Non-compliance isn't just a financial risk. It's a legal one — with consequences ranging from cascading penalties to business dissolution.

This guide is written for US-based businesses, foreign-owned US entities, NRIs and OCIs with US income, and international companies operating in the US. Whether you're filing for the first time or untangling years of missed obligations, what follows gives you a clear picture of what compliance requires and what's at stake when it lapses.

Key Takeaways

- US tax compliance covers federal, state, and local obligations — each with separate forms and deadlines

- Foreign-owned single-member LLCs must file Form 5472 even with zero income; failure carries a $25,000 minimum penalty

- Willful failure to file FATCA (Form 8938) or FBAR (FinCEN Form 114) can trigger criminal liability, not just financial penalties

- Extensions defer filing deadlines only — not payment deadlines

- The IRS now uses AI and data analytics to flag non-compliant returns — filing accurately the first time is no longer optional

What Is US Tax Compliance?

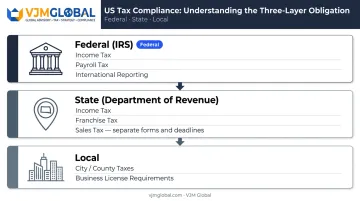

US tax compliance means accurately reporting income, expenses, and financial information to the IRS and relevant state authorities — and paying the correct amount of tax on time, under federal and state law.

There are three distinct layers:

- Federal (IRS): Governs income tax, payroll tax, and international reporting for all US entities and persons

- State (Department of Revenue): Each state maintains its own income tax, franchise tax, and sales tax rules — with separate filing requirements and deadlines

- Local: Some cities and counties impose additional taxes or business license requirements

Compliance goes beyond writing a check. It includes proper recordkeeping, timely submission of required forms, and responding accurately to IRS notices or compliance checks. Missing any one of these can trigger penalties, interest charges, or audit scrutiny — even when the underlying tax amount was paid in full.

Why US Tax Compliance Matters for Businesses

Legal Standing and Business Operations

Non-compliance carries real operational consequences. For US businesses — and especially foreign-owned entities — the risks extend well beyond a tax bill:

- Loss of good standing with the state, triggering potential dissolution

- Inability to renew licenses or bid on government contracts

- Damaged relationships with global partners when US filings are questioned

- Ripple effects on operations in other jurisdictions

Banks, investors, and potential partners frequently request a clean tax compliance report before extending credit or entering agreements. The IRS issues Letter 6201 (Tax Compliance Report for individuals and sole proprietors) and Letter 6574 (Business Tax Compliance Report for other entities) — documents that confirm a taxpayer is current with federal obligations.

The Financial Stakes

According to the IRS FY 2025 Data Book, the IRS assessed 54.2 million civil penalties totaling $1.247 trillion in a single fiscal year. The same data shows 214,099 federal tax liens and 339,137 levy requests issued during that period.

Penalties compound. A failure-to-file penalty adds 5% of unpaid tax per month (capped at 25%). Interest continues to accrue. What starts as a manageable oversight can become a serious financial liability within months.

AI-Driven Enforcement Is Growing

The IRS now deploys data analytics and AI to identify non-compliant returns. A TIGTA report from November 2024 confirmed the agency had 68 active AI-related projects, including models that flag irregular line items on individual returns and recommend audit issues. High-income filers and foreign-owned entities face the highest scrutiny.

With enforcement increasingly automated, the cost of a post-audit dispute — in time, fees, and penalties — almost always exceeds the cost of staying current year-round.

Key US Tax Compliance Requirements

Requirements vary by entity type and by whether the business is domestically or foreign-owned. Identifying which forms apply is the starting point.

Federal Income Tax Obligations

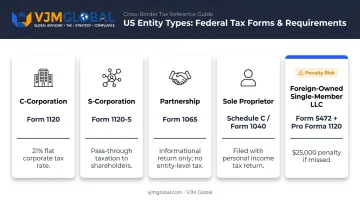

Every US entity must file an annual return with the IRS. The applicable form depends on entity structure:

| Entity Type | Required Form |

|---|---|

| C Corporation | Form 1120 |

| S Corporation | Form 1120-S |

| Partnership | Form 1065 (informational) |

| Sole Proprietor | Schedule C (Form 1040) |

| Foreign-owned single-member LLC | Form 5472 + Pro Forma 1120 |

Key distinctions to note:

- C-Corps pay a flat 21% corporate tax rate on taxable income

- Pass-through entities (LLCs, S-Corps, partnerships) report income on owners' personal returns

- Foreign-owned single-member LLCs must file Form 5472 even with zero income — failure to file carries a minimum $25,000 penalty per year

VJM Global's team of CPAs and Chartered Accountants prepares federal returns across these entity types, including Form 5472 and Pro Forma 1120 filings for foreign-owned structures.

Employment and Payroll Taxes

Businesses with employees must:

- Withhold federal income tax (based on employee's Form W-4)

- Withhold and deposit Social Security and Medicare taxes (FICA)

- Pay Federal Unemployment Tax (FUTA)

- File Form 941 (quarterly) or Form 944 (annual, for employers with $1,000 or less in annual employment tax liability)

- File Form 940 annually for FUTA

Estimated tax payments apply to sole proprietors, partners, and S-Corp shareholders expecting to owe $1,000 or more, and to corporations expecting to owe $500 or more. Missing these deadlines triggers underpayment penalties calculated at current IRS quarterly interest rates: 7% for standard underpayments as of Q3 2025.

State-Level and Sales Tax Obligations

Each state runs its own tax regime. Beyond income tax, businesses may face:

- Franchise taxes (for the privilege of operating in the state)

- Annual report requirements with filing fees

- Sales tax collection and remittance

Delaware is the most common state of incorporation for foreign companies. Delaware C-Corps must file their annual report and pay franchise tax by March 1. LLCs pay a flat $300 annual tax due by June 1.

Sales tax nexus is one of the most frequently overlooked obligations for growing businesses. Following the Supreme Court's ruling in South Dakota v. Wayfair (2018), physical presence is no longer required. A business selling into a state may trigger a filing obligation once it exceeds $100,000 in sales — and many states have since moved to dollar-only thresholds, dropping the 200-transaction test entirely. Tax Foundation data from 2024 shows more than 25 states now apply only dollar thresholds.

Note: Alaska, Delaware, Montana, New Hampshire, and Oregon have no statewide sales tax (though Alaska permits local sales taxes).

Multi-state nexus analysis requires tracking obligations across every state where a business has customers or activity. VJM Global helps businesses map that exposure early — before missed filings turn into penalties.

FATCA and International Reporting Obligations

The US taxes its citizens and permanent residents on worldwide income, regardless of where they live. For expats, NRIs with US status, and foreign-owned US entities, this means two overlapping reporting obligations on top of standard tax filing: FATCA and FBAR.

What Is FATCA and Who Must Report?

If you hold foreign financial assets — such as foreign bank accounts, securities, or interests in foreign entities — FATCA (Foreign Account Tax Compliance Act) requires you to report them to the IRS using Form 8938. Enacted in 2010, the law also obligates foreign financial institutions to report accounts held by US persons directly to the IRS.

Who must file Form 8938:

- US citizens living abroad

- Green Card holders with foreign accounts

- Domestic entities with foreign financial interests

- Certain foreign entities with US owners

Current IRS reporting thresholds (Form 8938):

| Filing Status | Living in the US | Living Abroad |

|---|---|---|

| Single / MFS | $50,000 (year-end) or $75,000 (any time) | $200,000 (year-end) or $300,000 (any time) |

| Married Filing Jointly | $100,000 (year-end) or $150,000 (any time) | $400,000 (year-end) or $600,000 (any time) |

Failure to file Form 8938 triggers a $10,000 penalty, with additional penalties up to $50,000 for continued non-compliance after IRS notice.

FBAR: Report of Foreign Bank Accounts

FATCA and FBAR are related but distinct obligations — and both can apply to the same accounts. US persons with a financial interest in, or signature authority over, foreign bank accounts must also file FinCEN Form 114 (FBAR). This requirement triggers if the aggregate value of all foreign accounts exceeded $10,000 at any point during the calendar year.

FBAR penalties are among the steepest in the tax code:

- Non-willful violations: Up to $16,536 per violation (inflation-adjusted as of January 2025)

- Willful violations: The greater of $165,353 or 50% of the account balance at the time of violation — plus potential criminal liability

Given the penalty exposure on both forms, many NRIs and cross-border entities work with a firm like VJM Global to ensure Form 8938 and FinCEN Form 114 are filed accurately and on time — particularly when accounts span multiple countries or ownership structures are complex.

US Tax Filing Deadlines and Key Dates

Federal Deadlines

| Entity / Filer | Standard Deadline | Extension Available |

|---|---|---|

| S-Corps, multi-member LLCs (partnerships) | March 15 | 6 months (Form 7004) |

| C-Corps, single-member LLCs, individuals | April 15 | 6 months |

| US taxpayers living abroad | June 15 (automatic) | Additional extension available |

Critical rule: Extensions apply to the filing deadline only — not the payment deadline. Tax owed by April 15 is still due April 15, even if you file in October. The IRS charges interest and failure-to-pay penalties on any unpaid balance from the original due date.

Federal deadlines are only part of the picture. Each state runs its own filing calendar — and the rules vary significantly.

State-Level Variations

Using Delaware as an example:

- C-Corp franchise tax and annual report: Due March 1

- LLC annual tax ($300): Due June 1

Every state sets its own rules, and nexus triggers — including economic nexus thresholds like $100,000 in annual sales or 200 transactions — can create filing obligations even without a physical office. Foreign-owned businesses must track requirements in every state where they have nexus or are registered.

Why a Compliance Calendar Matters

Missing one deadline can trigger cascading penalties — a late state filing, for instance, may void good standing and block banking or contract renewals. For businesses with multi-state or international operations, a structured annual compliance calendar should map every federal, state, and international filing date alongside its corresponding payment deadline. That distinction alone — filing vs. payment — prevents the most common and costly errors.

Common Penalties for US Tax Non-Compliance

Standard IRS Penalties

| Penalty Type | Rate |

|---|---|

| Failure to file | 5% of unpaid tax per month, capped at 25% |

| Failure to pay | 0.5% of unpaid tax per month, capped at 25% |

| Accuracy-related | 20% of the underpayment attributable to negligence or substantial understatement |

These can stack. A return filed late with unpaid tax accrues both failure-to-file and failure-to-pay penalties simultaneously, while interest compounds on the underlying balance.

International Reporting Penalties

These are in a different category entirely:

- Form 5472: $25,000 minimum per missed filing

- Form 8938 (FATCA): $10,000 initial penalty; up to $50,000 for continued non-compliance

- FBAR (willful): Greater of $165,353 or 50% of account balance per violation, plus potential criminal prosecution

The consequences don't stop at the penalties listed above. Non-compliance can also trigger IRS audits, state-level investigations, loss of good standing, and business dissolution. TIGTA's 2024 review of IRS technology projects confirmed that AI-driven enforcement now increasingly targets high-income earners and foreign-owned entities — making exposure harder to avoid.

For businesses managing cross-border US tax obligations, early expert involvement prevents these penalties from compounding. VJM Global has served 500+ American business owners, with a dedicated team of CPAs and US-compliant professionals handling everything from FBAR filings to FATCA reporting and annual tax returns.

Frequently Asked Questions

What is US tax reporting?

US tax reporting is the mandatory disclosure of income, expenses, and financial data to the IRS and relevant state authorities through prescribed forms. It applies to individuals, businesses, and foreign-owned entities, and is used to determine tax liability and confirm compliance with federal and state laws.

Who needs to do FATCA reporting?

FATCA reporting is required of US citizens, Green Card holders, and certain US entities with specified foreign financial assets above IRS thresholds. Foreign financial institutions that hold accounts belonging to US persons are also required to report under FATCA.

What happens if I don't file FATCA?

Failure to file Form 8938 results in a $10,000 civil penalty, with additional penalties up to $50,000 for continued non-compliance after IRS notice. Willful failure to report foreign assets may also carry criminal liability.

What forms do US businesses need to file annually?

Required forms depend on your entity type:

- C-Corporations: Form 1120

- Partnerships: Form 1065

- S-Corporations: Form 1120-S

- Sole Proprietors: Schedule C of Form 1040

- Foreign-owned single-member LLCs: Form 5472 + Pro Forma 1120

State-level filings vary by state of incorporation.

Do foreign-owned US companies need to file taxes even with no income?

Yes. All 100% foreign-owned single-member LLCs must file Form 5472 and a Pro Forma 1120 annually regardless of income or activity. Failure to do so results in a minimum $25,000 penalty per year.

What is the penalty for missing a US tax filing deadline?

Failure-to-file penalties run 5% of unpaid tax per month (capped at 25%), failure-to-pay penalties run 0.5% per month (capped at 25%), and accuracy-related penalties can add 20% of any underpayment. Your total exposure depends on entity type, filing history, and outstanding balance.