Introduction

Singapore companies are increasingly drawn to UAE free zones as strategic hubs for expansion into the Middle East and African markets. Nearly 400 Singaporean companies now operate in DMCC alone, reflecting 13% year-on-year growth and more than half of all Singapore business presence in the UAE. The appeal is clear: 100% foreign ownership, zero withholding tax on profit repatriation, and access to the Qualifying Free Zone Person (QFZP) 0% corporate tax rate on qualifying income.

These incentives, however, come with rigorous compliance obligations. UAE free zone entities must:

- Maintain IFRS-compliant financial statements

- Register for corporate tax regardless of QFZP status

- Submit annual audits to most Free Zone Authorities

- Navigate VAT, Economic Substance Regulations (ESR), and transfer pricing rules under both UAE and Singapore law

Singapore's Foreign-Sourced Income Exemption (FSIE) regime also excludes UAE free zone income, because the UAE's 9% headline rate falls below Singapore's 15% threshold. That means Singapore parent companies face potential tax exposure on repatriated profits, even with the Singapore-UAE Double Tax Treaty in place.

This guide walks Singapore company owners and finance teams through every core UAE free zone accounting requirement. Topics covered include bookkeeping standards, QFZP status conditions, audit timelines, cross-border transfer pricing compliance, and the critical interaction between UAE corporate tax law and IRAS guidelines.

Key Takeaways

- UAE free zone companies must maintain IFRS-compliant financial records and retain them for seven years (not five).

- The 0% corporate tax rate requires meeting all seven QFZP conditions — missing any single one triggers the 9% standard rate.

- Most major free zones require annual audited financial statements for license renewal, with deadlines varying by zone.

- VAT registration is mandatory once taxable supplies exceed AED 375,000 annually, with designated zone rules affecting logistics and trade entities.

- Singapore companies face dual transfer pricing compliance under both UAE CT law and IRAS Section 34D for intercompany transactions.

Why Singapore Companies Set Up in UAE Free Zones

UAE free zones offer Singapore companies a powerful geographic advantage: direct access to GCC and African markets, 100% foreign ownership, zero restrictions on profit repatriation, and historically low-tax operating environments. Bilateral merchandise trade between Singapore and the UAE reached S$24 billion in 2024, with Singapore investments into the UAE totalling S$4.9 billion in 2023. The GCC-Singapore Free Trade Agreement (GSFTA) further strengthens this corridor.

The Singapore Tax Interaction

Singapore's territorial tax system appears to complement UAE free zone benefits, but the reality is more complex. Under the IRAS e-Tax Guide on Foreign-Sourced Income Exemption (FSIE), three cumulative conditions must all be satisfied:

- The income must have been subject to tax in the foreign jurisdiction

- The foreign jurisdiction's headline corporate tax rate must be at least 15%

- The Comptroller must be satisfied the exemption is beneficial

The UAE's highest corporate tax rate is 9% — below the 15% threshold. This means FSIE exemption is unavailable for UAE free zone income remitted to Singapore, regardless of QFZP status.

Since the QFZP rate is 0%, there is also no foreign tax to credit under Singapore's Section 50 Double Taxation Relief. Singapore companies must therefore carefully structure profit repatriation and manage the timing and form of income recognition to limit Singapore tax exposure.

Because neither the FSIE exemption nor a foreign tax credit is available, UAE-side accounting and documentation carry direct Singapore tax consequences. Singapore parent companies need clear audit trails, qualifying income segregation, and transfer pricing documentation to substantiate both UAE QFZP claims and Singapore tax positions.

Core Bookkeeping and Financial Record-Keeping Requirements

Legal Foundation

All UAE free zone companies are legally required under Federal Decree-Law No. 47 of 2022 (UAE Corporate Tax Law) to maintain accurate, complete, and up-to-date books of account that clearly document every financial transaction. This applies regardless of company size or revenue — it is not optional.

Accounting Standards

Financial statements must be prepared in accordance with International Financial Reporting Standards (IFRS) or IFRS for SMEs. Ministerial Decision No. 114 of 2023 establishes revenue-based thresholds:

| Revenue Threshold | Accounting Method |

|---|---|

| Up to AED 3,000,000 | Cash basis permitted |

| AED 3,000,001 to AED 50,000,000 | IFRS for SMEs |

| Above AED 50,000,000 | Full IFRS |

Singapore companies should note that Singapore FRS, while converged with IFRS, differs in certain areas. UAE-side financial statements must be prepared under full IFRS as required by UAE law and the respective Free Zone Authority — not Singapore FRS or US GAAP.

Record Retention

Article 56 of Federal Decree-Law No. 47 of 2022 mandates a minimum seven-year retention period for all accounting records and supporting documents after the end of the relevant financial period. This covers:

- Invoices and receipts

- Contracts and bank statements

- General ledgers and journals

Missing documentation can trigger penalties during FTA reviews — this is a hard legal requirement, not a best practice.

Qualifying vs. Non-Qualifying Income Segregation

Revenue segregation must be built into the chart of accounts and accounting software from day one — it is foundational to maintaining QFZP status. Free zone companies must track:

- Qualifying income (transactions with other free zone persons, manufacturing, logistics, fund management, etc.)

- Non-qualifying income (mainland UAE transactions, excluded activities)

- De minimis threshold monitoring (non-qualifying revenue must not exceed the lower of 5% of total revenue or AED 5,000,000)

Software and Outsourcing

Cloud-based accounting software configured for UAE VAT and corporate tax requirements — such as Xero, QuickBooks, or Zoho Books — is strongly recommended. Singapore companies with remote management structures particularly benefit from real-time access to UAE entity financials.

Outsourcing UAE accounting to a firm with cross-border expertise keeps IFRS, VAT, and corporate tax reporting on track without adding headcount to your Singapore operations.

Corporate Tax Position of UAE Free Zone Companies

UAE Corporate Tax applies to all businesses, including free zone companies, at the following rates:

- 0% on taxable income up to AED 375,000

- 9% on taxable income exceeding AED 375,000

The QFZP framework allows eligible free zone entities to apply a 0% rate on qualifying income, but this is conditional and requires meeting seven cumulative conditions.

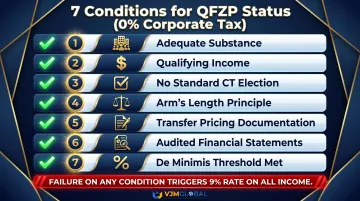

Qualifying Free Zone Person (QFZP) Status

Per the FTA Corporate Tax Guide for Free Zone Persons (CTGFZP1, May 2024), a Free Zone Person must satisfy all of the following to qualify as a QFZP:

- Maintain adequate substance in a Free Zone (undertake Core Income-Generating Activities in a Free Zone with adequate employees, assets, and operating expenditures)

- Derive Qualifying Income

- Not elected to be subject to standard CT rates (Article 19)

- Comply with the arm's length principle (Article 34)

- Maintain Transfer Pricing documentation (Article 55)

- Maintain audited Financial Statements

- Non-qualifying revenue meets the de minimis threshold: must not exceed the lower of 5% of total revenue or AED 5,000,000

Failure on any single condition in a tax period results in the full 9% rate applying to all income.

Qualifying Income and Excluded Activities

Qualifying Activities (per Ministerial Decision No. 265 of 2023) include:

- Manufacturing or processing of goods

- Trading of qualifying commodities

- Holding shares/securities for investment

- Ownership/management/operation of ships

- Reinsurance services

- Fund management and wealth management services

- Headquarter and treasury services to related parties

- Aircraft financing and leasing

- Distribution from a designated zone

- Logistics services

Several activity types fall outside this framework and generate non-qualifying income:

- Banking activities (except specific wholesale banking)

- Insurance activities (except reinsurance)

- Ownership or exploitation of mainland immovable property

- Finance and leasing (except qualifying aircraft/ship financing)

- Transactions with natural persons (with narrow exceptions)

The Mainland Transaction Trap

Two of those excluded categories — mainland immovable property and transactions with natural persons — directly connect to a risk that catches Singapore-owned free zone entities off guard: mainland UAE revenue.

Income earned from mainland UAE customers is generally not qualifying income. Singapore companies whose UAE free zone entities serve both free zone and mainland clients must carefully track and cap that revenue to protect QFZP status.

For example, if a DMCC logistics entity derives AED 10 million in total revenue, mainland revenue must not exceed AED 500,000 (the 5% cap) — not AED 5,000,000, because the lower of the two thresholds applies.

Registration and Filing

All free zone companies carry the following obligations, regardless of whether they ultimately qualify for the 0% rate:

- Register with the FTA and obtain a Tax Registration Number

- File the CT return within 9 months after the end of the tax period

- Submit a Transfer Pricing Disclosure Form if related-party transactions exist

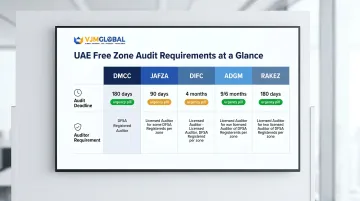

Audit Obligations and IFRS Compliance

While federal law does not universally mandate audits for every free zone company based solely on revenue, the practical reality is that **most Singapore companies with UAE free zone entities will need annual audited financial statements**. This is driven by three factors:

1. Free Zone Authority Requirements

Most major UAE free zones mandate annual audits as a condition of license renewal:

| Free Zone | Audit Deadline | Auditor Requirement |

|---|---|---|

| DMCC | 180 days (6 months) after FY end | DMCC-approved auditors |

| JAFZA | 90 days (3 months) after FY end | JAFZA-approved auditors |

| DIFC | 4 months after FY end | DIFC-registered auditors; IFRS mandatory |

| ADGM | 9 months (private); 6 months (public) | ADGM Recognised Auditors |

| RAKEZ | 180 days (6 months) after FY end | Authority-approved auditors |

2. QFZP Status Requirement

All QFZP entities must maintain audited financial statements as a mandatory condition. The FTA may request these during CT reviews to substantiate qualifying income calculations and adequate substance claims.

3. Bank and Investor Requirements

UAE banks and international investors require audited financials for credit facilities and governance compliance.

Preparing for the Audit

Singapore companies should:

- Maintain organized records throughout the year, not just at year-end

- Reconcile bank statements and VAT returns regularly to avoid year-end bottlenecks

- Ensure the chart of accounts supports qualifying vs. non-qualifying income segregation

- Engage an approved auditor early — ideally 2–3 months before the renewal deadline to avoid last-minute delays

When Free Zone Authority Rules Differ

Those preparation steps matter especially because UAE free zone rules are not uniform. Each Free Zone Authority sets its own audit submission timelines, document formats, and revenue thresholds. Singapore companies operating across multiple free zones — or considering a zone change — should verify audit requirements with their specific licensing authority. Non-compliance can result in license suspension independently of any FTA enforcement action.

Additional Compliance: VAT, ESR, Transfer Pricing, and the Singapore-UAE DTA

VAT and Economic Substance Regulations

VAT Registration and Filing

UAE VAT at 5% applies if taxable supplies exceed AED 375,000 annually. Voluntary registration is available once taxable supplies exceed AED 187,500. Filing frequency is quarterly for businesses with annual turnover below AED 150 million and monthly for turnover exceeding AED 150 million.

Designated Zone VAT Treatment

Per the FTA VAT Guide on Designated Zones (VATGDZ1):

- Goods supplies between Designated Zones: Outside the scope of VAT, provided goods are not released into circulation or altered

- Services within Designated Zones: Subject to standard 5% VAT

- Goods for resale or manufacturing within a DZ: Outside the scope of VAT

- Movement from DZ to mainland UAE: Treated as an import (import VAT payable)

For Singapore companies with UAE free zone entities involved in import/export, logistics, or B2B services, designated zone rules significantly affect whether VAT applies. Transactions with mainland UAE customers are generally standard-rated at 5%.

Economic Substance Regulations

ESR applies to all UAE entities (mainland and free zone) performing any of nine Relevant Activities: banking, insurance, investment fund management, lease-finance, headquarters, shipping, holding company, intellectual property, distribution and service center.

ESR Deadlines:

- ESR Notification: Within 6 months of financial year-end

- ESR Report: Within 12 months of financial year-end

Companies performing ESR Relevant Activities must demonstrate genuine economic presence in the UAE, including adequate qualified employees, operating expenditure, and physical assets. The FTA's definition of Core Income-Generating Activities (CIGA) for QFZP adequate substance is derived from ESR Resolution No. 57, meaning ESR substance requirements also underpin the QFZP adequate substance test.

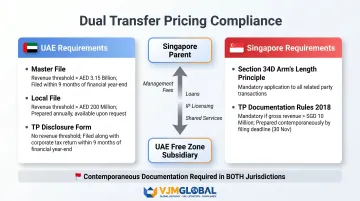

Transfer Pricing and the Singapore-UAE Double Tax Treaty

Dual Transfer Pricing Compliance

Singapore companies transacting with UAE free zone subsidiaries face dual TP compliance obligations:

UAE Requirements (Ministerial Decision No. 97 of 2023):

| Document | Threshold | Deadline |

|---|---|---|

| Master File | Group revenue AED 3.15B+ OR individual revenue AED 200M+ | Within 30 days upon FTA request |

| Local File | Group revenue AED 3.15B+ OR individual revenue AED 200M+ | Within 30 days upon FTA request |

| TP Disclosure Form | All entities with related-party transactions | With CT return (9 months after FY end) |

Singapore Requirements (IRAS Transfer Pricing Guidelines, 8th Edition, Nov 2025):

Section 34D of the Income Tax Act mandates the arm's length principle for all related-party transactions. TP documentation is governed by the Income Tax (Transfer Pricing Documentation) Rules 2018.

When a Singapore parent company transacts with its UAE free zone subsidiary — covering management fees, intercompany loans, IP licensing, or shared services — the arm's length principle must be applied under both UAE CT law and Singapore's transfer pricing guidelines. This dual documentation burden requires intercompany pricing that satisfies UAE Article 34 and Singapore ITA Section 34D simultaneously, with separate contemporaneous documentation for each jurisdiction.

Singapore-UAE Double Tax Treaty

The Agreement between Singapore and the UAE for the Avoidance of Double Taxation entered into force on 30 August 1996 and is effective retroactively from 1 January 1992.

Treaty Withholding Tax Caps:

| Income Type | Treaty Cap | UAE Actual WHT |

|---|---|---|

| Dividends | 5% | 0% |

| Interest | 7% | 0% |

| Royalties | 5% | 0% |

The UAE currently imposes 0% withholding tax on dividends, interest, and royalties paid to foreign entities. This means profit repatriation from UAE free zone subsidiaries to Singapore parents is currently tax-free at source.

The critical challenge, however, sits on the Singapore side. Because the UAE's 9% headline rate falls below the 15% FSIE threshold and QFZP income is taxed at 0%, UAE free zone income remitted to Singapore may be fully taxable at Singapore's 17% corporate rate with no foreign tax credit available.

Singapore companies should structure repatriation timing carefully and take advice on optimizing their position under the DTA and Singapore's remittance-based taxation framework before distributing profits.

Frequently Asked Questions

Is corporate tax registration mandatory for free zone companies in the UAE?

Yes, all UAE free zone companies—including those owned by Singapore entities—must register for corporate tax with the FTA and obtain a Tax Registration Number, regardless of whether they qualify for the 0% QFZP rate. Registration is a mandatory compliance step separate from tax liability.

Is an audit mandatory for free zone companies in the UAE?

Federal law does not universally mandate audits for every free zone company based solely on revenue. However, most major UAE free zones (DMCC, JAFZA, ADGM, RAKEZ, DIFC) require annual audited financial statements as a condition of license renewal. Audits are also practically necessary to substantiate QFZP status under corporate tax law.

Which accounting standards do free zone companies in the UAE follow — IFRS or GAAP?

UAE free zone companies are required to prepare financial statements in accordance with IFRS or IFRS for SMEs. US GAAP is not accepted. While Singapore FRS is largely converged with IFRS, Singapore companies should verify that their UAE entity's financial statements are prepared under full IFRS as required by UAE law and their Free Zone Authority.

Does Singapore have a double tax treaty with the UAE?

Yes. The Singapore–UAE DTA (in force since 30 August 1996) caps withholding tax on dividends at 5%, interest at 7%, and royalties at 5%. In practice, the UAE levies 0% WHT on all cross-border payments, meaning profit repatriation carries no UAE withholding tax. Note that the treaty does not eliminate Singapore-side tax exposure for UAE free zone income where the UAE's 9% headline rate falls below Singapore's 15% FSIE threshold.

How long must UAE free zone companies retain their accounting records?

UAE law requires companies to retain accounting records and supporting documents for a minimum of seven years after the end of the relevant financial period (Article 56, Federal Decree-Law No. 47 of 2022). Some free zone authorities specify longer retention periods, so confirm requirements with your specific Free Zone Authority.

Is CA or ACCA more valued for accounting roles in UAE free zone companies?

Both CA and ACCA qualifications are recognized in the UAE. For Singapore companies engaging external accountants or auditors for their UAE entity, the priority is ensuring the individual or firm is registered and approved by the relevant UAE Free Zone Authority.