Introduction

Singapore is home to approximately 650,000 overseas Indians — one of the largest Indian diaspora communities in Southeast Asia. For professionals, entrepreneurs, and permanent residents with financial ties to India, the Foreign Exchange Management Act (FEMA, 1999) directly governs how they bank, invest, and transfer money across borders.

FEMA covers every dimension of cross-border financial activity for Non-Resident Indians: which accounts you can legally hold, how you can invest in Indian assets, what repatriation limits apply, and which transactions are strictly prohibited.

Non-compliance carries real consequences — penalties of up to three times the amount involved and, in severe cases, criminal prosecution.

This guide walks Singapore-based NRIs through the essentials: who qualifies as an NRI under FEMA, which bank accounts are compliant, investment routes available, repatriation limits, prohibited transactions, and documentation requirements—with a Singapore-specific lens throughout.

Key Takeaways:

- You qualify as an NRI if you stayed outside India for more than 182 days in the preceding financial year with intent to remain abroad

- NRE accounts offer tax-free interest and full repatriation; NRO accounts cap repatriation at USD 1 million annually

- Singapore NRIs can invest in Indian equities, mutual funds, real estate, and businesses under FEMA Non-Debt Instruments Rules

- The India-Singapore DTAA prevents double taxation on investment income

- NRIs cannot hold agricultural land, farmhouses, PPF accounts, or small savings schemes in India

Who Qualifies as an NRI Under FEMA: What Singapore Residents Need to Know

The 182-Day Rule and the Intention Test

Under Section 2(v) of FEMA, 1999, you are classified as a Non-Resident Indian if you have not resided in India for more than 182 days during the preceding financial year and your stay outside India is for employment, business, or any purpose indicating an indefinite period abroad. The critical word here is preceding: FEMA looks at the financial year that just ended, not the current one.

Intention matters as much as day-count. Leaving for overseas employment or business establishes non-resident status from your departure date — even if you haven't yet crossed the 182-day mark. The reverse also applies: returning to India with the intent to stay indefinitely makes you a resident from arrival, regardless of where the day-count stands.

FEMA vs. Income Tax Act: Two Different Definitions

Singapore residents must confirm their status under both FEMA and the Income Tax Act before making investment decisions, as these laws use different criteria:

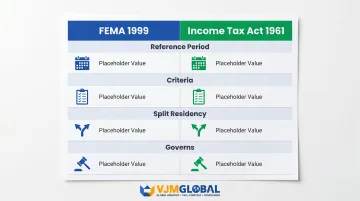

| Dimension | FEMA | Income Tax Act, 1961 |

|---|---|---|

| Reference period | Preceding financial year | Current financial year |

| Criteria | 182 days + intention/purpose | Day-count thresholds (182 days or 60 days + 365 days in prior 4 years) |

| Split residency | Permitted mid-year | Not permitted—status applies for entire year |

| Governs | Permissible forex transactions | Taxable income scope |

You can be a non-resident under FEMA while simultaneously being a resident under the Income Tax Act. This dual-status scenario is a real risk for Singapore-based professionals who make extended India trips — whether for family reasons or long project assignments.

NRI vs. OCI Under FEMA

Non-Resident Indians hold Indian citizenship but reside abroad. Overseas Citizens of India (OCIs) hold foreign citizenship — such as Singaporean citizenship — but have Indian heritage. Under the FEMA Non-Debt Instruments Rules, 2019, OCIs are treated on par with NRIs for investment purposes. Both categories share the same framework across:

- Eligible entry routes for investment

- Applicable sectoral caps

- Conditions for repatriation (remitting funds abroad) and non-repatriation (keeping funds in India)

- Reporting and compliance obligations

FEMA-Compliant Bank Accounts for Singapore NRIs

NRIs cannot maintain standard resident savings accounts in India. Once you become an NRI, existing resident accounts must be converted to NRO accounts or closed—failure to do so is a FEMA violation.

NRE Account (Non-Resident External)

The NRE account is designed for parking foreign-earned income—your SGD salary from Singapore, for example—in Indian Rupees. Key features:

- Accepts inward remittances in any convertible foreign currency, including SGD

- Both principal and interest are fully repatriable with no upper limit

- Interest earned is tax-free in India under Section 10(4)(ii) of the Income Tax Act

- Available as savings, current, fixed deposit (FD), or recurring deposit (RD)

NRE accounts work best when your primary goal is bringing Singapore earnings back to India and repatriating returns without tax drag—there's no cap on what you can move out.

NRO Account (Non-Resident Ordinary)

The NRO account handles India-sourced income: rental income, dividends, pension, or salary earned in India. Key features:

- Accepts both Indian-source income and foreign remittances

- Repatriation is capped at USD 1 million per financial year after payment of applicable taxes

- Interest income is taxable in India; TDS is deducted at 30% plus surcharge and cess

- Available as savings, current, FD, or RD

If you earn rent from an Indian property or receive dividends from Indian stocks, those funds must route through an NRO account—you can't credit them to an NRE account directly.

FCNR(B) Account (Foreign Currency Non-Resident)

SGD is not among the six permitted currencies for FCNR(B) accounts. Only USD, GBP, EUR, JPY, CAD, and AUD qualify—so Singapore NRIs must convert to one of these before depositing. That said, FCNR(B) accounts offer a genuine hedge against rupee depreciation for those comfortable with the conversion cost.

- Term deposits only (1 to 5 years)—not available as savings or current accounts

- Fully repatriable, both principal and interest

- Interest is tax-exempt in India under Section 10(4)(i)

- Requires conversion from SGD to a permitted currency, incurring forex costs

Account Comparison Table:

| Feature | NRE Account | NRO Account | FCNR(B) Account |

|---|---|---|---|

| Currency | INR (converted from forex) | INR | Foreign currency (USD, GBP, EUR, JPY, CAD, AUD) |

| SGD permitted? | ✅ Yes (converts to INR) | ✅ Yes (converts to INR) | ❌ No—must convert to permitted currency |

| Repatriability | Fully repatriable | USD 1 million/FY cap | Fully repatriable |

| Interest tax | Tax-free | 30% TDS + surcharge + cess | Tax-free |

| Funding | Forex only | Indian income + forex | Forex only |

| Account types | Savings, current, FD, RD | Savings, current, FD, RD | Term deposit only |

Investment Avenues for Singapore-Based NRIs Under FEMA

Singapore-based NRIs can invest across a wide range of asset classes in India — from listed equities and mutual funds to real estate and private businesses. The rules governing each avenue fall under the FEMA Non-Debt Instruments Rules, 2019, and the first decision you'll make applies to all of them: which investment route to use.

Repatriation vs. Non-Repatriation Basis

Under the FEMA Non-Debt Instruments Rules, 2019, NRIs can invest in India on two routes:

- Repatriation basis (Schedule III): Capital and profits can be freely sent back to Singapore

- Non-repatriation basis (Schedule IV): Funds remain in India and are treated as domestic investment

The repatriation basis suits investors who want to move gains back to Singapore; the non-repatriation basis is typically used when you plan to reinvest returns within India long-term.

Equity and Stock Market Investments

NRIs can invest in listed Indian companies through the Portfolio Investment Scheme (PIS), which must be linked to an NRE or NRO account via an authorised dealer bank. Investment caps apply:

- Individual cap: Maximum 5% of a company's total paid-up capital

- Aggregate NRI/OCI cap: 10% of paid-up equity capital (extendable to 24% by shareholder resolution)

These caps ensure that NRI holdings don't trigger foreign investment thresholds requiring additional regulatory approvals.

Mutual Funds and SIPs

Singapore NRIs can invest in Indian mutual funds — both equity-oriented and debt schemes — through Systematic Investment Plans (SIPs). Key points:

- Investments route through NRE accounts (repatriation basis) or NRO accounts (non-repatriation basis)

- KYC must reflect NRI status with the Asset Management Company (AMC)

- Singapore NRIs face none of the restrictions that apply to US/Canada-based NRIs. Those restrictions stem from FATCA and SEC compliance requirements; Singapore's tax information exchange framework operates under CRS, which most Indian AMCs readily accept

Beyond market-linked instruments, real estate is another avenue Singapore NRIs frequently use to deploy capital in India.

Real Estate

NRIs can purchase residential and commercial property in India without limit. Payment must route through NRE, NRO, or FCNR(B) (Foreign Currency Non-Resident Bank) accounts or via inward remittance through banking channels.

Prohibited purchases:

- Agricultural land

- Plantation property

- Farmhouses

You may inherit these prohibited property types but can only transfer them to Indian citizens permanently residing in India.

For NRIs looking to build an operating business — not just a portfolio — India offers structured entry options through LLPs and private companies.

Business Investments (LLPs and Private Companies)

Singapore NRIs can invest in Indian Limited Liability Partnerships (LLPs) and private limited companies on either repatriation or non-repatriation basis under Schedules III and IV of the FEMA Non-Debt Instruments Rules.

Key conditions:

- Repatriation basis: LLP or company must operate in a sector where 100% FDI is permitted under the automatic route

- Non-repatriation basis: No sectoral limits apply; the investment is treated as domestic

- At least one resident Indian must hold a mandatory director or designated partner role

Prohibited sectors (both routes):

- Agricultural or plantation activities

- Real estate trading (as distinct from development)

- Farmhouses

- Nidhi companies

- Transferable Development Rights (TDR)

Repatriation Rules and Limits Singapore NRIs Must Know

USD 1 Million Annual Cap from NRO Accounts

NRIs may repatriate up to USD 1 million per financial year from NRO accounts, covering sale proceeds of assets, rental income, and other India-sourced earnings. You must pay applicable taxes and submit proper documentation to the authorised dealer bank before the bank processes your repatriation.

NRE and FCNR(B) accounts carry no repatriation limit: funds can be freely transferred back to Singapore or any foreign account.

India-Singapore DTAA and Capital Gains

The Double Taxation Avoidance Agreement (DTAA) between India and Singapore prevents the same income from being taxed in both countries. The Third Protocol, signed in December 2016 and effective April 1, 2017, amended capital gains treatment:

| Share Acquisition Date | Capital Gains Tax Treatment |

|---|---|

| Before April 1, 2017 | Taxable only in Singapore (grandfathered) |

| April 1, 2017 to March 31, 2019 | May be taxed in India, capped at 50% of domestic rate |

| On or after April 1, 2019 | Fully taxable in India at domestic rates |

NRIs holding pre-2017 Indian equities are fully sheltered from Indian capital gains tax — a treaty protection that no longer applies to newer acquisitions.

To claim DTAA benefits:

- Obtain a Tax Residency Certificate (TRC) from IRAS Singapore, confirming Singapore tax residency

- File Form 10F with Indian tax authorities — mandatory under Section 90(5) of the Income Tax Act

Missing either document can result in denial of treaty benefits and application of full domestic Indian tax rates.

Property Sale Repatriation

Repatriation limits depend on how the property was originally purchased:

- Purchased with foreign exchange (NRE, FCNR, or inward remittance): principal may be repatriated for a maximum of two residential properties

- Purchased with rupee funds or inherited: proceeds fall under the USD 1 million per FY NRO cap; all sale proceeds must be credited to an NRO account first, with applicable taxes paid before repatriation

Transactions Prohibited Under FEMA for NRIs

Accounts and Savings Schemes

- Public Provident Fund (PPF): NRIs cannot open new PPF accounts. Existing PPF accounts opened while resident may be continued until maturity but cannot be extended or renewed

- Small savings schemes: National Savings Certificates, Kisan Vikas Patra, Sukanya Samriddhi, Senior Citizens Savings Scheme—all prohibited for NRIs

- Resident savings accounts: Cannot be maintained once you become an NRI; must convert to NRO or close

Real Estate and Business Prohibitions

NRIs cannot purchase:

- Agricultural land

- Plantation property

- Farmhouses

NRIs cannot invest in businesses engaged in:

- Agricultural/plantation activities

- Real estate trading (distinct from property development)

- Nidhi companies

- Transfer of Development Rights (TDR)

FEMA Penalty Framework

Violating these restrictions carries real financial and legal consequences under Section 13 of FEMA:

- Quantifiable violations: Up to three times the sum involved

- Non-quantifiable violations: Up to ₹2 lakh

- Continuing violations: Additional ₹5,000 per day after the first day

- Severe violations involving foreign assets exceeding ₹1 crore: Imprisonment up to five years with fine

Penalties can compound quickly — a continuing violation running for six months at ₹5,000 per day reaches ₹9 lakh before any base penalty applies. If you hold accounts or investments that no longer qualify under your NRI status, reviewing and restructuring them proactively is far less costly than enforcement.

Documentation and Compliance Checklist for Singapore NRIs

Core Identity and Status Documents

- Valid Indian passport (for NRIs who are Indian citizens)

- Singapore Employment Pass (EP), S Pass, or PR/Citizenship proof—establishing non-resident status

- Proof of address in Singapore (utility bill, tenancy agreement, bank statement)

- PAN card (Permanent Account Number)—mandatory for all financial transactions in India

NRIs whose PAN reflects non-resident status are exempt from mandatory PAN-Aadhaar linking. Those holding Aadhaar from their time as residents must link it to PAN if their PAN reflects resident status.

Transaction-Specific Documentation

Form A2 (Outward Remittance Declaration):

Mandatory for purchasing foreign exchange for outward remittances from India. Since July 2024, the RBI removed the USD 25,000 exemption—Form A2 is now compulsory for every cross-border transaction regardless of value. Submit to your authorised dealer (AD) bank.

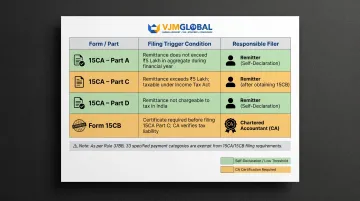

Form 15CA and 15CB (Remittance Tax Compliance):

| Form | When Required | Who Files |

|---|---|---|

| 15CA Part A | Remittance ≤ INR 5 lakh in FY | Remitter (self-declaration) |

| 15CA Part C | Remittance > INR 5 lakh + CA certificate (Form 15CB) obtained | Remitter |

| 15CA Part D | Remittance not chargeable to tax | Remitter |

| 15CB | Taxable remittance > INR 5 lakh | Chartered Accountant (certification) |

33 types of payments—including personal travel, education, and medical treatment—are exempt from 15CA/15CB requirements under Rule 37BB.

Tax Residency Certificate (TRC) and Form 10F:

To claim DTAA benefits, obtain a Certificate of Residence (COR)/TRC from IRAS and submit it alongside Form 10F to Indian tax authorities. This is mandatory under Section 90(5) of the Income Tax Act. All foreign exchange transactions must be routed through an authorised dealer bank designated by the RBI.

Working with Experienced Advisors

Navigating FEMA compliance involves multiple Indian regulatory bodies—RBI, CBDT, SEBI—and Singapore-side requirements from IRAS. From account structuring and investment routing to repatriation documentation and DTAA claims, the regulatory landscape is dense and unforgiving.

Experienced advisors like VJM Global, with 30+ years in NRI tax and FEMA compliance, help Singapore-based NRIs avoid costly missteps by coordinating with both Indian regulators and IRAS across every stage of the investment lifecycle.

Frequently Asked Questions

What is the new rule for NRI in India?

Recent updates include mandatory conversion of resident savings accounts to NRO accounts upon becoming an NRI, updated KYC requirements for mutual fund investments, and removal of the USD 25,000 exemption for Form A2 filing—making it compulsory for all outward remittances regardless of value.

Which transactions are prohibited under FEMA?

NRIs cannot invest in PPF or small savings schemes, purchase agricultural land, plantation property, or farmhouses, hold resident savings accounts, or invest in prohibited business sectors such as real estate trading, Nidhi companies, or TDR.

Can Singapore NRIs invest in SIPs (Systematic Investment Plans) in India?

Yes. Singapore NRIs can invest in Indian mutual funds via SIPs through NRE or NRO accounts. KYC must reflect NRI status with the AMC. Unlike US/Canada NRIs, Singapore NRIs face fewer fund-house restrictions due to Singapore's CRS-compliant tax framework.

What is the India-Singapore DTAA and how does it benefit NRI investors?

The DTAA prevents double taxation on the same income. Singapore NRIs can claim treaty benefits (reduced TDS rates or capital gains exemptions) by submitting a Tax Residency Certificate (TRC) from IRAS with Form 10F to Indian tax authorities. Shares acquired before April 2017 are grandfathered and taxable only in Singapore.

What is the repatriation limit from NRO accounts for NRIs?

NRIs can repatriate up to USD 1 million per financial year from NRO accounts after paying applicable taxes and submitting required documentation to the authorised dealer bank. NRE and FCNR(B) accounts allow unlimited repatriation.

What are the penalties for FEMA violations by NRIs?

FEMA violations attract penalties of up to three times the amount involved (or INR 2 lakh where not quantifiable), plus daily penalties of INR 5,000. Severe violations involving foreign assets exceeding INR 1 crore can result in imprisonment up to five years and a fine.