the India-Singapore DTAA and governed by Section 159 of the Income Tax Act, 2025.

The MAP process works as follows:

- Application filed via Form 34F

- Available for cases involving potential or actual double taxation

- Taxpayer has 30 days to accept or reject MAP resolution

- AO must implement agreed resolution within 90 days of acceptance

MAP access is denied in the following situations:

- ITAT has already passed an order on the issue

- Not available if taxpayer opted for Settlement Commission or Vivad se Vishwas scheme

- Permanently forfeited if taxpayer opted for Safe Harbour (Rule 10TG)

VJM Global has supported businesses through APA applications and MAP proceedings for 30+ years, coordinating directly with Indian and Singapore tax authorities. Our team helps you choose the right dispute resolution path based on your transaction profile and risk exposure.

Frequently Asked Questions

How does transfer pricing work in India?

Indian TP rules require transactions between associated enterprises (where at least one is non-resident) to be priced at arm's length—meaning at prices that would apply between unrelated parties—under Sections 92A–92F of the Income Tax Act. Compliance is certified annually by an independent Chartered Accountant via Form 3CEB (Form 48 from AY 2026-27).

What are the 5 methods of transfer pricing in India?

India actually prescribes six methods—CUP, Resale Price Method, Cost Plus Method, Profit Split Method, Transactional Net Margin Method (TNMM), and "Other Method." Taxpayers must apply the most appropriate method based on transaction type, functions performed, and available comparable data, with no prescribed hierarchy among the methods.

What are the documentation requirements for transfer pricing in India?

India follows a three-tier framework: Local File (annual TP study with FAR analysis and benchmarking), Master File (group-level data on MNE structure, intangibles, and financing), and Country-by-Country Report (CbCR). Each tier has a separate transaction or revenue threshold. All documents must be retained for eight years.

What is the threshold for TP documentation in India?

Mandatory Local File documentation applies when aggregate international transactions exceed INR 1 crore. Master File threshold is aggregate international transactions exceeding INR 50 crore with group turnover above INR 500 crore. CbCR applies to groups with consolidated revenue exceeding INR 6,400 crore. Form 3CEB must be filed irrespective of transaction value.

What is a transfer pricing audit in India?

A TP audit occurs when an Assessing Officer refers a case to a Transfer Pricing Officer (TPO), who independently determines the arm's length price. The TPO can examine unreported transactions and issue a binding adjustment order, with penalties ranging from 2% to 200% of the additional tax assessed.

What is an example of transfer pricing in India?

A Singapore parent charges its Indian subsidiary USD 500,000 for centralized finance, HR, and IT services. The Indian entity must prove this equals what an unrelated party would pay—using a method like TNMM or CPM—and document the arm's length basis in its Local File and Form 3CEB.