Introduction

Since June 2023, Indian businesses operating in Dubai face a transformed tax environment. The UAE introduced corporate tax under Federal Decree-Law No. 47 of 2022, ending decades of near-zero taxation and establishing comprehensive transfer pricing rules for all related-party transactions. For the Mumbai-based company with a DMCC subsidiary or the Bengaluru IT firm with a Dubai sales office, every intercompany invoice now falls under Federal Tax Authority (FTA) scrutiny.

That scrutiny creates a distinct dual compliance challenge: satisfying both the UAE's FTA and India's Central Board of Direct Taxes (CBDT) for the same cross-border transaction. A management fee charged from India to Dubai must be priced and documented under two separate regulatory frameworks at once. The FTA has moved from education-first guidance to active enforcement — informal intercompany pricing arrangements no longer suffice.

TLDR:

- UAE corporate tax (effective June 2023) requires arm's length pricing for all India-UAE related-party transactions

- Indian businesses must maintain separate documentation for both UAE FTA and India CBDT compliance

- Free zone entities risk losing 0% tax status if transfer pricing rules aren't followed

- Documentation requirements start at AED 40 million in aggregate transactions; penalties reach AED 1,000,000 for serious violations

- Non-compliance exposes businesses to double taxation, as India and UAE adjustments may not automatically offset each other

What Is UAE Transfer Pricing and Why Does It Matter for Indian Businesses?

Transfer pricing governs the pricing of goods, services, loans, intellectual property, and other transactions between related entities within the same corporate group. Under Article 34 of the UAE CT Law, these prices must reflect what unrelated parties would agree to in comparable circumstances — the arm's length principle (ALP).

For Indian businesses, this affects transactions woven into typical India-UAE business structures:

- Mumbai headquarters charging management fees to a DMCC trading subsidiary

- Pune manufacturing company extending interest-free loans to its Dubai branch

- Delhi IT firm billing its Dubai sales office for software development services

- Chennai exporter licensing brand IP to a JAFZA distribution entity

Each transaction now requires arm's length justification and contemporaneous documentation.

The FTA has adopted a "self-review approach" that places responsibility on taxpayers to disclose adjustments proactively. Businesses must independently verify arm's length compliance — not simply rely on financial statements.

For Indian businesses already managing transfer pricing under India's Income Tax Act, the UAE framework adds a parallel layer: separate thresholds, different documentation formats, and UAE-specific methods that must be satisfied concurrently with Indian obligations.

The UAE Transfer Pricing Legal Framework: Key Rules Indian Businesses Must Follow

Three Primary Legal Sources

The UAE transfer pricing regime rests on three pillars, all aligned with OECD Transfer Pricing Guidelines — the same framework underpinning India's CBDT rules:

| Source | Date Issued | Role |

|---|---|---|

| Federal Decree-Law No. 47 of 2022 | 3 October 2022 | Primary legislation; Chapter 10 establishes transfer pricing rules |

| Ministerial Decision No. 97 of 2023 | May 2023 | Documentation thresholds and compliance requirements |

| FTA Transfer Pricing Guide | 23 October 2023 | Detailed guidance on method selection and benchmarking |

Related Parties vs. Connected Persons

The UAE distinguishes between two relationship categories, both subject to arm's length scrutiny:

- Related Parties (Article 35): Entities where one party holds 50%+ ownership, voting rights, board seats, or profit entitlement — covering the typical Indian parent-UAE subsidiary structure.

- Connected Persons (Article 36): Owners, directors, officers, and their relatives. Salaries, dividends, and other compensation paid to Indian promoters must meet market value standards.

In practice, this means an Indian promoter drawing salary from their Dubai entity triggers the same documentation obligations as intercompany service fees — a distinction many business owners overlook until an audit.

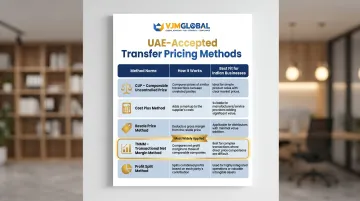

Five Accepted Transfer Pricing Methods

The UAE accepts five methods under Article 34(3), where taxpayers choose the method that best fits the transaction's facts and circumstances:

| Method | How It Works | Best Fit for Indian Businesses |

|---|---|---|

| Comparable Uncontrolled Price (CUP) | Compares intercompany price to unrelated-party prices in similar transactions | Commodity trading, standardized services |

| Cost Plus | Adds a market-rate markup to supplier costs | Manufacturing, contract services, back-office support |

| Resale Price | Subtracts an appropriate margin from the resale price | Distribution entities buying from related parties |

| Transactional Net Margin (TNMM) | Examines net profit margins against an appropriate base (sales, costs, or assets) | Most widely applied in UAE practice due to database availability |

| Profit Split | Allocates combined profits based on each party's contribution | Highly integrated operations or unique intangibles |

The methods mirror India's CBDT framework conceptually. The practical difference: UAE benchmarking relies on databases like Orbis and TP Catalyst rather than the Prowess/CMIE data common in Indian filings, so acceptable arm's length ranges can diverge even for identical transaction types.

QFZP Status and Transfer Pricing Compliance

Indian businesses frequently establish entities in UAE free zones — DMCC, JAFZA, DIFC — to access the 0% corporate tax rate available to Qualifying Free Zone Persons (QFZPs). However, QFZP status requires strict adherence to arm's length pricing. Failure to comply can result in loss of QFZP status, immediately subjecting the entity's entire income to the standard 9% corporate tax rate.

This creates a binary risk unique to UAE free zones: transfer pricing non-compliance doesn't just trigger penalties — it eliminates the foundational tax benefit.

Advance Pricing Agreements (APAs)

For businesses exposed to the QFZP risk above, APAs offer a way to lock in pricing certainty before an audit occurs. The FTA launched its APA programme in December 2025, currently accepting Unilateral APA applications for domestic related-party transactions. Key parameters:

- Minimum transaction value: AED 100 million per tax period

- Application fee: AED 30,000 (AED 15,000 for renewal)

- Coverage period: 3-5 years

- Mandatory prefiling consultation (6-9 months)

The AED 100 million threshold puts APAs out of reach for most mid-sized Indian groups — but for larger operations with recurring intercompany flows, they provide meaningful audit protection. Cross-border APAs, which would cover India-UAE transactions directly, are expected to open in 2026.

UAE Transfer Pricing Documentation Requirements and Thresholds

Key Compliance Thresholds

| Obligation | Threshold | Filing/Availability |

|---|---|---|

| Transfer Pricing Disclosure Form (TPDF) — Related Party Schedule | Aggregate transactions > AED 40 million; per-category disclosure > AED 4 million | Filed with CT return (within 9 months of year-end) |

| Connected Person Schedule | Aggregate CP transactions > AED 500,000 per person | Filed with CT return |

| Local File | UAE entity revenue ≥ AED 200 million OR group revenue ≥ AED 3.15 billion | Produced within 30 days of FTA request |

| Master File | Group consolidated revenue ≥ AED 3.15 billion | Produced within 30 days of FTA request |

| Country-by-Country Report | Group revenue ≥ AED 3.15 billion (~USD 858 million) | CbC Report within 12 months of year-end |

Transfer Pricing Disclosure Form (TPDF)

The TPDF must be filed alongside the corporate tax return — no later than nine months after the financial year-end. For Indian businesses with calendar-year accounting (year ending 31 December 2024), the deadline would be 30 September 2025.

Required disclosures include:

- Name and tax residence of each related party

- Transaction type and category

- Transfer pricing method applied

- Gross transaction value and arm's length value

- Any adjustments made to achieve arm's length pricing

Master File and Local File

The Master File gives regulators a group-level view of global transfer pricing policies, business structure, intangible assets, financing arrangements, and financial positions. It applies when consolidated group revenue exceeds AED 3.15 billion.

The Local File drills down to the UAE entity's own related-party transactions, covering:

- Detailed functional analysis (functions performed, assets used, risks assumed)

- Economic and industry analysis

- Comparability analysis and benchmarking data supporting arm's length pricing

- Financial information and intercompany agreements

Timing matters: Both files must be prepared contemporaneously — when transactions occur, not when an audit notice arrives. They must be ready to produce within 30 days of an FTA request. Retroactive compilation after an FTA inquiry is not an option.

Country-by-Country Reporting (CbCR)

Indian MNE groups with global consolidated revenue above AED 3.15 billion must file CbCR in the jurisdiction of the ultimate parent entity. If the Indian parent already files CbCR with India's CBDT, a separate UAE filing may still be required if the UAE entity qualifies as a reporting entity under local rules.

Across all documentation obligations, the burden of proof rests entirely with the taxpayer. Every file — TPDF, Local File, Master File, or CbCR — must affirmatively support the arm's length nature of transactions and be retained for the full statutory period.

VJM Global's cross-border tax team works with Indian businesses to build and maintain this documentation across both UAE and Indian requirements — so there are no gaps when either the FTA or India's tax authorities come asking.

The India-UAE Dual Compliance Challenge: Navigating Two Sets of Rules

Simultaneous Indian Transfer Pricing Obligations

Indian businesses don't receive a compliance waiver on the Indian side simply because a transaction is priced for UAE purposes. Section 92 of India's Income Tax Act requires all international transactions with associated enterprises to be priced at arm's length.

Form 3CEB — a CA-certified transfer pricing report — must be filed in India for transactions exceeding INR 1 crore (approximately USD 120,000).

This means:

- A management fee from Mumbai to Dubai must be documented for both UAE's TPDF and India's Form 3CEB

- Benchmarking studies must satisfy both FTA and CBDT standards

- Intercompany agreements must support arm's length claims in both jurisdictions

The India-UAE DTAA and Mutual Agreement Procedure

When the FTA makes an upward adjustment to a UAE entity's taxable income, the Indian parent may face economic double taxation unless it pursues a corresponding downward adjustment in India. The India-UAE Double Tax Avoidance Agreement includes a Mutual Agreement Procedure (MAP) to resolve such disputes.

MAP requests must be filed within three years of becoming aware of the dispute. To preserve MAP rights, maintain clear records of UAE transfer pricing adjustments and coordinate with advisors in both jurisdictions from the outset.

Key Methodological Differences

One key difference creates practical challenges:

| Jurisdiction | Arm's Length Benchmark | Legal Basis |

|---|---|---|

| India (CBDT) | Arithmetical mean of comparable prices | Section 92C: arm's length price is the arithmetic mean when multiple prices are determined |

| UAE (FTA) | Interquartile range (25th-75th percentile) | FTA TP Guide permits use of interquartile range or other statistical measures |

A transaction priced at the median of comparables may satisfy the UAE's interquartile range but fall outside India's arithmetic mean — or vice versa. Two approaches manage this gap:

- Overlap-zone benchmarking: Target a price point that satisfies both standards simultaneously

- Jurisdiction-specific documentation: Prepare separate studies for each jurisdiction, each demonstrating compliance under its own framework

Substance Requirements in Free Zones

Indian tax authorities now actively scrutinize UAE entities of Indian groups for substance — specifically whether they operate as genuine businesses or exist primarily to shift profits. UAE entities must have:

- Real physical presence (office space, not just virtual addresses)

- Employees performing substantive functions

- Independent decision-making authority

- Commercial rationale beyond tax benefits

Thin substance puts two things at risk simultaneously: QFZP status in the UAE (and the 0% tax rate that comes with it) and the entity's standing before the CBDT in India, where inadequate presence can trigger Permanent Establishment findings and profit reattribution to the Indian parent.

Common Transfer Pricing Risks Specific to Indian Businesses in Dubai

Management Fees and Shared Services

Many Indian groups charge Dubai subsidiaries for head-office services — HR, IT, legal, finance support — originating in India. The FTA scrutinizes these arrangements closely as a common profit-shifting mechanism. To withstand audit:

- The UAE entity must actually benefit from the service — generic "corporate overhead" allocations without demonstrable value face disallowance

- Cost-plus markups should reflect what third-party service providers would charge in the UAE market, not simply Indian cost allocations; in practice, markups typically range from 5–15% depending on service complexity

- Maintain records of services rendered, time spent, personnel involved, and how charges were calculated

Trading and Goods Transactions

Indian businesses using a Dubai trading entity to re-invoice goods exported from India to third-country buyers face heightened scrutiny from both Indian Customs/CBDT and the UAE FTA. Both authorities examine whether the margin retained in the UAE entity reflects genuine commercial substance and functions actually performed.

The Resale Price Method applies here: the UAE entity's gross margin should align with margins earned by independent distributors performing comparable functions. Watch for both directions of risk:

- Inflated margins — retaining excessive profit in the low-tax UAE entity draws FTA scrutiny

- Deflated margins — shifting profit back to India raises CBDT audit exposure

Intercompany Loans and Royalties

Interest-free or below-market loans represent the highest-risk transaction type under UAE transfer pricing rules. Key risks include:

- The FTA treats implicit financial support as a service that must be priced — interest-free loans can trigger notional income recognition in the lender's accounts or disallowance in the borrower's

- Extended trade receivables beyond normal credit periods: the FTA may reclassify these as loans subject to interest

- External benchmarks (SOFR, EURIBOR, EIBOR) and formal loan documentation — including terms, repayment schedules, and security — are expected

Royalties raise a distinct but related concern. Payments for use of an Indian parent's brand or IP by the UAE entity require explicit arm's length benchmarking. The FTA and CBDT both assess whether economic ownership of intangibles truly resides where claimed and whether licensing fees reflect market rates.

Practical Steps to Ensure Transfer Pricing Compliance in the UAE

Map and Classify All Related-Party Transactions

Begin with a comprehensive inventory:

- List every transaction between Indian and UAE entities (goods, services, loans, guarantees, IP licensing, management fees, rent, cost allocations)

- Quantify annual values for each transaction type

- Determine which UAE thresholds are triggered (TPDF, Connected Person Schedule, Local File)

This same inventory feeds directly into India's Form 3CEB preparation — so one structured exercise satisfies the documentation starting point for both jurisdictions.

Prepare a Transfer Pricing Policy and Contemporaneous Documentation

Develop a written transfer pricing policy specifying:

- Chosen method and rationale for each transaction type

- Benchmarking approach and data sources

- Adjustment mechanisms to maintain arm's length pricing

- Responsibility matrix (who maintains documentation, who reviews pricing annually)

Support the policy with a benchmarking study using regional (Middle East) comparables, as preferred by the UAE FTA. Execute formal intercompany agreements that reflect actual business conduct.

Note: Mismatches between written agreements and actual practice are among the most common triggers for FTA audit scrutiny — and the easiest to avoid with upfront alignment.

Seek Professional Guidance Early

The steps above — mapping transactions, selecting methods, preparing benchmarking studies, and drafting intercompany agreements — each carry different requirements under Indian and UAE rules. Getting them right across both frameworks at once is where many businesses run into gaps.

VJM Global works with Indian businesses operating in the UAE to build transfer pricing documentation that holds up under scrutiny from both the FTA and India's CBDT. Our services include:

- Dual-jurisdiction benchmarking studies addressing both UAE interquartile ranges and Indian arithmetic mean requirements

- Transfer pricing policy development aligned with both UAE and Indian regulatory expectations

- Documentation review and gap analysis for existing India-UAE structures

- TPDF and Form 3CEB preparation with coordinated disclosure strategies

- Representation and support during FTA and CBDT audits

Frequently Asked Questions

What is transfer pricing in Dubai?

Transfer pricing in Dubai (UAE) refers to pricing rules governing transactions between related companies or connected persons within the same group, established under Federal Decree-Law No. 47 of 2022. All such transactions must follow the arm's length principle and are overseen by the UAE Federal Tax Authority.

Do Indian businesses operating in a UAE free zone still need to follow transfer pricing rules?

Yes, free zone entities — including DMCC, JAFZA, and DIFC — must comply with UAE transfer pricing rules. Failing to price related-party transactions at arm's length can cause an entity to lose its QFZP status and become subject to the standard 9% corporate tax rate on all taxable income.

Does India's transfer pricing law apply to transactions with a UAE subsidiary?

Yes. Section 92 of India's Income Tax Act requires arm's length pricing for all international transactions with associated enterprises, including UAE subsidiaries. Form 3CEB must be filed with India's CBDT, creating dual compliance obligations on both sides.

What documents do Indian businesses need for UAE transfer pricing compliance?

Required documents include the Transfer Pricing Disclosure Form (filed with the CT return) and — depending on revenue thresholds — a Local File and Master File, both due within 30 days of an FTA request. Contemporaneous preparation is mandatory; backdating documentation after an audit begins is not accepted.

How does the India-UAE Double Tax Avoidance Agreement help in a transfer pricing dispute?

The India-UAE DTAA includes a Mutual Agreement Procedure (MAP) through which both tax authorities negotiate to eliminate double taxation arising from a transfer pricing adjustment. File a MAP request within three years of becoming aware of the dispute to seek a corresponding adjustment on the Indian side.

What penalties apply if an Indian business in Dubai violates UAE transfer pricing rules?

Penalties include AED 10,000 per documentation violation (AED 20,000 for repeat offences), up to AED 1,000,000 for CbCR non-compliance, and the risk of 9% corporate tax applying to the full taxable income of a free zone entity that loses its QFZP status.