The people launching these businesses span a wide range: professionals leaving employment, Indian and international entrepreneurs entering the UK market remotely, NRIs building cross-border ventures, and side-hustlers turning an income stream into a proper company.

This guide covers what to expect, how to choose the right structure, what legal steps are required, and what ongoing compliance obligations follow once you're trading.

Key Takeaways

- UK company registration moves quickly: standard online incorporation typically completes in 24 hours

- Choosing the wrong business structure creates avoidable tax and liability problems later

- The current VAT registration threshold is £90,000 — many older sources still cite the outdated £85,000 figure

- Non-UK residents can register a UK limited company, though a registered UK address is mandatory

- Compliance obligations begin from day one of trading, not when you first turn a profit

What to Know Before You Start

Registering a UK company is straightforward — the compliance that follows demands more sustained attention.

Most first-time founders underestimate the ongoing administrative load: annual accounts, tax returns, confirmation statements, VAT returns if applicable, and PAYE if you hire. These are not optional and missed deadlines carry financial penalties.

Before those penalties become a reality, it helps to go in with realistic expectations:

- Income timeline: Most SMEs take 6–18 months to generate consistent revenue. Plan your personal runway accordingly.

- Admin load: Even a one-person limited company requires annual accounts, a confirmation statement, and a Corporation Tax return every year.

- Solo vs. supported: Decide early whether you'll manage compliance yourself or bring in external support — trying to learn accounting and run a business simultaneously is a common early-stage mistake.

Note: UK compliance obligations begin the moment you start trading, regardless of whether you're generating revenue yet.

Business Structures Available in the UK

Three primary structures cover the vast majority of UK businesses. Each carries different consequences for liability, tax, and administration.

Sole Trader

The simplest option. You and the business are legally the same entity, which means unlimited personal liability for any debts the business incurs.

- Register via HMRC Self Assessment (required if self-employment income exceeds £1,000 in a tax year)

- Requires a National Insurance number

- Minimal admin: one annual Self Assessment tax return

- Best suited to freelancers, consultants, and anyone testing an idea before committing to a formal structure

Limited Company (Ltd)

A legally separate entity from its directors and shareholders. Your personal assets are protected from business liabilities, capped at what you've invested.

Requirements to register:

- At least one director (no UK residency required)

- Shareholders or guarantors

- A registered UK office address

- A Standard Industrial Classification (SIC) code

- Memorandum and articles of association

- Statement of capital

- Identity verification for directors and people with significant control (PSC)

More admin than a sole trader, but stronger liability protection and better tax planning options.

Partnership and LLP

- Ordinary partnerships: Two or more people sharing profits and personal liability — registered with HMRC, minimal setup

- Limited Liability Partnerships (LLPs): A separate legal entity combining partnership flexibility with limited liability protection; registered with Companies House, requires at least two designated members

LLPs are common in professional services — accountancy firms, law practices, consultancies.

Each structure suits different risk profiles, growth ambitions, and admin tolerances. Here's how they compare:

Which Structure Is Right for You?

| Sole Trader | Limited Company | LLP | |

|---|---|---|---|

| Personal liability | Unlimited | Limited | Limited |

| Tax filing | Self Assessment | Corporation Tax + personal | Self Assessment per member |

| Admin burden | Low | Medium–High | Medium |

| Best for | Freelancers, micro-businesses | Growth-focused ventures | Multi-founder professional firms |

For most first-time founders, the choice comes down to sole trader (simple, low cost, but full personal liability exposure) versus limited company (more structure, stronger liability protection, and easier access to outside investment).

How to Start a Business in the UK — Step by Step

Step 1: Validate Your Idea

Before registering anything, confirm that real customers will pay at the price point your model requires.

- Talk to at least 10–15 potential customers before building

- Review what competitors charge and how they acquire customers

- Assess whether the UK market is large enough and accessible enough to sustain the business

Avoid: Registering a business and building a product before confirming paying demand exists.

Step 2: Write a Business Plan

It doesn't need to be lengthy, but it must cover:

- What the business does and the problem it solves

- Target market and competitive landscape

- Pricing and revenue model

- Operational plan (how you'll deliver)

- 12-month cash flow forecast

The cash flow forecast matters most. More early-stage businesses fail from running out of cash than from having a bad idea.

Step 3: Register Your Business

For a limited company:

- Choose a unique company name — check availability on the Companies House register

- Set up a UK registered office address (mandatory — must be a physical UK address)

- Register online at Companies House — standard processing takes 24 hours, costs £100; same-day incorporation via software costs £156

- Register for Corporation Tax with HMRC within 3 months of starting to trade

For a sole trader: Notify HMRC by registering for Self Assessment online. HMRC typically processes the registration within a few days.

Non-UK residents: Directors do not need to live in the UK. You will need a registered UK address and must satisfy Companies House identity verification requirements. Accepted documents include biometric or machine-readable passports and PRADO-listed documents (the EU's register of accepted government-issued identity documents).

Step 4: Set Up Business Finances

Open a dedicated business bank account before you start taking revenue. Mixing personal and business finances creates accounting complications and makes tax returns harder to prepare accurately.

Bank options:

- Traditional: Barclays, HSBC, NatWest, Lloyds

- Digital: Starling (UK residents only), Tide (directors of UK-registered companies may apply), Revolut Business (applicants resident in UK, EEA, US, Australia, Singapore, or India)

- Eligibility criteria vary by provider — non-residents should check requirements directly with each bank before applying

Once your account is open, map out your funding options. Early-stage UK businesses have several routes:

- Start Up Loans (British Business Bank): £500–£25,000 per person; requires UK residence and right to work in the UK

- Government grants: search Find a Grant and Innovate UK's funding portal — non-repayable but competitive

- Angel investors and VCs: equity in exchange for capital

- Crowdfunding platforms: Kickstarter, Seedrs, Crowdcube

Step 5: Build Your Brand and Go to Market

Foundation steps before spending on marketing:

- Secure your domain name and set up a professional business email

- Build a functional website (not elaborate — just credible)

- Create a Google Business Profile and LinkedIn presence

- Identify one primary acquisition channel — the route through which your first paying customers will find you

Common miss: Launching without a clear route to customers, then spending on broad marketing before a single channel has been proven.

Tax and Compliance Obligations for UK Businesses

Once you start trading, compliance obligations apply immediately — regardless of business size or profitability.

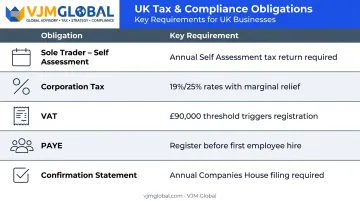

Tax Registration and Obligations

| Obligation | What's Required |

|---|---|

| Sole trader | Register for Self Assessment; notify HMRC by 5 October following the tax year |

| Limited company – Corporation Tax | Register with HMRC within 3 months of starting to trade; rate is 19% on profits up to £50,000, 25% above £250,000, with marginal relief between |

| VAT | Mandatory registration when taxable turnover exceeds £90,000 in the previous 12 months, or is expected to exceed that in the next 30 days |

| PAYE | Register before employing your first member of staff |

| Confirmation statement | Filed at least once every 12 months with Companies House |

Licences, Permits, and Industry Requirements

Not every business needs a licence — but many do. Food businesses, alcohol retailers, financial services firms, childcare providers, and street traders all face additional requirements.

Use the GOV.UK Find a licence tool to check what applies to your specific business activity and local authority area.

Business Insurance

- Employers' liability insurance: Legally required the moment you employ anyone — minimum cover of £5 million from an authorised insurer

- Public liability insurance: Not legally required in most sectors, but strongly recommended if customers visit your premises or you work at theirs

- Professional indemnity insurance: Recommended for consultants, advisors, and any business providing professional services

Operating without required employers' liability cover carries a fine of up to £2,500 per day.

Getting Support with Ongoing UK Compliance

Managing confirmation statements, annual accounts, Corporation Tax deadlines, and VAT returns requires consistent attention. For founders with cross-border operations — particularly those with shareholders, directors, or activities in India — the picture becomes more complex.

Cross-border obligations typically include:

- DTAA compliance: Double Taxation Avoidance Agreement obligations between the UK and India

- FEMA requirements: Regulatory compliance for investment flows into or out of India

- Transfer pricing: Documentation and reporting for transactions between related entities

VJM Global has worked with UK-based businesses navigating these obligations, providing support across international tax planning, cross-border accounting, and multi-jurisdiction advisory. For businesses managing both UK and Indian requirements, a single advisory team that understands both regulatory environments helps avoid errors and missed filing deadlines across both jurisdictions.

Conclusion

Starting a business in the UK is more accessible than most founders expect. Registration is fast, costs are modest, and the market is well-developed. That doesn't make building a successful business easy, but the barriers to entry are lower here than in most comparable economies.

The founders who struggle tend to skip the foundational work:

- Skipping demand validation before committing time and money to building

- Choosing a business structure without thinking through tax and liability implications

- Treating compliance as something to sort out later (it rarely gets easier)

The ones who succeed plan carefully, stay compliant from day one, and adjust based on what the market actually shows them — not what they expected it to say.

Frequently Asked Questions

Can I start a business in the UK as a foreigner?

Yes. Non-UK residents can register and direct a UK limited company without living in the UK. You'll need a registered UK office address and must satisfy Companies House identity verification requirements. Business registration rights are separate from visa or immigration status.

How much does it cost to open a business in the UK?

Online registration with Companies House costs £100 (same-day incorporation via software is £156). Beyond that, budget for business insurance, a registered address service if needed, accounting software, and potentially professional advisory fees. Total setup costs vary significantly by industry and business type.

What business can I start with £5,000 in the UK?

£5,000 comfortably covers many service-based or digital businesses: consultancy, freelancing, tutoring, e-commerce, cleaning, or digital marketing. Overheads in these models are low, with the primary investment being time and expertise rather than stock or premises.

How long does it take to register a company in the UK?

Standard online registration with Companies House typically processes within 24 hours. Same-day incorporation is available for £156. Sole trader registration with HMRC can be completed online and usually takes a few days to process.

Do I need a UK bank account to start a business in the UK?

A dedicated UK business account isn't legally required for all structures, but it is practically necessary. It simplifies accounting, VAT, and tax records considerably. Digital banks have made it easier for non-residents to apply, though eligibility varies by provider — check current requirements directly.

What taxes does a new UK business need to pay?

The main obligations depend on your structure. Sole traders pay Income Tax and National Insurance via Self Assessment. Limited companies pay Corporation Tax (19% up to £50,000; 25% above £250,000), and must register for VAT once turnover exceeds £90,000. Employers also need to register for PAYE before taking on staff.