FEMA (Foreign Exchange Management Act, 1999) governs every financial decision NRIs make in connection with India — bank accounts, investments, property, and repatriation. Most violations happen not out of intent, but out of unawareness. This guide covers what NRIs must know: who qualifies under FEMA, which accounts are compliant, what you can and cannot invest in, and how repatriation works.

Key Takeaways

- Existing resident savings accounts must be re-designated as NRO accounts the moment you become an NRI

- NRIs cannot open new PPF accounts; existing resident-opened PPF accounts may continue until maturity but cannot be extended

- NRIs may purchase residential or commercial property in India

- Agricultural land, farmhouses, and plantation properties are off-limits for NRI buyers

- NRO account repatriation is capped at USD 1 million per financial year

- NRE and FCNR funds are fully repatriable with no annual ceiling

- FEMA penalties run up to three times the sum involved, with asset confiscation possible in serious cases

What Is FEMA and Why Does It Matter for NRIs?

FEMA replaced the older Foreign Exchange Regulation Act, 1973 (FERA), coming into force on June 1, 2000 under Section 49 of the Foreign Exchange Management Act, 1999. The shift mattered: under FERA, violations were criminal offences. Under FEMA, most contraventions are civil offences handled through monetary penalties — a management-oriented framework rather than a punitive one.

FEMA is administered by the Reserve Bank of India (RBI), which issues regulations, master directions, and compounding guidance. The Enforcement Directorate (ED), under the Ministry of Finance, handles investigations and enforcement of serious contraventions.

The Core Principle NRIs Must Understand

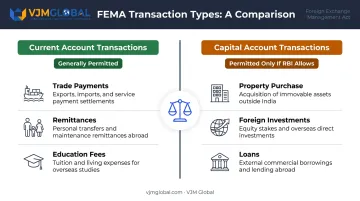

FEMA draws a sharp line between two transaction types:

- Current account transactions (trade, remittances, education payments) — generally permitted unless expressly restricted

- Capital account transactions (property purchase, foreign investments, loans) — prohibited unless expressly permitted by RBI regulations

This distinction is what makes FEMA particularly relevant for NRIs. Sending money abroad for daily expenses falls under current account rules and is generally fine. Buying a plot of land in India, however, triggers capital account regulations — and getting that wrong can mean penalties, not just paperwork.

Who Qualifies as an NRI Under FEMA?

The Residency Test

Under FEMA Section 2(v), a person is considered resident in India if they have been physically present in India for more than 182 days during the preceding financial year. The test is not purely mathematical, though. Purpose and intention matter just as much as the day count.

-----------|-----------|----------------| | NRI | Indian citizen residing outside India | Full NRI banking and property rights | | OCI | Foreign national of Indian origin with OCI card | Similar to NRI for most banking and property purposes | | Pakistan/Bangladesh nationals | Require prior RBI approval | Restricted — separate approval needed |

OCI cardholders must also be resident outside India to access NRI banking benefits. For most banking and property purposes, NRIs and OCIs are treated similarly under FEMA.

The Compliance Trigger

The compliance obligation is immediate. The moment your residential status shifts from resident Indian to NRI:

- Existing resident savings accounts must be re-designated as NRO accounts

- New investments must be reviewed for permissibility under NRI rules

- Ongoing income from Indian sources must route through the correct account types

There is no grace period built into FEMA. Delay itself constitutes a contravention.

FEMA-Compliant Bank Accounts for NRIs

According to RBI's NRI account FAQ, when a resident Indian becomes a person resident outside India, the existing resident savings account must be re-designated as an NRO account. Continuing to operate a resident savings account as an NRI is one of the most common FEMA violations.

Choosing the right account type from the start prevents re-designation penalties and keeps your funds repatriable. Three account types are permissible under FEMA:

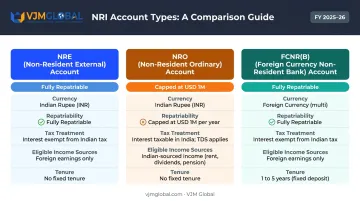

NRE Account (Non-Resident External)

- Rupee-denominated; funds originate from foreign earnings

- Fully repatriable — both principal and interest can be freely remitted abroad

- Interest is exempt from Indian income tax under the Income Tax Act

- Can be held as savings, current, recurring, or fixed deposit

- NRIs can hold jointly with another NRI; joint holding with a resident Indian is restricted to a "former or survivor" basis

NRO Account (Non-Resident Ordinary)

- Designed for income earned in India — rent, dividends, pension, asset sale proceeds

- Held in Indian rupees; not freely repatriable

- Repatriation capped at USD 1 million per financial year (April–March), inclusive of all sources

- Interest earned is taxable in India

FCNR (B) Account (Foreign Currency Non-Resident)

- Foreign currency fixed deposit in freely convertible currencies — USD, GBP, EUR, AUD, CAD, JPY

- Tenure: minimum 1 year, maximum 5 years

- No Indian income tax applies; principal and interest are fully repatriable

- Ideal for NRIs who want to avoid rupee exchange rate risk

Power of Attorney holders have restricted access to NRE and FCNR accounts — they can process local permissible payments or remittances back to the NRI account holder, but nothing beyond that. Exceeding this scope triggers ED scrutiny and can freeze the account pending inquiry.

Investment and Property Rules Under FEMA for NRIs

Permitted Investments

NRIs can invest across a broad range of Indian financial instruments:

- Listed equities and convertible debentures on stock exchanges (via Portfolio Investment Scheme regulated by SEBI)

- Mutual funds, government securities, bonds, and fixed deposits

- Both repatriable (NRE/FCNR basis) and non-repatriable (NRO basis) options exist

Under the FEMA Non-Debt Instruments Rules, 2019, NRI/OCI investment in listed equities is subject to:

- Individual cap: 5% of paid-up capital per company

- Aggregate NRI/OCI cap: 10% of paid-up capital

- Indian companies may raise the aggregate cap to 24% through board/shareholder approval

PPF and Small Savings: The Correct Position

NRI eligibility for small savings schemes is frequently misread. Under guidance from the National Savings Institute (NSI) and Department of Economic Affairs (DEA):

- NRIs cannot open a new PPF account

- An existing PPF account opened while resident may continue until maturity — contributions on a non-repatriation basis are permitted

- Extension after maturity is not allowed for NRIs; deposits made after maturity are irregular and refundable without interest

- Other small savings schemes are similarly off-limits for NRIs

Immovable Property: What's Allowed

NRIs can purchase residential or commercial property in India without RBI approval. Payment must be through banking channels — from NRE, NRO, or FCNR accounts. Cash, traveller's cheques, or foreign currency notes are not permitted.

Prohibited property types — regardless of source of funds:

- Agricultural land

- Plantation properties

- Farmhouses

NRIs can inherit agricultural land or receive residential/commercial property as a gift from a relative. FEMA does not explicitly permit gifting agricultural land to an NRI — treat this as prohibited unless you have obtained specific legal clearance.

Property Sale and Repatriation

Once you decide to sell, the rules shift from acquisition to exit. Sale proceeds from residential or commercial property can be repatriated abroad, subject to:

- Maximum of two such properties (the two-property limit applies to residential property repatriation)

- Original purchase must have been through foreign currency remittances or NRE/FCNR accounts

- Inherited property repatriation requires RBI approval if it exceeds USD 1 million per year

Repatriation of Funds: What NRIs Can and Cannot Send Abroad

The USD 1 Million NRO Cap

Per RBI's NRO account guidelines, NRIs can remit up to USD 1 million per financial year (April–March) from NRO accounts. This limit applies across all sources combined — bank balances, property sale proceeds, share proceeds, insurance maturities, and inheritance — not per transaction or per asset.

Full Repatriability from NRE and FCNR

NRE and FCNR(B) balances carry no annual repatriation ceiling. Principal, interest, and proceeds from investments made using these accounts are freely remittable abroad — meaning you can transfer the full amount overseas without filing against any annual limit or seeking separate RBI approval.

Current Income vs. Capital Proceeds

This distinction affects whether the USD 1 million cap applies:

| Income Type | Cap Applies? | Notes |

|---|---|---|

| Rental income, dividends, pension, interest | No | Treated as current income; remittable separately |

| Property sale proceeds, share sale proceeds | Yes | Counts against USD 1 million annual limit |

Procedural Requirements: Forms 15CA and 15CB

Before remitting funds from NRO accounts, NRIs must complete a two-step tax compliance process:

- File Form 15CA, which discloses payment details to the Indian tax authorities for any remittance to a non-resident

- Obtain Form 15CB, a Chartered Accountant's certificate verifying that all applicable Indian taxes have been paid — required when the taxable remittance exceeds ₹5,00,000 in aggregate

- Submit both to the Authorised Dealer bank, which must confirm all applicable Indian taxes have been paid

Failing to file these forms before remittance is itself a FEMA contravention. VJM Global works with NRI clients on this process end-to-end — from preparing the documentation to coordinating submission with the Authorised Dealer bank.

Common FEMA Violations and How to Avoid Them

Most NRI FEMA violations are inadvertent. These are the most frequent:

- Holding a resident savings account after becoming an NRI instead of converting it to NRO

- Opening a new PPF account after NRI status change, or attempting to extend an existing PPF beyond maturity

- Purchasing agricultural land in India — the prohibition applies regardless of funding source

- Repatriating funds without proper documentation or without filing Forms 15CA/15CB

- Routing Indian income (rent, dividends) into a resident account rather than an NRO account

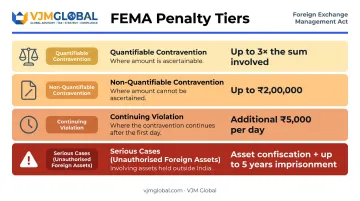

The Penalty Framework Under FEMA Section 13

| Violation Type | Penalty |

|---|---|

| Quantifiable contravention | Up to 3x the sum involved |

| Non-quantifiable contravention | Up to ₹2,00,000 |

| Continuing violation | Additional ₹5,000 per day |

| Serious cases (unauthorised foreign assets) | Asset confiscation; imprisonment up to 5 years |

RBI also operates a compounding mechanism — NRIs who voluntarily disclose and resolve contraventions can apply for compounding under Section 13, which typically results in a reduced monetary penalty without criminal proceedings.

When to Get Structured FEMA Advisory

FEMA regulations are updated regularly through RBI notifications, and the line between permitted and prohibited transactions shifts. For NRIs managing multiple Indian assets — property, shares, fixed deposits, business interests — a reactive approach to compliance carries real financial risk.

Structured advisory — not just at filing time — is especially important for NRIs who are:

- Inheriting Indian assets or receiving property through succession

- Planning to repatriate proceeds from property sales

- Holding Indian shares, fixed deposits, or business interests across multiple entities

- Unsure whether an existing investment remains permissible after a status change

VJM Global's Chartered Accountants have 30+ years of experience supporting NRI clients across the USA, UK, and Australia — covering everything from account re-designation and Form 15CA/15CB preparation to RBI clearances and ongoing portfolio monitoring. Getting this right early prevents violations from escalating to enforcement.

Frequently Asked Questions

What is the FEMA Act in India?

FEMA is India's primary law governing all foreign exchange transactions, in force since June 1, 2000, replacing FERA 1973. The RBI administers it, classifying transactions into current account (generally permitted) and capital account (permitted only as RBI specifies).

What are the FEMA rules for NRIs in India?

NRIs must hold NRE, NRO, or FCNR accounts — not regular resident savings accounts. They cannot open new PPF accounts or purchase agricultural land. Repatriation from NRO accounts is capped at USD 1 million per financial year; NRE and FCNR funds are fully repatriable.

What is a FEMA violation in India?

Common NRI violations include retaining a resident savings account after status change, unauthorized property purchases, and repatriating funds without Form 15CA/15CB. Penalties can reach up to 3x the transaction amount involved.

Is FEMA still in force in India?

Yes. FEMA remains active and is the primary legislation governing foreign exchange transactions in India. The RBI continuously issues updated regulations and master directions under it.

Can an NRI hold a regular savings account in India?

No. Under FEMA, an NRI cannot legally operate a regular resident savings account. Upon acquiring NRI status, the account must be re-designated as an NRO account, or funds transferred to an NRE account depending on the source of those funds.