Introduction

India's tax authorities audited transfer pricing cases involving billions in disputed adjustments last year — and UK multinationals are among the most scrutinised groups. Transfer pricing governs how related entities within a multinational group price their cross-border transactions, and India requires all such transactions to meet the "arm's length" standard under Sections 92–92F of the Income Tax Act, 1961.

That standard means each intercompany transaction must be priced as if it were between independent parties — preventing artificial profit shifting to lower-tax jurisdictions.

For UK-based multinationals with Indian subsidiaries or operations, compliance means satisfying both HMRC and the Central Board of Direct Taxes (CBDT) simultaneously. The penalties for getting it wrong are steep: up to 2% of each international transaction value, plus 200% of tax payable on misreported income, along with lasting reputational damage.

This guide covers India's transfer pricing legal framework, how arm's length pricing is determined, documentation obligations for UK companies, and practical strategies to reduce audit and penalty risk.

Key Takeaways

- India's TP rules apply to all international transactions with associated enterprises—no minimum value threshold exists

- UK multinationals must price intercompany transactions (goods, services, loans, royalties, IP) at arm's length using one of six prescribed methods

- Documentation includes Master File, Local File, and Country-by-Country Report, with Form 3CEB due by October 31

- Penalties reach 2% of transaction value for documentation failures, plus 50–200% of tax for under-reporting

- Advance Pricing Agreements, Safe Harbour Rules, and Mutual Agreement Procedure let UK multinationals lock in agreed pricing terms and avoid disputes with Indian tax authorities

What Is Transfer Pricing and How Does India Regulate It?

Transfer pricing is the process of setting prices for transactions between related entities (associated enterprises) within the same multinational group. Because tax rates vary across countries, these prices can be manipulated to shift profits to lower-tax jurisdictions, eroding India's tax base.

India's transfer pricing regime requires that income from such transactions be computed using the arm's length price (ALP): the price two unrelated, independent parties would agree on under comparable conditions. This is not the same as a simple "market price." Indian TP rules demand a structured comparability analysis rather than just referencing public price lists.

Key characteristics of ALP determination:

- Considers functions performed, assets employed, and risks assumed by each party

- Requires analysis of comparable uncontrolled transactions

- Uses statistical methods to establish acceptable pricing ranges

- Must be supported by contemporaneous documentation prepared before audit

India's TP regime aligns with OECD transfer pricing guidelines while maintaining India-specific requirements that often exceed international standards.

Why UK Multinationals Face Transfer Pricing Obligations in India

UK multinationals frequently engage in transaction types that trigger Indian TP rules:

- Management service fees charged by UK parent to Indian subsidiary

- Intellectual property royalties and software licensing

- Intercompany loans and financing arrangements

- Shared service arrangements for back-office functions

- Cost contribution agreements for R&D

India's Income Tax Department actively scrutinises these as high-risk categories because they represent common profit-shifting mechanisms. Whether any of these transactions trigger TP obligations depends on how Indian tax law defines the relationship between the two entities.

The Associated Enterprise Definition

Under Section 92A, two enterprises are associated if one participates (directly or indirectly) in the management, control, or capital of the other. Critical thresholds include:

- 26% or greater shareholding — the most common trigger for UK-India groups

- 51% or more of book value of total assets via loans

- 10% or more of total borrowings via guarantees

- More than 50% of directors appointed by the other enterprise

The 26% shareholding threshold is lower than many UK tax professionals expect, meaning even minority-owned Indian operations may trigger full TP compliance obligations.

Once the associated enterprise relationship is established, the compliance framework itself is where UK multinationals often encounter the most surprises.

Aligned but Not Identical Rules

The India-UK Double Tax Avoidance Agreement (DTAA) and OECD BEPS framework create aligned but not identical obligations. UK companies familiar with HMRC's TP rules must understand where Indian requirements are stricter, particularly around:

- Documentation timelines (India's October 31 Form 3CEB deadline is earlier than many OECD jurisdictions)

- Mandatory Chartered Accountant certification (Form 3CEB)

- Lower tolerance bands (±1% for wholesale trading versus ±3% for other transactions)

- Expanded disclosure requirements under the new Form 48 (effective FY 2026-27)

India's Transfer Pricing Legal Framework: Sections 92–92F Explained

Sections 92 to 92F of the Income Tax Act, 1961 form the statutory backbone of India's TP regime. These provisions are being reorganised under the Income Tax Act, 2025, effective April 1, 2026, with enhanced alignment to OECD standards and expanded coverage to digital assets and platform economies.

International Transactions Under Section 92B

An international transaction occurs between two or more associated enterprises where at least one is non-resident. Coverage includes:

- Purchase, sale, or lease of tangible and intangible property

- Provision of services

- Lending or borrowing

- Business restructuring

- Cost contribution agreements

The definition is wide enough to capture management fees, IT services, brand royalties, and guarantee arrangements typical in UK-India group structures. Transactions with third parties also fall within scope where a prior agreement exists with an associated enterprise.

Specified Domestic Transactions (Section 92BA)

Certain domestic related-party transactions are subject to TP rules when the aggregate value exceeds INR 20 crore in a financial year. These primarily involve profit-linked tax deductions under Chapter VI-A.

For UK multinationals that have restructured Indian operations into Special Economic Zones or other tax-incentive structures, this matters directly. Such arrangements can trigger domestic TP obligations on top of international TP requirements.

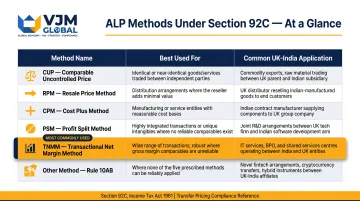

Arm's Length Price Methods

Section 92C prescribes six methods for computing ALP:

| Method | Best Used For | Common UK-India Application |

|---|---|---|

| Comparable Uncontrolled Price (CUP) | Identical transactions with unrelated parties | Intercompany loans, commodity transactions |

| Resale Price Method (RPM) | Distribution arrangements | UK goods sold through Indian distributors |

| Cost Plus Method (CPM) | Manufacturing and service contracts | Contract manufacturing, routine services |

| Profit Split Method (PSM) | Highly integrated operations | Joint R&D, shared IP development |

| Transactional Net Margin Method (TNMM) | Service transactions | IT services, back-office operations, KPO |

| Other Method | When prescribed methods unsuitable | Complex digital transactions |

TNMM is most commonly used for service transactions (IT, back-office, KPO) typical of UK-India arrangements, whilst CUP is preferred for intercompany loans. The taxpayer must select and justify the "most appropriate method" for the specific transaction type.

Range Concept and Tolerance Band

When the most appropriate method produces multiple data points using at least six comparables:

- The arm's length range is set at the 35th to 65th percentile

- If the tested price falls within this range, no adjustment is made

- If it falls outside, it is adjusted to the median

Tolerance bands apply before adjustment:

- ±1% for wholesale trading

- ±3% for other cases

The Finance Act 2025 signals a shift away from the arithmetic mean approach for determining ALP. UK multinationals should factor this into their 2025–26 TP planning and benchmarking exercises.

Transfer Pricing Documentation Requirements for UK-Based Entities

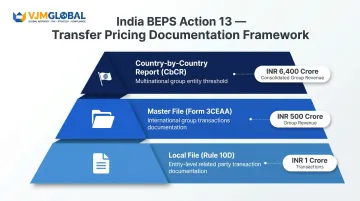

Three-Tier BEPS Action 13 Framework

India follows the OECD BEPS Action 13 three-tier documentation framework:

1. Master File (Form 3CEAA)

- Group-level overview of structure, supply chain, intangibles, and financing

- Required when consolidated group revenue exceeds INR 500 crore AND aggregate international transactions exceed INR 50 crore (or INR 10 crore for intangible property)

2. Local File (Rule 10D)

- Entity-level analysis of each controlled transaction

- Includes FAR analysis, pricing methodology, and benchmarking

- Required when aggregate international transactions exceed INR 1 crore

3. Country-by-Country Report (CbCR)

- Applies to groups with consolidated revenue above INR 6,400 crore (aligned with OECD EUR 750 million threshold)

- Filed annually with details of revenue, profit, tax paid, and economic activity by jurisdiction

Form 3CEB: The Accountant's Certificate

Every entity entering into international transactions must obtain Form 3CEB from a Chartered Accountant, confirming:

- Nature and value of all international transactions

- Arm's length compliance

- Methods used and justification

- Comparables selected

Critical deadlines:

- Form 3CEB due October 31 (one month before income tax return)

- Income tax return due November 30

From FY 2026-27, the new Form 48 requires enhanced disclosures including:

- Comparables data

- APA coverage details

- Royalty, financing, and guarantee agreements

- Business restructuring details

"Contemporaneous" means the Local File and supporting records must be prepared and in existence by the specified date — not reconstructed during an audit. Required documentation includes:

- Contracts and intercompany agreements

- Invoices and payment records

- Benchmarking studies

- Board resolutions

- FAR analysis

All documents must be retained for eight years from the end of the relevant assessment year.

Functional, Asset, and Risk (FAR) Analysis

FAR analysis forms the foundation of TP documentation and directly determines how profits are allocated across the group. It maps three dimensions of each entity's role:

- Functions: Which entity performs R&D, manufacturing, distribution, customer acquisition, and strategic decision-making

- Assets: Who owns IP, equipment, brands, customer relationships, and working capital

- Risks: Which entity bears market, credit, operational, foreign exchange, and regulatory risk

Profit allocation must be proportionate to this FAR profile. UK parent companies typically retain high-value functions and assets, so Indian subsidiaries are usually characterised as limited-risk service providers or contract manufacturers — with correspondingly lower profit margins.

For UK multinationals navigating these requirements for the first time, having local support for benchmarking studies (using Indian databases such as Prowess and Capitaline), Form 3CEB certification, and audit-ready record maintenance can significantly reduce compliance risk. VJM Global works with UK entities at each stage of this process, from initial FAR mapping through to final filing.

Penalties for Transfer Pricing Non-Compliance in India

India's penalty regime is multi-layered and severe:

Transactional Penalties

- Section 271AA: 2% of international transaction value for failure to maintain documentation, failure to report a transaction, or maintaining incorrect information

- Section 271BA: ₹10,00,000 (approximately £9,500) for failure to furnish Form 3CEB

- Section 271G: Additional 2% of transaction value for failure to furnish information when requested by Transfer Pricing Officer

Under-Reporting and Misreporting Penalties (Section 270A)

- Under-reported income: 50% of tax payable on the under-reported amount

- Misreported income: 200% of tax payable — applied to deliberate mispricing

That said, Section 270A(7) offers a meaningful escape route. Taxpayers can claim immunity from these penalties if they:

- Maintained prescribed documentation

- Reported the transaction

- Disclosed all material facts

- Determined price in good faith

In practice, this means thorough documentation filed on time can eliminate penalty exposure entirely — even where an adjustment is made.

Common Compliance Mistakes for UK Multinationals

- Using UK/European comparables rather than Indian comparables when required by regulations

- Applying global group TP policies without adapting to Indian regulatory requirements

- Missing the October 31 Form 3CEB deadline, resulting in an automatic ₹10,00,000 penalty

- Mischaracterising Indian entities (e.g., treating a limited-risk distributor as a full-risk entity), leading to inflated TP adjustments during audits

- Failing to update benchmarking annually, using outdated comparable data

- Not maintaining contemporaneous documentation (records prepared at the time of the transaction — attempting to reconstruct records during audit is a red flag for auditors)

Reducing Risk: APAs, Safe Harbour Rules, and MAP for UK Multinationals

Advance Pricing Agreements (APAs)

APAs are pre-emptive binding agreements between a taxpayer and CBDT that lock in the TP methodology for up to 5 prospective years, with the ability to roll back up to 4 years (9 years total certainty).

Types available:

- Unilateral (UAPA)

- Bilateral (BAPA)

- Multilateral (MAPA)

India signed a record 174 APAs in FY 2024-25, with the UK ranking as India's second-highest bilateral APA partner after the USA. This makes bilateral APAs a viable and increasingly used tool for UK groups seeking long-term certainty on Indian TP pricing.

Average processing times:

- Unilateral APAs: 35.76 months

- Bilateral APAs: 58.90 months

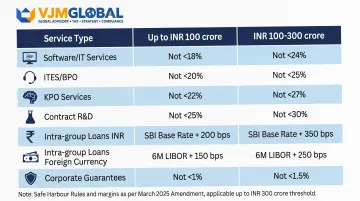

Safe Harbour Rules (Section 92CB)

Safe harbour provides predefined profit margins that, if met, are accepted by Indian tax authorities without further scrutiny. March 2025 amendments raised the transaction threshold to INR 300 crore and extended applicability through AY 2026-27.

Key margins for UK-India transactions:

| Service Type | Up to INR 100 crore | INR 100-300 crore |

|---|---|---|

| Software Development / IT Services | 17% on operating costs | 18% on operating costs |

| ITES / BPO | 17% on operating costs | 18% on operating costs |

| KPO Services | 24% on operating costs | 25% on operating costs |

| Contract R&D (Software) | 24% on operating costs | 25% on operating costs |

| Intra-group Loans (INR) | SBI MCLR + 175 basis points | - |

| Intra-group Loans (Foreign Currency) | SOFR/EURIBOR + 150bp | SOFR/EURIBOR + 300bp |

| Corporate Guarantees | 1% p.a. | 1.75% p.a. |

For UK multinationals with Indian IT service captives or R&D centres, safe harbour election can significantly reduce audit risk and compliance burden.

Mutual Agreement Procedure (MAP)

MAP under the India-UK DTAA provides recourse when transfer pricing adjustments by Indian authorities create double taxation. The UK and Indian competent authorities negotiate to resolve the discrepancy.

India's updated MAP rules (2020) target a 24-month resolution timeline. Key points to factor into your decision:

- Targets resolution within 24 months of initiating the procedure

- Available when Indian TP adjustments result in double taxation under the DTAA

- Companies electing safe harbour treatment cannot simultaneously invoke MAP

- The choice between MAP and safe harbour must reflect transaction complexity, audit exposure, and long-term plans

VJM Global helps UK multinationals evaluate which mechanism — APA, safe harbour, or MAP — is the right fit given their transaction profile, audit history, and India growth plans.

Frequently Asked Questions

Is transfer pricing mandatory in India?

Yes, transfer pricing compliance is mandatory for all international transactions between associated enterprises regardless of value, and for specified domestic transactions exceeding INR 20 crore. There is no minimum threshold for international transactions, making it applicable even to small intercompany service arrangements.

What is the threshold for transfer pricing documentation and audit in India?

Full documentation under Rule 10D is required when aggregate international transactions exceed INR 1 crore. Master File obligations apply when group revenue exceeds INR 500 crore (with international transactions above INR 50 crore), and Country-by-Country Reporting applies to groups with consolidated revenue above INR 6,400 crore.

What does Section 92 of the Income Tax Act say about transfer pricing?

Section 92 requires any income arising from an international transaction to be computed with reference to the arm's length price. Allowances for expenses or interest from such transactions must also be determined at ALP, but TP provisions only apply where they increase (not decrease) taxable income in India.

What is a specified domestic transaction referred to in Section 92BA?

A Specified Domestic Transaction (SDT) is a domestic related-party transaction—not an international transaction—that involves profit-linked tax deductions under Chapter VI-A. TP rules apply only when the aggregate value of all such transactions exceeds INR 20 crore in the financial year.

What are the penalties for transfer pricing non-compliance in India?

Three primary penalty provisions apply:

- Section 271AA: 2% of international transaction value for documentation failures or incorrect reporting

- Section 271BA: INR 1,00,000 for failure to file Form 3CEB

- Section 270A: 50–200% of tax payable for under-reporting or misreporting income due to TP adjustments

How can businesses avoid transfer pricing penalties in India?

Key steps to stay compliant:

- Prepare TP documentation as transactions occur — not retrospectively

- File Form 3CEB by the October 31 deadline each year

- Conduct annual benchmarking using Indian comparables

- Consider Safe Harbour elections or Advance Pricing Agreements for greater certainty

- Work with India-experienced advisors familiar with CBDT audit triggers for foreign-parented entities