Introduction

The UK has become one of the more accessible international markets for Indian entrepreneurs. Company formation is fast, the legal system is transparent, English is the working language, and Indian nationals face no residency requirement to incorporate. You can register a UK private limited company from India in as little as 24 hours.

That ease at registration doesn't extend to the full setup. Indian entrepreneurs face a compliance layer that UK-based founders simply don't:

- FEMA regulations governing outbound capital transfers from India

- Cross-border tax obligations under the UK-India Double Taxation Avoidance Agreement (DTAA)

- UK banking requirements that can take weeks to clear as a non-resident

This guide covers the complete picture: choosing a structure, filing with Companies House, handling FEMA and HMRC obligations, and navigating visa options — written specifically for someone starting from India.

Key Takeaways

- Indian nationals can register a UK private limited company remotely via Companies House for £100, with incorporation typically confirmed within 24 hours.

- No UK-resident director or local partner is required — you can serve as sole director from India.

- The full setup (banking, HMRC registration, FEMA compliance) typically takes 4–8 weeks beyond incorporation.

- Managing a UK company from India requires structuring under both the UK-India DTAA and FEMA's Overseas Direct Investment (ODI) rules — getting this right protects you on both sides.

- A UK visa is only needed if you plan to physically live and work in the UK — not to incorporate or manage the company remotely.

Why the UK Is a Strategic Market for Indian Entrepreneurs

The UK-India trade relationship is substantial. According to the UK Department for Business and Trade's 2026 India factsheet, total trade in goods and services reached £47.9 billion in the four quarters to end of Q4 2025 — making India the UK's 11th largest trading partner.

The ONS Census 2021 recorded 920,000 India-born usual residents in England and Wales alone. That diaspora creates real commercial demand across food, retail, professional services, and technology — demand that Indian entrepreneurs are well-placed to serve.

The UK has also signed trade agreements with 72 countries and territories, giving UK-registered businesses access to markets far beyond Europe. For Indian entrepreneurs, a UK entity opens doors that a purely India-based structure cannot.

Where the Friction Lies

That said, honest expectations matter. The registration itself is fast. The complications arise after incorporation:

- FEMA compliance — capital transferred from India to fund a UK company must follow the RBI's Overseas Direct Investment (ODI) framework or Liberalised Remittance Scheme (LRS), depending on the amount and transaction type

- UK banking — traditional banks often require in-person verification for non-resident directors; digital alternatives exist but come with their own caveats

- Dual tax obligations — an Indian tax resident earning income from a UK company must manage HMRC filings in the UK and income disclosure in India, with the DTAA governing how income is treated across both

Business Structures in the UK: Which One Is Right for You

The structure decision shapes everything — liability exposure, tax treatment, filing obligations, and how the business scales. For Indian entrepreneurs, that decision comes down to four realistic options, each with distinct trade-offs.

| Structure | Setup | Liability | Tax Treatment | Best For |

|---|---|---|---|---|

| Sole Trader | HMRC registration only | Unlimited personal | Income tax on profits | Freelancers testing the UK market |

| Private Limited (Ltd) | Companies House filing | Limited | UK Corporation Tax (19%–25%) | Scalable UK businesses |

| LLP | Companies House filing | Limited | Pass-through (partners taxed individually) | Professional services, joint ventures |

| Branch / Overseas Establishment | Form OS IN01, £124 | Full parent liability | Profits taxed as part of parent company | Established Indian companies expanding |

Why Most Indian Entrepreneurs Choose Private Limited (Ltd)

The vast majority of Indian entrepreneurs setting up in the UK use the private limited company structure. It creates a separate legal entity, limits your personal liability, and is the structure most UK banks, clients, and investors expect to deal with.

UK Corporation Tax rates are currently:

- 19% on profits up to £50,000

- 25% on profits above £250,000

- Marginal Relief applies between £50,000 and £250,000

Other Structures Worth Knowing

- Sole Trader: Requires only HMRC self-assessment — no Companies House filing. Zero separation between personal and business finances means unlimited personal liability. Suitable for low-risk, low-revenue consulting work.

- LLP: Requires at least two partners; files accounts publicly with Companies House. Common for professional services firms like accountancy or legal practices.

- Branch Office: Best for an Indian company that is already operational and wants UK presence without creating a new entity. The parent company retains full liability for UK operations.

How to Start a Business in the UK from India – Step by Step

Each step below is manageable when you know what to expect. The process becomes complicated only when entrepreneurs skip preparation — particularly around banking and FEMA compliance.

Step 1 – Choose Your Company Name and Check Availability

The name must be unique and comply with Companies House naming rules — no names identical or overly similar to existing registered companies. Certain terms (such as "Royal," "International," or "Bank") require prior approval.

Check availability using the Companies House name availability checker before filing. Name reservation happens as part of the incorporation submission — there is no separate pre-reservation process.

Step 2 – Appoint a Director and Arrange a UK Registered Office Address

At least one director is required. There is no legal requirement for that director to be a UK resident — an Indian national can serve as sole director from India.

However, a physical UK registered office address is mandatory. A Royal Mail PO Box does not qualify. Indian entrepreneurs without a UK presence typically use a registered office service or virtual office provider to satisfy this requirement. This is a common, well-established solution and costs between £50–£150 per year depending on the provider.

Step 3 – File for Incorporation with Companies House

Submit your application through the GOV.UK Companies House portal. You'll need to provide:

- Company name and registered office address

- Director details (including identity verification)

- Shareholder information

- Memorandum and articles of association

- £100 online registration fee

Incorporation is typically confirmed within 24 hours online. You'll receive a Certificate of Incorporation and a Companies Registration Number (CRN). Indian entrepreneurs who want guided support through this filing — including document preparation and submission — typically work with a cross-border advisory firm familiar with both Companies House requirements and Indian regulatory context.

Step 4 – Register for HMRC Taxes

After incorporation, HMRC automatically sends a 10-digit Unique Taxpayer Reference (UTR) to your registered office address within a few weeks. Use this to register for corporation tax — you must do so within 3 months of starting to trade.

On VAT:

- Compulsory registration when taxable turnover exceeds £90,000 in the previous 12 months

- If your business is not established in the UK, the threshold does not apply — you must register for VAT from the first taxable supply, regardless of value

- Voluntary registration before the threshold can be beneficial in B2B sectors where input VAT recovery matters

Step 5 – Open a UK Business Bank Account

This is consistently the most time-consuming step for non-resident Indian directors.

- Traditional UK banks (Barclays, HSBC, NatWest) may require in-person verification and can take several weeks to process accounts for non-residents

- Digital alternatives are widely used as a starting point:

- Tide — accepts UK-registered limited company directors not based in the UK (note: requires a UK mobile number and UK App Store access)

- Airwallex — FCA-regulated e-money institution that supports online onboarding without UK residency; useful for international payments and multi-currency accounts

- Starling Bank — does not accept non-resident directors; all directors and PSCs must be UK residents

A dedicated business account is required before the company can receive revenue, pay expenses, or meet HMRC compliance expectations.

Step 6 – Handle FEMA Compliance for Capital Transfer from India

If you're transferring money from India to fund your UK company — paying for setup costs, injecting share capital, or covering early operating expenses — this must comply with FEMA.

The relevant frameworks depend on the nature and amount of the transfer:

- Overseas Direct Investment (ODI) route — applicable when subscribing to shares in a foreign entity (including a newly incorporated UK company). Must be handled through an authorised dealer bank in India.

- Liberalised Remittance Scheme (LRS) — permits resident individuals to remit up to USD 250,000 per financial year for permitted current or capital account transactions. Relevant for smaller operational transfers.

FEMA non-compliance is among the costliest oversights Indian entrepreneurs make when setting up abroad — penalties can reach three times the amount involved. Getting the ODI structuring and authorised dealer coordination right from the start matters. VJM Global's cross-border advisory team handles this specifically for Indian entrepreneurs setting up in the UK, covering ODI filings, RBI compliance, and authorised dealer coordination.

Tax, Compliance, and Cross-Border Obligations

Running a UK company as an Indian tax resident creates a dual-compliance obligation. The UK company has its own HMRC obligations. You, as an Indian resident, must also account for foreign-sourced income in India.

The UK-India DTAA: What It Actually Does

The UK-India Double Taxation Convention, in force since 1993, prevents the same income from being taxed in full in both countries. The practical implications for Indian directors of UK companies:

- Dividends (Article 11): India retains primary taxing rights on dividends from a UK company paid to an Indian resident. UK withholding tax may also apply depending on treaty provisions and whether you hold beneficial ownership of the income.

- Director's fees (Article 17): Remuneration earned as a board member of a UK-resident company is taxable in the UK. Treaty relief is available but requires supporting documentation filed in both jurisdictions.

Claiming DTAA benefits is not automatic — it requires correct filings in both the UK (HMRC) and India (Income Tax Return, including Schedule FA for foreign assets and Schedule FSI for foreign-source income).

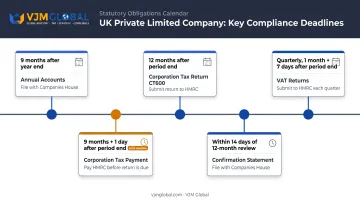

UK Compliance Calendar for a Private Limited Company

| Obligation | Deadline |

|---|---|

| Annual accounts — Companies House | 9 months after financial year end |

| Corporation Tax return (CT600) | 12 months after accounting period end |

| Corporation Tax payment | 9 months and 1 day after accounting period end |

| Confirmation statement | Within 14 days of the 12-month review period ending |

| VAT returns (if VAT-registered) | Quarterly; due 1 month and 7 days after period end |

First-time filers commonly miss the Corporation Tax payment deadline — which falls before the return deadline. Missing it triggers automatic interest charges.

VJM Global's Chartered Accountants and CPAs handle both sides of this equation — UK-side HMRC compliance and India-side DTAA filings that most UK accountants won't touch.

Visa Routes for Indian Entrepreneurs Planning to Relocate

To be clear: incorporating a UK company from India does not require a UK visa. Directors do not have to live in the UK, and registration can be completed entirely online. A visa is only necessary if you intend to physically live and work in the UK.

Primary Routes for Indian Founders

Innovator Founder Visa

- For entrepreneurs with an innovative, scalable business idea, vetted by an approved endorsing body

- Application fee from outside the UK: £1,357 per person

- Endorsement fee: £1,000 (excluding VAT)

- Personal funds requirement: at least £1,270 held in a bank account for 28 consecutive days before applying

- Post-approval checkpoint meetings with your endorsing body are required to maintain visa status — each costs £500

Global Talent Visa

- Targets recognized experts in digital technology, research, or the arts — no specific business idea required

- Total fee: £766 (split between £561 for endorsement and £205 for the visa itself)

- Qualifying criterion is demonstrated recognition of existing expertise, not a business plan

India Young Professionals Scheme

- For Indian nationals aged 18–30 with a bachelor's degree (RQF Level 6 or above)

- Requires £2,530 in savings held for at least 28 consecutive days

- 3,000 places available in 2026, allocated via ballot

- Application fee: £340, plus £1,552 healthcare surcharge (£1,892 total)

Planning Your Timeline

Visa approval and endorsement processes add substantial lead time. Budget a 3–6 month runway between starting the visa process and your planned operational launch in the UK. Use that window productively:

- Research and approach endorsing bodies early — shortlisting takes 2–4 weeks alone

- Open a UK business bank account in parallel with your visa application

- Register your company with Companies House so it's active when you arrive

Conclusion

Starting a UK business from India is genuinely achievable. Company formation is fast, the legal framework is straightforward, and Indian nationals face no residency hurdle to incorporate. The complications are real — and most are avoidable when you address them before incorporation, not after.

The India-specific compliance layer — FEMA requirements for capital transfers, DTAA structuring between UK and Indian tax obligations, and HMRC registration timing — is where most founders either get things right or create problems that are expensive to unwind later.

Founders who navigate this well treat cross-border compliance as a core part of setup — not a loose end to tidy up once revenue arrives. Working with advisors who understand both UK company law and Indian regulatory requirements reduces the risk of costly errors on either side. VJM Global's team handles exactly this intersection: FEMA advisory, DTAA structuring, and UK business setup support for Indian founders and businesses.

Frequently Asked Questions

Can an Indian national start a business in the UK?

Yes. Indian nationals can legally register a UK private limited company from India without being a UK resident. No UK-based director or local partner is required. The only requirement is a valid physical UK registered office address.

How much does it cost to start a business in the UK?

The Companies House online registration fee is £100. Additional costs typically include a registered office service (£50–£150/year) and bank account setup. Operational costs vary significantly depending on your sector and whether you have UK staff.

How much bank balance is required for a UK business visa?

For the Innovator Founder Visa, applicants must show at least £1,270 in savings held for 28 consecutive days. The India Young Professionals Scheme requires £2,530 under the same conditions. These are personal funds requirements, separate from any business capital.

Do I need to be physically present in the UK to register and run a company?

No. Physical presence is not required for registration, and remote operation is possible. However, physically conducting business in the UK — employing staff, managing on-the-ground operations, meeting clients — requires an appropriate UK visa.

What taxes does an Indian entrepreneur pay on a UK business?

The UK company pays Corporation Tax on profits (19%–25% depending on profit level), plus VAT if turnover exceeds £90,000. As an Indian tax resident, the UK-India DTAA governs how dividends or director remuneration are taxed across both countries. A cross-border tax advisor should review your structure before you begin.