Introduction

SAFE (Simple Agreement for Future Equity) agreement accounting poses a critical but often misunderstood challenge for Singapore startups. Despite the instrument's "simple" name, its accounting treatment under Singapore Financial Reporting Standards (SFRS/SFRS(I)) requires careful contractual analysis and professional judgement.

Most founders understand the mechanics — investors provide capital now and receive the right to convert into equity later. Few understand how these instruments must actually appear on financial statements. A misclassification can distort the balance sheet, complicate investor due diligence, and create compliance exposure under ACRA's Financial Reporting Surveillance Programme.

Singapore-incorporated companies applying SFRS(I)—Singapore's IFRS-aligned standards—must evaluate each SAFE under SFRS(I) 1-32 (Financial Instruments: Presentation) and SFRS(I) 9 (Financial Instruments). The classification outcome determines whether the SAFE appears as equity or as a financial liability, directly affecting key metrics investors scrutinise during Series A due diligence.

Getting this right matters from day one. This guide covers how Singapore companies should classify, record, measure, and disclose SAFEs under SFRS(I) — from initial receipt of funds through to conversion.

Key Takeaways

- A SAFE is not automatically classified as equity in Singapore—specific contractual terms can force liability classification under SFRS(I) 1-32

- Classification depends on passing the "fixed-for-fixed" test with no cash settlement obligation

- At initial recognition, the credit posts to equity reserves or financial liability based on classification

- Upon conversion, the SAFE balance transfers to share capital and share premium

- Misclassification distorts financial ratios, triggers audit findings, and undermines investor confidence—get accounting advice early

What a SAFE Represents from an Accounting Perspective in Singapore

In accounting terms, a SAFE is a financial instrument issued by the startup in exchange for investor cash. It carries a contractual right to deliver equity shares upon a future trigger event (typically a priced equity round), with no interest accrual and no fixed repayment date.

Singapore-incorporated companies applying SFRS(I) must evaluate SAFEs under SFRS(I) 1-32 and SFRS(I) 9 to determine whether the instrument is:

- An equity instrument

- A financial liability

- A compound instrument with both components

A SAFE is not debt in the traditional sense—no maturity date, no interest—but it is not straightforward equity either. It is a contingent equity instrument whose classification depends entirely on its contractual terms. Under SFRS(I), which is aligned with IFRS as issued by the IASB, classification follows the substance of the contractual arrangement. Commercial intent ("it functions like equity") carries no weight in this analysis.

How SAFEs Differ from Convertible Notes

A convertible note carries an embedded derivative and a debt host component requiring separation (bifurcation) under SFRS(I) 9. A SAFE typically lacks a debt host—no interest accrual, no maturity date. That structural difference does not make equity classification automatic under SFRS(I). Specific contractual features still control the outcome, evaluated term by term under SFRS(I) 1-32.

Factors That Influence SAFE Accounting Classification

Specific contractual features drive the classification decision:

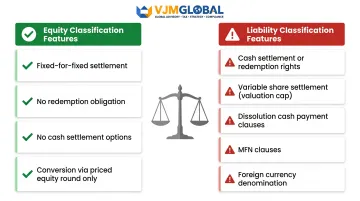

Features pointing toward equity classification:

- Fixed-for-fixed settlement (fixed cash amount converts to fixed number of shares)

- No redemption obligation

- No cash settlement options

- Conversion triggered solely by a future priced equity round

Features pointing toward liability classification:

- Cash settlement options or redemption rights

- Variable share settlement (e.g., conversion based on valuation cap producing indeterminate share count at issuance)

- Dissolution clauses requiring cash payment

- MFN (most-favoured-nation) clauses adjusting terms dynamically

- USD-denomination when functional currency is SGD

Most Singapore SAFE structures—post-money YC-style SAFEs with valuation caps and no cash redemption—will typically qualify for equity classification. However, a full review of the specific terms is required before reaching that conclusion. Any single liability-pointing feature can shift the entire classification.

Equity vs. Liability Classification Under SFRS(I)

SFRS(I) 1-32 provides the classification framework: a financial instrument is an equity instrument only if it contains no contractual obligation to deliver cash or another financial asset, and if it will be settled by exchanging a fixed amount of cash for a fixed number of the entity's own equity shares.

This is known as the "fixed-for-fixed" test.

Applying the Fixed-for-Fixed Test to SAFEs

A SAFE with a valuation cap does not convert into a fixed number of shares at inception. The share count is determined only at the conversion date based on the then-applicable valuation.

According to IFRIC guidance, instruments with caps and floors on conversion numbers typically fail the fixed-for-fixed test because neither the amount of cash nor the number of shares is truly fixed.

Some practitioners take the view that if conversion mechanics result in a fixed monetary amount converting into a variable (but determinable) number of shares denominated in the entity's functional currency, equity classification may still be appropriate. Given how much turns on the specific wording of each SAFE, founders should obtain a written accounting opinion tailored to their instrument before finalising the books.

Liability Classification: When and What It Means

A SAFE must be classified as a financial liability when it contains:

- A redemption clause (investor can claim back investment upon dissolution)

- A cash settlement alternative

- Terms that fail the fixed-for-fixed test

When liability classification applies, the SAFE is initially recognised at fair value — typically the cash received. At each subsequent reporting date, it must be remeasured at fair value with changes recognised in profit or loss (FVTPL) under SFRS(I) 9.

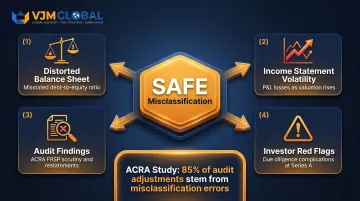

This creates income statement volatility that equity classification avoids. Counterintuitively, as the startup's valuation increases (bringing conversion closer to the cap), the SAFE liability's fair value increases, producing a loss in the income statement.

That misclassification risk is not theoretical. ACRA's January 2022 study of 412 Singapore-listed companies found 22,051 proposed audit adjustments totalling $78,670 million — with factual and misclassification errors accounting for 85% of all adjustments. Getting the classification wrong on a SAFE can trigger restatements, qualified audit opinions, and scrutiny from regulators at precisely the moment a startup least needs it.

Compound Instruments

Some SAFEs may be compound instruments (part equity, part liability), requiring split accounting under SFRS(I) 1-32. The equity component is recognised in other reserves, and the liability component is measured at amortised cost or FVTPL.

How SAFEs Are Recorded and Disclosed in Singapore

Once classification is determined, founders and their accountants must apply consistent journal entries, balance sheet presentation, and financial statement disclosures.

Initial Recognition: Recording the Cash Received

Journal entry when SAFE proceeds are received:

If equity-classified:

Debit: Cash/Bank

Credit: SAFE Instrument – Other Equity Reserves

If liability-classified:

Debit: Cash/Bank

Credit: Financial Liability at FVTPL

SAFEs require no interest accrual entries after recognition — unlike convertible notes — which simplifies periodic bookkeeping. However, if classified as a liability at FVTPL, fair value remeasurement entries are required at each reporting date.

Balance Sheet Presentation

Equity-classified SAFEs:

- Appear as a separate line item within equity

- Typically below share capital and share premium

- Clearly labelled (e.g., "Proceeds from SAFE instruments pending conversion")

- Helps readers understand these funds are not yet converted to shares

Liability-classified SAFEs:

- Appear under non-current or current liabilities (depending on expected conversion timing)

- Require separate disclosure of fair value and key contractual terms in the notes

When the SAFE eventually converts, the balance sheet entries above are reversed and replaced with the appropriate equity components.

At Conversion: Recording the Equity Conversion

Journal entry upon a priced equity round (the trigger event):

Debit: SAFE Instrument / Equity Reserve (or Financial Liability)

Credit: Share Capital (for par value of shares issued)

Credit: Share Premium (for excess over par value)

This completes the instrument's lifecycle. If the SAFE was classified as a liability at FVTPL, any gain or loss from fair value remeasurement up to the conversion date flows through profit or loss before reclassification.

Disclosure Requirements Under SFRS(I) 7

SFRS(I) 7 (Financial Instruments: Disclosures) requires Singapore companies to disclose:

- Nature and terms of outstanding SAFEs

- Accounting policies applied (equity vs. liability and the basis for that judgement)

- Carrying amounts by measurement category

- Significant assumptions used in fair value measurement

For startups preparing for Series A or institutional investors, accurate SAFE accounting and transparent disclosures are essential for due diligence. Engaging advisors with cross-border accounting experience — particularly those familiar with SFRS(I) requirements — can prevent costly restatements when investor scrutiny intensifies.

Key Accounting Properties That Affect SAFE Classification

Specific SAFE terms directly determine the accounting outcome. The three most consequential properties are the valuation cap structure, dissolution/redemption clauses, and conversion currency.

Valuation Cap and Its Accounting Implication

A valuation cap sets a maximum conversion valuation, effectively creating a variable conversion ratio. The number of shares delivered depends on which is lower—the cap-derived price or the actual round price.

IFRIC guidance confirms that instruments with caps and floors on conversion numbers are classified as liabilities because the number of shares to be exchanged is not truly fixed.

The cap itself does not automatically cause liability classification, but it affects the share count at conversion. Accountants must assess whether the cap introduces a variable settlement feature that fails the fixed-for-fixed test.

Dissolution and Redemption Clauses

Any clause giving the investor a right to receive their investment back in cash (for example, upon winding-up before a priced round) creates a contractual obligation to deliver cash, typically mandating liability classification.

SFRS(I) 1-32 paragraph 25(b) provides a narrow exception: if the issuer can be required to settle only in the event of liquidation, the entity may retain equity classification for that instrument. However, broader triggers (change of control, time-based) will not qualify for this exception.

Founders drafting SAFEs with redemption triggers beyond liquidation should expect liability classification from day one.

Conversion Currency and Functional Currency Considerations

Beyond dissolution terms, the currency in which a SAFE is denominated introduces a third classification risk. For Singapore-based startups raising SAFEs in USD, the functional currency question has direct accounting consequences.

If the entity's functional currency is SGD but the SAFE is USD-denominated, the fixed-for-fixed test is automatically failed. A fixed amount of foreign currency does not constitute a fixed amount of cash in the entity's functional currency (except for pro-rata rights issues).

The IFRIC November 2009 staff paper confirms this treatment. USD-denominated SAFEs issued by SGD-functional-currency entities will generally be classified as financial liabilities, requiring foreign exchange remeasurement at each reporting date.

Misclassification Risks and Common Misconceptions About SAFE Accounting in Singapore

Most Common Misconception

Founders and some accountants assume that because a SAFE is "not a loan" it must be equity. Under SFRS(I), however, the absence of interest and maturity does not determine classification—contractual settlement terms do.

Audit and Compliance Risk

If a SAFE is misclassified as equity when it should be a liability (or vice versa):

- Debt-to-equity ratio is misstated

- Net asset value is incorrect

- Profit/loss figures are wrong

This creates findings during statutory audit, potential ACRA-related issues during filing, and red flags for Series A investors reviewing historical financials.

ACRA's fourth FRSP report concluded that "knowledge gap and insufficient due diligence remain the main root causes contributing to material non-compliances with accounting standards."

ASA vs. SAFE Accounting

Misclassification risk extends beyond SAFEs alone. Some founders assume that an ASA (Advance Subscription Agreement), a structurally similar instrument more commonly used in the UK, is identical to a SAFE for accounting purposes.

ASAs and SAFEs are separate legal documents with different terms. The accounting treatment for each must be evaluated independently under SFRS(I) based on their specific provisions.

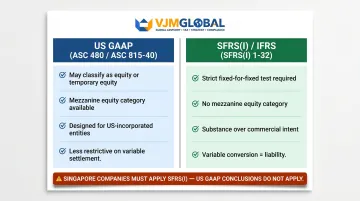

US GAAP vs. SFRS(I) Divergence

Singapore-incorporated entities must not apply US GAAP guidance — specifically ASC 480 or ASC 815-40 — to SAFE accounting. The frameworks are materially different.

KPMG confirms that "many instruments classified as a financial liability under IFRS could be classified as equity or temporary equity under US GAAP." Singapore companies use SFRS(I)/IFRS, which has a materially different classification framework, and the conclusions may differ significantly.

The Y Combinator SAFE was designed for US-incorporated entities under US GAAP. Cooley offers a Singapore-specific SAFE generator, but adapting the legal form does not resolve the accounting classification question.

Each startup must perform its own first-principles analysis under SFRS(I) — or engage professional advisors — before recording a SAFE on its balance sheet.

Frequently Asked Questions

How do you account for SAFEs in Singapore?

SAFEs are accounted for under SFRS(I) 1-32 and SFRS(I) 9. Proceeds are recognised initially as either an equity reserve or a financial liability depending on whether the instrument passes the fixed-for-fixed test and contains no cash settlement obligation. Upon conversion, the balance is reclassified into share capital and share premium.

How does a SAFE agreement work in Singapore?

A SAFE allows Singapore startups to raise capital now without setting a valuation. Investors receive the right to convert their investment into equity shares at a future priced round or liquidity event, using conversion mechanics such as a valuation cap or discount rate.

Is an ASA the same as a SAFE in Singapore?

No. An ASA (Advance Subscription Agreement) originates from UK practice and serves a similar commercial purpose, but it is a distinct legal document with its own terms. Accounting treatment under SFRS(I) must be evaluated independently for each instrument.

Are SAFEs classified as equity or liabilities under SFRS(I) in Singapore?

SAFEs can be classified as either equity or financial liabilities depending on their contractual terms—specifically whether they include cash settlement rights or fail the fixed-for-fixed test. Professional judgement is required for each SAFE agreement based on its specific provisions.

What happens to the accounting entries when a SAFE converts to equity in Singapore?

At conversion, the SAFE balance (whether held in equity reserves or as a liability) is debited, and the corresponding credit is made to share capital and share premium. This transfers the instrument from its interim classification into permanent equity.

What are the disclosure requirements for SAFEs in Singapore financial statements?

Under SFRS(I) 7, companies must disclose the nature and terms of outstanding SAFEs, the accounting policy and classification basis, carrying amounts, and any significant fair value assumptions.

If the questions above apply to your situation, VJM Global's accounting team can help ensure your SAFE instruments are classified correctly under SFRS(I) from day one. Reach out at info@vjmglobal.com to discuss your specific SAFE structure and accounting needs.