Introduction

Small business owners in Singapore often face a critical decision: which accounting framework applies to their company, and how do they balance compliance costs against reporting quality? The answer affects financial statement preparation costs, disclosure obligations, and how much confidence stakeholders place in your numbers.

Singapore maintains three distinct accounting frameworks: SFRS(I) (aligned with IFRS), full SFRS, and SFRS for Small Entities (SFRS SE).

This guide focuses on SFRS SE — a simplified framework for smaller businesses without public accountability. If you're a director, finance manager, or business owner evaluating your options, understanding eligibility, technical differences, and the strategic trade-offs is what this guide covers.

By the end, you'll know the eligibility thresholds, the technical differences that matter most to SMEs, how to decide whether adoption fits your business, and the disclosure mistakes that most commonly trip up compliance.

TLDR:

- SFRS SE is a simplified framework for small entities meeting size thresholds and lacking public accountability

- Key simplifications cover lease treatment, impairment models, and reduced risk disclosures

- Eligibility requires meeting two of three criteria: revenue ≤S$10M, assets ≤S$10M, employees ≤50

- Framework choice is strategic: weigh stakeholder requirements, consolidation needs, and growth plans

- New 2027 amendments require ageing analysis of receivables and liability maturity disclosures

What Is SFRS for Small Entities?

SFRS for Small Entities (SFRS SE) is a self-contained, simplified financial reporting framework developed specifically for smaller businesses without public accountability. The framework reduces compliance complexity while still producing financial statements that lenders, shareholders, and owners can rely on for decision-making.

The Accounting Standards Council (ASC) of Singapore introduced SFRS SE by adopting the IFRS for SMEs Accounting Standard without modification. This alignment means Singapore's small entity framework mirrors a globally recognised standard, providing consistency for businesses with international operations or stakeholders. According to the ASC's Statement of Intent, the framework was introduced to reduce the cost and complexity burden that full SFRS placed on smaller, owner-managed entities.

SFRS SE does not mean fewer obligations altogether. Entities must still present a complete set of financial statements and provide a true and fair view. That complete set includes:

- Statement of financial position

- Statement of comprehensive income

- Statement of changes in equity

- Notes to the financial statements

The simplification applies to specific recognition, measurement, and disclosure requirements — not to the overall obligation to report accurately.

The most recent version (Third Edition) was issued on 18 August 2025 and is effective for annual reporting periods beginning on or after 1 January 2027, with early application permitted.

Who Qualifies? Eligibility Criteria for SFRS for Small Entities

Eligibility for SFRS SE requires satisfying two simultaneous conditions: meeting the prescribed size thresholds and not being publicly accountable. Both tests must pass for a company to qualify.

Size Thresholds

Companies must meet at least two of the following three criteria to qualify:

- Annual revenue not exceeding S$10 million

- Total assets not exceeding S$10 million

- Average number of employees not exceeding 50

This "two out of three" rule provides flexibility. A company with S$12 million in revenue but only S$8 million in assets and 30 employees would still qualify.

Critical timing rules apply. According to IRAS guidance, a company is disqualified from using SFRS SE only if it fails to meet the prescribed criteria for two consecutive financial years. This provides a one-year grace period for businesses experiencing temporary growth spurts or revenue fluctuations. Conversely, entities currently on full SFRS become eligible to switch to SFRS SE only after satisfying the threshold criteria for two consecutive years.

Newly incorporated companies are immediately eligible in their first two years of operation, provided they are not publicly accountable.

Group-level assessment: If your company is part of a group, the size criteria should be assessed on a consolidated basis across all group entities. A subsidiary that individually meets the thresholds may still be disqualified if the group as a whole exceeds them.

Public Accountability Test

Even if a company meets all size thresholds, it is excluded from SFRS SE if it is "publicly accountable." This designation applies to:

- Companies whose shares or debt instruments are traded (or being prepared for trading) in a public market

- Entities that hold assets in a fiduciary capacity for a broad group of outsiders as a primary activity—including banks, insurers, securities dealers, and mutual funds

- Public companies as defined under the Singapore Companies Act

- Charities registered under the Charities Act

Two exclusions frequently catch growing companies off guard.

Group Consolidation Conflicts

If the entity is part of a group where the parent company uses full SFRS or IFRS, differences in accounting policies between frameworks may complicate group consolidation. The parent's framework typically prevails in these situations.

That means a Singapore subsidiary could be required to report under full SFRS for consolidation purposes, even if it independently qualifies for SFRS SE.

IPO Planning

Companies preparing for an initial public offering should not adopt SFRS SE. Raising capital through public markets establishes public accountability and disqualifies the entity outright. Switching frameworks mid-IPO preparation creates unnecessary transition costs.

Key Differences Between SFRS for Small Entities and Full SFRS

While SFRS SE reduces complexity, the differences are specific and technical—not a blanket removal of rules. Understanding exactly where the frameworks diverge is essential before making a framework decision.

Lease Accounting

The most significant divergence involves lease treatment. Under full SFRS 116 (aligned with IFRS 16), lessees must recognise virtually all leases on the balance sheet as right-of-use assets and corresponding lease liabilities. This requirement fundamentally changes how leases appear in financial statements.

SFRS SE retains the traditional operating/finance lease classification model. Operating leases are expensed on a straight-line basis over the lease period without balance-sheet recognition. The IASB confirmed that leases will be addressed in the Board's next comprehensive review — so the Third Edition of SFRS SE has not been updated for IFRS 16.

For most SMEs, the SFRS 116 approach adds reconciliation complexity for tax filings and internal reporting that rarely justifies the effort. The practical effect: common lease types stay as simple expense line items:

- Property leases — expensed straight-line, no balance sheet impact

- Equipment rentals — recognised as period costs without asset capitalisation

- Vehicle leases — treated as operating expenses throughout the lease term

Impairment of Receivables

Full SFRS 109 requires companies to apply the Expected Credit Loss (ECL) model to assess receivables impairment. This forward-looking model demands historical data analysis, customer credit assessments, and professional judgement to estimate losses that haven't yet occurred — a substantial exercise for a small finance team.

SFRS SE retains the simpler incurred loss model. Under Section 11 of the IFRS for SMEs, entities recognise impairment only when there is "objective evidence" resulting from "loss events" that a financial asset is impaired. The framework explicitly states that entities "shall not consider possible future credit losses not yet incurred."

2027 amendment: The Third Edition (effective 1 January 2027) introduces a new requirement in paragraph 11.43. SFRS SE entities must provide an ageing analysis of trade receivables and other financial assets measured at amortised cost, determined by reference to the due date.

The disclosure must show separately: (a) amortised cost before any impairment reduction, and (b) any allowance for impairment or uncollectability. The ECL model itself, however, remains inapplicable to SFRS SE entities despite this new disclosure requirement.

Treatment of Non-Financial Assets and Goodwill

SFRS SE permits only the cost model for all non-financial assets. The revaluation model available under full SFRS is not permitted. This simplifies subsequent measurement and eliminates the need for regular independent valuations.

Goodwill treatment differs substantially. All intangible assets under SFRS SE — including goodwill — are presumed to have finite useful lives and must be amortised on a systematic basis. Paragraph 19.34 of the Third Edition specifies that if an entity cannot reliably establish the useful life of goodwill, the estimate shall not exceed ten years. Entities may amortise over longer periods only if they can reliably establish that specific useful life.

Under full SFRS (SFRS(I) 3 and SFRS(I) 1-36), goodwill is not amortised but tested annually for impairment — a more complex and judgemental process.

Financial Risk Disclosures

Full SFRS 107 requires extensive disclosures on credit, liquidity, and market risks, including:

- Qualitative disclosures about the nature and extent of risks

- Sensitivity analyses for market risks

- Detailed ECL reconciliations

These requirements do not apply under SFRS SE. The framework specifically excludes qualitative risk disclosures equivalent to IFRS 7.33, sensitivity analysis requirements equivalent to IFRS 7.40, and detailed ECL reconciliations.

From 2027, SFRS SE entities will need to disclose:

- An ageing analysis of trade receivables by due date (paragraph 11.43)

- A maturity analysis for financial liabilities, showing remaining contractual maturities using contractual undiscounted cash flows (paragraph 11.43A)

These new disclosures improve transparency without imposing the full burden of SFRS 107 compliance.

Borrowing Costs

SFRS SE requires that all borrowing costs be recognised as expenses in the period they are incurred. Capitalisation is not permitted, regardless of how the funds are used.

Full SFRS (SFRS(I) 1-23, aligned with IAS 23) takes the opposite approach: borrowing costs directly attributable to acquiring, constructing, or producing a qualifying asset must be capitalised as part of that asset's cost.

For SMEs building or acquiring major assets, this distinction has real practical weight. Interest expense flows straight to profit or loss under SFRS SE. Full SFRS requires finance teams to track qualifying borrowings, calculate capitalisation rates, and maintain detailed attribution records throughout the asset's construction or acquisition period.

Should Your Business Adopt SFRS for Small Entities?

Eligibility is a necessary but not sufficient condition for adoption. Directors should treat framework choice as a strategic governance decision, not an routine administrative choice.

For Newly Incorporated Entities

New startups that meet SFRS SE thresholds are in the best position to adopt immediately. They have:

- No legacy accounting systems to modify

- No transition costs

- No staff retraining requirements

- No comparative figures to restate

Finance processes can be set up aligned with SFRS SE from day one. The immediate benefit is reduced disclosure requirements and simpler accounting policies, allowing the finance function to focus resources on business growth rather than complex compliance.

For Existing SFRS-Compliant Companies

Companies already reporting under full SFRS face a different calculation. Transitioning to SFRS SE may require:

- Modifying accounting software configurations

- Retraining finance staff on different recognition and measurement rules

- Restating comparative figures for the prior year

- Updating accounting policy documentation

The core question is whether compliance savings outweigh the transition investment. Companies already comfortable under full SFRS and not facing excessive compliance burden are better off staying on full SFRS rather than absorbing transition costs for limited gain.

Stakeholder and Strategic Considerations

Four factors should inform your framework decision:

- Lender and investor requirements: Some lenders require full SFRS-level financials for credit decisions or covenant monitoring. Switching without consultation could trigger renegotiation obligations.

- Group consolidation alignment: Subsidiaries within a group reporting under full SFRS or IFRS may need to match the parent's framework. Different policies create reconciliation burdens and consolidation errors.

- Growth trajectory and exit plans: If an IPO, acquisition, or significant funding round is anticipated within two to three years, starting on full SFRS avoids disruptive framework changes during capital events.

- Commercial sensitivity: ACRA lodgement makes financials visible to competitors. SFRS SE's reduced disclosure requirements can limit exposure of commercially sensitive information.

VJM Global's accounting and compliance advisory team works with foreign companies and SMEs to evaluate whether SFRS SE fits their specific structure, ownership profile, and growth trajectory, providing guidance tailored to each business's actual circumstances.

Common Disclosure Pitfalls Small Entities Should Avoid

"Simpler" does not mean "minimal." Over-reducing disclosures is one of the most common mistakes small entity finance teams make — and the gaps it creates tend to surface at the worst possible time: during audits or regulatory filings.

Five recurring disclosure issues:

Copying policies from old SFRS templates without tailoring them to actual transactions creates disconnects. Remove irrelevant sections, add entity-specific treatments, and make sure what's written reflects what the company actually does.

Director accounts, shareholder loans, and associated-entity transactions buried under "other receivables/payables" draw immediate scrutiny. SFRS SE requires separate disclosure of the relationship, transaction details, and key terms — interest-free, unsecured, repayable on demand. This is consistently one of the first things auditors flag.

Inventory write-downs, provisions, trade receivable impairment, and asset useful lives all require brief but specific explanations of the assumptions used. "Management assessed" without any supporting basis raises questions for auditors and weakens the notes.

Note references on the face of financial statements must match supporting notes exactly. If the statement of financial position points to "Note 8" for PPE, Note 8 must contain PPE — not inventory or something else. Mismatches create audit delays and signal poor quality control.

Even under a simplified framework, material off-balance sheet exposures cannot be skipped. Common omissions include:

- Significant guarantees given

- Major customer concentration (e.g., one customer representing >20% of revenue)

- Pledged assets securing borrowings

- Operating lease commitments (even though not capitalised under SFRS SE)

Leaving these out doesn't reduce compliance burden — it just shifts the problem to the next audit cycle, usually with additional queries attached.

How to Transition Between Accounting Frameworks

Framework transitions run in two directions: from full SFRS to SFRS SE when entities become eligible and want to reduce compliance costs, or from SFRS SE to full SFRS when companies grow beyond thresholds, prepare for listing, or face new group reporting requirements.

Both transitions require:

- Identifying recognition and measurement differences between frameworks

- Making transition adjustments to retained earnings or comparative figures

- Providing specific transition disclosures in the year of change

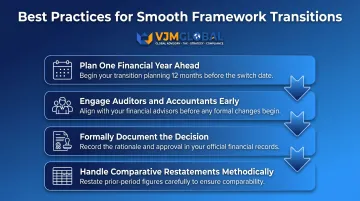

Meeting these requirements is straightforward with early planning. The four practices below consistently separate smooth transitions from disruptive ones.

Best practices for smooth transitions:

Start planning a full financial year ahead. This gives enough time to identify all accounting policy differences and assess their impact on financial statements before the transition year begins.

Bring in auditors and accountants early. Advisers can flag implications for bank covenants (which often reference specific accounting ratios), group reporting requirements, and regulatory filings — issues that are costly to discover after the transition is underway.

Formally document the decision. The board or shareholders should record the framework change decision, including business rationale and expected benefits. This record supports regulatory filings and demonstrates proper governance.

Handle comparative restatements methodically. Transitions generally require restating prior-period comparatives under the new framework — meaning two sets of figures for the transition year: opening balances under the new framework and prior-year comparatives adjusted for accounting policy changes.

Working through these steps with a qualified accountant reduces the risk of errors in comparative figures and ensures transition disclosures meet ACRA requirements.

Frequently Asked Questions

What is the main difference between SFRS and SFRS for Small Entities?

Full SFRS is a comprehensive framework built for companies with diverse external users and complex transactions. SFRS SE is a simplified alternative for eligible smaller entities without public accountability, offering targeted reductions in lease accounting, financial risk disclosures, asset measurement, and impairment requirements.

Can a company voluntarily choose to use full SFRS even if it qualifies for SFRS for Small Entities?

Yes — meeting the SFRS SE eligibility criteria does not obligate adoption. Companies that prefer full SFRS reporting, have stakeholders requiring it, or anticipate future growth events can continue using full SFRS.

What happens if a company exceeds the SFRS for Small Entities size thresholds?

A company loses SFRS SE eligibility only after failing to meet the size criteria for two consecutive financial years. A single year of exceeding the threshold does not trigger an immediate framework switch, which benefits businesses with fluctuating revenue.

Are foreign-owned companies incorporated in Singapore eligible for SFRS for Small Entities?

Eligibility is based on the company's own size thresholds and public accountability status, not its shareholders' nationality. However, if the foreign parent prepares consolidated accounts under full SFRS or IFRS, the subsidiary may need to align with the group's reporting framework.

Do companies using SFRS for Small Entities still need a statutory audit?

Accounting framework choice and audit requirements are separate matters. Singapore's Companies Act sets its own audit exemption criteria based on "small company" status, meaning a company could still be required to undergo a statutory audit even while using SFRS SE.

What financial statements must be prepared under SFRS for Small Entities?

A complete set of financial statements is still required. This includes:

- Statement of financial position

- Statement of comprehensive income (or a separate income statement)

- Statement of changes in equity (or a combined statement of income and retained earnings, if conditions are met)

- Notes covering accounting policies and other explanatory information