Introduction

Singapore-based entrepreneurs and NRIs face significant challenges when establishing a business presence in India. According to MCA data, LLP registrations hit a record 86,476 in FY 2025-26—a 40% increase from the previous year—reflecting growing international interest in this flexible business structure.

You can register a Limited Liability Partnership entirely online without being physically present in India—but Singapore-based partners face requirements around document apostille, Indian resident co-partner obligations, and FEMA compliance that differ from domestic registrations.

This guide walks Singapore residents, Singaporean companies, and NRIs through the full process. Here's what we'll cover:

- Eligibility rules for foreign partners

- Document checklist with apostille requirements

- Five-step MCA portal registration process

- Post-registration compliance obligations including FEMA reporting

Key Takeaways

- At least one designated partner must be an Indian resident (182+ days/year); Singapore partners qualify but cannot be the sole designated partner

- The entire registration process is conducted online via the MCA portal; no physical presence in India required

- All Singapore-issued documents (passport, address proof, LLP agreement) must be apostilled via the Singapore Academy of Law

- Four key steps: obtain DSC and DPIN, reserve a name via RUN-LLP, file the FiLLiP form, then submit the LLP Agreement within 30 days

- Foreign capital contributions trigger FEMA reporting; the LLP must file the required RBI forms within 30 days of receipt

What Is an LLP and Why Singapore-Based Entrepreneurs Choose It for India Entry

A Limited Liability Partnership (LLP) is a separate legal entity governed by the Limited Liability Partnership Act, 2008 in India. It combines a partnership's operational flexibility with a company's limited liability protection, meaning partners' personal assets are shielded from business debts.

Why Singapore-based founders prefer LLPs for India entry:

- The LLP Act imposes no minimum capital requirement, so contribution arrangements stay flexible from day one

- Lower compliance burden — no audit required if annual turnover is below ₹40 lakhs AND partner contribution stays under ₹25 lakhs

- Pass-through taxation — LLPs pay tax at 30% (plus surcharge and cess) on total income, but profit distributions to partners are exempt from tax — no dividend distribution tax applies

- Full commercial operations — unlike branch or liaison offices (which have restrictions on revenue-generating activities), LLPs can conduct full commercial operations, own property, and enter contracts

How LLPs compare to other India entry structures:

| Feature | LLP | Private Limited Co. | Branch / Liaison Office |

|---|---|---|---|

| Board of directors | Not required | Required | Not applicable |

| Statutory audit | Only above ₹40L turnover | Mandatory | Mandatory |

| Dividend distribution tax | Not applicable | Applicable | Not applicable |

| Revenue-generating activities | Fully permitted | Fully permitted | Restricted |

| RBI approval to operate | Not required | Not required | Required |

VJM Global has helped foreign nationals and multinational companies navigate India entry for 30+ years. For Singapore-based founders weighing structure options, that experience translates into fewer missteps during setup and cleaner compliance from the start.

Eligibility Criteria for Singapore-Based Partners

Core requirements for LLP formation:

- Minimum two designated partners required

- At least one designated partner must be a resident of India (stayed in India for 182+ days in the immediately preceding financial year)

- No maximum limit on number of partners

- Foreign nationals and Singapore citizens are permitted as partners

Singapore-specific considerations:

A Singapore citizen or permanent resident with no Indian residency can be a partner but cannot be the sole designated partner—you must have an Indian resident co-designated partner.

A Singapore-based corporate entity (company or LLP) can be a general partner but cannot serve as a designated partner—only individuals qualify for designated partner status.

FDI and sector restrictions:

Capital contributed by a Singapore-based partner to an Indian LLP qualifies as FDI under FEMA — meaning sector restrictions apply. Per the DPIIT Consolidated FDI Policy 2020, LLPs can receive FDI under the automatic route (no prior government approval needed) only in sectors where:

- 100% FDI is allowed through automatic route

- There are no FDI-linked performance conditions

FDI into LLPs is blocked or restricted in the following cases:

- Sectors with FDI caps below 100%

- Sectors requiring prior government approval

- Prohibited sectors: lottery, gambling, real estate business, and tobacco manufacturing

Documents Singapore-Based Partners Must Prepare

Identity and Address Proof

- Valid passport — serves as mandatory identity proof

- Overseas address proof — driving licence, bank statement, or government-issued ID showing address (must not be older than 2 months)

- Recent passport-size photograph

- Notarised English translation — required for all documents in languages other than English

Apostille and Notarisation Requirements

Since Singapore acceded to the Hague Apostille Convention on 16 September 2021, documents issued in Singapore must be apostilled through the Singapore Academy of Law (SAL) — Singapore's designated Competent Authority.

Alternatively, documents can be verified by the Indian High Commission in Singapore.

Documents requiring apostille include:

- Passport copies

- Address proof documents

- LLP Agreement signature pages

Note: The Singapore Embassy cannot apostille documents—all applications must go through SAL.

Indian Registered Office Documents

- Utility bill (electricity, gas, or water) not older than 2 months for the registered address

- No Objection Certificate (NOC) from property owner (if rented)

- Rent or lease agreement (if applicable)

Singapore-based founders usually arrange a registered office address through a trusted contact, co-working space, or professional registered office service in India.

Digital Signature Certificate (DSC)

Each designated partner must obtain a Class 3 DSC from a government-certified certifying authority in India. Singapore-based partners can apply remotely through agencies like eMudhra (with approvals often processed within one hour) or Sify by submitting:

- Passport copies

- Overseas address proof

- Video-based KYC verification

Getting this documentation right the first time matters — incomplete or incorrectly apostilled submissions are one of the most common causes of registration delays. VJM Global works with Singapore-based founders through each step, covering apostille guidance, DSC procurement, and registered office arrangements.

Step-by-Step: How to Register an LLP in India from Singapore

Process overview and timeline:

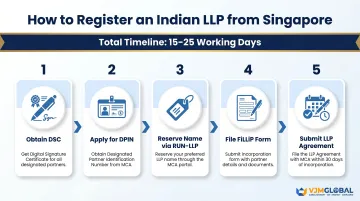

The complete registration process typically takes 15–25 working days for foreign partners—slightly longer than domestic registration due to document apostille time. Here are the five key steps:

Step 1: Obtain Digital Signature Certificate (DSC)

The DSC is the foundational requirement—all MCA portal filings must be digitally signed. Each designated partner needs their own Class 3 DSC.

Singapore-based applicants can apply through government-authorised agencies (eMudhra, Sify) entirely online:

- Apply through eMudhra or Sify using their online portals

- Submit passport and overseas address proof

- Complete video-based KYC verification

- DSC typically issued within 2–3 working days once documents are verified

Step 2: Apply for Designated Partner Identification Number (DPIN)

The DPIN (or DIN) is a unique number issued by the MCA to each designated partner. There are two ways to obtain it:

- Via FiLLiP (Step 4) — new applicants can apply for DPIN directly through the incorporation form, so a separate filing isn't required

- Via Form DIR-3 — file in advance on the MCA portal with scanned identity/address proof, signed by a practicing Chartered Accountant or Company Secretary in India

Step 3: Name Reservation via RUN-LLP

Reserve the proposed LLP name using the RUN-LLP service on the MCA portal.

The name must end with "LLP" or "Limited Liability Partnership," must not resemble existing companies or registered trademarks, and must not be offensive or misleading. Each application allows up to 2 name proposals for a fee of ₹200.

Approval or rejection typically comes within 2–3 working days. Once approved, incorporation must be completed within 3 months.

Step 4: File the FiLLiP Incorporation Form

FiLLiP (Form for Incorporation of Limited Liability Partnership) is the main incorporation form filed on the MCA portal. It captures partner details and DPIN information, the registered office address, capital contribution amounts, objects of the LLP, and attached documents (identity proof, address proof, office proof, NOC).

All designated partners digitally sign the form using their DSCs. It is then submitted to the Registrar of Companies (ROC) with jurisdiction over the state of the registered office. Once approved, the ROC issues the Certificate of Incorporation electronically.

Step 5: Draft and File the LLP Agreement (Form 3)

With incorporation complete, the final step is filing the LLP Agreement—the document that governs mutual rights and duties of partners.

The agreement must cover:

- Capital contribution details

- Profit-sharing ratios

- Decision-making processes

- Partner exit provisions

Critical deadline: Form 3 must be filed on the MCA portal within 30 days of incorporation under Section 23 of the LLP Act.

For Singapore-based partners, the agreement must be printed on stamp paper (stamp duty varies by state) and signed by all partners. Partners signing overseas must have the agreement pages apostilled through SAL or verified by the Indian High Commission in Singapore before submission.

Post-Registration Compliance and FEMA Considerations

Annual Compliance Obligations

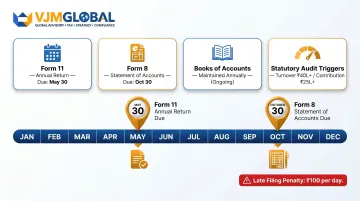

Once your LLP is registered, you must meet these recurring deadlines each year:

- Form 11 (Annual Return) — due by May 30 (within 60 days of the March 31 financial year-end)

- Form 8 (Statement of Accounts and Solvency) — due by October 30

- Books of accounts — must be properly maintained at all times

- Statutory audit — required if turnover exceeds ₹40 lakhs OR partner contribution exceeds ₹25 lakhs

Late filing attracts ₹100 per day per form from the due date — with no maximum cap. Continued non-filing for two or more consecutive years may result in strike-off of the LLP and disqualification of designated partners.

FEMA Reporting for Foreign Capital

When a foreign partner contributes capital to an Indian LLP, it constitutes FDI and must be reported to the Reserve Bank of India (RBI). Missing these filings is one of the most frequent compliance gaps for foreign-founded LLPs — set calendar reminders before you receive the first capital transfer.

- File Form LLP-I within 30 days of receiving capital contribution through the FIRMS Portal

- File Form LLP-II within 60 days for any transfer of capital contribution between resident and non-resident

- Receive funds only through banking channels

- Ensure capital contribution is priced at fair value per RBI valuation guidelines

Tax Registrations Required After Incorporation

Once the LLP is live, three tax registrations typically apply:

- PAN (Permanent Account Number) — required for filing income tax returns

- TAN (Tax Deduction and Collection Account Number) — required if the LLP is responsible for tax deduction at source

- GST registration — mandatory if turnover exceeds ₹40 lakhs (₹20 lakhs for services in most states); also required for inter-state supply or e-commerce operations

With these in place, your LLP can operate and transact in full compliance — and is positioned to benefit from the India-Singapore tax treaty.

India-Singapore DTAA Benefits

The Agreement between India and Singapore for Avoidance of Double Taxation protects Singapore-resident partners from being taxed twice on the same income. Key provisions:

- Business profits — taxable only in the state of residence, unless the entity operates through a Permanent Establishment in India

- Double taxation relief — the Credit Method applies, meaning tax paid in one country is allowed as a credit against tax liability in the other

- Dividend withholding tax — capped at 10% if the beneficial owner holds at least 25% of shares; 15% otherwise

Singapore-based partners should work with an international tax advisor — VJM Global's international tax team handles DTAA structuring regularly — to structure profit distributions efficiently under the treaty.

Frequently Asked Questions

What are the steps to register an LLP in India?

The four key steps are: obtain DSC and DPIN for all designated partners, reserve the LLP name via RUN-LLP on the MCA portal, file the FiLLiP incorporation form with the ROC, and submit the LLP Agreement (Form 3) within 30 days of incorporation.

Who is eligible for LLP?

Any individual (Indian or foreign national, including Singapore citizens) can be a partner. A minimum of two designated partners is required, with at least one being a resident of India (stayed 182+ days in the preceding financial year). Minors, persons of unsound mind, and undischarged insolvents cannot be partners.

Is GST compulsory for LLP?

GST registration is not mandatory at incorporation. It becomes compulsory only when annual turnover exceeds ₹40 lakhs (for goods) or ₹20 lakhs (for services). LLPs engaged in inter-state supply or operating through e-commerce platforms must register regardless of turnover.

Can a Singapore citizen register an LLP in India without visiting India?

Yes, the entire process is conducted online via the MCA portal. Singapore-based partners can obtain DSC remotely, sign documents digitally, and apostille the LLP agreement locally. Physical presence in India is not required, though a trusted Indian resident must serve as co-designated partner.

Do Singapore-based LLP partners need to comply with FEMA when contributing capital?

Yes, contributions from Singapore-based partners constitute FDI under FEMA. Funds must come through banking channels, and the LLP must report receipt to RBI within 30 days via the FIRMS portal (Form LLP-I). Most sectors permit FDI under the automatic route, requiring no prior government approval.

Need expert assistance with LLP registration from Singapore? VJM Global has 30+ years of experience helping foreign nationals establish business operations in India. Our team handles the full LLP setup process—from document apostille and DSC procurement to FEMA compliance and ongoing annual filings. Contact us at info@vjmglobal.com or +91 9891576441 for a consultation.