Introduction

UK businesses earning income from India face a persistent challenge: the risk of paying tax on the same income twice—once to Indian authorities and again to HMRC. According to recent data, India's domestic withholding tax rates on cross-border payments can reach 20% plus surcharge and cess for royalties and fees for technical services, well above the rates available under the treaty.

While the India-UK Double Taxation Avoidance Agreement (DTAA) exists specifically to prevent this dual burden, claiming relief is not automatic. UK businesses must navigate correct documentation, precise filing sequences, and accurate identification of which relief mechanism applies to their specific income stream. Missing even a single required form can lock in higher domestic TDS rates that take months to recover.

What follows covers exactly that: who qualifies under the UK-India DTAA, what documents must be in place before payments are made, how to file correctly, and which errors most commonly cause claims to fail.

Key Takeaways

- India and the UK maintain a comprehensive DTAA (signed 1993, fully in force post-Brexit) preventing double taxation

- Three relief mechanisms apply: income exemption, foreign tax credit (FTC), or reduced withholding rates (10–15% vs. the 20% domestic rate)

- Prerequisites include a Tax Residency Certificate from HMRC, e-filed Form 10F, and Form 67 for any FTC claim

- Relief rates differ by income type — dividends, royalties, and capital gains each fall under separate DTAA articles

- Most UK businesses overpay Indian tax due to documentation errors or citing the wrong DTAA article

What is the India-UK DTAA and How Does Double Taxation Relief Work?

A Double Taxation Avoidance Agreement is a bilateral treaty that determines which country has taxing rights over specific income types when the same income would otherwise be taxed in both the source country (India) and residence country (UK). These treaties prevent businesses from paying tax twice on the same profit.

The India-UK DTAA was signed on 25 January 1993 and entered into force on 25 October 1993. It remains fully operational post-Brexit and covers all major categories of cross-border income: business profits, dividends, interest, royalties, fees for technical services, and capital gains.

The treaty was updated by a 2013 Protocol — which tightened anti-avoidance provisions — and the 2020 Multilateral Instrument, which aligned it with the OECD's BEPS standards. Both changes affect how UK businesses structure Indian operations today.

Three Relief Mechanisms Available Under the India-UK DTAA

Exemption Method

If your UK business earns income from India without a Permanent Establishment there, that income stays out of India's tax base entirely. Under Article 7, business profits are taxable only in the UK — India has no claim on them. This is the cleanest outcome: one jurisdiction, one tax bill.

Foreign Tax Credit (FTC) Method

Where both countries tax the same income, the UK allows Indian tax paid to be credited against your UK corporation tax liability. Under TIOPA 2010 Section 18, the credit is capped at the lower of:

- Foreign tax actually paid, or

- UK corporation tax attributable to that income

This ensures you never pay more than the higher of the two countries' tax rates. Excess tax paid in India beyond treaty limits must be recovered through the Indian refund process, not through additional UK credits.

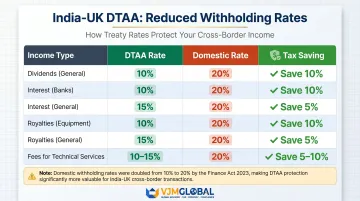

Reduced Withholding Tax Rates

India's domestic TDS rates for non-residents often reach 20% plus surcharge and cess. The DTAA cuts these substantially:

| Income Type | DTAA Rate | Domestic Rate | Saving |

|---|---|---|---|

| Dividends (general) | 10% | 20% | 10 percentage points |

| Interest (banks) | 10% | 20% | 10 percentage points |

| Interest (general) | 15% | 20% | 5 percentage points |

| Royalties (equipment) | 10% | 20% | 10 percentage points |

| Royalties (general) | 15% | 20% | 5 percentage points |

| Fees for Technical Services | 10-15% | 20% | 5-10 percentage points |

India's Finance Act 2023 doubled the domestic withholding rate on royalties and FTS from 10% to 20%, making treaty claims even more financially significant.

Treaty Override Principle: Section 90(2)

Section 90(2) of India's Income Tax Act 1961 gives UK businesses a valuable option. You can choose whichever treatment is more beneficial — the DTAA rate or India's domestic tax provisions — for each category of income. You are not locked into treaty rates if domestic law offers a better outcome.

How UK Businesses Can Claim Double Taxation Relief in India: Step-by-Step

The claim process follows a strict sequence. Reversing or skipping steps leads to denial of relief or excess TDS that can only be recovered through lengthy refund procedures.

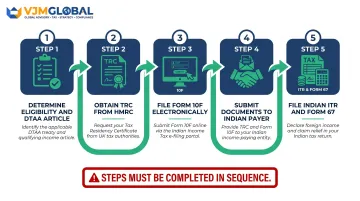

Step 1: Determine Eligibility and Identify the Applicable DTAA Article

First, confirm that:

- The transaction is taxable in both India and the UK

- Your UK entity qualifies as a non-resident for Indian tax purposes

- You can identify your income type (business profits, dividends, interest, royalties, capital gains)

Each income type corresponds to a specific DTAA article with different relief mechanisms:

| DTAA Article | Income Type | Rate / Treatment |

|---|---|---|

| Article 7 | Business Profits | Taxable only in the UK if no PE exists in India |

| Article 11 | Dividends | 10% withholding (15% for property investment vehicles) |

| Article 12 | Interest | 15% general; 10% for banks; 0% for government-guaranteed loans |

| Article 13 | Royalties / FTS | 10–15% depending on whether payments relate to industrial equipment use |

Misidentifying the income category is one of the most common errors UK businesses make—leading to application of the wrong rate or article.

Step 2: Obtain a Tax Residency Certificate (TRC) from HMRC

The TRC is mandatory documentation confirming your UK tax residency. Apply via HMRC's RES1 online service.

Your TRC must contain:

- Legal name and registered address

- UK tax identification number

- Period of residency covered

- Confirmation you are subject to UK tax on the income claimed

- Confirmation you are the beneficial owner of the income

For newly incorporated companies that haven't yet filed a UK tax return, you must provide names and addresses of all directors and shareholders. Indian tax authorities routinely deny DTAA benefits if your TRC is absent, expired, or incomplete.

Step 3: File Form 10F Electronically on India's Income Tax Portal

If your HMRC certificate doesn't contain all particulars required under Rule 21AB of India's Income Tax Rules, you must file Form 10F electronically on India's e-filing portal. This has been mandatory since 16 July 2022—paper forms are no longer accepted.

UK businesses without an Indian PAN can register using the 'Non-residents not holding and not required to have PAN' option on the portal, using your UK tax identification number instead.

File Form 10F before your Indian income tax return deadline and ideally before the Indian payer deducts TDS, as this maximizes your ability to claim reduced rates upfront.

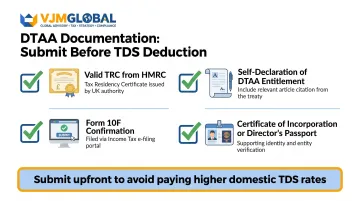

Step 4: Submit DTAA Documentation to the Indian Payer

Before your Indian counterparty deducts TDS, provide them with:

- Valid TRC from HMRC

- Self-declaration of DTAA entitlement citing the relevant article and reduced rate

- Form 10F confirmation

- Copy of certificate of incorporation or director's passport

Submitting these documents upfront allows the reduced DTAA rate to apply immediately, avoiding the cash flow impact of paying the higher domestic rate and waiting months for a refund.

Step 5: File Indian Income Tax Return and Form 67 (For FTC Claims)

UK businesses with taxable Indian income must file an Indian income tax return — ITR-6 for foreign companies. The filing deadline for audited companies is generally 31 October of the assessment year.

If you're claiming a foreign tax credit in the UK, file Form 67 before your ITR deadline. This form declares:

- Foreign income earned

- Indian taxes paid

- FTC amount being claimed in the UK

The FTC is capped at the lower of Indian tax paid or the UK tax that would apply to the same income. You cannot claim credit for tax paid in excess of treaty rates.

What UK Businesses Need Before Claiming Double Taxation Relief

Documentation gaps are the primary cause of DTAA claim failures. Most UK businesses that overpay Indian tax do so not because they're ineligible, but because they lack the right documents at the right time.

Required Documents and Registrations

- Tax Residency Certificate from HMRC (must be current and complete)

- Form 10F filed electronically on India's income tax portal

- Indian PAN card if you have ongoing India operations (optional for one-off transactions using the non-PAN portal route)

- Form 16A (TDS certificate from your Indian payer as proof of tax deducted)

- Form 67 if claiming FTC in the UK

- Self-declaration stating DTAA entitlement with specific article citation

A single missing item can trigger full domestic TDS at rates 5-10 percentage points higher than treaty-protected rates.

PE status is the other prerequisite that shapes everything. Before documents even come into play, your PE position determines whether India has the right to tax your business profits at all.

Understanding Permanent Establishment (PE) Status

The type of relief you qualify for—and how much India can tax—depends on whether you have a Permanent Establishment in India.

PE thresholds under Article 5 of the India-UK DTAA:

| PE Type | Threshold | Consequence |

|---|---|---|

| Construction PE | Project continuing more than 6 months | India can tax profits attributable to the PE |

| Service PE (general) | Employees present more than 90 days in any 12-month period | India gains taxing rights on service income |

| Service PE (associated enterprises) | More than 30 days in any 12-month period when working for/with related Indian entities | PE created at lower threshold |

| Agency PE | Dependent agent habitually exercising authority to conclude contracts | India can tax income generated through the agent |

With no PE, business profits are generally taxable only in the UK under Article 7. A PE created through a branch, dependent agent, fixed place of business, or extended employee presence gives India the right to tax profits attributable to that PE.

The 30-day threshold for service PE involving associated enterprises is the one most UK businesses underestimate. Staff deployed to work with Indian subsidiaries or related entities can create a PE faster than many finance teams realize — making presence-day tracking a compliance priority, not an afterthought. VJM Global's PE exposure analysis, drawn from working with 250+ UK businesses, helps identify these risks before they become tax liabilities.

Key Factors That Affect the Amount of Double Taxation Relief

Relief amounts are not fixed—they vary based on technical variables you must assess before filing.

Income Type and the Applicable DTAA Article

Different income streams follow different DTAA articles, each with prescribed treatment:

| Income Type | DTAA Article | Withholding Rate |

|---|---|---|

| Dividends | Article 11 | 10% (reduced from 15% by the 2013 Protocol) — a full 10 percentage point saving vs. the 20% domestic rate |

| Interest | Article 12 | 15% general; 10% for banks and financial institutions; 0% for government-backed or ECGD-guaranteed loans |

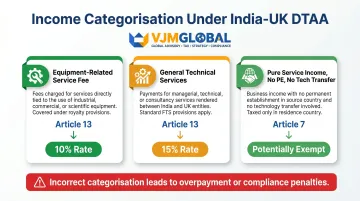

| Royalties and FTS | Article 13 | 15% general; 10% for royalties on industrial, commercial, or scientific equipment |

| Business Profits | Article 7 | Fully exempt if no PE exists; only profits attributable to the PE are taxable in India |

One categorisation trap worth noting: payments labelled as "service fees" may qualify as royalties or FTS under treaty definitions, triggering different rates and articles. Incorrect categorisation here is a frequent source of overpayment.

Tax Residency Determination and Tie-Breaker Rules

DTAA benefits apply only to entities that qualify as UK tax residents under the treaty. Residency is determined by where your company is incorporated and where effective management occurs—not merely where it is registered.

If a business has dual-residency characteristics (for example, incorporated in the UK but managed from India), Article 4(3) tie-breaker rules apply. The deciding factor is place of effective management (POEM) — entities are deemed resident only in the state where POEM is situated.

Obtain clear confirmation of your residency status before filing to avoid disputes.

Timing of Documentation Submission

Once residency is confirmed, the next variable is when you submit your documentation. Claiming reduced TDS upfront — by submitting documents to the Indian payer before deduction — is far more efficient than paying the higher domestic rate and claiming a refund later. Refunds can take 6–12 months to process and typically trigger scrutiny assessments.

For UK businesses with recurring India income — ongoing royalties, interest payments, or service fees — maintaining updated TRC and Form 10F filings annually is essential. Without current documentation, payers must default to the higher domestic withholding rate, creating immediate cash flow impact.

Common Mistakes UK Businesses Make When Claiming DTAA Benefits in India

Missing or Incorrectly Completing Form 10F and TRC Documentation

Submitting an expired TRC, an incomplete Form 10F, or failing to file Form 10F electronically before the ITR deadline are among the most frequently cited reasons for denial of DTAA-reduced rates.

A 2026 ITAT ruling held that DTAA benefits cannot be denied solely for delayed electronic filing of Form 10F, treating it as a procedural and curable defect. Still, timely filing remains best practice—it avoids disputes and ensures immediate access to reduced rates.

Misidentifying the Income Category and Applying the Wrong DTAA Article

A payment your contract labels as a "service fee" may qualify as a royalty or fee for technical services under treaty definitions. Common classifications under the UK-India DTAA include:

- Service fees related to equipment use: potentially 10% under Article 13

- General technical services: 15% under Article 13

- Pure service income with no technology transfer: possibly exempt if no PE exists

UK businesses that don't map each income stream to the correct DTAA article either under-claim relief (paying more tax than required) or claim under the wrong provision, creating compliance risk and potential penalties.

Failing to Assess Permanent Establishment Exposure Before Filing

Some UK businesses unknowingly create a PE in India through:

- Extended employee presence (exceeding 90 days, or just 30 days when working with associated enterprises)

- Dependent agents exercising contracting authority

- On-site project work lasting more than 6 months

Without a proper PE analysis, you may claim business profit exemption you're not entitled to, or miss the chance to restructure operations before PE exposure takes hold. India-specialist advisors like VJM Global can map your operational footprint against PE thresholds early, resolving exposure before it becomes a compliance problem.

Frequently Asked Questions

How to claim DTAA benefit in India?

To claim DTAA benefits in India, obtain a Tax Residency Certificate from HMRC, file Form 10F electronically on India's income tax portal, submit these documents to the Indian payer before TDS is deducted, and file an Indian ITR along with Form 67 if claiming foreign tax credit in the UK.

How to avoid double taxation on foreign income in India?

India's DTAA network and domestic provisions under Sections 90, 90A, and 91 of the Income Tax Act offer three main relief mechanisms: income exemptions, foreign tax credits, and reduced withholding rates. These apply as long as documentation requirements are met.

How does double taxation work in India?

Double taxation occurs when the same income is taxable both in India (as the source country) and in the UK (as the residence country). India's Income Tax Act and DTAA treaties address this by assigning taxing rights to one country, reducing applicable rates, or allowing tax credits to offset liability in the residence country.

What are the benefits of DTAA with NRIs?

DTAA benefits extend to foreign businesses and non-resident entities, not just NRIs. They can pay tax in only one jurisdiction, access reduced TDS rates on Indian-sourced income (interest, dividends, royalties), and avoid cash outflows from duplicate taxation.

Is DTAA available between India and the USA?

Yes, India has a comprehensive DTAA with the USA, which came into effect on 21 December 1990. The applicable treaty is determined by the tax residency of the entity receiving income—UK businesses should apply the India-UK DTAA specifically.

Can we file Indian income tax from the USA?

Yes, non-resident entities—including UK and US businesses—can file Indian income tax returns remotely through India's online income tax portal (incometax.gov.in). Foreign companies with Indian-sourced income are typically required to file an ITR in India regardless of DTAA claims.

Need Expert Support with India-UK DTAA Claims?

VJM Global has helped over 250 UK businesses manage India's cross-border tax compliance requirements, from PE exposure analysis to DTAA documentation and ITR filing. Our team of chartered accountants and international tax specialists helps you claim full relief while staying fully compliant.

Contact us at info@vjmglobal.com or call +91 9213397070 for a consultation on your India tax obligations.