Introduction

For UK companies expanding into Asia, Singapore is the default first move — but the setup process is more involved than most founders expect. Singapore drew US$143 billion in FDI in 2024, a 6% year-on-year increase, and a Private Limited Company (Pte Ltd) remains the structure international businesses consistently choose as their regional base.

The challenges UK founders run into aren't always obvious upfront. You cannot register directly — a licensed Corporate Service Provider must file on your behalf. A locally resident director is mandatory. Before your company trades, HMRC's Controlled Foreign Company rules also require serious attention.

This guide covers every stage: legal requirements, the step-by-step registration process, realistic costs, ongoing compliance, and the UK-specific tax considerations that matter most.

Key Takeaways

- A Singapore Pte Ltd can be 100% UK-owned, but requires at least one locally resident director and a Singapore-resident company secretary

- UK companies must appoint a licensed Corporate Service Provider (CSP) — direct registration through ACRA is not permitted for foreign applicants

- Government fees total SGD 315, but first-year professional service costs typically run SGD 2,000–5,000+

- HMRC's Controlled Foreign Company rules may still apply to UK shareholders, so seek UK tax advice before trading begins

- Ongoing compliance covers ACRA annual returns, IRAS tax filings, and GST registration if turnover exceeds SGD 1 million

Why UK Companies Should Set Up a Singapore Private Limited Company

The Pte Ltd Structure Explained

A Singapore Pte Ltd is a separate legal entity incorporated under the Singapore Companies Act. It can hold assets, enter contracts, and employ staff independently of its UK parent. Shareholders benefit from limited liability, and the structure supports up to 50 shareholders — including a UK parent company as the sole corporate shareholder.

That legal separation is what makes the Pte Ltd the default choice — it means Singapore liabilities stay in Singapore, and UK parent exposure is capped at the shareholding. Neither alternative provides the same protection:

- Branch office — tied to the UK parent's legal liability; all obligations flow upward

- Representative office — restricted to non-trading market research activities only

The Commercial Case for Singapore

The numbers make a strong argument:

- 17% corporate tax rate — flat rate applicable to both local and foreign companies, confirmed by IRAS

- Start-Up Tax Exemption — 75% exemption on the first SGD 100,000 of chargeable income for the first three consecutive years of assessment

- UK-Singapore trade — total trade in goods and services reached GBP 28.3 billion in the four quarters to Q4 2025; the UK-Singapore Free Trade Agreement (in force since 11 February 2021) supports preferential market access in both directions

- Regional connectivity — Singapore connects to nearly 160 cities via 100 airlines, giving UK companies direct access to ASEAN's 680 million-person consumer market

Singapore also ranked 1st in the 2026 IMD World Competitiveness Ranking, reflecting its stable regulatory environment and openness to foreign investment.

Key Requirements for UK Companies Setting Up a Pte Ltd

Mandatory Use of a Corporate Service Provider

ACRA requires all foreigners and foreign businesses to engage a licensed Corporate Service Provider to reserve a company name and submit the incorporation application. This is a legal requirement, not an optional convenience, and applies to all UK nationals and UK corporate shareholders.

Your CSP will handle the BizFile+ submission, guide document preparation, and ensure officer endorsements are completed correctly.

Local Resident Director

Every Singapore Pte Ltd must have at least one director who is ordinarily resident in Singapore. ACRA defines this as:

- A Singapore citizen

- A Singapore permanent resident

- A valid Employment Pass, Personalised Employment Pass, or Overseas Networks & Expertise Pass holder

UK founders who are not relocating to Singapore cannot personally fulfil this role. The standard arrangement is a professional nominee director: an individual who holds the statutory director position on your behalf. Nominee directors carry genuine legal duties under Singapore law, so the authority they exercise and the limits on that authority must be clearly documented from the outset.

Company Secretary

A qualified company secretary must be appointed within six months of incorporation. Key rules:

- Must be a natural person resident in Singapore

- Cannot be the same individual as the sole director

- Cannot be a corporate entity

This differs from UK practice, where a company secretary is optional for most private companies.

Registered Office Address

The company must maintain a Singapore registered office address, accessible to the public during normal business hours. Address changes must be reported to ACRA within 14 days. Failing to maintain a properly accessible office can attract a fine of up to SGD 5,000. Registered address services are available through most CSPs.

Remaining Structural Requirements

| Requirement | Minimum / Rule |

|---|---|

| Paid-up share capital | SGD 1 minimum (one share minimum) |

| Shareholders | At least one (UK parent company can be sole shareholder) |

| Company name | Must meet ACRA naming rules; cannot duplicate existing entities |

| Financial year end | Must be defined at incorporation for reporting and tax purposes |

In practice, higher paid-up capital strengthens bank account applications and improves credibility with Singapore counterparties. SGD 1 satisfies the legal minimum, but most CSPs recommend starting with a more substantial amount if you plan to open a corporate bank account early.

Step-by-Step: How to Register a Singapore Pte Ltd from the UK

The entire registration process can be managed remotely through your CSP. Before you begin, prepare: passport copies for all directors and shareholders, UK company documents if the parent is a shareholder, and source-of-funds information.

Step 1: Reserve the Company Name

Your CSP submits the proposed name through ACRA's BizFile+ portal. Once approved, the name is reserved for 120 days — sufficient time to complete preparation and file.

ACRA will reject names that are identical to existing entities, considered undesirable, or that resemble government bodies. If your UK brand name is already in use in Singapore, you will need an alternative. Check Singapore trademark records separately before submitting.

Step 2: Prepare Required Documents

Documents needed include:

- Passport copies for all directors and shareholders

- Company constitution (ACRA provides a standard template)

- Singapore registered office address

- Company secretary's details and consent

- SSIC code identifying your primary business activity

- If a UK company is a shareholder: certified corporate documents, certificate of incorporation, and ownership evidence

Keep your source-of-funds narrative and business profile ready at this stage — banks require these independently of ACRA, and having them prepared now avoids delays later.

Step 3: Submit via ACRA BizFile+

Your CSP submits the application electronically through BizFile+ — the only permitted channel. When a CSP files on your behalf, officer endorsement is handled as part of that process. For self-filed applications, all appointed officers must endorse their positions within 60 days of submission.

Submit accurate, complete information. If ACRA refers a name to another authority for review, that process alone can add up to 60 days — separate from any delays caused by incomplete filings.

Step 4: Receive Certificate of Incorporation and UEN

Most registrations are approved shortly after payment, though complex cases can take up to 15 working days. Upon approval, ACRA issues:

- A notice of successful incorporation

- A Unique Entity Number (UEN) — required on all invoices, contracts, and official correspondence

From this point, your Singapore Pte Ltd can sign contracts, open bank accounts, and begin trading.

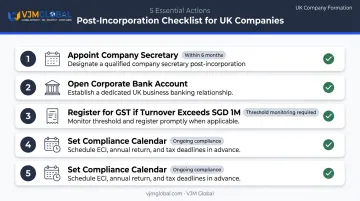

Step 5: Complete Post-Incorporation Actions

Immediately after incorporation:

- Appoint your company secretary within six months of incorporation

- Open a Singapore corporate bank account — prepare a business plan, director identification, and source-of-funds documentation; the relationship manager engagement process typically takes several weeks

- Register for GST if projected annual turnover will exceed SGD 1 million

- Set your compliance calendar covering ECI filing, annual return, and tax return deadlines from your first financial year end

Costs and Timeframe

Government Fees

| Item | Fee |

|---|---|

| Name application | SGD 15 |

| Company registration | SGD 300 |

| Annual return filing | SGD 60 (per year) |

| Total setup (government only) | SGD 315 |

Always verify current fees directly with ACRA's fee schedule.

Professional Services Costs

Government fees represent only a fraction of your first-year outlay. Based on published market rates from Singapore CSPs:

| Service | Typical Annual Range |

|---|---|

| Nominee director | SGD 1,500 – SGD 5,000 |

| Company secretary | SGD 300 – SGD 1,500 |

| Registered address | SGD 200 – SGD 500 |

| CSP incorporation service | SGD 600 – SGD 2,000 (one-off) |

Your actual cost depends on service scope, risk profile, and provider. Request an itemised quote covering all first-year costs before committing.

Realistic Timeline

Budget for both money and time before committing — the two tend to track together for foreign-owned companies.

- Name reservation to ACRA approval: typically a few working days for straightforward applications; up to 15 working days for complex cases

- Document preparation: 1–2 weeks for most UK applicants, longer if corporate shareholder documents require notarisation

- Bank account opening: several weeks — foreign-owned companies typically work through a relationship manager process

- Full operational readiness: allow 3–5 weeks from name reservation to having an active bank account

Post-Registration Compliance and UK-Specific Tax Considerations

ACRA Annual Compliance

Key ongoing obligations with ACRA:

- Annual return: must be filed within 7 months of the financial year end for non-listed companies

- Statutory registers: must be kept updated via BizFile+; changes to officers, shareholders, and registered address require prompt notification

- Financial statements: must comply with Singapore Financial Reporting Standards (SFRS) — not UK GAAP or IFRS as adopted in the UK

- XBRL filing: most Singapore companies must file financial statements in XBRL format with ACRA; smaller companies may qualify for simplified XBRL plus PDF submission

IRAS Tax Obligations

- Estimated Chargeable Income (ECI): must be filed within 3 months of the financial year end (subject to waiver conditions)

- Corporate tax rate: 17% flat rate on chargeable income

- Start-Up Tax Exemption (SUTE): for the first three consecutive Years of Assessment, 75% exemption on the first SGD 100,000 of normal chargeable income and 50% on the next SGD 100,000 — maximum exemption SGD 125,000 per year. Verify current thresholds with IRAS

- GST registration: mandatory if annual taxable turnover exceeds SGD 1 million

UK CFC Rules — The Issue Most UK Founders Miss

Under HMRC's Controlled Foreign Company framework, UK resident shareholders controlling a Singapore company may face UK tax on undistributed profits if applicable CFC exemptions do not apply. The regime (Part 9A TIOPA 2010) applies to CFC accounting periods starting on or after 1 January 2013.

Five entity-level exemptions exist. The most commonly relevant is the Low Profits Exemption, which applies where accounting profits are £500,000 or less and non-trading income does not exceed £50,000. Whether any exemption applies depends entirely on the specific facts of your structure.

Take UK tax advice before your Singapore company begins trading. CFC exposure can create unexpected UK tax costs that wipe out Singapore's tax efficiency — often before founders realise the liability exists.

UK-Singapore Double Taxation Agreement

The UK-Singapore DTA, in force since 19 December 1997 and modified by the Multilateral Instrument from 1 January 2020, can provide relief on dividends, interest, and royalties flowing between the two countries. Treaty benefits are not automatic, however. They depend on:

- Where the company's management and control sits

- Whether the Singapore entity has genuine business substance

- How the MLI's Principal Purposes Test is applied to the structure

That last point connects directly to how IRAS determines Singapore tax residence — based on where control and management are exercised, typically where the board makes strategic decisions. A Singapore company that takes instructions exclusively from UK-based directors may not qualify as Singapore tax resident with IRAS, undermining both the DTA position and the corporate tax benefits.

Common Mistakes UK Companies Should Avoid

Three Structural Mistakes

1. Treating the nominee director role as a formality Singapore directors carry genuine legal duties under the Companies Act. Without clearly documented authority limits and controls, both you and your nominee director face legal exposure. Get this in writing before incorporation.

2. Forming the company before the banking strategy is clear Singapore banks apply thorough due diligence to foreign-owned entities. A company with no transaction history, no Singapore-based staff, and an unclear business profile faces significant delays. Some UK-owned companies wait months for account approval. Plan your banking approach before you file.

3. Assuming a Singapore company removes UK tax exposure CFC rules, transfer pricing requirements, and DTA residency tests all operate independently of the Singapore registration. The UK tax position requires a separate analysis.

The Substance Requirement

Singapore's tax benefits, DTA protections, and banking access all work best when the Singapore entity has real economic activity. Companies established primarily as offshore holding structures (without genuine management, staffing, or operational presence in Singapore) face challenges from both IRAS on tax residency and HMRC on CFC exemptions and DTA claims.

Substance is built through:

- Management and control decisions made in Singapore

- Locally based employees

- Genuine operational activity on the ground

UK vs Singapore Corporate Governance Differences

UK founders frequently underestimate these differences:

- Company secretary is legally required in Singapore — not optional as in most UK private companies

- Financial statements must follow SFRS, not UK GAAP

- XBRL filing is required for ACRA annual submissions

- AGM obligations differ from UK requirements

For UK-owned Singapore companies managing cross-border accounting, ACRA compliance, and IRAS tax filings simultaneously, specialist support matters. VJM Global has worked with 250+ UK businesses across international markets and can close compliance gaps before they compound.

Frequently Asked Questions

Can a foreigner set up a private limited company in Singapore?

Yes. UK nationals and UK corporate entities can own 100% of a Singapore Pte Ltd. Foreigners must engage a licensed Corporate Service Provider to handle registration and must meet the local resident director and company secretary requirements.

How much does it cost to set up a private limited company in Singapore?

Government fees total SGD 315 (SGD 15 name reservation plus SGD 300 registration). Total first-year costs — including a nominee director, company secretary, registered address, and CSP incorporation fee — are considerably higher. Request an itemised quote from your service provider before committing.

What is the minimum paid-up capital for a private limited company in Singapore?

The legal minimum is SGD 1 per ACRA requirements. Higher paid-up capital can improve the company's credibility when opening a corporate bank account or bidding for contracts with Singapore counterparties.

Does a UK company need a local resident director to register a Pte Ltd in Singapore?

Yes. Every Singapore Pte Ltd must have at least one director who is ordinarily resident in Singapore. UK founders not relocating must appoint a Singapore-resident individual or engage a professional nominee director service.

How long does it take to set up a private limited company in Singapore from the UK?

ACRA registration typically completes within a few working days for straightforward applications. The full process from document preparation to an operational bank account generally takes 3–5 weeks for UK applicants. Banking is typically the longest step.

Do I need to travel to Singapore to register a private limited company?

In most cases, no — registration can be completed remotely through a licensed CSP. However, some banks may require in-person attendance for account opening. If you plan to relocate and manage the business from Singapore, you will need to obtain a valid work pass before relocating.