Introduction

Picture this: your UK consulting firm completes a successful project for an Indian client, invoices £50,000 in service fees, and receives payment. Then you notice 20.8% has been deducted at source by Indian tax authorities. When you file your UK tax return, HMRC taxes the same income again. Without proper planning, you've just lost over £10,000 to double taxation.

This scenario plays out repeatedly for UK businesses entering India. Many encounter unexpected tax bills on service fees, royalties, dividends from Indian subsidiaries, and interest on loans — then face the same income taxed again by HMRC.

Under India's domestic rules, foreign companies face withholding tax (TDS) of 20% plus surcharge and cess, bringing the effective rate to 20.8%–21.84% on most cross-border payments. Without Double Taxation Avoidance Agreement (DTAA) protection, those rates can devastate project margins.

This guide is a practical reference for UK businesses on India's DTAA network — covering what the India-UK agreement includes, which countries are part of the network, applicable withholding rates, and a step-by-step process to claim relief.

VJM Global has guided 250+ UK businesses through Indian tax compliance over 30+ years. The processes outlined here reflect what actually works in practice.

Key Takeaways

- India has DTAAs with 94 countries, including the UK, cutting withholding tax rates on interest, dividends, royalties, and fees

- The India-UK DTAA (signed 1993, modified by MLI in 2020) reduces typical TDS from 20.8% to 10–15% depending on income type

- To claim treaty benefits, UK businesses need a Tax Residency Certificate from HMRC and a Form 10F filed on India's e-filing portal

- Missing documentation results in higher domestic TDS rates—recovering overpaid tax adds months of compliance burden

- Treaty benefits are not automatic — the right paperwork filed before payment is the difference between 10% and 20.8% TDS

What is a DTAA and Why It Matters for UK Businesses

A Double Taxation Avoidance Agreement (DTAA) is a bilateral tax treaty between two countries that allocates taxing rights on cross-border income. The core purpose: ensure the same income isn't taxed twice—once in the source country (where the income is earned) and again in the residence country (where the taxpayer is registered). They fall into two categories:

- Comprehensive DTAAs cover all income categories: business profits, service fees, dividends, interest, royalties, capital gains, and employment income

- Limited DTAAs cover only specific categories, typically shipping and airline profits

For UK businesses operating in India, the distinction has a direct impact on your tax bill. Income streams like service fees, royalties, dividends from Indian subsidiaries, and interest on loans are all subject to Indian TDS.

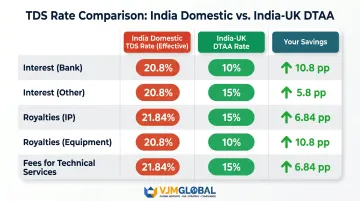

Under India's domestic Income Tax Act (Section 115A), foreign companies face base withholding rates of 20% on interest, royalties, fees for technical services (FTS), and dividends. After adding surcharge (2-5%) and health & education cess (4%), the effective TDS rate reaches 20.8% to 21.84%.

The India-UK DTAA reduces these rates significantly:

| Income Type | Domestic Rate (effective) | India-UK DTAA Rate | Savings |

|---|---|---|---|

| Interest (bank) | 20.8%-21.84% | 10% | ~11 percentage points |

| Interest (other) | 20.8%-21.84% | 15% | ~6 percentage points |

| Royalties (IP) | 20.8%-21.84% | 15% | ~6 percentage points |

| Royalties (equipment) | 20.8%-21.84% | 10% | ~11 percentage points |

| Fees for Technical Services | 20.8%-21.84% | 15% | ~6 percentage points |

India's DTAA network is one of the largest in Asia, covering over 94 comprehensive agreements and 8 limited agreements globally. For UK businesses, that breadth means treaty protection applies across most jurisdictions where group entities or counterparties are based—reducing exposure to double taxation at multiple points in a transaction chain.

The India-UK DTAA: Key Provisions UK Businesses Need to Know

Treaty Framework and MLI Modifications

India and the UK signed their Comprehensive DTAA on 25 January 1993, which entered into force on 25 October 1993. This treaty has been significantly modified by the Multilateral Instrument (MLI) under the OECD's BEPS (Base Erosion and Profit Shifting) framework, with MLI provisions taking effect for withholding taxes from 1 April 2020 (India) and 1 January 2020 (UK).

The MLI introduced critical anti-abuse provisions, most notably the Principal Purpose Test (PPT). This test allows tax authorities to deny treaty benefits if one of the principal purposes of an arrangement was to obtain those benefits. Granting them must also align with the treaty's object and purpose. For UK businesses, this means cross-border structures must demonstrate genuine commercial substance beyond tax optimisation.

Withholding Tax Rates Under the India-UK DTAA

The treaty establishes reduced rates for the most common income types UK businesses encounter:

Interest (Article 12):

- 10% for interest paid to bona fide banks

- 15% for all other cases

Dividends (Article 11):

- 10% in general cases

- 15% for income from immovable property via investment vehicles

Royalties (Article 13):

- 15% for intellectual property rights (copyrights, patents, trademarks)

- 10% for industrial, commercial, or scientific equipment use

Fees for Technical Services (Article 13):

- 15% for general technical services

- 10% for services ancillary to equipment rental

Interest and dividends paid to government entities, the Reserve Bank of India, or UK Export Credits Guarantee Department are fully exempt from source-country taxation.

Permanent Establishment (PE) Thresholds

A UK business is only subject to Indian corporate tax on business profits if it establishes a Permanent Establishment in India. The India-UK DTAA defines several PE triggers:

Service PE thresholds (Article 5):

- More than 90 days of service provision within any 12-month period (general threshold)

- More than 30 days when services are provided to associated enterprises

- More than 6 months for construction projects

This is critical for UK IT, consulting, and engineering firms deploying staff to India. Once the threshold is breached, the UK entity faces Indian business profits tax — not just withholding tax on fees — creating far greater compliance obligations.

A practical note on day counting: time spent on vacation, business development, or non-service activities in India is generally excluded from the threshold calculation. UK businesses should document the nature of each India visit carefully to support this position.

Capital Gains Provisions

Under Article 14 of the India-UK DTAA, India retains full taxing rights on capital gains in accordance with its domestic law, except for gains from aircraft and ships. This means UK businesses selling shares in Indian companies face Indian capital gains tax.

Unlike the Mauritius and Singapore treaties — which originally exempted capital gains but were amended in 2016 — the India-UK treaty has always preserved source-state taxation on share disposals. UK shareholders planning exits from Indian investments should factor Indian capital gains tax into deal structuring from the outset.

Residency Tie-Breaker Rules

When an individual or entity could be considered tax resident in both the UK and India, the treaty uses tie-breaker rules to determine primary taxing rights. Key factors include:

- Place of effective management

- Location of permanent home

- Centre of vital interests

- Habitual abode

This becomes particularly relevant for UK businesses incorporating Indian subsidiaries or having directors who travel frequently between both countries. In practice, a UK company whose key management decisions are made in India — even informally, in board calls or director visits — risks being treated as Indian tax resident, with all the filing obligations that follow.

Complete List of India DTAA Countries with Withholding Tax Rates

India has signed comprehensive DTAAs with over 94 countries, with TDS rates on interest typically ranging from 7.5% to 15% depending on the treaty. The rates shown below represent the maximum withholding tax on interest income under each DTAA; rates for dividends, royalties, and fees for technical services may differ and should be verified against specific treaty texts.

Important note: Under Section 90(2) of India's Income Tax Act, taxpayers may apply the more beneficial of the DTAA rate or the domestic rate. Where the domestic rate is lower, that rate applies.

Comprehensive DTAA Countries and Interest Withholding Rates

| Country | Interest TDS Rate | Country | Interest TDS Rate |

|---|---|---|---|

| Armenia | 10% | Lithuania | 10% |

| Australia | 15% | Luxembourg | 10% |

| Austria | 10% | Malaysia | 10% |

| Bangladesh | 10% | Malta | 10% |

| Belgium | 10%/15% | Mauritius | 7.5% |

| Botswana | 10% | Mongolia | 15% |

| Brazil | 15% | Montenegro | 10% |

| Bulgaria | 15% | Morocco | 10% |

| Canada | 15% | Mozambique | 10% |

| China | 10% | Myanmar | 10% |

| Cyprus | 10% | Namibia | 10% |

| Czech Republic | 10% | Nepal | 15% |

| Denmark | 10%/15% | Netherlands | 10% |

| Egypt | 10% | New Zealand | 10% |

| Estonia | 10% | Norway | 10% |

| Finland | 10% | Oman | 10% |

| France | 10% | Philippines | 10%/15% |

| Georgia | 10% | Poland | 10% |

| Germany | 10% | Portugal | 10% |

| Hungary | 10% | Qatar | 10% |

| Iceland | 10% | Romania | 15% |

| Indonesia | 10% | Russia | 10% |

| Ireland | 10% | Saudi Arabia | 10% |

| Israel | 10% | Serbia | 10% |

| Italy | 15% | Singapore | 10%/15% |

| Japan | 10% | Slovenia | 10% |

| Kazakhstan | 10% | South Africa | 10% |

| Kenya | 15% | South Korea | 15% |

| Kuwait | 10% | Spain | 15% |

| Country | Interest TDS Rate | Country | Interest TDS Rate |

|---|---|---|---|

| Sri Lanka | 10% | Turkmenistan | 10% |

| Sudan | 10% | UAE | 5%/12.5% |

| Sweden | 10% | Uganda | 10% |

| Switzerland | 10% | UK | 10%/15% |

| Syria | 7.5% | Ukraine | 10% |

| Tajikistan | 10% | USA | 10%/15% |

| Tanzania | 12.5% | Uzbekistan | 15% |

| Thailand | 25% | Vietnam | 10% |

| Trinidad & Tobago | 10% | Zambia | 10% |

| Turkey | 15% |

UK Businesses: Your Treaty Position

The India-UK treaty rate of 10% for bank lending and 15% for other interest compares extremely favourably with India's domestic TDS effective rate of 20.8%-21.84%. This represents a saving of approximately 6-11 percentage points on every cross-border interest payment.

To access this preferential rate, UK businesses must hold a valid Tax Residency Certificate (TRC) from HMRC and file Form 10F electronically on India's Income Tax portal. Without these documents, the Indian payer will deduct TDS at the full domestic rate of 20.8%-21.84%.

Limited DTAAs and Tax Information Exchange Agreements

India maintains 8 Limited DTAAs covering only shipping and airline income with:

India maintains 8 Limited DTAAs covering only shipping and airline income with:

- Afghanistan

- Ethiopia

- Lebanon

- Maldives

- Pakistan

- Yemen

India has also concluded Tax Information Exchange Agreements (TIEAs) with 21 jurisdictions, including Cayman Islands, Bermuda, Isle of Man, Jersey, Bahamas, and British Virgin Islands. These TIEAs facilitate information sharing only — they carry no withholding tax relief. UK businesses using holding structures in these jurisdictions remain fully exposed to India's domestic TDS rates and should restructure accordingly.

How to Claim India DTAA Benefits: A Step-by-Step Guide for UK Businesses

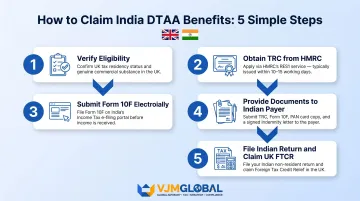

DTAA benefits don't apply automatically. UK businesses must complete specific compliance steps before payment is made. Here's the complete process:

Step 1 – Verify Eligibility

Confirm your UK business is a tax resident of the UK (not merely incorporated there) and that the income type falls within the India-UK DTAA's scope. Under the MLI's Principal Purpose Test, only UK residents with commercial substance can claim treaty benefits. Shell companies or entities structured primarily for tax advantage risk denial of benefits.

Key eligibility criteria:

- UK tax residency status (not just registration)

- Income covered by the treaty (business profits, interest, dividends, royalties, FTS)

- Beneficial ownership of the income (not acting as conduit)

- Commercial substance in the UK (real operations, not just mailbox)

Step 2 – Obtain a Tax Residency Certificate from HMRC

A Tax Residency Certificate (TRC) is legally required under Sections 90 and 90A of India's Income Tax Act before an Indian payer can apply the reduced DTAA rate.

Apply online via HMRC's RES1 service. You'll need to specify the India-UK DTAA, confirm beneficial ownership of the income, and confirm you're subject to UK tax on it. Newly incorporated companies must also provide director and shareholder details.

HMRC typically issues certificates within 10-15 working days.

The certificate confirms your UK tax residency status for the specified period and income types.

Step 3 – Submit Form 10F Electronically

Since 16 July 2022 (CBDT Notification No. 3/2022), Form 10F must be filed electronically on India's Income Tax e-filing portal. This mandate effectively requires UK businesses to obtain an Indian PAN (Permanent Account Number) first.

Form 10F requirements (Rule 21AB):

- Name of the taxpayer

- Status (individual/company/firm)

- Nationality or country of incorporation

- Tax identification number (UK UTR or Company Registration Number)

- Period of residential status in the UK

- Address in the UK

- Attach the HMRC-issued TRC

How to file:

- Obtain an Indian PAN (if you don't have one)

- Register on incometaxindiaefiling.gov.in

- Navigate to e-File > Income Tax Forms > Form 10F

- Complete the form and upload your TRC

- Submit electronically

Step 4 – Provide Documentation to the Indian Payer

The Indian entity making the payment (your client, subsidiary, or borrower) is responsible for deducting TDS at the correct treaty rate. You must provide documentation before the payment is made:

Documents to submit:

- Valid Tax Residency Certificate from HMRC

- Completed Form 10F acknowledgement from the e-filing portal

- Self-declaration/indemnity letter (often requested by the deductor)

- Copy of your Indian PAN

If these documents are not provided before payment, the Indian payer must deduct TDS at the higher domestic rate (20.8%-21.84%). The UK business can later seek a refund, but this adds significant time and compliance cost.

Step 5 – File Indian Tax Returns and Claim Credit in the UK

Where excess TDS was deducted (as described in Step 4), file an Indian income tax return to claim a refund of the excess amount. Indian tax authorities typically process refunds within 6-12 months.

To eliminate double taxation in the UK:

Claim Foreign Tax Credit Relief (FTCR) in your UK Corporation Tax or Self Assessment return for Indian taxes paid. The India-UK DTAA uses the credit method, letting you offset Indian tax against UK tax liability on the same income.

How to claim FTCR:

- Report the Indian-source income in your UK tax return

- Attach evidence of Indian tax paid (Form 26AS or TDS certificate)

- Use HMRC helpsheet HS263 for calculation guidance

- Claim credit up to the amount of UK tax on the same income

VJM Global has supported over 250 UK businesses through this process, handling everything from TRC applications and Form 10F filings to Indian tax return submissions and UK foreign tax credit claims. With 30+ years in Indian tax compliance, the firm provides practical support at every stage.

Common Mistakes UK Businesses Make When Using India's DTAA

Mistake 1 – Assuming DTAA Benefits Apply Automatically

Many UK businesses incorrectly assume the Indian payer will automatically apply the treaty rate. In practice, if the TRC and Form 10F are not provided before the payment date, TDS is deducted at the full domestic rate (20.8%–21.84%).

The UK business bears full responsibility for proactive documentation. Recovering over-deducted TDS means filing an Indian tax return and waiting 6–12 months for a refund, adding real compliance cost and cash flow pressure that correct upfront documentation avoids entirely.

Mistake 2 – Ignoring Permanent Establishment Risk

UK service companies—particularly IT, consulting, and engineering firms—frequently send teams to India for project-based work without tracking the 90-day service PE threshold. Once this threshold is breached, the UK company triggers a Permanent Establishment in India, subjecting business profits to Indian corporate tax (not just withholding tax on fees).

Example scenario: A UK consulting firm deploys three consultants to an Indian client site for a six-month transformation project. Each consultant spends 120 active service days in India over the contract period. This exceeds the 90-day threshold, triggering a PE. The UK firm now faces:

- Indian corporate tax return filing obligations

- Transfer pricing documentation requirements

- GST registration and compliance

- Payroll withholding for Indian-based activity

- Potential double taxation if UK-India profit allocation isn't properly documented

How to avoid:

- Track cumulative service days rigorously (exclude vacation and non-service days)

- Structure contracts to stay below 90 days per 12-month period

- Consider splitting projects across multiple tax years

- Document service allocation clearly in contracts

- Seek advance PE risk assessment for long-term projects

Careful day-counting is backed by law. A March 2024 Indian tribunal ruling confirmed that only active service days count (vacation, business development, and transit days are excluded). UK firms must maintain detailed time records to substantiate those exclusions if challenged.

Mistake 3 – Overlooking Post-MLI Changes to the India-UK Treaty

The Multilateral Instrument modified several provisions of the India-UK DTAA, including adding the Principal Purpose Test (PPT). UK businesses that establish holding structures or route income through India without genuine commercial substance now risk denial of treaty benefits.

CBDT Circular No. 01/2025 (issued 21 January 2025) clarified that PPT applies prospectively from 1 April 2020 and on a fact-specific, case-by-case basis. While grandfathered transactions (such as shares acquired before 1 April 2017 under Mauritius/Singapore/Cyprus treaties) are protected, all new arrangements from April 2020 onwards are subject to PPT scrutiny.

What this means for UK businesses:

- Transactions must have a genuine commercial purpose, not just a tax benefit

- Holding company structures require demonstrable operational substance

- Structures with no commercial activity beyond tax routing face active challenge from Indian authorities

- Maintain written records of the business rationale behind every cross-border arrangement

The synthesised text of the India-UK DTAA (incorporating MLI changes) is available on the UK government's DTAA reference page and should be reviewed alongside the original 1993 treaty.

Frequently Asked Questions

Is there a double taxation agreement with India?

Yes, India has active DTAAs with over 94 countries, including the UK, USA, Australia, Germany, Singapore, and UAE. These agreements prevent the same income from being taxed twice and provide reduced withholding tax rates on cross-border income flows such as interest, dividends, royalties, and fees for technical services.

How to apply for DTAA in India?

To claim DTAA benefits in India, obtain a Tax Residency Certificate (TRC) from your home country's tax authority (HMRC for UK businesses) and file Form 10F electronically on India's Income Tax e-filing portal. Provide both documents to the Indian payer before payment is made to ensure the reduced treaty rate applies.

Which countries have DTAA with India?

India has active DTAAs with 94+ countries spanning Europe (UK, Germany, Netherlands), North America (USA, Canada), Asia-Pacific (Australia, Singapore, Japan), Middle East (UAE, Saudi Arabia), and Africa (South Africa, Mauritius). A full list with withholding tax rates is provided in this guide.

Does India have a DTAA with the USA?

Yes, India has a full DTAA with the USA, with withholding tax rates of 10% on interest paid to banks and 15% for other interest. The treaty covers dividends, royalties, capital gains, and fees for technical services.

Does India have a DTAA with Australia?

India has an active DTAA with Australia (15% on interest), modified by the Multilateral Instrument. Australian businesses must obtain a TRC from the Australian Tax Office and file Form 10F to claim treaty benefits in India — the same process as UK businesses.

Does India have a DTAA with Cyprus?

Yes, India has an active DTAA with Cyprus (10% on interest), with a synthesised text incorporating MLI changes available on the CBDT website. UK businesses using Cyprus in holding structures should ensure compliance with the Principal Purpose Test — failure to do so can result in treaty benefits being denied.

Need expert support navigating India DTAA compliance? VJM Global has assisted over 250 UK businesses with TRC applications, Form 10F filings, Indian tax return submissions, and DTAA planning. With 30+ years of experience and a 95% client retention rate, our team ensures you access every available treaty benefit while maintaining full compliance. Contact us at info@vjmglobal.com or call +91 9213397070 for a consultation.