Introduction

Nearly 6,000 US companies currently operate in Singapore, according to the Singapore Economic Development Board — and that number keeps growing. Still, many US businesses struggle to navigate an unfamiliar legal landscape when expanding into Asia: which entity type to choose, what compliance looks like, and how the structure maps to what they already know back home.

The draw is straightforward: a stable regulatory environment, a 17% corporate tax rate, and direct access to Southeast Asia's market of over 684 million people make Singapore one of the most practical bases for US companies expanding into the region.

For most US businesses, the vehicle of choice is the Singapore Private Limited Company (Pte. Ltd.). It's the most common and flexible structure available, and the entire registration process can be handled online without setting foot in Singapore.

This guide covers what US companies need to know: how the Pte. Ltd. compares to familiar US structures, why Singapore works as an expansion base, what setup actually requires, and what ongoing tax and compliance obligations to expect.

Key Takeaways

- US citizens and companies can own 100% of a Singapore Pte. Ltd., but at least one locally resident director is required by law

- The Pte. Ltd. is Singapore's closest equivalent to a US LLC or C-Corporation — with limited liability and separate legal entity status

- Singapore's corporate tax rate is 17%, with no capital gains tax or withholding tax on dividends to foreign shareholders

- The US and Singapore have no comprehensive double taxation treaty, making cross-border tax planning an area that warrants professional guidance

- Incorporation is handled entirely online through ACRA's BizFile+ portal via an appointed Corporate Service Provider

What Is a Singapore Private Limited Company (Pte. Ltd.)?

Under the Companies Act 1967, a Singapore Pte. Ltd. is a separate legal entity — distinct from its shareholders, capable of entering contracts, owning assets, and incurring liabilities independently. Shareholders' personal assets are protected; liability is capped at their investment in the company.

Key structural characteristics include:

- Maximum of 50 shareholders (Section 18 of the Companies Act)

- Perpetual succession — the company continues operating regardless of ownership changes

- Ability to issue shares and raise equity capital

- Corporate income taxed at the company level at a flat 17% rate

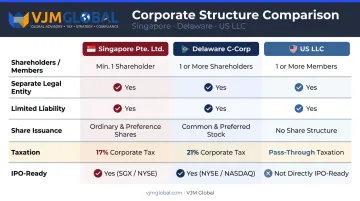

Pte. Ltd. vs US Corporate Structures

US founders often ask which American structure the Pte. Ltd. most closely resembles. It sits somewhere between a Delaware C-Corp and an LLC.

| Feature | Singapore Pte. Ltd. | Delaware C-Corp | US LLC |

|---|---|---|---|

| Shareholders/Members | Up to 50 | Unlimited | Typically unlimited |

| Separate legal entity | Yes | Yes | Yes |

| Limited liability | Yes | Yes | Yes |

| Share issuance | Yes | Yes | No (membership interests) |

| Taxation | Corporate level (17%) | Corporate level (21%) | Pass-through (default) |

| IPO-ready | No (private) | Yes | No |

The critical distinction for US owners: a Singapore Pte. Ltd. is taxed at the corporate level, not as a pass-through entity. Unlike a US LLC where profits flow directly to members' personal returns, Singapore taxes the company first at 17%, then shareholders receive dividends — which carry no withholding tax in Singapore.

Standalone vs. Subsidiary Structure

That tax structure shapes how the entity fits into your broader corporate setup. US companies entering Singapore typically choose between two approaches:

- Standalone Pte. Ltd. — A new, independent Singapore entity with no formal parent-subsidiary relationship

- Wholly-owned subsidiary — The US parent company owns 100% of the Singapore Pte. Ltd.'s shares

For existing US businesses, the subsidiary structure is generally recommended. It insulates parent company assets from Singapore-side liabilities. It also makes your corporate structure transparent to investors, banks, and regulators — which matters when you scale.

Why US Companies Choose Singapore for Business Expansion

Singapore's appeal goes well beyond tax rates. Several structural factors make it a practical operating base, not just a tax-efficient address.

Market Access and the USSFTA

Singapore sits at the center of ASEAN, a regional bloc with a 2024 population of 684 million people across 10 member states. The US-Singapore Free Trade Agreement, in force since January 1, 2004, provides US companies with expanded market access, enhanced IP protections, and investment guarantees that most other Asian jurisdictions don't offer.

The US is also Singapore's largest foreign direct investment partner, with US companies committing S$6.6 billion in fixed asset investments in 2023 alone — nearly half of Singapore's total FAI commitments that year.

Tax and Regulatory Environment

Singapore's tax regime offers several concrete advantages:

- 17% flat corporate tax rate (versus 21% US federal rate, plus state taxes)

- No capital gains tax — gains on asset disposals are generally not taxable

- No withholding tax on dividends paid to foreign shareholders

- Startup tax exemption: new qualifying companies receive 75% exemption on the first SGD 100,000 of chargeable income, and 50% on the next SGD 100,000, for each of the first three consecutive Years of Assessment

- Territorial tax system — Singapore generally taxes only Singapore-sourced income, a significant contrast to the US worldwide taxation system

The World Bank's Business Ready 2025 report ranks Singapore as the leading economy globally in Operational Efficiency, placing it in the top quintile across all three assessment pillars.

Financial Infrastructure and Legal Framework

Singapore ranks 4th globally in the Global Financial Centres Index 38 (September 2025), with a rating of 763. US companies can access multi-currency accounts, trade financing, and international payment rails with minimal setup friction.

On the legal side, Singapore's system is rooted in English common law. Key practical features include:

- Strong IP protections enforceable through an independent judiciary

- Singapore International Arbitration Centre (SIAC) for internationally recognized commercial dispute resolution

- Contract enforceability that holds up across borders — relevant when protecting business assets in cross-border deals

Key Requirements for US Companies Setting Up a Singapore Pte. Ltd.

Getting incorporated is the easy part. Understanding the ongoing obligations from day one prevents problems later.

Locally Resident Director

Section 145 of the Companies Act requires every Singapore company to have at least one director who ordinarily resides in Singapore — meaning a Singapore citizen, permanent resident, or holder of a valid Employment Pass, EntrePass, or Dependant Pass.

US-based founders without a Singapore presence must engage a professional nominee director service to satisfy this requirement. This is a standard, widely-used arrangement — not a workaround.

Registered Office Address

Under Section 142 of the Companies Act, the company must maintain a registered office in Singapore that is open and accessible to the public for at least three hours during ordinary business hours on each business day. Virtual office and professional registered address services satisfy this requirement.

Share Capital and Ownership

- Minimum share capital: SGD 1

- US individuals and corporate entities (such as a US parent company) can hold 100% of shares as the ultimate beneficial owner

- No restrictions on profit repatriation

Company Secretary

A qualified Singapore-resident company secretary must be appointed within six months of incorporation. Under Section 171(1E) of the Companies Act, the sole director cannot also serve as company secretary — these must be separate individuals.

Data Protection Officer (DPO)

Appointing a DPO is mandatory under Singapore's Personal Data Protection Act (PDPA). From December 1, 2024, DPO registration moved from ACRA's BizFile+ to PDPC's online form.

US companies collecting customer data in Singapore must designate a DPO and make their contact information publicly available. Most US companies handle this through a local compliance professional or their corporate services provider — similar to the nominee director arrangement.

How to Register a Singapore Pte. Ltd. from the USA

The entire registration process runs online — no travel to Singapore required. That said, some banks may require an in-person visit or video call for business account opening, so factor that into your timeline.

Step 1 — Engage a Corporate Service Provider (CSP)

ACRA requires foreigners, including US companies, to engage an ACRA-registered Corporate Service Provider to submit applications through BizFile+. The CSP handles the KYC onboarding process and document preparation. You'll typically need:

- Passport copies for all directors and shareholders

- Proof of residential address

- Proposed company name

- Preferred financial year-end

Step 2 — Name Reservation and Document Submission

The CSP submits a name application through BizFile+ (SGD 15 fee; reservation valid for up to 120 days). Core documents required include:

- Directors' and shareholders' details

- Registered office address

- Company constitution

- Company secretary details

Government registration fee: SGD 300.

Step 3 — Receive Incorporation Certificate and UEN

Once approved, ACRA issues an e-Certificate of Incorporation and a Unique Entity Number (UEN), which appears on all commercial correspondence with customers, partners, and government agencies. Most applications process within 1–3 business days of payment. Complex cases, or those requiring referral authority approval, can extend to 15 working days or more.

Tax and US Reporting Considerations

Singapore's tax advantages are genuine — but US ownership of a Pte. Ltd. creates a parallel set of domestic reporting obligations that run regardless of where profits are earned.

No Comprehensive US-Singapore Tax Treaty

IRAS's list of tax agreements does not include the United States as a comprehensive Double Taxation Agreement (DTA) jurisdiction. This means some transactions may face taxation in both countries. A Tax Information Exchange Agreement (TIEA) between the US and Singapore entered into force on March 5, 2020, allowing information sharing between tax authorities. This is not a DTA and does not provide the same double-taxation relief.

Professional tax advice is essential before structuring your Singapore entity.

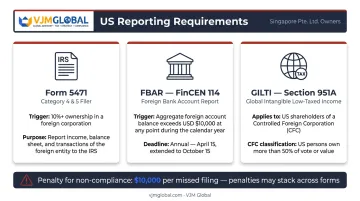

US Federal Reporting Obligations

US persons (citizens, green card holders, and corporate entities) who own a Singapore Pte. Ltd. may face the following US reporting requirements:

- Form 5471 — Required for US persons who own 10% or more of a foreign corporation's total value or voting power

- FBAR (FinCEN 114) — Required if aggregate foreign bank account balances exceed USD $10,000 at any point during the calendar year

- GILTI (Global Intangible Low-Taxed Income, Section 951A) — Applies to US shareholders of Controlled Foreign Corporations; CFC status determines whether this applies, so classification matters before assuming exposure

These obligations exist regardless of where profits are earned. Non-compliance can trigger penalties starting at $10,000 per missed filing, with criminal exposure for willful violations.

Ongoing Compliance Obligations for a Singapore Pte. Ltd.

Once incorporated, the company has recurring compliance deadlines. Missing them carries fines.

Key annual requirements:

- Annual General Meeting — Must be held within six months after financial year-end (private companies may be exempt if they send financial statements to all members within five months and meet other qualifying conditions)

- Annual Returns — Filed with ACRA within seven months after financial year-end

- Corporate Income Tax Return — Filed with IRAS annually (YA 2026 deadline: November 30, 2026)

- Statutory registers — Directors, shareholders, and controllers must be kept updated

- GST registration — Mandatory once annual taxable turnover exceeds SGD 1 million (either retrospectively at calendar year-end or prospectively when future turnover is expected to exceed that threshold)

Managing these deadlines from the US across a different time zone and regulatory system adds real operational complexity. Most US-based operators engage a local Singapore corporate secretarial firm for ACRA filings and on-the-ground compliance, while partnering with a cross-border advisor to keep their US and Singapore reporting aligned. VJM Global works with US companies navigating multi-jurisdiction obligations — particularly where India operations intersect with Singapore holding structures — helping ensure financial reporting and tax filings remain coordinated across entities.

Frequently Asked Questions

Can a US citizen open a private limited company in Singapore?

Yes. US citizens can fully own 100% of a Singapore Pte. Ltd. as the ultimate beneficial owner. The company must appoint at least one locally resident director, which US-based founders can fulfil through a professional nominee director service.

What is the US equivalent of a private limited company in Singapore?

The Singapore Pte. Ltd. is most comparable to a US LLC (for limited liability and operational flexibility) or a Delaware C-Corporation (for share issuance and investor-readiness). Unlike a US LLC, the Pte. Ltd. is taxed at the corporate level rather than as a pass-through entity.

Do I need to travel to Singapore to register a Pte. Ltd.?

Physical presence in Singapore is not required for company registration. The entire incorporation process is handled online through BizFile+ via an ACRA-registered Corporate Service Provider. Some banks, however, may require a visit or video call for corporate bank account opening.

Do I need a local director as a US company setting up in Singapore?

Yes. Singapore law requires at least one director who ordinarily resides in Singapore. US companies without a Singapore-based employee can engage a professional nominee director service through a registered corporate service provider to meet this requirement.

What are the tax implications for US companies owning a Singapore Pte. Ltd.?

Singapore taxes profits at a flat 17% corporate rate on Singapore-sourced income. US shareholders also carry federal reporting and tax obligations — including Form 5471 and GILTI provisions. Note that no comprehensive US-Singapore double tax treaty exists, so cross-border tax advice is strongly recommended.

How long does it take to register a Singapore Pte. Ltd. from the USA?

Most straightforward applications are approved soon after submission through a registered Corporate Service Provider. Complex or referred cases may take up to 15 working days. Including document preparation, the full process typically runs two to four weeks.