Introduction

You're an Indian manufacturer expanding exports beyond Asia, or an IT services provider looking for a tax-efficient base for global clients. Dubai makes sense—strategically located, business-friendly, connected to every major market. Then you encounter the term "FZE" in incorporation guides. What does it mean? How is it different from other Dubai structures? And what does owning one mean for your compliance obligations back in India?

For Indian entrepreneurs, the FZE structure is worth understanding in detail. This guide explains the structure clearly and covers the India-specific compliance implications most setup guides skip—FEMA reporting, RBI's Overseas Direct Investment (ODI) framework, and the India-UAE Double Taxation Avoidance Agreement (DTAA).

TLDR

- FZE (Free Zone Establishment) is a single-shareholder company registered in one of Dubai's 20+ designated free zones, offering 100% foreign ownership and 0% corporate tax on qualifying income

- Key difference from FZCO: FZE has exactly one owner; FZCO allows 2-50 shareholders, making it suitable for partnerships

- Indian nationals can own a Dubai FZE outright, but must comply with FEMA regulations and RBI's ODI framework, including Annual Performance Reports due by December 31 each year

- Best suited for solo entrepreneurs, exporters, or professionals seeking a credible Dubai base for global operations—not for businesses primarily targeting UAE mainland customers

- India-UAE bilateral trade crossed USD 100 billion in FY 2025-26, making this one of the most mature business corridors for Indian entrepreneurs

What is FZE in Dubai?

A Free Zone Establishment (FZE) is a single-shareholder limited liability company registered within one of Dubai's designated free zones. The sole shareholder can be either an individual (such as an Indian national) or a corporate entity (such as an Indian company). The FZE possesses a separate legal personality from its owner, meaning your personal assets remain shielded from business liabilities—your financial exposure is capped at the capital you've invested.

The Free Zone Ecosystem

Dubai operates more than 20 specialized free zones (part of the UAE's 40+ national network), each governed by its own regulatory authority. Dubai built these zones to attract international business, offering advantages traditional mainland structures couldn't match:

- 100% foreign ownership with no UAE national partner required

- 0% customs duty on goods imported into the free zone or stored for re-export

- Faster setup procedures with sector-specific licensing

However, this comes with a critical operational constraint: FZEs cannot sell directly to UAE mainland customers without appointing a licensed local distributor or establishing a separate mainland entity. Your FZE can trade internationally, transact with other free zone companies, and re-export goods, but direct mainland market access requires additional licensing.

Popular free zones for Indian entrepreneurs include:

- DMCC (Dubai Multi Commodities Centre): Trading, commodities, precious metals

- IFZA (International Free Zone Authority): Services, consulting, technology

- RAKEZ (Ras Al Khaimah Economic Zone): Cost-conscious SMEs, light manufacturing

- JAFZA (Jebel Ali Free Zone): Logistics, warehousing, import-export

Governance and Compliance Requirements

Setting up an FZE is just the beginning. Ongoing obligations include:

Annual Requirements:

- Trade licence renewal (typically before expiry date)

- Audited financial statements submission to free zone authority

- Corporate tax return filing (if applicable)

- Registered office address maintenance (physical office or flexi-desk)

UAE Corporate Tax Framework:

Under Federal Decree-Law No. 47 of 2022, the UAE introduced corporate taxation effective from June 2023:

| Income Type | Tax Rate | Threshold/Condition |

|---|---|---|

| Standard corporate income | 0% | Taxable income up to AED 375,000 |

| Standard corporate income | 9% | Taxable income exceeding AED 375,000 |

| Qualifying Free Zone Person—qualifying income | 0% | Must meet substance and activity criteria |

| Qualifying Free Zone Person—non-qualifying income | 9% | Income from mainland UAE or excluded activities |

To claim the 0% rate on qualifying income, your FZE must meet all four conditions:

- Maintain adequate substance in the UAE (real office, employees, genuine operations)

- Derive income from qualifying activities (international trade, intra-free-zone transactions)

- Remain on the qualifying free zone regime (not opted into standard taxation)

- Comply with transfer pricing documentation requirements

For Indian entrepreneurs specifically: if your FZE earns revenue from UAE mainland customers exceeding AED 375,000, that income is classified as non-qualifying and taxed at 9%. The 0% rate requires deliberate structuring and active compliance — it is not applied by default.

FZE vs. FZCO: Key Differences Indian Owners Should Know

The choice between FZE and FZCO hinges on one factor: how many shareholders you need.

| Feature | FZE | FZCO |

|---|---|---|

| Shareholders | Exactly 1 (individual or corporate) | 2 to 50 |

| Ideal for | Solo founders, wholly-owned subsidiaries | Joint ventures, co-founders, investor structures |

| Management | Single decision-maker | Requires board of directors for multi-shareholder governance |

| Capital requirements | Generally lower minimum capital | Varies by free zone; same as FZE in most cases |

| Setup complexity | Simpler (fewer KYC documents, single MOA) | More documentation (multiple shareholders, board resolutions) |

| Conversion flexibility | Can convert to FZCO when adding shareholders | Can convert to FZE if reduced to single shareholder |

When to Choose FZCO Over FZE

Choose FZCO if you're:

- Co-founding a Dubai venture with a partner

- Planning to bring in equity investors (Indian or international)

- Structuring a joint venture with a UAE or foreign entity

- Setting up a subsidiary with multiple shareholders from the parent group

You're not locked into your initial choice. JAFZA and other free zones allow conversion from FZE to FZCO (or vice versa) without dissolving and re-incorporating.

The process requires updated documentation — a new Memorandum of Association, shareholder KYC, and board resolutions — plus an appointment with the free zone's licensing team. Your trade licence and business continuity remain intact throughout.

Liability Protection: Same for Both

Both FZE and FZCO offer limited liability, which matters practically for Indian entrepreneurs with assets back home. Your financial exposure is capped at your capital contribution, meaning your home in India, savings, and other personal investments stay protected from business creditors.

This protection does not exist under sole proprietorship structures, where personal and business liability merge completely.

Other Entity Types You Might Encounter

- Mainland LLC: Allows direct access to UAE mainland market but historically required a local sponsor (though recent reforms now permit 100% foreign ownership in many sectors)

- Offshore company: Tax-efficient holding structure with no physical office requirement, but cannot conduct business within the UAE

- Branch office: Extension of the parent company (not a separate legal entity), suitable for project-based work

For Indian entrepreneurs prioritising full ownership and straightforward setup, FZE is typically where to start — with the option to scale into an FZCO structure as your ownership or investor base grows.

Key Benefits of an FZE in Dubai for Indian Entrepreneurs

100% Foreign Ownership—No Local Partner Required

Unlike mainland UAE companies which historically required a 51/49 ownership split favouring a UAE national, free zone FZEs allow Indian nationals to own the entire business outright. No profit-sharing obligations, no sponsor fees, complete control.

Tax Efficiency for International Operations

Two-layer tax benefit:

- 0% corporate tax on qualifying income (international sales, intra-free-zone transactions)

- 0% personal income tax on salaries and dividends in the UAE

For an Indian IT services provider billing clients in the US, UK, and Australia from a Dubai FZE, this means every dollar of qualifying revenue is taxed at 0% at the entity level—a significant advantage over operating from India (where corporate tax can reach 25-30% depending on turnover).

Customs duty exemption: Goods imported into the free zone or stored for re-export face zero customs duty, making it practical for Indian traders to use Dubai as a re-export hub to Africa, Europe, or the Middle East.

India Leads Dubai Business Registrations

Dubai Chamber of Commerce registered 13,851 new Indian companies in Q1-Q3 2025—a 13.9% year-over-year growth. India topped the list of non-UAE company registrations, ahead of Pakistan (6,850), Egypt (3,754), and the United Kingdom (2,071). For Indian entrepreneurs, these numbers signal well-worn regulatory paths, established banking relationships, and a peer network that makes the setup process far less uncertain than in most other jurisdictions.

Booming India-UAE Trade Creates Direct Opportunities

Bilateral merchandise trade nearly doubled from USD 43.3 billion in FY 2020-21 to USD 83.7 billion in FY 2023-24 following the India-UAE Comprehensive Economic Partnership Agreement (CEPA). Commerce Minister Piyush Goyal confirmed bilateral trade reached USD 101.25 billion in FY 2025-26, crossing the USD 100 billion milestone for the first time.

Key figures from that trade expansion:

- 240,000+ Certificates of Origin filed under CEPA preferential duties

- USD 19.87 billion in Indian exports enabled through those certificates

- India-UAE bilateral trade grew ~134% over four fiscal years

For Indian manufacturers and exporters, a Dubai FZE positions you directly inside this trade corridor—not watching it from the outside.

Speed and Ease of Setup

With this level of trade activity, speed to market matters. Most free zones now support remote registration:

- RAKEZ: Company registration completed within 4 working days

- IFZA: 100% remote setup without in-person UAE visit required

- DMCC: Pre-approval takes 7 working days to 1 month

While some steps—visa stamping, bank account opening—may still require an in-person visit, the initial incorporation can often be completed from India with digital document submission.

Tax and Compliance Considerations for Indian Nationals Owning a Dubai FZE

Most guides cover how to set up a Dubai FZE. For Indian entrepreneurs, the harder question is what happens after — because establishing an FZE triggers compliance obligations in both the UAE and India simultaneously.

FEMA and Overseas Direct Investment (ODI): India-Side Framework

Indian residents setting up an FZE must comply with the Foreign Exchange Management Act (FEMA) under the RBI's Overseas Direct Investment framework.

Two routes for funding:

1. Liberalised Remittance Scheme (LRS):

- Permits Indian resident individuals to remit up to USD 250,000 per financial year (April-March) for eligible purposes, including ODI

- No prior RBI approval required within this limit

- LRS cap is cumulative across all overseas remittances (not just business investment)

2. Formal ODI Route:

- Required for investments exceeding USD 250,000

- Requires reporting through an Authorised Dealer (AD) Bank

- May require RBI approval depending on investment size and structure

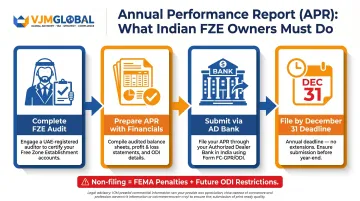

Mandatory Annual Performance Report (APR) Filing

Under RBI's Master Direction on Overseas Investment (dated August 22, 2022), Indian residents making an ODI must file Annual Performance Reports (APR) for each foreign entity.

APR requirements:

- Filing deadline: December 31 each year

- Mandatory regardless of operational status (even if FZE is dormant or loss-making)

- Must include audited financial statements of the FZE; if UAE does not mandate audits for your FZE (rare—most major free zones require it), an Indian Chartered Accountant may audit for APR purposes

- Filed through your AD Bank

Consequences of non-filing: FEMA violations attract penalties and can jeopardize future ODI applications. This is not optional paperwork—it's a legal obligation.

India-UAE DTAA: Avoiding Double Taxation

The India-UAE Double Taxation Avoidance Agreement (effective since 1993, amended in 2007 and 2013) helps prevent the same income from being taxed in both countries.

Key treaty provisions:

| Income Type | Maximum Withholding Tax | Treaty Article |

|---|---|---|

| Dividends | 10% | Article 10 |

| Interest (bank loans) | 5% | Article 11 |

| Interest (other) | 12.5% | Article 11 |

| Royalties | 10% | Article 12 |

Permanent Establishment (PE) thresholds:

- Construction projects create a PE only if they continue for more than 9 months

- Consultancy services create a PE if activities continue for more than 9 months within any 12-month period

Tax residency determines treaty access: To claim DTAA benefits, you must establish tax residency in the UAE, which requires meeting specific criteria under Cabinet Resolution No. 85 of 2022.

UAE Tax Residency: Three Paths

Effective March 1, 2023, individuals can establish UAE tax residency through:

1. 183-day rule: Physical presence of 183 days or more during any 12 consecutive months

2. 90-day rule: Physical presence of 90 days or more during 12 consecutive months, plus one of:

- UAE nationality

- Valid UAE residence permit

- GCC nationality

You must also have a permanent place of residence or be actively practicing a job or business in the UAE.

3. Centre of interests: Main place of residence and centre of financial/personal interests is in the UAE

Critical for Indian entrepreneurs: Carefully track days spent in both countries. Dual residency (meeting residency tests in both India and UAE) creates complex tie-breaker scenarios under the DTAA. Professional tax advice is essential.

Residential Status Impact: The India Tax Trap

Under Section 5 of the Indian Income Tax Act, 1961, a person who is "resident and ordinarily resident" in India is taxed on their entire world income, wherever accrued or received.

Two scenarios:

Scenario 1: NRI/OCI Setting Up an FZE

- If you've established non-resident status in India (typically by spending less than 182 days in India during the financial year), your FZE profits are generally not taxable in India unless they're India-sourced

- DTAA provides additional relief from double taxation

- Fewer India-side tax complications

Scenario 2: Resident Indian Setting Up an FZE

- If you remain resident and ordinarily resident in India, your global income—including FZE profits—is taxable in India

- Even if the FZE pays 0% corporate tax in the UAE, any income attributed to you (dividends, deemed accrual) may be assessed under Indian tax law

- DTAA may provide credit for taxes paid in the UAE, but the Indian tax obligation remains

The structural tension: You can benefit from UAE's 0% corporate tax on qualifying income, but if you're an Indian resident, that income may still be taxable in India when distributed or deemed accrued to you. Proper structuring—timing of dividend repatriation, salary vs. dividend mix, treaty application—becomes critical.

Where VJM Global Comes In

The intersection of UAE free zone rules and Indian tax and FEMA compliance requires advice that covers both sides of the equation. VJM Global — with 30+ years of experience and a dedicated team of Chartered Accountants — helps Indian business owners stay structured and compliant in both jurisdictions.

VJM Global's cross-border India-UAE services include:

- FEMA compliance advisory: Guidance on ODI framework, LRS remittances, and foreign exchange regulations

- Annual Performance Report (APR) filing: End-to-end preparation and timely submission to RBI through your AD bank, including coordination with UAE auditors

- Indian income tax disclosure: Advisory on tax residency status, global income taxation, DTAA application, and annual ITR filing for foreign entity owners

- Tax structuring: Optimizing the timing and structure of dividend repatriation, salary, and other income flows to minimize dual taxation

- Ongoing compliance coordination: Ensuring alignment between UAE audit/tax filing timelines and India-side reporting deadlines

How to Set Up a Dubai FZE as an Indian National

Step-by-Step Process

1. Choose the Right Free Zone Match your business activity to the zone's specialization and budget:

- DMCC: Commodities trading, diamond/gold trading, professional services (higher cost, premium network)

- IFZA: IT services, consulting, creative industries (100% remote setup supported)

- RAKEZ: Manufacturing, trading, services (cost-effective, fast 4-day setup)

- JAFZA: Logistics, warehousing, import-export (largest free zone)

- SHAMS: Media, marketing, creative services

2. Select Trade Name Check name availability through the free zone portal. Name must comply with UAE naming regulations (avoid religious or offensive terms, comply with activity description).

3. Prepare and Submit Documents

Standard documents for Indian nationals:

- Valid Indian passport copy (minimum 6 months validity)

- Recent passport-sized photographs (white background)

- Proof of residential address (utility bill or bank statement, not older than 3 months)

- Business activity description or business plan

- KYC form (generated by free zone portal for shareholder and directors)

- Ultimate Beneficial Owner (UBO) declaration

If shareholder is an Indian company (corporate FZE):

- Certificate of Incorporation

- Memorandum and Articles of Association

- Board resolution authorizing the investment

- Corporate documents typically require attestation (2-3 week process)

4. Obtain Initial Approval Submit documents through free zone portal. Pre-approval timelines:

- RAKEZ: 4 working days

- DMCC: 7 working days to 1 month

- IFZA: 5-7 working days

5. Pay Fees and Finalize Licence Pay licence fees, lease agreement for office space (minimum 1 year), and share capital deposit (varies by free zone). Receive trade licence and company incorporation certificate.

Post-Setup Steps Often Overlooked

Getting your licence is only half the work. These four steps trip up most first-time FZE owners — plan for them before you finalize your setup timeline.

1. Open a Corporate Bank Account UAE banks apply strict due diligence for free zone companies. Required documents typically include:

- Trade licence and company incorporation certificate

- Memorandum of Association

- Shareholder and director passports and Emirates ID

- Source of funds documentation (bank statements, proof of income, tax returns from India)

- Business plan and revenue projections

Account opening takes 2-4 weeks. Most banks require at least one in-person meeting, so plan your UAE visit accordingly. Popular business banks include Emirates NBD, Mashreq, ADCB, and RAKBank.

2. Apply for a UAE Residence Visa FZE owners can sponsor investor visas for themselves and employment visas for staff. The investor visa is valid for 3 years (renewable) and requires:

- Medical fitness test and Emirates ID registration

- In-person visit to UAE (can be combined with bank account opening)

- No immigration deposit required for the investor visa

3. Register for VAT VAT registration is mandatory once your taxable supplies and imports exceed AED 375,000. Voluntary registration is available from AED 187,500. Register through the UAE Federal Tax Authority portal.

4. Appoint an External Auditor Most free zones — including DMCC, JAFZA, RAKEZ, IFZA, and SHAMS — require annual audited financial statements. Appoint a free-zone-approved auditor after licensing. Budget AED 5,000–15,000 annually depending on your turnover and business complexity.

Is an FZE the Right Structure for Your Indian Business?

When FZE Makes Strong Sense

An FZE is ideal if you're:

- A solo entrepreneur seeking international presence without multi-shareholder complexity

- An IT/software exporter billing global clients (US, UK, Europe, Australia) from a tax-efficient base

- A trader using Dubai as a re-export hub (import from China, re-export to Africa/Middle East)

- A professional services provider (consultant, designer, marketer) wanting a credible international address

- Setting up a wholly-owned subsidiary of your Indian parent company

When FZE May Not Be Ideal

Reconsider if:

- Your primary market is UAE mainland consumers—you'll need a local distributor or mainland licence anyway

- You're raising equity from multiple investors from day one—FZCO's multi-shareholder structure is more appropriate

- You need significant local hires and physical infrastructure in India—a simpler Indian entity structure may suffice

- You're an Indian resident unwilling to manage dual-jurisdiction compliance (FEMA + UAE)—the ongoing reporting burden is real

Beyond Setup: The Compliance Reality

Incorporating the FZE takes 5-10 days. Maintaining it requires active management:

UAE-side (Annual):

- Trade licence renewal

- Audited financial statements submission

- Corporate tax return filing (if taxable income exceeds AED 375,000 or you're a QFZP)

- VAT returns (if registered)

India-side (Annual):

- Annual Performance Report (APR) to RBI by December 31

- Income tax return disclosure of foreign assets and income

- FEMA compliance updates if shareholding/investment changes

Both sets of obligations run simultaneously—missing a deadline in either jurisdiction can trigger penalties or compliance flags.

Many Indian entrepreneurs treat the Dubai FZE as a "set and forget" entity. It isn't. Active governance, proper bookkeeping, and timely filings in both jurisdictions are non-negotiable from year one.

Before incorporating, get clarity on free zone selection, QFZP qualifying income criteria, Indian tax residency implications, and realistic ongoing compliance costs. Structural errors at this stage are expensive to unwind later.

Frequently Asked Questions

What does FZE mean?

FZE stands for Free Zone Establishment—a single-shareholder limited liability company registered within a UAE designated free zone. It offers 100% foreign ownership, limited personal liability, and eligibility for 0% corporate tax on qualifying income.

What is the difference between FZE and FZCO in Dubai?

The core difference is ownership: an FZE has exactly one shareholder (individual or corporate), while an FZCO allows 2-50 shareholders. FZE suits solo founders; FZCO suits partnerships, joint ventures, or businesses anticipating multiple investors.

What does FZ mean in UAE?

FZ stands for Free Zone—a designated area within the UAE where businesses operate under a separate regulatory framework offering incentives like 100% foreign ownership, tax exemptions, and zero customs duty. Dubai has 20+ free zones.

Can an Indian citizen own 100% of an FZE in Dubai?

Yes, Indian nationals can own 100% of a Dubai FZE without requiring a UAE national partner. However, they must comply with India's FEMA regulations and report the overseas investment to the RBI under the LRS or ODI framework.

Is income from a Dubai FZE taxable in India?

For Indian residents (persons ordinarily resident in India), global income—including FZE profits—is generally taxable under Section 5 of the Income Tax Act. The India-UAE DTAA may reduce double taxation but does not eliminate the Indian obligation. NRIs and OCIs face different rules, so professional tax advice is essential.

Do FZE companies in Dubai need to file audited accounts?

Yes, most Dubai free zones—including DMCC, JAFZA, RAKEZ, IFZA, and SHAMS—require FZEs to submit audited financial statements annually. Under the UAE corporate tax regime, companies must also maintain proper books and file tax returns accordingly.

Setting up a Dubai FZE as an Indian entrepreneur involves both UAE formation and Indian compliance obligations. VJM Global's cross-border advisory team specializes in FEMA reporting, ODI structuring, APR filings, and dual-jurisdiction tax planning for Indian founders. Reach us at info@vjmglobal.com or call +91 9891576441.