The obligations go well beyond basic bookkeeping. You're dealing with statutory accounts, Corporation Tax returns, VAT, payroll, and personal Self Assessment — each with its own deadlines, rules, and consequences for getting it wrong.

This guide covers everything UK limited company directors need to know: what records to keep, how annual accounts work, every major tax obligation, the key deadlines and penalties, and how to decide whether to manage this yourself or bring in professional support.

Key Takeaways

- All UK limited companies must file annual accounts with Companies House and a Corporation Tax return (CT600) with HMRC every year — including dormant companies

- Accounts are due at Companies House 9 months after the financial year end; Corporation Tax is due for payment at 9 months and 1 day

- Directors remain personally liable for accuracy and deadlines, even when using an accountant

- Late filing penalties at Companies House double if accounts are filed late two years in a row

- VAT registration becomes mandatory once taxable turnover exceeds £90,000 in any rolling 12-month period

What Does Accounting for a Limited Company Actually Involve?

GOV.UK confirms that directors are legally responsible for company records, accounts, and performance — hiring an accountant is operational support, not a transfer of legal responsibility. That distinction matters more than many directors realise.

A limited company is a separate legal entity. Its finances must be kept entirely distinct from the director's personal finances. This isn't just good practice — it's a legal requirement.

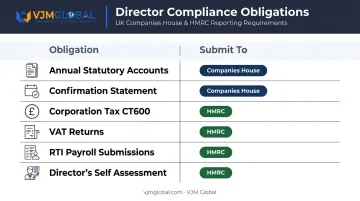

Core Obligations Every Director Must Meet

| Obligation | Submitted To |

|---|---|

| Annual statutory accounts | Companies House + HMRC (via CT600) |

| Confirmation Statement | Companies House |

| Corporation Tax return (CT600) | HMRC |

| VAT returns (if registered) | HMRC |

| RTI payroll submissions | HMRC |

| Director's Self Assessment | HMRC |

The Companies House and HMRC obligations are separate, with different deadlines and different consequences for late filing. Many directors conflate the two — a costly mistake.

That separation extends to how the company is taxed. Limited company accounting works differently from sole trader accounting: the company files its own tax return, pays its own Corporation Tax, and holds its own assets. A director's salary and dividends are personal income drawn from the company, distinct from the company's profit.

Bookkeeping and Record-Keeping Requirements

Under the Companies Act 2006, companies must keep accounting records that show and explain transactions, disclose financial position, and record day-to-day money flows.

What Records Must Be Kept

- All money received and spent, with supporting invoices and receipts

- Bank statements

- Details of assets owned and liabilities owed

- Year-end stock records (where applicable)

- Details of goods bought and sold — including supplier and customer identity (except retail)

- Payroll records: pay, deductions, RTI submissions, tax code notices, taxable benefits

Retention rule: GOV.UK requires all business records to be kept for a minimum of 6 years from the end of the financial year they relate to. HMRC can request records at any point during that window for a compliance check. PAYE records have a shorter retention period of 3 years from the end of the relevant tax year.

Making Tax Digital

MTD for VAT is already live: all VAT-registered businesses must use compatible software to keep digital records and submit returns. MTD for Corporation Tax is not currently planned for mandation.

Cloud accounting software (Xero, QuickBooks, Sage) keeps records organised, MTD-compliant, and audit-ready throughout the year. Worth adopting early regardless of your VAT status.

Preparing and Filing Annual Accounts

Statutory accounts are a formal legal document, not just an internal summary. They must be prepared under either UK GAAP or IFRS and typically include:

- A balance sheet (signed by a director)

- A profit and loss account

- A directors' report

- Notes to the accounts

- An auditor's report (unless exempt)

Audit Exemption and Simplified Accounts

Most small companies qualify for audit exemption and can file abridged accounts with Companies House rather than full statutory accounts. The thresholds depend on when your accounting period began.

For periods beginning on or after 6 April 2025 (current thresholds):

| Size | Turnover | Balance Sheet | Employees |

|---|---|---|---|

| Small company | ≤ £15m | ≤ £7.5m | ≤ 50 |

| Micro-entity | ≤ £1m | ≤ £500,000 | ≤ 10 |

Meet at least two of three criteria to qualify. For periods before 6 April 2025, the previous thresholds were:

| Size | Turnover | Balance Sheet | Employees |

|---|---|---|---|

| Small company | ≤ £10.2m | ≤ £5.1m | ≤ 50 |

| Micro-entity | ≤ £632,000 | ≤ £316,000 | ≤ 10 |

Micro-entities prepare a simplified balance sheet with minimal notes and no public profit and loss account. From 1 April 2028, Companies House rules will require micro and small companies to file a profit and loss account — though publication opt-out rules will apply.

Dormant Companies

Filing obligations don't disappear just because a company is inactive. Dormant companies must still submit simplified annual accounts and a Confirmation Statement to Companies House each year, even with no significant transactions.

Filing Deadlines

- Private companies: accounts due 9 months after the Accounting Reference Date (ARD)

- First accounts: due within 21 months of incorporation (where the first period exceeds 12 months)

- Your accounts submission to HMRC forms part of the CT600 filing

Tax Obligations: Corporation Tax, VAT, and Director's Self Assessment

Corporation Tax (CT600)

Every active limited company must register for Corporation Tax — typically done automatically at incorporation — then meet two separate deadlines each year:

- Pay Corporation Tax: 9 months and 1 day after the accounting period ends

- File the CT600 return: 12 months after the accounting period ends

The payment deadline falls before the filing deadline. Miss it, and HMRC will charge interest on the unpaid amount from day one.

Current Corporation Tax rates (from 1 April 2023):

- 19% on taxable profits below £50,000

- 25% on profits above £250,000

- Marginal Relief applies for profits between £50,000 and £250,000

Key reliefs worth knowing: the Annual Investment Allowance (AIA) for capital expenditure, and R&D tax credits if your company carries out qualifying research and development.

VAT

VAT registration is mandatory when taxable turnover exceeds £90,000 in any rolling 12-month period (threshold increased from £85,000 on 1 April 2024). You can also register voluntarily below the threshold — useful if you incur significant VAT on business purchases and want to reclaim it.

Once registered, you'll file quarterly VAT returns and must use MTD-compatible software to do so.

Director's Self Assessment

Not every director automatically needs to file a Self Assessment return — but most do. GOV.UK guidance states directors should file if they receive dividends, have untaxed income in addition to salary, or HMRC requests a return.

Dividends above the annual allowance (£500 for 2024/25) are taxed at the following personal rates:

- 8.75% — basic rate

- 33.75% — higher rate

- 39.35% — additional rate

Self Assessment is a personal tax obligation — entirely separate from the company's Corporation Tax bill. That distinction matters when planning your salary and dividend mix.

Payroll and PAYE

If the company pays salaries — including a director's salary — it must register as an employer and submit Real Time Information (RTI) returns to HMRC on or before each payday.

Many directors structure their pay to minimise National Insurance by keeping salary at or just below the thresholds, then drawing the remainder as dividends. For 2024/25, the key figures are:

- Employee Primary Threshold: £242/week (£1,048/month)

- Employer Secondary Threshold: £175/week (£758/month)

- Director salary strategy: Pay up to the Primary Threshold to retain State Pension entitlement without triggering employee NI

Key Filing Deadlines and Penalties

Deadline Summary

| Filing | Deadline |

|---|---|

| Confirmation Statement | Within 14 days of the 12-month review date |

| Annual accounts — Companies House | 9 months after ARD |

| Corporation Tax payment | 9 months and 1 day after accounting period |

| CT600 return — HMRC | 12 months after accounting period end |

Companies House Late Filing Penalties

GOV.UK confirms the following penalties apply to private companies that miss their accounts deadline:

| How Late | Penalty |

|---|---|

| Up to 1 month | £150 |

| 1 to 3 months | £375 |

| 3 to 6 months | £750 |

| More than 6 months | £1,500 |

Critical: these penalties double if accounts are late for two consecutive financial years. Continued failure is a criminal offence — directors can be personally fined and the company struck off the register.

HMRC Penalties for Late CT600 Filing

Current HMRC penalties for late Company Tax Returns scale with how long the return is overdue:

| How Late | Penalty |

|---|---|

| 1 day late | £200 |

| 3 months late | Another £200 (rises to £1,000 each if late three times running) |

| 6 months late | 10% of unpaid tax added |

| 12 months late | Another 10% of unpaid tax added |

Late payment interest also applies — currently Bank of England base rate plus 4% (7.75% from January 2026 for Corporation Tax).

Should You Hire an Accountant or Do It Yourself?

There's no legal requirement to use an accountant. A director can prepare and file their own accounts. But ICAEW research found that three quarters of SMEs used an external accountant in the past year — and there are good reasons for that.

What a Qualified Accountant Provides

- Expert knowledge of current rates, thresholds, and legislation — which change regularly

- Reduced risk of errors that trigger penalties or HMRC enquiries

- Tax planning: efficient salary/dividend structuring, AIA, R&D credits

- Handling HMRC correspondence if questions arise

- Time freed up to focus on running the business

The accountant cost typically pays for itself through legitimate tax savings and penalty avoidance — particularly as a business grows or takes on complexity.

For UK limited company directors with cross-border activity, particularly those with operations or expansion plans in India, generalist accountants often fall short. Dual-jurisdiction compliance spans UK statutory requirements alongside Indian obligations like FEMA, GST, and transfer pricing rules — coordination that requires specialist expertise.

VJM Global's team of Chartered Accountants has supported 250+ UK businesses with accounting, compliance, and tax obligations, maintaining a 95% client retention rate. Directors who need integrated UK-India accounting support, or simply want expert oversight without building an in-house finance team, can use their outsourced accounting and CFO services as a cost-effective alternative to full-time hires.

Frequently Asked Questions

How much do accountants charge for limited companies in the UK?

Fees vary based on business complexity and the scope of services required. Simple small companies typically pay a few hundred to over a thousand pounds per year. Compare fixed-fee packages against hourly rates — fixed fees are generally more predictable for standard compliance work.

Do I need an accountant for a limited company in the UK?

No legal requirement exists, but directors remain personally responsible for accuracy and deadlines regardless of who prepares the accounts. Professional support reduces the risk of errors, missed deadlines, and financial penalties.

What is the 2-year rule for small companies?

This refers to Companies House's rule that late filing penalties double if a company's accounts are filed late for two consecutive financial years.

What records does a limited company need to keep in the UK?

Key categories include income and expenses, invoices, bank statements, payroll records, asset details, and liabilities. All records must be retained for a minimum of 6 years from the end of the financial year they relate to.

When does a limited company need to register for VAT?

VAT registration is mandatory when taxable turnover exceeds £90,000 in any rolling 12-month period. Voluntary registration below the threshold is also permitted — useful if you want to reclaim VAT on business purchases.

Can I do my own accounting for a limited company?

Yes, it's legally permitted. However, limited company accounting involves detailed compliance knowledge across multiple obligations and deadlines. Mistakes can result in financial penalties or incorrect tax filings — both of which are more costly to fix than to prevent.