Introduction

Singapore-based Indians are increasingly registering companies in India — to tap into a growing domestic market, structure cross-border investments, or establish a formal presence for family assets. For NRIs, OCIs, and PIOs, this typically means incorporating a Private Limited Company or LLP that complies with India's Foreign Exchange Management Act (FEMA) and the Companies Act, 2013.

Singapore-based incorporators face requirements that domestic applicants don't. Documents signed in Singapore must be notarised and apostilled by the Singapore Academy of Law (SAL), since Singapore is a Hague Convention country.

FEMA compliance adds another layer — particularly the mandatory FC-GPR filing with the RBI within 30 days of share allotment, which carries strict penalties for late submission. Remote incorporation is entirely possible, but the process demands precision and attention to multiple regulatory timelines.

This guide covers:

- Why registering now makes strategic sense for Singapore-based NRIs

- Which company structure fits your situation

- The exact step-by-step incorporation process

- Singapore-specific documentation requirements

- Post-incorporation compliance obligations

- Common pitfalls and how to avoid them

Key Takeaways

- Singapore-based NRIs can register a Private Limited Company in India without physically visiting — the entire process completes remotely in 15–25 business days

- Registration requires a DSC, DIN, and SPICe+ filing on the MCA portal, plus notarised documents

- Singapore is a Hague Convention member, so apostille through SAL (Singapore Academy of Law) is mandatory

- Appoint at least one Indian resident director (182+ days in India) — required by law even with 100% NRI ownership

- File FC-GPR with the RBI within 30 days of share allotment — missing this deadline triggers FEMA penalties up to 3x the investment amount

- The India-Singapore DTAA caps dividend withholding tax at 10–15%, versus the domestic 20% rate, saving up to 10% on dividend withholding tax at repatriation

Why Singapore-Based NRIs Are Choosing to Register Companies in India

India remains one of the world's fastest-growing major economies. The IMF projects GDP growth at 6.5% for both 2026 and 2027, while the World Bank forecasts 6.6% for FY27. For Singapore-based NRIs, this growth creates a practical case for establishing a formal business presence — whether to serve Indian customers, access talent, or deploy capital in high-growth sectors.

Singapore is consistently among India's top FDI source countries. In FY 2024-25, Singapore was the largest source of FDI into India with investments exceeding USD 14 billion. Cumulatively from April 2000 to December 2024, Singapore ranks 2nd with USD 171.92 billion, representing 23.87% of total cumulative FDI inflow. This well-established investment corridor provides structural advantages for Singapore-based NRIs entering the Indian market.

Key advantages specific to Singapore-based NRIs:

- India-Singapore DTAA: Dividend withholding tax is capped at 10% (25%+ shareholding) or 15% — well below the standard 20% NRI rate under Section 195

- Automatic FDI route: Private Limited Companies accept 100% FDI without prior RBI or DPIIT approval in IT, manufacturing, consulting, healthcare, and e-commerce

- Startup India eligibility: NRI-incorporated entities under 10 years old with turnover below ₹100 crore can qualify for DPIIT recognition, unlocking tax exemptions and funding access

- Simplified document apostille: Singapore joined the Hague Apostille Convention in September 2021, so SAL-apostilled documents are accepted directly for Indian MCA filings

Structuring a company correctly from the start — entity type, shareholding, and repatriation planning — determines how much of these advantages you actually capture. Getting that foundation right is where professional guidance makes the biggest difference.

Business Structures Available to Singapore-Based NRIs

Three structures are available to Singapore-based NRIs, but only two are practical for most business scenarios:

1. Private Limited Company (Recommended)

- Allows 100% FDI under the automatic route in most sectors

- Cleanest compliance structure with clear separation of personal and business liability

- Both automatic and government approval routes available

- Suitable for IT services, manufacturing, consulting, healthcare, and e-commerce marketplace models

2. Limited Liability Partnership (LLP)

- Permitted only in sectors where 100% FDI is allowed under the automatic route and there are no FDI-linked performance conditions

- Structurally simpler than a Private Limited Company but restricted in sectoral eligibility

- Cannot access the government approval route, unlike Private Limited Companies

3. Wholly-Owned Subsidiary

- Used when a Singapore-registered company wants to establish an Indian entity under its corporate umbrella

- Follows the same Private Limited Company incorporation process but with the foreign parent as the sole shareholder

Prohibited Structures for NRI Investment

Not all business forms qualify — several structures are off-limits under FEMA. The following cannot receive FDI:

- Sole proprietorships

- Partnership firms

- One Person Companies (OPCs)

OPCs are a particularly common misconception. Section 3(1)(c) of the Companies Act requires an OPC to have a single Indian resident natural person as its sole member, making it structurally incompatible with foreign investment.

Step-by-Step: How NRIs in Singapore Register a Company in India

The entire process from initiating DSC to receiving the Certificate of Incorporation typically takes 15–25 business days for Singapore-based NRIs. The apostille process is the most time-sensitive step and should be started first — ideally 2–3 weeks before you plan to file SPICe+.

Before you begin: Singapore is a Hague Convention signatory, so all incorporation documents signed there must be notarised by a local Singapore notary and apostilled by the Singapore Academy of Law (SAL). This authentication is what makes them legally valid for Indian MCA filings.

Step 1: Obtain Digital Signature Certificate (DSC)

Each proposed director must obtain a Class 3 DSC from an Indian Certifying Authority such as eMudhra or Protean eGov Technologies (formerly NSDL). Singapore-based NRIs can complete this remotely through video verification without visiting India. The DSC is used to digitally sign all MCA filing documents and typically takes 2 working days to procure.

Step 2: Apply for Director Identification Number (DIN)

You obtain DIN directly through the SPICe+ incorporation form — no separate application needed. NRI directors must submit a notarised and apostilled passport copy as identity proof. The DIN is a unique, lifelong number tied to anyone serving as a director in any Indian company.

Step 3: Reserve Company Name and Prepare Incorporation Documents

File SPICe+ Part A on the MCA portal to reserve your company name. The name must comply with MCA naming guidelines and must not conflict with existing companies or trademarks.

At the same time, draft your Memorandum of Association (MoA) and Articles of Association (AoA). Standard e-MoA and e-AoA templates are on the MCA portal — customise them to match your company's objects and shareholding structure.

Step 4: File SPICe+ Form on MCA Portal

SPICe+ (Simplified Proforma for Incorporating Company Electronically Plus) is a single integrated form that simultaneously handles:

- Name approval

- DIN allotment

- Incorporation

- PAN application

- TAN application

- Optional GST registration

- EPFO and ESIC registration

All apostilled documents are uploaded here. Once submitted and verified by the Registrar of Companies, the Certificate of Incorporation is issued digitally. This step typically takes 5 days after name approval.

Step 5: Post-Incorporation Actions

Three mandatory post-incorporation steps:

- Open an Indian business bank account using the Certificate of Incorporation — note that some banks require at least one director to be physically present, so choose a bank experienced with NRI-owned companies

- Receive the NRI's foreign investment via inward remittance to the company's NRE or FCNR(B) account

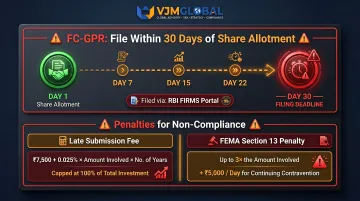

- File FC-GPR with RBI through the FIRMS portal within 30 days of allotting shares to the NRI investor — missing this deadline triggers FEMA penalties

Documents Required: A Singapore-Specific Checklist

For Singapore-Resident NRIs (Indian Passport Holders)

- Valid Indian passport (primary identity proof)

- Singapore address proof (utility bill, bank statement, or Singapore government-issued document, not older than two months)

- Indian PAN card (mandatory for NRI directors; apply via Form 49A if not already held)

- Aadhaar card, if available (optional for NRIs)

Apostille Requirement Specific to Singapore

Since Singapore is a Hague Convention country, the notarisation and apostille process has three steps:

- Get the document notarised by a Singapore Commissioner for Oaths or Notary Public

- Submit to the Singapore Academy of Law (SAL) for apostille

- The apostilled document is valid for Indian MCA filings without further embassy attestation

SAL charges S$10.70 per document with a processing timeline of 1-2 working days (excluding submission day). Private documents must first be notarised before SAL can apostille them.

Registered Office Address in India

Since the NRI is based in Singapore, the company still needs a physical registered office address in India for all official correspondence. Options include:

- Using a trusted contact's address

- Renting a commercial space

- Engaging a professional virtual office service in India

- Required proof documents: utility bill, rent agreement, and NOC from the property owner

Resident Director Documentation

The Indian resident director (who qualifies by spending 182+ days in India in the previous calendar year) must provide:

- Aadhaar card

- PAN card

- Indian address proof

- DSC

This person is legally responsible for ensuring the company maintains compliance. If no trusted contact is available in India, a professional firm can appoint a nominee director on your behalf.

OCI-Specific Documentation Pitfall

OCIs (Overseas Citizens of India) living in Singapore hold an OCI card, not an Indian passport. While OCIs are treated on par with NRIs for most investment purposes under FEMA's NDI Rules, their identity proof for MCA filings must include both their OCI card and their foreign passport. When filing for an OCI-card holder, always include both documents to avoid MCA rejection.

FEMA, RBI, and Tax Obligations You Cannot Ignore

Critical RBI Filings for NRI-Owned Companies

FC-GPR (Foreign Currency Gross Provisional Return):

- Must be filed within 30 days of share allotment to foreign/NRI investors via the RBI FIRMS portal

- Failure to file on time attracts FEMA compounding penalties

- Late Submission Fee (LSF) formula: ₹7,500 + (0.025% × Amount × Years of delay), capped at 100% of investment amount

- FEMA Section 13 penalties can reach 3× the amount involved or ₹2 lakh (if amount not quantifiable), plus ₹5,000 per day for continuing contravention

FLA Return (Foreign Liabilities and Assets Annual Return):

- Filed by July 15 each year on the RBI FLAIR portal

- Reports all foreign investment received as on March 31

Share Pricing Requirement Under FEMA

Shares issued to an NRI investor must be priced at or above Fair Market Value (FMV). For unlisted private limited companies, FMV is determined via the Discounted Cash Flow (DCF) method by a SEBI-registered Merchant Banker or a Chartered Accountant — shares cannot be issued below FMV to prevent under-reporting of FDI.

VJM Global's Chartered Accountants handle FMV determination and RBI compliance filings, keeping NRI investors on the right side of FEMA.

Key Tax Considerations

Corporate Income Tax:

- Standard rate for companies with turnover below ₹400 crore: approximately 26-29% (effective rate including surcharge and cess)

- Section 115BAA concessional rate: 22% base rate, approximately 25.17% effective rate — new Indian subsidiaries can opt in from inception

Dividend Withholding Tax:

| Scenario | WHT Rate |

|---|---|

| Domestic rate (Section 195) | 20% (plus surcharge and cess) |

| India-Singapore DTAA (25%+ equity) | 10% |

| India-Singapore DTAA (<25% equity) | 15% |

To claim the lower DTAA rate, the Singapore-resident shareholder must provide a valid Tax Residency Certificate (TRC) and Form 10F.

Transfer Pricing:

Transactions between the Indian company and any related Singapore entity — such as a parent company — fall under India's Transfer Pricing regulations (Sections 92 to 92F of the Income Tax Act). VJM Global handles Transfer Pricing compliance, including benchmarking studies, documentation, and representation before tax authorities.

Common Mistakes Singapore-Based NRIs Make During Registration

Structural Mistake: Assuming OPC or Sole Proprietorship Is an Option

Many Singapore-based NRIs who are solo entrepreneurs incorrectly pursue OPC registration only to be rejected. FEMA does not permit FDI in OPCs, sole proprietorships, or partnership firms. The correct structure for a single NRI founder is a Private Limited Company with at least one Indian resident director as the second director.

Apostille Timing Error

NRIs consistently underestimate how long the Singapore notarisation and apostille process takes — particularly when multiple directors are involved — and delay it until other steps are already done. This causes the entire SPICe+ filing to stall. Start the apostille process first, not last. Also note that apostilled documents have a general validity period and should be used promptly.

Post-Incorporation Compliance Gap

Many NRI-owned companies receive their Certificate of Incorporation, assume registration is "complete," and miss the mandatory 30-day FC-GPR filing window with RBI. This triggers FEMA compounding proceedings. These post-incorporation steps are non-negotiable legal obligations:

- FC-GPR filing with RBI within 30 days of share allotment

- Bank account opening for the Indian entity

- FLA annual return filed every July with RBI

Frequently Asked Questions

Can an NRI register a company in India?

Yes, NRIs can register a Private Limited Company or LLP in India. FDI is permitted under the automatic route in most sectors (IT, manufacturing, consulting, healthcare, e-commerce marketplace model), and the process can be completed remotely without physically visiting India.

How much will it cost to register a company in India?

Total cost includes government fees (MCA filing fees, stamp duty — which varies by state), professional service fees, and apostille/notarisation charges in Singapore (S$10.70 per document via SAL). Costs vary based on authorised capital and state of incorporation, so obtaining a professional quote is the most reliable way to budget accurately.

Which is better, NRI or OCI?

For company registration purposes, both NRIs and OCIs are treated similarly under FEMA's NDI Rules. OCIs can invest on a non-repatriation basis freely, and on a repatriation basis in most sectors. The key difference is documentation: OCIs must submit their foreign passport along with the OCI card.

What is the new rule of NRI in India?

Under the Income Tax Act, spending fewer than 182 days in India in a financial year triggers NRI tax status. Recent updates to FEMA's NDI Rules have also expanded investment options for both NRIs and OCIs — a CA can confirm the latest provisions applicable to your situation.

Can a Singapore permanent resident (non-Indian) start a company in India?

A Singapore PR of non-Indian origin qualifies as a foreign national, not an NRI. They can still register a Private Limited Company in India under FDI rules — the automatic route applies to most sectors — though documentation differs (notarised and apostilled foreign passport) and NRI-specific FEMA investment provisions do not apply.

Ready to register your company in India from Singapore? VJM Global's team of Chartered Accountants and business setup professionals provides full support across every step — from DSC procurement and SPICe+ filing to FC-GPR compliance and DTAA structuring. Contact us at info@vjmglobal.com or +91 9891576441 to start your incorporation journey today.