According to Companies House statistics for FY2025, private limited companies account for over 92% of all registered corporate bodies in the UK — more than 5.2 million entities. That dominance isn't accidental.

This guide covers everything you need to know: what a private limited company actually is, how it works, the real advantages and drawbacks, what you owe HMRC and Companies House, and how to get one registered.

Key Takeaways

- A private limited company is a legally separate entity from its owners, protecting personal assets from business debts

- Shareholders' liability is capped at the unpaid value of their shares — often just £1

- Directors can draw earnings via salary and dividends, with profits subject to corporation tax

- Annual accounts, a confirmation statement, and a corporation tax return are mandatory each year

- Non-UK residents can form and own a UK private limited company, with a UK registered office address as the only location requirement

What Is a Private Limited Company in the UK?

A private limited company is a legally incorporated business entity (registered with Companies House) that exists as a distinct legal "person," entirely separate from the individuals who own or run it. The company itself owns assets, enters contracts, opens bank accounts, and bears responsibility for its own debts.

The word "private" has a specific meaning here: shares in the company are not listed or traded on a public stock exchange. Ownership stays within a defined group — typically founders, family members, or private investors.

Once Companies House approves a registration, it issues a Certificate of Incorporation confirming the company's registered number and formation date — and trading can begin immediately.

How does this differ from other structures?

- A sole trader has no legal separation between the person and the business — they are one and the same

- A public limited company (PLC) can offer shares to the general public; a private limited company cannot

- A partnership distributes liability across partners personally, with no separate corporate entity

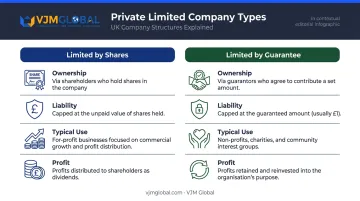

Companies Limited by Shares vs. Companies Limited by Guarantee

There are two types of private limited company, and the difference matters:

| Type | Ownership | Liability | Typical Use |

|---|---|---|---|

| Limited by shares | Shareholders holding defined shares | Capped at unpaid share value | For-profit businesses |

| Limited by guarantee | Guarantors pledging a fixed amount (usually £1) | Capped at guaranteed amount | Non-profits, charities, community groups |

Most commercial businesses incorporate as companies limited by shares. If you're setting up a business to generate and distribute profit, this is the structure you want. Companies limited by guarantee are designed to reinvest any surplus rather than pay it out to owners — if you're unsure which applies, the company's purpose (profit distribution vs. mission-driven reinvestment) is the deciding factor.

Key Characteristics of a UK Private Limited Company

A private limited company has what lawyers call separate legal personality — it can own property, employ people, sue, and be sued entirely in its own name. This principle was established in the landmark 1896 case Salomon v Salomon & Co Ltd, where the House of Lords confirmed that an incorporated company must be treated as an independent person with its own rights and liabilities.

In practical terms, this means the company's financial obligations belong to the company — not to the people behind it.

What Does "Limited" Actually Mean?

"Limited" refers to the capped financial exposure of the company's members. For a company limited by shares, liability is restricted to the unpaid value of shares held. If you've paid £1 for one share and the business collapses with £500,000 in debt, your personal exposure is £1.

GOV.UK confirms that sole traders carry unlimited personal liability — meaning creditors can pursue a sole trader's home, savings, and personal assets to recover business debts. A limited company removes that exposure entirely, provided the company's finances are kept properly separate.

Who Owns and Runs a Private Limited Company?

Two distinct roles govern a private limited company:

- Shareholders are the owners. Their stake is proportional to the shares they hold. They receive dividends and typically vote on major company decisions, depending on share class.

- Directors manage the company day-to-day. They're responsible for filing obligations, strategic decisions, and compliance with the Companies Act 2006.

One person can hold both roles simultaneously, a common arrangement for small owner-managed businesses. Under the Companies Act 2006, a private company must have at least one director and at least one shareholder, and these can be the same individual.

Directors carry specific legal duties under sections 171–177 of the Companies Act 2006, including:

- Acting within their powers as defined by the company's constitution

- Promoting the success of the company for the benefit of its members

- Avoiding conflicts of interest with the company's affairs

- Exercising reasonable care, skill, and diligence in their role

Advantages of a Private Limited Company in the UK

Limited Liability Protection

Personal assets stay off-limits to company creditors. For any business owner taking on contracts, employees, or significant costs, this protection alone often justifies incorporation. Unlike sole traders, limited company owners are not personally liable for business debts — a distinction that matters most when things go wrong.

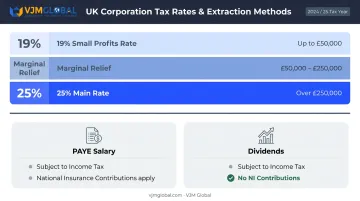

Tax Efficiency

Corporation tax applies to company profits — not personal income tax. Current rates (from 1 April 2026):

- 19% small profits rate on profits up to £50,000

- 25% main rate on profits over £250,000

- Marginal Relief applies between £50,000 and £250,000

Directors can then extract earnings as a combination of salary and dividends. Dividends are not subject to National Insurance contributions — confirmed by HMRC's National Insurance Manual. That makes dividend income more tax-efficient than an equivalent salary for many directors.

Professional Credibility and Name Protection

Operating as "Ltd" signals that your business is formally incorporated and regulated. Clients, suppliers, and lenders consistently treat limited companies as more credible counterparties. Practically, registering your company name with Companies House also protects it — no other UK company can register an identical name.

Perpetual Succession and Investment Access

Because the company exists independently of its owners, the business continues even if ownership changes. This structure offers practical advantages sole traders and partnerships cannot match:

- Shares can be sold, transferred, or passed on without disrupting operations

- The company survives changes in ownership or directorship

- New shares can be issued to raise capital from investors

Disadvantages of a Private Limited Company in the UK

Administrative and Compliance Burden

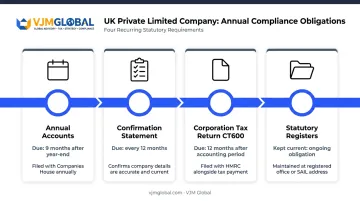

Running a limited company means accepting ongoing obligations:

- Annual accounts filed with Companies House within 9 months of the financial year-end

- A confirmation statement filed at least once every 12 months

- A corporation tax return (CT600) filed annually with HMRC

- Statutory registers maintained and kept current

Late accounts carry financial penalties starting at £150 for up to one month's delay, rising to £1,500 for delays exceeding six months — and those penalties double in consecutive late-filing years.

Reduced Financial Privacy

Everything filed with Companies House becomes publicly accessible — registered address, director details, filed accounts, and mortgage charges. Small companies can reduce disclosure requirements through available exemptions.

Micro-entities (turnover up to £1M, balance sheet up to £500,000, up to 10 employees) have even more limited filing obligations. Even so, some level of public transparency is unavoidable.

Complexity in Withdrawing Money

Unlike a sole trader, a limited company director cannot freely draw money from the business. Funds must be extracted through formal channels, each with distinct tax implications:

- PAYE salary — processed through payroll, subject to income tax and National Insurance

- Declared dividends — paid from post-tax profits, taxed at dividend rates

Mixing personal and company finances creates both legal liability and HMRC compliance issues.

Tax and Compliance Obligations for a Private Limited Company

Running a private limited company comes with firm statutory deadlines — miss them and you risk penalties, interest charges, or worse. Here's what directors are responsible for from day one.

Core Tax Obligations

A private limited company must:

- Register for corporation tax within three months of starting to trade

- File a CT600 annually — deadline is 12 months after the end of the accounting period

- Pay corporation tax — due 9 months and 1 day after the accounting period ends (for companies with taxable profits up to £1.5M)

- Register for VAT if taxable turnover exceeds £90,000 in any 12-month period, or if you expect to cross that threshold within the next 30 days

Ongoing Companies House Obligations

- Annual accounts: due 9 months after the accounting reference date

- Confirmation statement: due at least once every 12 months, confirming company details are current

- Failure to file a confirmation statement is a criminal offence — directors can be personally fined, and the company risks being struck off the register

UK companies expanding into markets like India face an additional compliance layer on top of these domestic obligations — covering FEMA regulations, GST registration, and transfer pricing requirements. VJM Global has supported over 250 UK businesses with exactly this challenge, handling cross-border accounting, compliance management, and India market entry from a single team.

How to Register a Private Limited Company in the UK

Registration runs through Companies House. Online applications cost £100 and are typically processed within 24 hours. Postal applications using form IN01 cost £124 and take 8–10 days.

What You'll Need Before Registering

- A unique company name that complies with Companies House naming rules

- A physical UK registered office address (PO Boxes are not permitted)

- At least one director (aged 16 or over)

- At least one shareholder

- A Standard Industrial Classification (SIC) code

- A memorandum and articles of association (you can use model articles or draft bespoke ones)

- Details of all People with Significant Control (PSCs) — anyone holding more than 25% of shares or voting rights must be disclosed

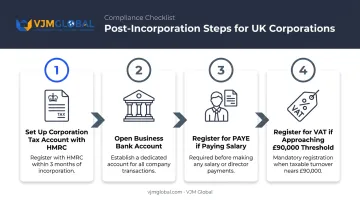

After Incorporation

Once Companies House issues the Certificate of Incorporation:

- Set up your corporation tax account with HMRC (often done automatically via the online registration service)

- Open a dedicated business bank account

- Register for PAYE if taking on employees or paying yourself a director's salary

- Register for VAT if turnover is approaching the £90,000 threshold

These post-incorporation steps apply equally to international founders. Directors do not need to live in the UK — a UK registered office address is the only location requirement, making incorporation accessible to non-residents. That said, non-UK directors should take advice on the tax residency implications for the company itself.

Frequently Asked Questions

What is a UK private limited company?

A UK private limited company is a legally incorporated business registered with Companies House. It exists as a separate legal entity from its owners, with shareholders' liability capped at the unpaid value of their shares — meaning personal assets are protected from company debts.

What is an example of a private limited company in the UK?

A local restaurant, independent retailer, or small consultancy operating under a name ending in "Ltd" is typically a private limited company. The company doesn't trade shares publicly and is usually owned by one or a small number of founders or investors.

Is it worth setting up a limited company in the UK?

For most businesses generating sustainable income, incorporation is worthwhile. Limited liability protection, tax efficiency through salary and dividends, and professional credibility are strong incentives. The trade-off is ongoing compliance obligations that typically require professional support.

Can a non-UK resident set up a private limited company in the UK?

Yes. There is no residency requirement for directors or shareholders. The only location obligation is a physical UK registered office address — not a requirement to live or work in the UK.

What is the difference between a private limited company and a sole trader in the UK?

The three main differences are:

- Legal separation: A limited company is its own legal entity; a sole trader is not

- Liability: Sole traders face unlimited personal liability; limited company shareholders do not

- Tax treatment: Limited companies pay corporation tax on profits; sole traders pay income tax and Class 4 NICs

How long does it take to register a private limited company in the UK?

Online applications via Companies House are typically processed within 24 hours. Postal applications take 8–10 business days. Almost everyone uses the online route.