This creates a compliance burden that catches many NRIs off guard: you can simultaneously be a US tax resident (as a citizen, Green Card holder, or Substantial Presence Test qualifier) and an Indian non-resident, with active filing obligations in both countries.

This guide covers exactly what US-based NRIs need to know for AY 2026-27 — when Indian ITR filing is mandatory, what income is taxable, how to file from the US, and how the India-US DTAA and FBAR rules interact with your Indian compliance decisions.

Key Takeaways

- Indian ITR filing is mandatory if your total Indian income exceeds ₹2.5 lakh (old regime) or ₹4 lakh (new default regime) for AY 2026-27

- The standard filing deadline is July 31, 2026; belated returns are accepted until December 31, 2026 with a late fee

- NRE FD interest is tax-free in India but fully taxable in the US — a common source of underreporting for US-based NRIs

- The India-US DTAA prevents double taxation, but you must act: file Form 67 in India and Form 1116 in the US

- Most US-based NRIs should file using ITR-2; ITR-1 is not available to NRIs under any circumstances

Do US-Based NRIs Need to File Taxes in India?

Establishing NRI Status Under Indian Law

Under Section 6 of the Income Tax Act, you are a non-resident Indian for tax purposes if you were present in India for fewer than 182 days during the financial year (April 1 – March 31). A secondary test also applies: if you were present for 60 or more days in the current year and 365 or more days across the four preceding years, you may qualify as a resident.

The Finance Act 2020 added a further layer under Section 6(1A). If you are an Indian citizen earning more than ₹15 lakh from Indian sources and pay no tax in any other country by reason of domicile or residence, you are deemed a resident for tax purposes.

This rule applies from AY 2021-22 onward and catches US-based NRIs who earn India-sourced income but have no tax liability abroad — a group that often assumes non-resident status without verifying this provision.

When ITR Filing Is Mandatory

Filing is required if:

- Your total taxable Indian income exceeds ₹4 lakh under the new default regime, or ₹2.5 lakh under the old regime

- You have had aggregate deposits of over ₹1 crore in Indian current accounts during the year

- Foreign travel expenditure from India exceeded ₹2 lakh, or electricity expenditure exceeded ₹1 lakh

- TDS has been deducted on your Indian income and you want to claim a refund

When Filing Is Not Mandatory — But Still Smart

If your only Indian income is NRE or FCNR interest (both exempt under Indian law) and your total Indian income falls below the exemption threshold, strict filing is not required.

Voluntary filing still makes sense for several reasons:

- Builds an audit trail with Indian tax authorities

- Supports future property purchases or sales in India

- Preserves the ability to carry forward capital losses

Even if your income is fully exempt under the India-US DTAA, you may still need to file an ITR to formally claim those treaty benefits. Check the latest Income Tax Department guidance before assuming a zero-income year needs no filing.

What Income Is Taxable in India for US NRIs?

The Core Rule: Indian-Sourced Income Only

Under Section 5(2) of the Income Tax Act, NRIs are taxed only on income that accrues, arises, or is received in India. Your US salary, foreign investments, and income from American sources are entirely outside India's tax net.

Here's a quick breakdown:

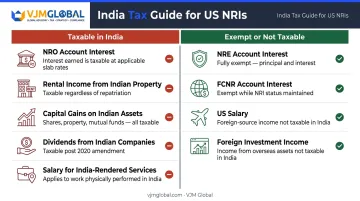

| Income Type | India Tax Status |

|---|---|

| NRO account interest | Taxable |

| Rental income from Indian property | Taxable |

| Capital gains on Indian assets | Taxable |

| Dividends from Indian companies | Taxable |

| Salary for services rendered in India | Taxable |

| NRE account interest | Exempt (Section 10(4)(ii)) |

| FCNR account interest | Exempt |

| US salary and foreign investment income | Not taxable in India |

AY 2026-27 Tax Slabs for NRIs

The new regime is now the default. NRIs do not receive age-based higher exemptions — the senior citizen slab benefits apply only to resident individuals.

New Default Regime:

| Income Slab | Rate |

|---|---|

| ₹0 – ₹4 lakh | Nil |

| ₹4 – ₹8 lakh | 5% |

| ₹8 – ₹12 lakh | 10% |

| ₹12 – ₹16 lakh | 15% |

| ₹16 – ₹20 lakh | 20% |

| ₹20 – ₹24 lakh | 25% |

| Above ₹24 lakh | 30% |

Old Regime: Nil up to ₹2.5 lakh; 5% from ₹2.5–5 lakh; 20% from ₹5–10 lakh; 30% above ₹10 lakh.

Which regime saves you more depends on the deductions you can claim — and the old regime offers several that the new one does not.

Deductions Under the Old Regime

- Up to ₹1.5 lakh for ELSS, life insurance premiums, and home loan principal (Section 80C)

- Health insurance premiums (Section 80D)

- Education loan interest (Section 80E)

- Qualifying charitable donations (Section 80G)

If you hold significant Indian investments, run the numbers under both regimes before filing — the difference can be substantial.

Capital Gains: Updated Rates for AY 2026-27

Following the Finance (No. 2) Act, 2024, capital gains rates changed substantially for transfers on or after July 23, 2024:

- LTCG on listed equity / equity mutual funds (Section 112A): 12.5% on gains above ₹1.25 lakh

- STCG on listed equity (Section 111A): 20%

- LTCG on immovable property: 12.5% without indexation

The 20%-with-indexation option for property transfers applies to resident individuals and HUFs — NRIs should confirm with a tax advisor whether they qualify before assuming eligibility.

TDS is deducted at source on property sales under Section 195. Claim that withheld amount as a Foreign Tax Credit on your US return.

How to File Your India Income Tax Return as a US NRI

NRIs can file their India ITR entirely online from the US via incometax.gov.in. No physical presence in India is required.

Documents to gather before you start:

- Active PAN (linked with Aadhaar where applicable)

- Passport (for residential status confirmation)

- Form 26AS and Annual Information Statement (AIS)

- Form 16A — TDS certificates from Indian banks and brokers

- NRO and NRE bank statements

- Capital gains statements from AMCs or brokers

- Tax Residency Certificate (TRC) from the US if claiming DTAA benefits

- Investment proofs for deductions (if opting for old regime)

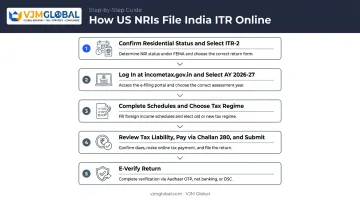

Step 1: Confirm Residential Status and Select Your Form

Count your days in India for the financial year and the preceding four years to confirm NRI status. Then choose your form:

- ITR-2 — For most US NRIs with salary, house property, capital gains, or other sources (no business income)

- ITR-3 — Required if you have Indian business or professional income

- ITR-1 — Not available to NRIs under any circumstances

Step 2: Log In and Set Up Your Filing

Register or log in at incometax.gov.in using your PAN as the User ID. Select AY 2026-27 (covering income earned April 2025 – March 2026). Cross-check pre-filled data against your Form 26AS and AIS before proceeding, since errors in pre-filled data are common and must be corrected before submission.

Step 3: Complete Schedules and Choose Your Regime

Fill in all applicable schedules in ITR-2:

- Schedule Salary — if applicable

- Schedule House Property — rental income

- Schedule Capital Gains — equity, mutual funds, property

- Schedule Other Sources — NRO interest, dividends

The portal selects the new regime by default. Switching to the old regime requires a manual selection inside the ITR form. If claiming DTAA credit for taxes paid in the US, file Form 67 before or alongside the ITR submission.

Step 4: Verify Tax Liability, Pay Dues, and Submit

Review the auto-computed tax liability in Part B-TTI. If additional tax is owed, pay via Challan 280 before submitting. Key deadlines for AY 2026-27:

- July 31, 2026 — Standard filing deadline

- October 31, 2026 — Extended deadline for NRIs with tax audit accounts

- December 31, 2026 — Belated return deadline, with a late fee of ₹5,000 (capped at ₹1,000 if total income does not exceed ₹5 lakh)

Step 5: E-Verify the Return

E-verification options for US-based NRIs include:

- Net banking EVC

- Demat account EVC

- Digital Signature Certificate (DSC)

If none of these options are available, print and sign the ITR-V and courier it via speed post to CPC Bengaluru within 30 days of filing.

Cases involving DTAA claims, capital gains across multiple asset classes, or NRO/NRE account reporting can get complex quickly. VJM Global's NRI tax filing team manages the end-to-end process remotely for US-based NRIs — from document collection to e-verification.

Key US-India Tax Complexities: DTAA, FBAR, and Double Taxation

How the India-US DTAA Works in Practice

The India-US Double Taxation Avoidance Agreement, signed in 1989 and in force since December 18, 1990, prevents the same income from being taxed twice — but only if you take the right steps.

Here's the practical flow:

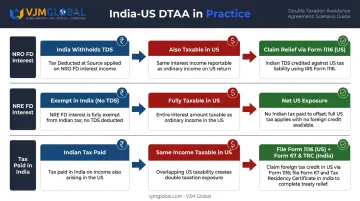

- NRO FD interest: India withholds TDS on this income. The same interest is also taxable in the US. You can claim the Indian tax withheld as a Foreign Tax Credit on US Form 1040 using Form 1116.

- NRE FD interest: Fully exempt in India (no tax collected). Fully taxable in the US as ordinary income. There is no Indian tax to offset against the US liability — making NRE FD income a net US tax exposure that many NRIs overlook.

- Indian taxes already paid: If you've paid Indian tax on income also taxable in the US, file Form 1116 (US) to claim credit. If you've paid US tax on income also taxable in India, file Form 67 in India along with a Tax Residency Certificate (TRC) from the US.

To claim DTAA benefits in India, you need your US TRC. Rates under the treaty vary by income type — consult a cross-border tax specialist rather than assuming a standard rate applies.

FBAR and FATCA: What US NRIs Must File

These are separate from your income tax return and non-compliance carries serious consequences:

- FBAR (FinCEN Form 114): Required if the aggregate balance of your foreign financial accounts (NRO, NRE, savings) exceeded USD 10,000 at any point during the calendar year. Filed electronically through FinCEN's BSA e-filing system, not with your tax return. Deadline is April 15 with an automatic extension to October 15.

- Form 8938 (FATCA): Required for unmarried US residents if foreign financial assets exceeded USD 50,000 on the last day of the tax year or USD 75,000 at any point during the year. Filed with your federal income tax return.

Indian banks report account data directly to the IRS under the India-US FATCA Intergovernmental Agreement (signed July 9, 2015). The IRS already receives your account information — gaps in your filings are detectable.

FBAR penalties matter. Following the Supreme Court's Bittner v. United States ruling (February 28, 2023), the non-willful FBAR penalty accrues per report (not per account). The inflation-adjusted maximum for a non-willful violation is currently USD 16,536 for 2025.

The PFIC Problem with Indian Mutual Funds

Beyond FBAR and FATCA, Indian mutual fund holdings introduce another layer of US tax complexity. The IRS may classify these funds as Passive Foreign Investment Companies (PFICs), which triggers consequences most NRI investors don't anticipate:

- Gains taxed as ordinary income under the default Section 1291 regime — not at lower capital gains rates

- Form 8621 required for each fund held, filed annually with your US return

- Interest charges applied retroactively on deferred income in certain election scenarios

This makes Indian mutual fund investing significantly more expensive and complex for US residents.

Whether any specific fund qualifies as a PFIC depends on the facts and circumstances. Before investing in Indian mutual funds as a US-based NRI, consult a cross-border tax specialist — the US tax cost may outweigh the Indian investment return.

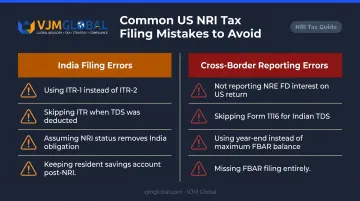

Common Mistakes US NRIs Make When Filing India Taxes

Filing Errors

- Assuming NRI status means no India filing obligation — not true if Indian income exceeds the exemption limit or specific transactions occurred

- Using ITR-1 — NRIs are categorically ineligible for ITR-1; ITR-2 is the correct form in most cases

- Not filing to claim a TDS refund — if TDS was deducted on NRO interest or capital gains, an ITR must be filed to recover it; there is no other route

- Continuing to operate a resident savings account after becoming an NRI — RBI guidance requires redesignating the account as NRO; failure to do so is a FEMA contravention under Section 13, subject to penalty

Cross-Border Reporting Errors

- Not reporting NRE FD interest on the US return — it is taxable in the US even though exempt in India

- Skipping Form 1116 — missing Foreign Tax Credit claims for Indian TDS paid on NRO income means paying tax twice unnecessarily

- Wrong FBAR balance methodology — FBAR requires the maximum balance during the year, not the year-end balance; using year-end figures can result in underreporting

- Missing FBAR entirely — many NRIs do not realize FBAR is a separate filing from their tax return

Deadline and Documentation Errors

These documentation gaps are where otherwise careful filers get tripped up at the finish line.

- Missing the July 31, 2026 deadline — belated filing attracts fees and interest charges

- No day-count log — the Income Tax Department can question NRI status; a record of India stays is essential if challenged

- Not obtaining Form 16A — TDS certificates from Indian banks must be collected before filing

Managing obligations across two tax systems is where errors compound quickly. VJM Global's Chartered Accountants have 30+ years of experience serving US-based Indian clients, covering NRI ITR filing, DTAA claims, capital gains schedules, and cross-border compliance coordination.

Frequently Asked Questions

Do NRIs need to file an income tax return in India?

Yes, if your total Indian income exceeds ₹2.5 lakh under the old regime or ₹4 lakh under the new default regime for AY 2026-27. Specific transactions — TDS deductions, capital gains, or high-value account deposits — can also trigger the obligation even below these thresholds. Filing voluntarily below the exemption limit is worth considering if you need to claim a TDS refund or maintain documentation for loans or visa applications.

Is income earned in India by an NRI taxable in the United States?

Yes. US citizens, Green Card holders, and tax residents must report worldwide income to the IRS — including rental income, NRO interest, and capital gains from Indian assets. NRE FD interest is also taxable in the US despite its India exemption. The India-US DTAA and Foreign Tax Credit (Form 1116) prevent double taxation where Indian tax was actually paid.

Which ITR form should a US-based NRI use?

Most US-based NRIs should file ITR-2, which covers income from salary, house property, capital gains, and other sources. ITR-3 applies if you have Indian business or professional income. ITR-1 is not available to NRIs under any circumstances.

What is the deadline to file India income tax returns for AY 2026-27?

The standard deadline is July 31, 2026 for NRIs without audit requirements. Belated returns can be filed until December 31, 2026 with a late fee. NRIs with accounts subject to tax audit have until October 31, 2026.

How does the India-US DTAA prevent double taxation?

The treaty lets you offset taxes paid in one country against your liability in the other — so the same income is taxed at the higher of the two rates, not both combined. In India, file Form 67 along with a US Tax Residency Certificate; in the US, file Form 1116 to claim the Foreign Tax Credit.

What happens if I don't file FBAR for my Indian accounts?

If your Indian accounts exceeded USD 10,000 in aggregate at any point during the year, FBAR filing is mandatory. Missing the deadline exposes you to non-willful penalties of up to USD 16,536 per report (2025 inflation-adjusted, per the Bittner ruling). Indian banks report account data to the IRS automatically under FATCA, so non-filing is readily detected.