Introduction

Indian entrepreneurs are increasingly looking to Singapore as their preferred offshore hub. India ranks among the top source countries for foreign business registrations in Singapore — and with good reason. Bilateral trade hit USD 34.3 billion in FY 2024-25, the India-Singapore DTAA cuts cross-border tax friction, and Singapore sits at the centre of ASEAN's 671.7 million consumer market.

This guide is written for:

- Indian founders setting up their first offshore entity

- SMEs planning to scale into Southeast Asian markets

- NRIs and OCIs exploring a Singapore base

- Tech and e-commerce businesses seeking a global-facing headquarters

Unlike generic incorporation guides, this article covers the India-side requirements most resources skip — specifically FEMA compliance and RBI Overseas Direct Investment (ODI) filings — alongside the full Singapore setup process.

Whether you're staying in India and operating remotely or relocating to Singapore, you'll find everything needed to handle both jurisdictions without missing a regulatory step.

Key Takeaways

- Indian nationals can own 100% of a Singapore company but must appoint at least one locally resident director and use a registered filing agent

- Minimum paid-up capital is S$1; government fees total S$315 (S$15 name reservation + S$300 registration)

- Complete FEMA and RBI ODI compliance before remitting capital; non-compliance triggers penalties under Indian law

- Private Limited Company (Pte Ltd) offers limited liability, tax advantages, and credibility with banks and investors

- Expect 1–3 business days for incorporation once documents are ready, plus 2–4 weeks to open a corporate bank account

Why Indian Entrepreneurs Are Choosing Singapore

Singapore consistently ranks as one of the world's most business-friendly jurisdictions. The IMD World Competitiveness Yearbook 2024 placed Singapore 1st out of 67 economies, while the World Bank Business Ready 2024 report scored Singapore in the top 20% globally for regulatory framework, public services, and business entry (94/100 points).

Key advantages for Indian founders:

- India-Singapore DTAA caps withholding tax on dividends at 10% (when the Singapore parent holds at least 25% equity), eliminating double taxation

- Capital gains are generally not taxable unless classified as trading activity

- Corporate tax is capped at 17%, with startup exemptions bringing effective rates as low as 4.25% for the first three years

- 100% foreign ownership is permitted, with no restrictions on shareholding or profit repatriation

- Singapore serves as a gateway to 671.7 million consumers across Southeast Asia through ASEAN membership

- EntrePass and Employment Pass provide clear immigration pathways for founders and senior executives

These advantages stack up in ways that matter specifically to Indian founders: favourable tax treaty terms, a familiar common-law business environment, and proximity to both Indian and Southeast Asian markets.

Unlike most Western jurisdictions, Singapore imposes no complex residency requirements for foreign ownership. Indian entrepreneurs can structure their business remotely or relocate through established visa pathways — the infrastructure supports both approaches equally.

What Indian Founders Must Know Before Setting Up

Starting a Singapore company from India is not just a Singapore process. Indian founders must first satisfy Indian outbound investment regulations before a single dollar of capital can be moved. Skipping this step creates compliance risk in both jurisdictions.

FEMA and RBI Overseas Direct Investment (ODI) Framework

Under the Foreign Exchange Management Act (FEMA) and RBI's Overseas Investment Regulations 2022, Indian residents (individuals and companies) remitting funds to set up a foreign entity must:

- File Form FC with an authorised dealer (AD) bank to obtain a Unique Identification Number (UIN) before sending any outward remittance

- Comply with the Liberalised Remittance Scheme (LRS), which permits resident individuals to remit up to USD 250,000 per financial year (April–March)

- Submit proper documentation to the AD bank for all capital transfers

- File Annual Performance Reports (APR) by December 31 each year based on audited financials of the foreign entity

Penalties for non-compliance:

- Late Submission Fee (LSF): INR 7,500 + (0.025% × Amount × years of delay), capped at 100% of the amount

- FEMA Section 13 penalties: Up to three times the sum involved, plus potential confiscation of foreign security

Realistic Timeline and Hands-On Involvement

While Singapore registration itself can be completed in 1–3 business days, India-side regulatory preparation typically adds 2–4 weeks to the overall timeline. This includes:

- ODI form preparation and submission

- Document notarisation and apostille (India acceded to the Apostille Convention, so Indian apostilled documents are accepted directly in Singapore)

- AD bank processing and UIN issuance

- Capital remittance approval

Physical Presence Question

Indian nationals who plan to remain in India can still own and operate a Singapore company remotely. The requirement: appoint a nominee director who is ordinarily resident in Singapore. You retain full ownership and control through shareholder rights.

For founders who want to relocate and act as resident director, Singapore offers two main visa routes: an EntrePass for innovative startups, or an Employment Pass requiring a minimum S$5,600 monthly salary and 40 COMPASS points.

Key Early Decisions

Your residency decision connects directly to your entity structure choice. Whether you're an individual founder or an established Indian company determines which Singapore setup path applies — and each carries different ODI, transfer pricing, and compliance implications:

- Fresh Pte Ltd: Common for new ventures by individual Indian founders with no existing Indian entity

- Singapore Subsidiary: Preferred when an established Indian parent company already exists and the Singapore entity is an extension, allowing profit repatriation and intra-group service fees under the India-Singapore Double Taxation Avoidance Agreement (DTAA)

Choosing the Right Business Structure as an Indian National

Singapore offers several business vehicles to foreign individuals and companies. For Indian founders, two structures stand out: the Private Limited Company (Pte Ltd) and the Subsidiary Company.

Private Limited Company (Pte Ltd)

The Pte Ltd is the most credible structure for banking, fundraising, and client contracts.

Key features:

- Separate legal entity with limited liability

- 100% foreign ownership allowed

- 1–50 shareholders permitted

- Corporate tax at 17% with startup exemptions (75% exemption on first S$100,000 of chargeable income for three years)

- Qualifies for Singapore tax residency if controlled and managed in Singapore

- Requires at least one locally resident director

Contrast with Sole Proprietorship:

- No separate legal identity

- Unlimited personal liability

- Better suited only for micro-businesses with minimal risk

The Pte Ltd works well for most individual founders — but if you already run an established Indian company, a Subsidiary structure may serve you better.

When to Choose a Singapore Subsidiary vs. Fresh Pte Ltd

| Feature | Singapore Subsidiary | Fresh Pte Ltd |

|---|---|---|

| Best for | Established Indian parent company seeking regional presence | Individual Indian founders starting new venture |

| Legal relationship | Parent-subsidiary structure maintained | Standalone entity |

| Repatriation | Structured dividend flows under DTAA | Direct shareholder distributions |

| Transfer pricing | Intra-group contracts require arm's length documentation | Not applicable if no related parties |

| Tax residency | Singapore tax resident if controlled/managed in Singapore | Singapore tax resident if controlled/managed in Singapore |

| Liability | Limited to subsidiary's assets | Limited to company's assets |

Once you've identified the right structure, the next step is understanding Singapore's registration requirements and timelines.

How to Set Up a Business in Singapore from India: Step by Step

Indian founders need to complete India-side compliance before touching Singapore registration. Reversing the order creates FEMA penalties and capital remittance problems that are difficult to unwind.

Step 1 – Sort India-Side Regulatory Compliance First

Before any Singapore registration activity, Indian founders must complete their ODI filings under FEMA. You must file Form FC with your authorised dealer bank to obtain a UIN before sending outward remittance or acquiring equity capital.

Common miss: Indian founders who register the Singapore company first and attempt to remit capital afterwards without prior ODI filings face penalties under FEMA Section 13.

How VJM Global can help: VJM Global offers FEMA advisory and ODI compliance services—covering form preparation, AD bank coordination, and documentation support—so your capital remittance is fully compliant before incorporation.

Step 2 – Define the Business Objective, Model, and Structure

Decide whether the Singapore entity will serve as a regional HQ, a trading/invoicing hub, a tech holding company, or a service delivery arm. This determines:

- The most appropriate structure (fresh Pte Ltd vs. Subsidiary)

- The SSIC (Singapore Standard Industrial Classification) business activity code selection during registration

- Future licensing and regulatory requirements

Common miss: Selecting a vague or mismatched SSIC code during registration creates friction with licensing, banking, and regulatory classification later.

Step 3 – Reserve the Company Name via BizFile+

Use Singapore's BizFile+ portal (managed by ACRA) to check availability and reserve the company name. The fee is S$15 and the reservation is valid for 120 days.

Naming rules:

- No offensive words

- No names identical or deceptively similar to existing entities

- No restricted or regulated terms without approval

Since Indian nationals cannot self-register on BizFile+ (foreigners must engage a registered filing agent), this step is typically handled by the appointed corporate service provider.

Step 4 – Appoint a Resident Director and Corporate Secretary

Singapore law requires at least one director who is ordinarily resident in Singapore (citizen, PR, or valid work pass holder). Indian nationals who are not relocating must appoint a nominee director through a registered corporate service provider.

Important: A nominee director does not have access to company funds or operational control. A formal agreement protects the founder's ownership and decision-making authority.

A company secretary must also be appointed within six months of incorporation. They manage statutory filings, annual returns, and regulatory compliance.

Step 5 – Prepare and Submit Incorporation Documents

Compile the required documents:

- Passport copies of all directors and shareholders

- Proof of residential address

- Company constitution (standard ACRA model or customised)

- Registered Singapore office address

- Share structure details

- SSIC code

Indian documents may require apostille or notarisation. Since Singapore acceded to the Apostille Convention (effective 16 September 2021), Singapore accepts apostilled Indian documents directly—no further legalisation needed.

Submit the full incorporation application on BizFile+ through the registered filing agent. In straightforward cases, ACRA approves within 1–3 business days and issues a Unique Entity Number (UEN) and Certificate of Incorporation.

Step 6 – Open a Corporate Bank Account in Singapore

Most Singapore banks (DBS, OCBC, UOB) require the following before activating a corporate account:

- In-person signing or video KYC

- Certificate of Incorporation

- Company BizFile profile

- KYC documents for all directors and beneficial owners

For Indian founders who cannot travel, some banks offer remote account opening (OCBC offers 100% remote onboarding) or digital bank alternatives like Airwallex (48-hour processing) and Wise Business.

Common miss: Underestimating the time and documentation required for bank KYC—plan for 2–4 weeks from incorporation for a bank account to be fully operational.

Step 7 – Register for GST and Obtain Necessary Licenses

GST (Goods and Services Tax) registration in Singapore is mandatory once annual taxable turnover exceeds S$1 million. The current GST rate is 9% effective 1 January 2024.

Voluntary registration is available below the threshold and can benefit B2B companies claiming input tax credits. Key conditions:

- Remain registered for at least 2 years

- Maintain a GIRO account with IRAS

- Fulfil all ongoing GST compliance obligations

Depending on the business activity, specific licenses or permits may be required (financial services, food, education, healthcare)—verify requirements via Singapore's GoBusiness portal.

Step 8 – Set Up Accounting, Payroll, and Ongoing Compliance

Singapore companies must maintain proper accounting records, file annual returns with ACRA, and submit corporate income tax returns with IRAS. Appoint an accounting or corporate services firm early to ensure these obligations are met from the first financial year.

How VJM Global can help: VJM Global manages India-side obligations in parallel with your Singapore operations—covering ongoing ODI reporting, transfer pricing documentation between the two entities, and cross-border accounting support across both jurisdictions.

Post-Setup Obligations: Managing Compliance on Both Sides

Running a Singapore company from India creates a dual compliance burden that most Indian founders underestimate.

Singapore-Side Obligations

- Annual ACRA filings (annual returns, financial statements)

- IRAS corporate income tax returns

- GST returns (if registered)

- Maintenance of proper accounting records

India-Side Obligations

- Annual ODI reporting to the RBI (through the authorised dealer bank) by December 31 each year, based on audited financials of the Singapore entity

- FEMA compliance for any repatriation of profits

- Transfer pricing documentation for intra-group transactions

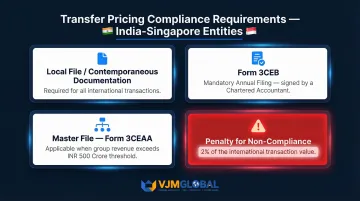

Transfer Pricing Compliance

Transfer pricing is a specific risk area when your Indian entity and Singapore entity transact with each other. Any intra-group transactions — services, IP licensing, management fees — must be at arm's length and documented for both Singapore's IRAS and India's income tax authorities.

Indian transfer pricing regulations set out clear documentation requirements:

- Local File (contemporaneous documentation): Required for all international transactions

- Form 3CEB: Mandatory annual filing with India's income tax return

- Master File (Form 3CEAA): Required when consolidated group revenue exceeds INR 500 crore and international transactions exceed INR 50 crore

- Penalty for non-compliance: 2% of the transaction value for failure to maintain required documents

Repatriation of Singapore Profits

Profit repatriation to India — whether as dividends or otherwise — must follow FEMA guidelines and be reported appropriately. The India-Singapore DTAA(12-aug-2011).pdf?sfvrsn=9f5e0a70_0) provides meaningful dividend withholding tax relief:

- Singapore does not impose withholding tax on dividends (Article 10(3))

- Indian withholding tax is capped at 10% if the Singapore beneficial owner holds at least 25% equity; otherwise 15%

Working with VJM Global: VJM Global handles DTAA advisory, transfer pricing documentation, and ongoing ODI reporting — keeping your cross-border structure compliant on both sides.

Frequently Asked Questions

Can a foreigner start a business in Singapore?

Yes, foreigners including Indian nationals can own 100% of a Singapore company. However, you must appoint at least one locally resident director and engage a registered filing agent to complete incorporation, as foreigners cannot self-register on BizFile+.

What is the minimum capital to start a company in Singapore?

The minimum paid-up capital is just S$1—there is no minimum capital requirement for most business types. However, Indian founders remitting funds from India must comply with FEMA/ODI rules regardless of the amount being transferred.

How much money do I need to start a business in Singapore?

Government fees total S$315 (S$15 name reservation + S$300 incorporation). Additional costs for nominee director, registered address, and corporate secretarial services mean all-inclusive incorporation packages from corporate service providers typically range from a few hundred to a few thousand SGD depending on inclusions.

What is the 60 day rule in Singapore?

The 60-day rule refers to the requirement that a company must have at least one director who is ordinarily resident in Singapore. For foreign-owned companies, this typically means appointing a nominee director or obtaining an appropriate work pass (EntrePass or Employment Pass) to fulfil this residency condition.

How do I start a small business in Singapore?

Incorporate as a Pte Ltd by reserving a name on BizFile+, appointing a resident director, and filing documents through a registered filing agent. Indian founders should complete FEMA/ODI compliance before remitting funds or opening a corporate bank account.

What business is booming in Singapore?

According to the EDB Annual Report 2023/24, priority sectors include advanced manufacturing, the digital economy (AI, data services), fintech, and the green economy. For Indian entrepreneurs, professional services and enterprise SaaS also offer strong entry points.

Ready to start your Singapore expansion? VJM Global's FEMA specialists and cross-border accounting experts handle everything from India-side ODI compliance to Singapore incorporation and ongoing dual-jurisdiction reporting. Contact us to discuss your specific requirements.