Introduction

UK businesses trading with India face a significant tax challenge: the same income can be taxed twice—once by Indian authorities via withholding tax and again in the UK as part of global taxable income. Total trade between the UK and India reached £47.4 billion in 2025, with many businesses unknowingly overpaying tax because they haven't claimed Double Taxation Avoidance Agreement (DTAA) benefits.

The India-UK DTAA is a bilateral tax treaty that prevents this double taxation and significantly reduces withholding tax rates on cross-border income. This guide covers everything UK businesses need to know:

- What the treaty covers and which income types qualify

- Specific withholding tax rates that apply under the DTAA

- How to claim relief and what documentation you need

- Common compliance mistakes that cost businesses money

Key Takeaways

- The India-UK DTAA caps Indian withholding taxes at 10-15% on dividends, interest, royalties, and technical fees—versus domestic rates exceeding 20%

- UK businesses must obtain a Tax Residency Certificate from HMRC and file Form 10F electronically before any payments are made

- The treaty defines Permanent Establishment rules that determine whether UK business profits are taxable in India

- Failing to claim treaty benefits exposes UK companies to Indian withholding rates of approximately 21.84%

What Is the India-UK Double Taxation Treaty?

The India-UK DTAA is a comprehensive bilateral tax treaty signed on 25 January 1993 (updated by a 2012 Protocol and 2020 MLI modifications) that eliminates double taxation on income flowing between both countries and prevents tax evasion. It allocates taxing rights across different income categories — dividends, interest, royalties, capital gains, and business profits.

Without the DTAA, a UK company earning royalties or technical service fees from an Indian source could be taxed once in India through withholding tax (approximately 21.84% effective rate) and again in the UK on the same income as part of its global corporation tax liability. This materially inflates effective tax costs and creates cash flow burdens.

One scope limitation often overlooked by UK finance teams: the DTAA only covers direct taxes. Indirect taxes fall entirely outside its protections:

- Covered: Income tax, corporation tax, capital gains tax

- Not covered: GST, customs duties, trade tariffs

Why the India-UK DTAA Matters for UK Businesses

The Scale of UK-India Economic Activity

Bilateral trade in goods and services totalled £47.4 billion in the four quarters to Q3 2025, an 11.7% increase from the prior year. UK outward FDI stock in India reached £19.1 billion by end of 2024. Cross-border service flows—particularly IT services, technical consulting, and royalty payments—generate substantial withholding tax exposure for UK businesses.

The Financial Impact of Not Using the Treaty

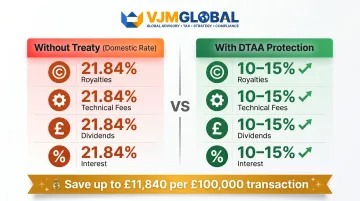

The table below shows how treaty protection changes your withholding tax position:

| Payment Type | Without Treaty (Domestic Rate) | With DTAA Protection |

|---|---|---|

| Royalties | ~21.84% (incl. surcharge & cess) | 10–15% depending on type |

| Fees for Technical Services | ~21.84% | 10–15% depending on category |

| Dividends | ~20.8–21.84% | 10–15% depending on shareholding |

| Interest | ~20.8–21.84% | 10–15% depending on lender type |

On a £100,000 royalty payment, that difference translates to approximately £6,840–£11,840 in tax saved per transaction — just by filing the right DTAA documentation.

Post-Brexit Clarity

These savings are equally available to UK businesses today as they were before 2020. The India-UK DTAA is a bilateral treaty between two sovereign governments, signed in 1993 and independent of the UK's EU membership. The treaty remains fully in force post-Brexit, unaffected by EU-India trade relations. UK businesses continue to benefit from all treaty provisions when trading with or investing in India.

Key Provisions of the India-UK DTAA

The treaty allocates taxing rights across different income categories. UK businesses must identify which treaty article applies to their specific income stream to claim the correct reduced withholding rate.

Passive Income: Dividends, Interest, Royalties, and Fees for Technical Services

Withholding Tax Rates Under the Treaty:

| Income Type | Treaty Rate | Indian Domestic Rate (without treaty) |

|---|---|---|

| Dividends (general) | 10% | Approx. 20.8–21.84% |

| Dividends (property income) | 15% | Approx. 20.8–21.84% |

| Interest (banks) | 10% | Approx. 20.8–21.84% |

| Interest (general) | 15% | Approx. 20.8–21.84% |

| Interest (UK government) | 0% | Approx. 20.8–21.84% |

| Royalties (equipment use) | 10% | Approx. 21.84% |

| Royalties (other) | 15% | Approx. 21.84% |

| Fees for Technical Services (equipment-related) | 10% | Approx. 21.84% |

| Fees for Technical Services (other) | 15% | Approx. 21.84% |

Source: HMRC Double Taxation Relief Manual DT9552

Beneficial Ownership Requirement:

These reduced rates only apply when the UK company is the beneficial owner of the income — not when acting as an intermediary or conduit. Indian tax authorities scrutinise this condition carefully, particularly for royalty and technical service payments.

UK businesses must maintain documentation proving:

- The right to use and enjoy the income

- Control over the underlying asset or service

- That they bear the associated commercial risks

Business Profits and Permanent Establishment (PE)

Under the treaty, a UK company's business profits are taxable in India only if it has a Permanent Establishment (PE) there. A PE is created in three main ways:

- Fixed place of business — an office, branch, factory, workshop, mine, or any fixed place where business is conducted in India

- Dependent agent — a person in India who habitually negotiates and concludes contracts on behalf of the UK company, maintains stock for regular delivery, or secures orders almost wholly for the UK enterprise

- Service PE — activities continuing for more than 90 days within any 12-month period (or more than 30 days for associated enterprises)

Practical relevance for UK businesses: Deploying UK employees to India for extended project work, establishing service delivery arrangements, or engaging local agents who can bind the company all create PE risk. Unintentionally creating a PE exposes the entire profits attributable to that PE to Indian corporate tax—not just withholding tax on specific payments.

VJM Global assists UK businesses with PE risk assessments, particularly for scenarios involving seconded employees, long-duration service contracts, and dependent agent relationships.

Capital Gains

Under the India-UK DTAA, capital gains are generally taxed in the country where the asset is situated. This means:

- India taxes gains on shares in Indian companies

- India taxes gains on Indian property and immovable assets

- The treaty provides limited shelter compared to passive income provisions

UK businesses selling shares in Indian companies or disposing of Indian property must comply with Indian capital gains tax rules. The applicable rates depend on the asset type and holding period:

| Asset Type | Holding Period | Tax Rate |

|---|---|---|

| Listed equity shares | >12 months (long-term) | 12.5% |

| Listed equity shares | ≤12 months (short-term) | 20% |

| Unlisted shares | >24 months (long-term) | 12.5% |

Relief from double taxation is available through a Foreign Tax Credit claimed in the UK corporation tax return. Getting the holding period classification right is critical — misclassifying the gain can result in a higher Indian tax charge that HMRC may not fully credit.

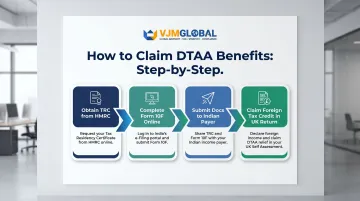

How UK Businesses Can Claim DTAA Benefits

Critical principle: Treaty benefits are not applied automatically. UK businesses must proactively follow a documentation and filing process with Indian tax authorities. Without compliance, Indian payers deduct withholding tax at domestic rates by default—resulting in significant overpayment.

Step 1: Obtain a Tax Residency Certificate (TRC) from HMRC

The TRC is foundational proof that your UK business is a tax resident of the UK. Without it, you cannot claim treaty benefits.

What the TRC must contain:

- Company legal name

- UK registered address

- UK tax identification number (Corporation Tax UTR)

- Period of UK tax residency

- Confirmation of UK tax residency status

How to apply:

- UK companies apply via the HMRC RES1 online service

- State the reason for the certificate, the specific DTAA (India-UK), income type, relevant treaty article, and period required

- Confirm beneficial ownership and UK tax liability on the income

- Newly incorporated companies must provide additional director/shareholder details

Renewal requirement: The TRC must be renewed for each financial year in which treaty benefits are claimed.

Step 2: Complete and Submit Form 10F

Form 10F is an Indian tax authority requirement under Section 90 of the Income Tax Act. Electronic filing became mandatory in July 2022.

Key fields:

- Taxpayer name and legal status

- UK tax identification number

- Period of residential status

- Nationality and address

- Confirmation of beneficial ownership

Filing process:

- Register on the Indian Income Tax e-filing portal

- Complete Form 10F electronically

- Upload supporting TRC documentation

- Submit before the income payment is made or the withholding tax return is due

Step 3: Submit Documentation to the Indian Payer and File Returns

Provide your TRC and completed Form 10F to your Indian counterpart (the payer) before payment is made. This enables the Indian payer to apply the reduced DTAA withholding rate rather than the domestic rate.

Why this matters: The Indian payer bears legal responsibility and may face penalties for under-deducting withholding tax. Indian companies therefore proactively request documentation and are often reluctant to apply treaty rates without complete compliance evidence on file.

VJM Global handles Form 10F registration, e-filing, and liaison with Indian payers — ensuring documentation reaches the right counterparts before payment deadlines.

Step 4: Claim Foreign Tax Credit in the UK

After withholding tax has been deducted in India at the treaty rate, report the Indian-source income and tax withheld in your UK corporation tax return.

How to claim relief:

- Report the gross Indian income in your UK corporation tax computation

- Claim a Foreign Tax Credit for the Indian withholding tax already paid

- The credit is limited to the UK corporation tax attributable to that income

- Maintain records of Indian tax paid (Form 16A withholding tax certificates)

Source: HMRC International Manual INTM161010

VJM Global can coordinate with your UK-side accountants to ensure Form 16A documentation is correctly applied and Foreign Tax Credit claims are accurately prepared.

Common Misconceptions UK Businesses Have About the India-UK DTAA

"Signing a contract with an Indian company means no Indian tax is due"

Indian TDS (Tax Deducted at Source) rules under Section 195 require the Indian payer to withhold tax at the time of payment regardless of contract terms. The deduction happens automatically unless the UK business has provided valid TRC and Form 10F documentation in advance. Responsibility for ensuring treaty rates are applied lies with the UK business.

"The DTAA eliminates all Indian tax obligations"

The treaty reduces or reallocates taxing rights but does not create zero-tax outcomes in all cases. The treaty provides relief from double taxation — not exemption from all taxation. Two scenarios where Indian tax still applies:

- A UK company with a PE in India remains fully taxable on attributed profits at the applicable Indian corporate tax rate

- Capital gains on Indian assets may still attract Indian tax regardless of treaty status

"DTAA eligibility means transfer pricing compliance isn't required"

UK businesses with Indian subsidiaries must comply with Indian transfer pricing rules on intercompany transactions — covering royalties, management fees, and loans — independently of any DTAA benefits. Treaty rates on cross-border payments do not exempt intercompany arrangements from arm's length scrutiny under Sections 92-92F of the Income Tax Act.

This is an area where a specialist cross-border tax advisor familiar with both Indian and UK requirements can help UK businesses structure intercompany arrangements correctly and avoid costly disputes.

Frequently Asked Questions

What is a double taxation avoidance agreement (DTAA) in India?

A DTAA is a bilateral treaty between India and another country that prevents the same income from being taxed twice by allocating taxing rights between the two countries and reducing withholding tax rates on specific income types like dividends, interest, and royalties.

How can I avoid double taxation on my India investments as a UK business or investor?

Claim India-UK DTAA benefits by following three steps:

- Obtain a Tax Residency Certificate (TRC) from HMRC

- File Form 10F with Indian tax authorities before payment is made

- Claim a Foreign Tax Credit in your UK corporation tax return for any Indian tax already paid

What are the withholding tax rates under the India-UK Double Tax Treaty?

Treaty rates are significantly lower than India's domestic withholding rate of approximately 20.8–21.84%:

- Dividends: 10–15%

- Interest: 10% (banks), 15% (general), 0% (UK government)

- Royalties: 10–15% depending on type

- Fees for Technical Services: 10–15% depending on category

Is the India-UK Double Tax Treaty still in effect after Brexit?

Yes. The India-UK DTAA is a bilateral treaty entirely separate from the UK's EU membership. It was not affected by Brexit and remains fully operative, so UK businesses continue to benefit from its provisions when trading with or investing in India.

Does a UK company need a Permanent Establishment in India to be taxed there?

Under the India-UK DTAA, a UK company's business profits are only taxable in India if it has a Permanent Establishment there. However, withholding taxes on passive income (dividends, interest, royalties, technical fees) apply regardless of whether a PE exists.

What happens if a UK business does not submit Form 10F to the Indian tax authority?

Without Form 10F and a valid TRC, the Indian payer must deduct withholding tax at the domestic rate — approximately 21.84% for royalties and technical fees, versus the 10–15% treaty rate. Any excess tax paid is potentially refundable via an Indian tax return, but the process creates cash flow delays and added compliance work.

VJM Global has served over 250 UK businesses with India-UK cross-border tax compliance, DTAA documentation, transfer pricing, and PE risk assessments. Our team manages the entire DTAA benefit claim process—from TRC applications and Form 10F filing to liaison with Indian payers and Foreign Tax Credit coordination. Contact us at info@vjmglobal.com or call +91 9213397070 for expert guidance on India-UK tax treaty compliance.