Introduction

UK businesses operating in India face a real risk: paying tax on the same income twice. A UK company earning income from India could pay withholding tax to Indian authorities at source, then face UK corporation tax on those same profits.

The India-UK Double Taxation Avoidance Agreement (DTAA) resolves this. Originally signed on 25 January 1993 and amended by a 2012 Protocol, the treaty allocates taxing rights, sets reduced withholding tax rates, and establishes mechanisms to eliminate double taxation. Since the India-UK Free Trade Agreement signed in July 2025, bilateral business activity is expected to surge—making DTAA compliance more urgent than ever.

This guide covers the treaty's key provisions in practical terms: withholding tax rates, Permanent Establishment (PE) rules, income categories, and exactly how to claim treaty benefits. Whether you're a UK parent company receiving dividends from an Indian subsidiary, a branch operating in India, or a service provider billing Indian clients, the sections below give you what you need to act correctly from the start.

TLDR:

- The India-UK DTAA caps withholding tax at 10–15% on dividends, interest, royalties, and fees for technical services—significantly lower than India's 20% domestic rate

- UK companies must obtain a Tax Residency Certificate from HMRC and file Form 10F to claim treaty benefits

- Permanent Establishment rules determine when India can tax UK business profits; thresholds include 6+ months for construction and 90+ days for service provision

- Anti-avoidance rules under the Multilateral Instrument's Principal Purpose Test now apply, so genuine commercial substance is required to access treaty benefits

- Relief methods under the treaty include both exemption and tax credit mechanisms, depending on the income type and the provisions claimed

What is the India-UK DTAA and Who Does It Apply To?

The India-UK DTAA is a bilateral tax treaty that prevents UK businesses from being taxed twice on the same income. Signed on 25 January 1993 in New Delhi, it entered into force on 26 October 1993 and became effective in India from 1 January 1994.

A subsequent Protocol signed on 30 October 2012 (effective 27 December 2013) introduced significant updates, including anti-abuse provisions and expanded information exchange.

The treaty operates under Section 90 of India's Income Tax Act, 1961. This provision allows UK-resident companies to choose the more beneficial rate—either the DTAA rate or India's domestic withholding rate. If the treaty rate is lower, it takes precedence.

Who the Treaty Covers

The DTAA applies to UK-resident companies liable to tax in the UK based on their:

- Place of incorporation

- Domicile

- Place of effective management

This includes:

- UK parent companies receiving dividends, interest, royalties, or technical service fees from Indian entities

- UK branch offices operating in India with a Permanent Establishment

- UK subsidiaries earning India-sourced income

- UK service providers billing Indian clients for consulting, IT, or managerial services

Taxes Covered

The treaty covers the following taxes in both jurisdictions:

In India:

- Income tax

- Surcharges on income tax

- Cess (currently 4% Health and Education Cess)

In the United Kingdom:

- Income tax

- Corporation tax

- Capital gains tax

- Petroleum revenue tax

Structure of the Treaty

The original Convention contained 31 articles. The 2012 Protocol made structural changes — it deleted Article 25 (Partnerships) and added three new articles:

- Article 28A — Tax Examinations Abroad

- Article 28B — Assistance in Collection of Taxes

- Article 28C — Limitation of Benefits

The treaty now comprises 33 articles covering different income categories and administrative provisions.

Income Types Covered Under the India-UK DTAA

The treaty governs how specific income categories are taxed. Understanding which article applies to your income type determines your withholding tax rate and taxing rights.

Main Business Income Categories

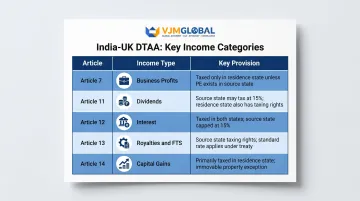

| Article | Income Type | Key Provision |

|---|---|---|

| Article 7 | Business Profits | Taxable only in UK unless a Permanent Establishment exists in India |

| Article 11 | Dividends | 10% general rate; 15% for immovable property investment vehicles |

| Article 12 | Interest | 10% for bank interest; 15% general rate; exempt for government payments |

| Article 13 | Royalties and Fees for Technical Services | 10% for equipment royalties; 15% for other royalties and FTS |

| Article 14 | Capital Gains | Each country taxes per domestic law (except shipping/air transport) |

The "Make Available" Condition for Technical Services

Article 13(4)(c) introduces a critical requirement for Fees for Technical Services (FTS): the services must "make available technical knowledge, experience, skill, know-how or processes" to the recipient. This means the Indian entity must be able to apply the transferred knowledge independently in the future.

To determine whether the condition is met, three criteria must hold:

- The service transfers specific technical knowledge, skill, or know-how

- The recipient can use that knowledge independently after the engagement ends

- The transfer is genuine — not just access to results or outputs

A UK IT consulting firm providing project management services that don't transfer underlying technical expertise won't trigger Indian withholding tax under the FTS provisions.

This interpretation was confirmed in ESAB Holding Limited v DCIT (Mumbai ITAT, 24 October 2024), where the tribunal ruled that managerial services provided by a UK company to its Indian subsidiary were not taxable as FTS under Article 13.

The services didn't transfer technical knowledge the recipient could use independently. Without a PE in India, the income also fell outside Article 7 — leaving it untaxed in India entirely.

This "make available" standard is unique to certain Indian treaties (including India-UK, India-US, India-Singapore). Treaties without this clause — such as India-France or India-Germany — use broader definitions, meaning more payments qualify as taxable FTS.

Residual Income

Income types not specifically addressed by the treaty default to being taxable in the country of the taxpayer's residence. UK-resident companies retain UK tax rights on income not sourced in India.

Withholding Tax Rates Under the India-UK DTAA

When an Indian entity makes payments to a UK company, Indian Tax Deducted at Source (TDS) applies. The DTAA sets maximum withholding rates that are lower than India's domestic rates.

Why This Matters Now

India's Finance Act 2023 raised the domestic withholding tax rate on royalties and FTS from 10% to 20% (effective 1 April 2023). After adding the 5% surcharge and 4% Health and Education Cess, the effective domestic rate is approximately 21.84%.

The DTAA rate of 15% is now substantially better—making treaty compliance financially essential.

DTAA Withholding Tax Rates vs. Domestic Rates

| Income Type | DTAA Rate | India Domestic Rate (Effective) | Savings |

|---|---|---|---|

| Dividends (general) | 10% | 21.84% | 11.84% |

| Dividends (immovable property) | 15% | 21.84% | 6.84% |

| Interest (bank) | 10% | 21.84% | 11.84% |

| Interest (general) | 15% | 21.84% | 6.84% |

| Royalties (equipment use) | 10% | 21.84% | 11.84% |

| Royalties (other) | 15% | 21.84% | 6.84% |

| Fees for Technical Services | 15% (with "make available" condition) | 21.84% | 6.84% |

Understanding Dividend Taxation

India abolished Dividend Distribution Tax (DDT) effective 1 April 2020. Previously, Indian companies paid DDT before distributing dividends, and shareholders received dividends tax-free. Now, dividends are taxable in the hands of the recipient.

For UK companies receiving dividends from Indian subsidiaries:

- India withholds tax at the DTAA rate (10% or 15%)

- The UK parent can claim a foreign tax credit against UK corporation tax

- Net effect: the same income isn't taxed twice

The treaty goes further than simply avoiding double taxation on dividends—it also protects the value of India's tax incentives through sparing provisions.

Tax Credit and Tax Sparing Provisions

Article 24(3) allows UK companies to claim credit for Indian taxes that were notionally waived under specific Indian incentive programmes (such as deductions under Sections 10A, 10B, or 80-IA of the Income Tax Act). This "tax sparing" relief is available for up to 10 fiscal years from when the exemption is first granted.

Practical Example:

An Indian subsidiary qualifies for a tax holiday under Section 10A. Even though no Indian tax is paid, the UK parent company can claim credit against UK corporation tax as if the Indian tax had been paid—preserving the value of India's tax incentive.

Claiming Foreign Tax Credit in the UK

UK companies can claim a credit for Indian TDS withheld, reducing UK corporation tax liability. The credit mechanism requires:

- Proper documentation of Indian tax paid (TDS certificates, Form 16A)

- Timely filing in both jurisdictions

- Ensuring the income is included in both Indian and UK tax returns

Missing documentation is the most common reason claims are rejected—get Form 16A from your Indian payer before filing UK returns.

Permanent Establishment Rules: Critical for UK Businesses in India

A Permanent Establishment (PE) is the threshold that gives India the right to tax a UK company's business profits. If your operations create a PE in India, the profits attributable to that PE become taxable in India. This includes the portion of global profits linked to Indian operations, not just income directly sourced there.

PE Definition Under Article 5

A PE is a fixed place of business through which a UK enterprise wholly or partly carries on business in India. This includes:

- Branch offices

- Factories

- Workshops

- Warehouses used for sales

- Mines, oil wells, quarries

- Places of management

PE Thresholds That Matter to UK Businesses

| PE Type | Threshold | Example |

|---|---|---|

| Construction/Installation PE | More than 6 months | A UK engineering firm managing a factory installation in India for 7 months triggers PE |

| Service PE (general) | More than 90 days within any 12-month period | UK consultants physically present in India for 95 days providing services create PE |

| Service PE (associated enterprise) | More than 30 days within any 12-month period | Services provided to an Indian subsidiary by UK staff for 35 days trigger PE |

| Agency PE | A dependent agent habitually concluding contracts on behalf of the UK company | An Indian sales agent with authority to sign contracts creates PE |

Important: The construction/installation threshold under this treaty is more than 6 months — a common point of confusion. Confirm the applicable threshold for your specific project type before structuring India operations.

How PE Affects Tax Liability

Crossing one of these thresholds has direct consequences for your Indian tax obligations:

- Only profits attributable to the Indian PE are taxable in India—not the UK company's global profits

- Proper profit attribution requires arm's length pricing and transfer pricing documentation

- The PE must maintain separate accounts and file Indian income tax returns

Branch Office vs. Subsidiary

Branch Office:

- Legally part of the UK company

- Treated as a PE under the DTAA

- Profits attributable to the branch are taxed in India

- Requires profit attribution documentation

Indian Subsidiary:

- Separate legal entity, tax-resident in India

- Taxed under Indian domestic law as an Indian company

- Payments to the UK parent (dividends, royalties, interest) are subject to DTAA withholding rates

- No PE issues for the UK parent unless additional activities create one

MLI's Impact on PE Rules

India ratified the Multilateral Instrument (MLI) on 25 June 2019, which entered into force on 1 October 2019. The India-UK DTAA is a covered agreement under the MLI.

Key MLI modifications:

- Article 13 prevents artificial PE avoidance through "preparatory or auxiliary" activity exemptions—activities that form part of a cohesive business operation can no longer claim exemption

- Commissionnaire arrangements (where an agent sells in its own name but on behalf of a foreign principal) and independent agent status rules are now stricter under OECD BEPS Action 7

- Arrangements designed to artificially fragment operations or avoid PE status face increased scrutiny

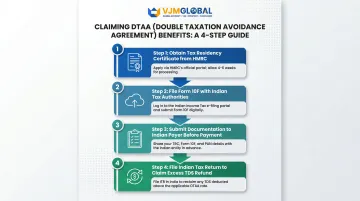

How to Claim DTAA Benefits as a UK Business

Without the right paperwork in place, Indian payers default to domestic withholding rates — which can be significantly higher than DTAA rates. Here's exactly what UK companies need to do before and after a payment is made.

Step 1: Obtain a Tax Residency Certificate (TRC) from HMRC

Under Section 90(4) of the Income Tax Act, 1961, a UK company must obtain a Tax Residency Certificate from HMRC to claim DTAA benefits. The TRC confirms that the company is resident in the UK for tax purposes.

How to obtain:

- Apply to HMRC using Form UK-Individual or UK-Company

- HMRC typically issues the TRC within 10-15 working days

- The TRC is valid for the financial year stated

Step 2: File Form 10F

Form 10F is a self-declaration required by Indian tax law. Since 16 July 2022, it must be filed electronically with Indian tax authorities.

Information required in Form 10F:

- Name and address of the UK company

- Tax Identification Number (UTR or Corporation Tax reference)

- Period of residency

- Tax year for which benefits are claimed

- Address and status of the taxpayer

Form 10F can now be filed without a PAN (Permanent Account Number), though PAN is required for filing Indian income tax returns.

Step 3: Provide Documentation to the Indian Payer

Before the payment is made, the UK company must provide the Indian payer with:

- Valid Tax Residency Certificate

- Completed Form 10F (proof of e-filing)

- Self-declaration of beneficial ownership

- Certificate of incorporation (if requested)

The Indian payer uses this documentation to deduct TDS at the applicable DTAA rate rather than the domestic rate.

Step 4: If Excess TDS Has Already Been Deducted

If the Indian payer has already deducted tax at the higher domestic rate, the UK company can:

- File an Indian income tax return claiming the excess as a refund

- The deadline for companies is 31 October of the assessment year (or 30 November if transfer pricing provisions apply)

Form 15CA and 15CB Requirements

The Indian payer also carries separate filing obligations. For remittances exceeding ₹5 lakh in a financial year, Section 195 and Rule 37BB require:

- Form 15CA — A pre-remittance declaration with four parts, depending on payment nature and whether a CA certificate or Assessing Officer order has been obtained

- Form 15CB — A Chartered Accountant certificate confirming payment details, applicable TDS rate, and nature of remittance

Engage Specialists for Complex Compliance

VJM Global has supported 250+ UK businesses through India's cross-border tax requirements, covering:

- TRC procurement and Form 10F e-filing

- Transfer pricing documentation for PE profit attribution

- Annual corporate tax return filing

- Advance rulings for rate certainty

- Representation before Indian tax authorities

Missing a procedural step — even a correctly calculated TDS rate — can trigger penalties or delayed refunds. Getting specialist support early avoids those costs.

Recent Developments Affecting UK Businesses

Finance Act 2023: Domestic Rate Increase

India's Finance Act 2023 doubled the withholding tax rate on royalties and FTS paid to non-residents from 10% to 20%, effective 1 April 2023.

Effective rates after surcharge and cess:

- Pre-1 April 2023: ~10.92%

- Post-1 April 2023: ~21.84%

For UK companies that previously relied on domestic rates, DTAA compliance is now non-optional. The treaty rate of 15% delivers a 6.84 percentage point saving—substantial for high-value payments.

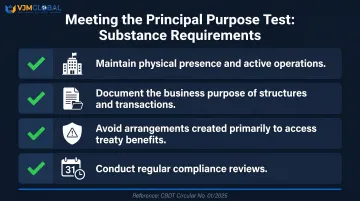

Principal Purpose Test (PPT) Now Operative

The MLI introduced the Principal Purpose Test into the India-UK DTAA via Article 7(1), replacing the original Article 28C (Limitation of Benefits). Under the PPT, Indian authorities can deny treaty benefits if obtaining those benefits was one of the principal purposes of an arrangement — and granting them would be contrary to the treaty's object and purpose.

CBDT Circular No. 01/2025 (issued 21 January 2025) clarified the PPT's application:

- Application is fact-specific and case-by-case

- Tax authorities must scrutinise commercial rationale before denying benefits

- PPT applies prospectively from the date MLI provisions entered into effect

Ensure your Indian operations and transactions have genuine commercial substance:

- Maintain physical presence and active operations

- Document the business purpose of structures and transactions

- Avoid arrangements created primarily to access treaty benefits

- Conduct regular compliance reviews

India-UK Free Trade Agreement (2025)

Alongside tightening treaty access rules, a separate bilateral development is reshaping the commercial landscape. The India-UK Free Trade Agreement was agreed in principle on 6 May 2025 and formally signed on 24 July 2025, concluding negotiations that launched on 13 January 2022.

Coverage:

- Tariff reductions on 90% of UK exports and 99% of Indian exports

- Services liberalisation across 36+ sectors

- Government procurement access

- Intellectual property protections

Tax Implications:

The FTA contains no direct tax provisions interacting with the DTAA. It includes only a "Double Contribution Convention" addressing social security and National Insurance contributions for temporary workers—distinct from direct taxation.

The DTAA remains the governing framework for direct tax treatment — the FTA expands bilateral trade flows, but how that income is taxed continues to be determined by the treaty.

Frequently Asked Questions

What is the DTAA between India and the UK?

The India-UK DTAA is a bilateral tax treaty signed on 25 January 1993 (amended by a 2012 Protocol effective 27 December 2013) that allocates taxing rights on different income types, prevents double taxation, and allows tax credits. It applies to both individuals and corporate entities resident in either country.

What is the new treaty between India and the UK?

The treaty has not been replaced. The 2012 Protocol introduced anti-abuse provisions, and the Multilateral Instrument (effective 1 October 2019) has further modified several articles. The India-UK Free Trade Agreement (July 2025) covers goods and services only — it does not replace or alter the DTAA.

What tax rates apply under the India-UK DTAA?

Key withholding tax rates are: dividends at 10-15%, interest at 10-15%, royalties at 10-15%, and fees for technical services at up to 15%. These rates are significantly lower than India's current domestic withholding rate of approximately 21.84% (20% plus surcharge and cess) introduced by Finance Act 2023.

What does Article 12 of the India-UK DTAA cover?

Article 12 covers interest payments, capping withholding tax at 15% (10% for bank interest). Article 13 — which covers royalties and fees for technical services — includes the critical "make available" condition: technical knowledge must be genuinely transferred to the recipient for FTS provisions to apply.

What does Article 14 (capital gains) of the India-UK DTAA cover?

Article 14 provides that capital gains are generally taxed according to the domestic laws of the country where the asset is situated or the gain arises. There are specific rules for immovable property, PE assets, and shares. There is no blanket capital gains exemption—India retains full taxing rights on gains arising in India.

How can you avoid double taxation between India and the UK?

Two mechanisms apply:

- Apply DTAA rates at source by submitting a Tax Residency Certificate and Form 10F to the Indian payer before payment

- Claim a foreign tax credit in the UK for Indian taxes paid, supported by proper documentation