Introduction

India runs a year-round compliance calendar with simultaneous monthly, quarterly, and annual obligations across GST, income tax, TDS, and transfer pricing — often requiring 24 or more filings per entity, per year. For Singapore businesses used to a streamlined tax environment, this is a significant operational shift.

Missing a single deadline triggers automatic interest and penalties that compound fast. Getting ahead of this calendar isn't just good practice — it's operationally critical from day one.

This guide is written for Singapore companies operating or planning to operate in India — whether through a wholly owned subsidiary, branch office, liaison office, or project structure. It covers the taxes you will encounter, the compliance timelines you must track, and the pitfalls that most commonly catch foreign businesses off guard.

VJM Global has spent 30+ years helping foreign companies navigate India's compliance landscape, including Singapore businesses at every stage of their India entry.

Key Takeaways

- Five separate tax regimes apply — corporate income tax, TDS, GST, advance tax, and transfer pricing — each with its own registration, filing, and penalties

- India's financial year (April 1–March 31) differs from Singapore's calendar year, directly affecting tax planning and filing schedules

- The India-Singapore DTAA reduces withholding tax on royalties and interest from 20% to 10% — valid only with a Tax Residency Certificate and Form 10F

- Non-compliance triggers financial penalties, interest at 1–1.5% per month, and potential prosecution

- Set up compliant systems and engage local tax expertise before operations begin — India's compliance burden is consistently underestimated

What Tax Compliance in India Means for Singapore Businesses

Tax compliance in India means fulfilling all obligations under the Income Tax Act 1961 and the GST Act: registering with the appropriate authorities, accurately reporting taxable income and transactions, filing returns by prescribed deadlines, and paying all applicable taxes — both direct (income tax, capital gains) and indirect (GST).

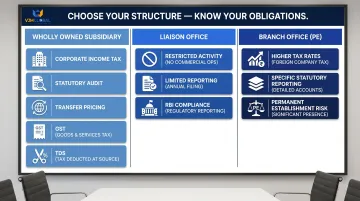

Your entity structure determines exactly which obligations apply. Each structure carries a distinct compliance profile:

- Wholly owned subsidiary (Indian company): corporate income tax, statutory audit, transfer pricing documentation, GST returns, and TDS filings

- Liaison office: limited activity permission with a narrower, but still mandatory, compliance scope

- Branch office (Permanent Establishment): higher applicable tax rates and specific reporting requirements

Choosing the right structure before entering India is critical — it shapes every filing, registration, and tax exposure that follows.

Once your structure is in place, the nature of India's tax system adds another layer of responsibility. India operates on self-assessment: the onus is on the taxpayer — not the tax authority — to correctly compute, report, and pay taxes. This differs fundamentally from a notice-based system.

Many Singapore businesses, accustomed to a straightforward annual filing, are caught off guard by India's compliance calendar with year-round deadlines requiring consistent attention throughout the financial year.

Key Taxes Singapore Businesses Must Comply With in India

Corporate Income Tax (CIT)

Indian subsidiaries of Singapore companies are taxed as domestic companies on their worldwide income. Most opt for the Section 115BAA regime at an effective rate of 25.168%, which eliminates Minimum Alternate Tax (MAT) exposure and provides rate certainty regardless of income level. The standard regime imposes rates of 30% (base) with surcharge and cess, reaching effective rates up to 34.944%.

Permanent Establishments (PE) — such as branch offices — face a higher rate: base rate of 35% plus surcharge and cess, resulting in effective rates up to 38.22%. This creates an approximately 13 percentage-point disadvantage versus a subsidiary on the 115BAA regime, making subsidiary incorporation the preferred structure for sustained operations.

MAT provisions apply to companies not under Section 115BAA. The rate was reduced from 15% to 14% as proposed in Union Budget 2025, effective April 2026. MAT credit can be carried forward for 15 years.

Tax Deducted at Source (TDS)

TDS is a mechanism where the payer deducts tax at the point of payment on specified transactions — salaries, contractor payments, rent, professional fees, royalties — and deposits it with the government by the 7th of the following month.

Key TDS rates include:

- Contractor payments: 1% (individual/HUF), 2% (others)

- Professional fees: 10%

- Technical services: 2%

- Rent (land, building): 10%

- Interest: 10%

For cross-border payments from Singapore to India, TDS rates under domestic law (often 20% on royalties and fees for technical services) can be reduced by invoking the India-Singapore DTAA.

Failure to deduct TDS makes the payer an "assessee in default" under Section 201, attracting interest at 1% per month (non-deduction) or 1.5% per month (deducted but not deposited), with no discretionary waiver.

Goods and Services Tax (GST)

GST is an indirect tax on the supply of goods and services in India, structured as CGST + SGST for intra-state and IGST for inter-state/import transactions.

Registration thresholds:

- Services or mixed supply: ₹20 lakh annual turnover

- Exclusively goods: ₹40 lakh (except specified items)

- Inter-state supply of goods: compulsory registration regardless of turnover

Periodic returns include GSTR-1 (outward supplies) and GSTR-3B (summary and payment), filed monthly or quarterly depending on turnover. Late filing attracts interest and late fees (₹200 per day) and can block GST credit claims.

Reverse charge on imported services: When an Indian entity receives services from a Singapore parent — such as management, technology, or consulting — the Indian recipient must self-assess and deposit GST under the reverse charge mechanism. VJM Global handles GST registration, GSTR-1 and GSTR-3B filing, and reverse charge advisory for Singapore businesses operating in India.

Transfer Pricing

Beyond indirect taxes, related-party transactions between a Singapore parent and its Indian subsidiary — management fees, loans, IP licensing, shared services — carry their own compliance burden. Each must be conducted at arm's length price and documented in a Transfer Pricing report (Form 3CEB).

Documentation requirements:

- Local File: Required for every international transaction, regardless of value

- Form 3CEB: CA-certified TP report filed by October 31 each year

- Master File: Mandatory when consolidated group revenue exceeds ₹500 crore

- Country-by-Country Report (CbCR): Required above ₹5,500 crore consolidated group revenue

India has one of the most active transfer pricing enforcement regimes in Asia. Non-compliance or inadequate documentation can result in significant tax adjustments and penalties (flat ₹1 lakh for non-filing of Form 3CEB). VJM Global's transfer pricing team helps structure and document inter-company transactions to hold up under audit.

Advance Tax and Withholding Obligations

If an Indian entity's estimated annual tax liability exceeds ₹10,000, it must pay advance tax in four instalments:

| Instalment | Due Date | Cumulative % of Estimated Tax |

|---|---|---|

| 1st | June 15 | 15% |

| 2nd | September 15 | 45% |

| 3rd | December 15 | 75% |

| 4th | March 15 | 100% |

Missing instalments attracts interest under Sections 234B and 234C. Singapore businesses often miss the first instalment (June 15) because their India entities are still being set up.

TAN (Tax Deduction Account Number) is required for any entity obligated to deduct or collect tax at source — a registration separate from PAN.

The Tax Compliance Process in India: From Registration to Annual Filing

India's tax year runs April 1 to March 31, meaning Singapore businesses must align their India entity's reporting periods accordingly. Compliance is a continuous, year-round process with monthly, quarterly, and annual obligations running in parallel.

Step 1: Registrations Before You Operate

Before a Singapore company's Indian entity can conduct taxable operations, it must obtain:

- PAN (Permanent Account Number): The primary tax identity

- TAN: If it will deduct tax at source

- GST registration: If turnover threshold applies or if conducting inter-state supply

These registrations are prerequisites for opening a bank account, executing contracts, and filing returns. VJM Global handles PAN, TAN, and GST registration for Singapore companies' Indian entities as part of business setup.

Step 2: Ongoing Monthly and Quarterly Filings

TDS compliance:

- Deduct TDS on applicable payments

- Deposit by 7th of the following month (30 April for March)

- File quarterly TDS returns: Form 24Q (salary), Form 26Q (non-salary domestic), Form 27Q (non-residents)

GST returns:

- GSTR-1 (outward supplies)

- GSTR-3B (summary and payment)

- Filed monthly or quarterly depending on turnover

Delays or errors attract interest, late fees, and blocked GST credit claims.

Step 3: Advance Tax Payments

Indian entities must pay advance tax in four instalments across the financial year:

| Due Date | Cumulative Payment Required |

|---|---|

| June 15 | 15% of estimated tax liability |

| September 15 | 45% of estimated tax liability |

| December 15 | 75% of estimated tax liability |

| March 15 | 100% of estimated tax liability |

Missing instalments attract interest under Sections 234B and 234C at 1% per month. Once advance tax is settled, attention shifts to the annual filing cycle.

Step 4: Annual Income Tax Return (ITR) Filing and Audit

Key deadlines:

- Tax audit report (Form 3CD): September 30

- ITR filing: October 31 for companies subject to tax audit

- ITR with transfer pricing certification (Form 3CEB): November 30

If the Indian entity's turnover exceeds ₹1 crore (or ₹50 lakh for professional income), a tax audit by a Chartered Accountant is mandatory. Singapore-owned Indian companies with related-party transactions must also file Form 3CEB. VJM Global's team of Chartered Accountants and compliance professionals supports Singapore businesses through each stage of this annual cycle, conducting statutory tax audits and coordinating transfer pricing certifications.

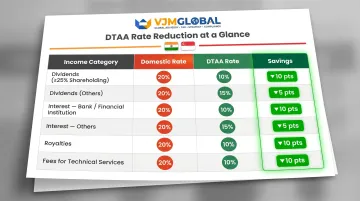

How the India-Singapore DTAA Affects Your Tax Obligations

The India-Singapore Double Taxation Avoidance Agreement (DTAA) is one of the most valuable tools available to Singapore businesses operating in India — it can cut your withholding tax burden by up to 50% on key payment categories.

DTAA-reduced rates:

| Income Category | Domestic Rate | DTAA Rate | Savings |

|---|---|---|---|

| Dividends (25%+ shareholding) | 20% | 10% | 10 ppt |

| Dividends (others) | 20% | 15% | 5 ppt |

| Interest (bank/financial institution) | 20% | 10% | 10 ppt |

| Interest (others) | 20% | 15% | 5 ppt |

| Royalties | 20% | 10% | 10 ppt |

| Fees for Technical Services | 20% | 10% | 10 ppt |

To claim DTAA rates, your Singapore entity must meet two procedural requirements:

- Obtain a Tax Residency Certificate (TRC) from IRAS confirming Singapore tax residency

- File Form 10F electronically on the Indian Income Tax portal before payments are processed

VJM Global helps Singapore companies navigate both steps — from obtaining the TRC to completing Form 10F on the Indian portal — so treaty benefits aren't lost to procedural gaps.

Claiming the DTAA rate is only part of the picture. Singapore businesses also need to monitor their physical presence in India to avoid triggering a Permanent Establishment (PE).

Permanent Establishment (PE) Risk

If a Singapore company's employees or agents are active in India beyond a permissible scope, India can claim the right to tax that entity's profits as if it had a PE.

Service PE thresholds under the India-Singapore DTAA:

- General services: More than 90 days in any 12-month period

- Services to associated enterprises: More than 30 days in any 12-month period

This applies directly to Singapore businesses providing management services, deploying staff in India, or using India-based subsidiaries for day-to-day operations. Singapore service companies must track deployment days meticulously to avoid triggering PE status.

General Anti-Avoidance Rules (GAAR)

India's GAAR, effective from April 2017, allows tax authorities to deny treaty benefits where the principal purpose of an arrangement is to obtain a tax benefit. GAAR applies when the aggregate tax benefit exceeds ₹3 crore (approximately ₹30 million).

For Singapore businesses, substance is critical. Holding structures and service arrangements must have genuine commercial rationale and real operational presence — employees, office space, and local decision-making authority — to withstand GAAR scrutiny.

VJM Global advises on structuring cross-border arrangements to satisfy both GAAR requirements and the Multilateral Instrument's Principal Purpose Test, helping Singapore businesses protect their treaty positions from challenge.

Common Compliance Mistakes Singapore Businesses Make in India

Missing TDS Obligations on Cross-Border Payments

Many Singapore businesses assume that paying from a Singapore bank account to India is outside India's TDS scope. However, if the payment is for services rendered in India or the payee has Indian-sourced income, TDS obligations may apply. Non-deduction makes the payer an "assessee in default," creating liability for the unpaid tax plus interest at 1% per month.

A frequent misstep is deducting TDS at the wrong rate by failing to invoke the DTAA correctly. Always secure a valid Tax Residency Certificate (TRC) and file Form 10F to claim reduced treaty rates.

Treating India Compliance as an Extension of Singapore Accounting

Singapore's calendar financial year (January–December) and straightforward tax filing requirements lead many businesses to under-resource their India compliance teams. India requires:

- A separate, India-specific compliance calendar

- Reconciled GST returns

- Statutory audit under the Companies Act

- Transfer pricing documentation

All must be managed as distinct processes with dedicated local expertise — not as an extension of Singapore's systems.

Underestimating Transfer Pricing Documentation Requirements

Singapore businesses with inter-company transactions frequently enter India without arm's length documentation in place. Common transaction types that attract scrutiny include:

- Management fees

- Shared IT infrastructure costs

- Intercompany loans

- Brand royalties

Transfer pricing audits in India are active and penalties can far exceed the tax saved on the original transaction. VJM Global helps Singapore businesses prepare benchmarking studies, Local Files, and Form 3CEB certifications before scrutiny arises — not after.

Frequently Asked Questions

What is tax compliance in India?

Tax compliance in India means fulfilling all obligations under Indian tax law: registering with authorities, accurately reporting income and transactions, filing returns on time, and paying the correct taxes including corporate income tax, GST, and TDS, as required by the Income Tax Act 1961 and the GST Act.

How serious is a tax compliance check in India?

India's Income Tax Department conducts scrutiny assessments, including faceless assessments, and can select returns for detailed review. Non-compliance can result in tax demands, interest, penalties, and in cases of wilful evasion, prosecution. Singapore businesses operating in India should treat deadlines as non-negotiable.

What is a tax notice in India?

A tax notice is a formal communication from the Income Tax Department requesting information, explanation of discrepancies, or response to a proposed tax adjustment. Notices must be responded to within the specified deadline, or the taxpayer risks adverse orders and penalties.

How many years back can the Income Tax Department send a notice in India?

For regular assessments, the department can reopen cases up to 3 years and 3 months for escaped income below ₹50 lakh, and up to 5 years and 3 months for escaped income of ₹50 lakh or more. This means maintaining well-organised records for at least six years is advisable.

Does the India-Singapore tax treaty reduce double taxation for Singapore businesses?

Yes. The India-Singapore DTAA provides reduced withholding tax rates on dividends, royalties, and interest, and prevents the same income from being taxed in both countries. To claim treaty benefits, Singapore entities must provide a valid Tax Residency Certificate and Form 10F to the Indian payer.

What happens if a Singapore company misses an Indian tax filing deadline?

Late filing of income tax returns attracts a late fee and interest on outstanding tax. Missing TDS or GST filing deadlines triggers interest and penalties. Repeated or significant non-compliance can lead to scrutiny assessment, disallowance of expenses, or blocking of GST portal access.

Need help navigating India's tax compliance landscape? VJM Global's team of Chartered Accountants and international tax specialists supports Singapore businesses at every stage — from entity structure advisory and tax registrations to monthly compliance, statutory audits, and transfer pricing certification. Contact us at info@vjmglobal.com or call +91 98915 76441 to discuss your India compliance needs.