Three questions come up consistently: Do I need to relocate? Which structure works for a non-resident? How do cross-border taxes actually function? This guide answers each one directly, walking through every practical step — from choosing a structure to opening a bank account — built specifically for founders operating from Singapore.

Key Takeaways

- Singapore residents can register and own a UK limited company entirely online — no residency requirement for directors or shareholders

- A Private Limited Company (Ltd) is the correct structure; sole trader registration is not viable from Singapore

- Companies House online registration costs £100 and typically completes within 24 hours

- The UK-Singapore Double Taxation Agreement prevents double taxation on dividends, interest, and royalties

- Three annual obligations apply: Confirmation Statement, statutory accounts, and Corporation Tax return — all filed remotely

Why Singapore Entrepreneurs Are Looking to the UK

The UK's company formation environment has no minimum share capital requirement and imposes no director residency rules. Companies House recorded 801,864 new incorporations in the financial year ending March 2025, with 14,574 overseas companies maintaining a UK establishment. That incorporation volume points to sustained commercial demand from international founders, not just administrative activity.

Sectors Worth Noting

Enterprise Singapore's UK market guide flags six sectors with strong entry potential for Singapore businesses:

- Fintech: the UK runs one of the most developed regulatory sandboxes globally, making it easier to test financial products before full launch

- Digital technology — London consistently ranks among Europe's top tech hubs

- E-commerce: a mature consumer market with established payment infrastructure and high digital adoption rates

- Green energy and sustainability — strong government procurement pipelines and net-zero commitments support new entrants

- Lifestyle retail: premium Singapore brands have demonstrated traction with UK consumers

Practical Operational Fit

Beyond sector opportunity, the setup genuinely suits Singapore founders:

- English is the business language in both markets, removing translation overhead from day-to-day operations

- Both jurisdictions use common law contract frameworks, which reduces friction when adapting Singapore agreements for UK use

- UK business hours overlap with European and Middle Eastern markets — useful for founders already running multi-region operations from Singapore

What to Know Before You Register a UK Business from Singapore

Before you file anything, four practical factors regularly catch Singapore-based founders off guard — visas, banking, address requirements, and tax residency.

Visas and Physical Presence

Registering and owning a UK company remotely does not require a visa. Directors of UK companies are not required to live in the UK. A visa only becomes necessary if you intend to physically work or operate from within the UK.

For founders who want to relocate, the Innovator Founder Visa is the most relevant route:

- Requires endorsement from an approved body

- Grants up to a 3-year stay, extendable

- No fixed minimum investment threshold, though applicants must demonstrate adequate funding to their endorsing body

The UK Banking Challenge

Traditional banks like Barclays and HSBC typically require in-person verification, which makes them impractical for non-resident founders. Digital banks are the realistic path:

| Bank | Non-Resident Eligible | Notes |

|---|---|---|

| Wise Business | Yes | Supports UK-incorporated businesses with overseas owners; identity verification typically 1–2 working days |

| Tide | Conditional | Directors may have overseas home address, but requires a valid UK mobile number |

| Starling | No | All PSCs and directors with account access must be UK residents |

Plan for 1–4 weeks to get a fully operational account, accounting for document review.

Registered Office Requirement

Every UK Ltd must have a physical UK address — not a PO Box — in the country where the company is registered. Since March 2024, PO Boxes are explicitly prohibited. Third-party registered office services fulfil this requirement, with costs starting from £39–£275 per year depending on location and whether mail forwarding is included. A London address will sit at the higher end.

You must also provide a registered email address at the point of incorporation (required since March 2024). It does not appear on the public register.

The Tax Residency Point Most Founders Miss

A UK-incorporated company is automatically UK tax resident by default. However, if the company is centrally managed and controlled from Singapore — meaning board-level strategic decisions are made there — HMRC's own guidance indicates that's relevant evidence for where tax residency actually sits.

This is not a loophole; it requires careful structuring. Before incorporating, get advice on the UK–Singapore double tax treaty and how your management arrangements affect residency determinations in both jurisdictions.

Choosing the Right UK Business Structure as a Non-Resident

Why Sole Trader Doesn't Work

A sole trader registration requires a UK National Insurance number, which can only be obtained by being physically present in the UK with the right to work. For a Singapore-based founder, this route is simply unavailable.

The Case for a Private Limited Company (Ltd)

A UK Ltd is the default and correct structure for non-residents. The practical reasons:

- Personal assets are legally separated from business liabilities

- Corporation Tax applies to company profits — not personal income tax rates

- Non-UK-resident directors and shareholders are fully permitted

- Stronger credibility with UK clients, suppliers, and banking partners

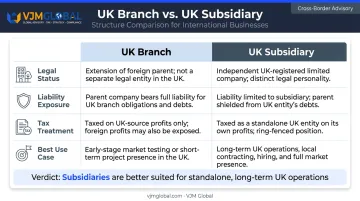

UK Branch vs. UK Subsidiary

If you already operate a registered Singapore company, two expansion options exist:

| UK Branch | UK Subsidiary | |

|---|---|---|

| Legal status | Extension of Singapore parent | Separate UK legal entity |

| Liability | Parent bears full liability | Ring-fenced from parent |

| Tax exposure | Worldwide profits may face UK scrutiny | Only UK-sourced profits taxable in UK |

| Best for | Testing the market short-term | Standalone UK operations |

Most Singapore founders choose the subsidiary structure to keep UK tax exposure contained to UK-sourced profits.

Director and Shareholder Requirements

Once you've settled on a UK Ltd subsidiary, incorporation requires meeting a few baseline conditions:

- At least one director (non-UK resident is acceptable)

- At least one shareholder — can be the same person, or a corporate entity

- Minimum share capital of £1 (no upper limit required)

How to Register a UK Company from Singapore — Step by Step

The entire process can be completed online without travelling to the UK. That said, common mistakes trip up founders at predictable points: skipping the registered address step before filing, underestimating banking timelines, and missing the Corporation Tax registration window.

Step 1 — Choose a Company Name and Secure a Registered Office Address

Name rules:

- Must be unique — check the Companies House register before committing

- Cannot be misleading or imply connections to government bodies

- Must end in "Limited" or "Ltd"

Secure your registered office address before you file — you need it on the incorporation form. Budget £39–£275/year depending on location.

Step 2 — Register with Companies House

Documents and information required:

- Memorandum of Association

- Articles of Association (model articles are acceptable for most new companies)

- Director details (name, date of birth, service address, country of residence)

- Shareholder details and Statement of Capital

- SIC code(s) — your industry classification

- People with Significant Control (PSC) information

- Registered office address and registered email address

Fees and timelines:

- Online registration: £100

- Same-day software filing: £156

- Standard processing time: 24 hours

On approval, you receive a Certificate of Incorporation confirming the company is legally established.

Step 3 — Register for Corporation Tax with HMRC

All UK Ltd companies must register for Corporation Tax within 3 months of starting to trade. "Starting to trade" includes providing services, earning interest, and managing investments — not just selling goods. You'll receive a Unique Taxpayer Reference (UTR) automatically after Companies House registration.

2025–2026 Corporation Tax rates:

| Profit Level | Rate |

|---|---|

| Under £50,000 | 19% (small profits rate) |

| £50,000 – £250,000 | Marginal relief applies |

| Over £250,000 | 25% (main rate) |

Step 4 — Open a UK Business Bank Account

For Singapore-based founders, digital banks are the accessible route. Two options worth considering:

- Wise Business — supports UK-incorporated companies with overseas owners, offers multi-currency accounts (useful for GBP-to-SGD transfers), and identity verification typically completes within 1–3 working days

- Tide — a workable alternative, though it requires a valid UK mobile number

VJM Global works with Singapore-based founders on cross-border business setup and compliance. Their team can assist with document preparation and entity structuring so the company is correctly set up from incorporation.

Step 5 — Register for VAT and PAYE (Where Required)

VAT: Mandatory once taxable UK turnover exceeds £90,000 (threshold as of 1 April 2024). Voluntary registration below the threshold is available — worth considering if you're selling B2B to VAT-registered UK clients, as it allows you to reclaim VAT on purchases.

PAYE: Required before your first payday if the company hires UK employees or if you pay yourself a salary through the UK company. You cannot register more than 2 months before you start paying people.

UK Tax, Compliance, and Ongoing Obligations for Singapore-Based Owners

The Three Annual Obligations

Every UK Ltd must meet three recurring filing requirements:

- Confirmation Statement — filed with Companies House at least once per year; £50 online (£110 paper)

- Annual Accounts — filed within 9 months of financial year-end; late penalties range from £150 (up to one month late) to £1,500 (over six months), and double if late two years running

- Corporation Tax Return — submitted to HMRC within 12 months of the accounting period end

All three can be managed remotely with proper accounting support. VJM Global's cross-border compliance services cover clients operating across multiple jurisdictions, so your UK filings sit cleanly alongside your Singapore reporting obligations.

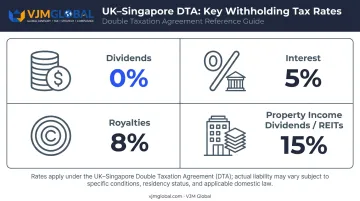

The UK-Singapore Double Taxation Agreement

The DTA between the UK and Singapore prevents the same income from being taxed in both countries. Key treaty rates:

| Income Type | Treaty Rate |

|---|---|

| Portfolio and direct investment dividends | 0% |

| Interest | 5% |

| Royalties | 8% |

| Property income dividends (REITs) | 15% |

For Singapore-based shareholders, dividends paid from a UK Ltd are generally subject to 0% UK withholding tax under this treaty. UK Corporation Tax still applies to the company's profits, but the dividend flow to Singapore is clean in most structures. Confirm the details with a cross-border tax adviser before finalising how you'll repatriate profits — treaty benefits depend on how ownership and residency are documented.

UK GDPR — Often Overlooked

If your UK company processes data from UK customers, UK GDPR applies regardless of where you're based. Core requirements:

- A privacy policy covering how customer data is collected and used

- Data processing agreements with any third-party vendors handling UK customer data

- A documented process for responding to data subject access requests

Frequently Asked Questions

How much money do I need to start a business in the UK?

Minimum share capital is £1, so there's no meaningful capital threshold. Practical first-year costs include the £100 Companies House registration fee, a registered office service (from £39/year), and banking setup. Budget approximately £500–£1,500 for the first year, including basic compliance support.

Can a foreigner start a business in the UK?

Yes. Non-UK residents and foreign nationals can register a UK limited company with no residency requirement for directors or shareholders. The entire incorporation process is completed online from Singapore.

Do I need to live in the UK to run a UK limited company?

No — many Singapore-based founders manage UK companies entirely remotely. You do need a UK registered address, and physical presence or decision-making patterns can affect UK tax residency under the central management and control rules.

Do I need a UK business bank account to operate a UK company?

Yes, practically speaking. A UK account is essential for receiving payments and demonstrating compliance. Wise Business and Tide are the most accessible options for non-UK-resident directors. Starling Bank requires UK residency.

What taxes does a non-resident-owned UK company pay?

UK Corporation Tax on UK-sourced profits (19%–25% depending on profit level), VAT once turnover exceeds £90,000, and PAYE if UK employees are hired. The UK-Singapore DTA shapes how dividends and other income flows back to Singapore-based shareholders.

How does the UK-Singapore Double Taxation Agreement work?

The DTA prevents income from being taxed in both the UK and Singapore. For standard dividends paid to a Singapore-based shareholder, the treaty rate is 0% UK withholding tax. Rates differ for royalty income and property gains, so structuring profit repatriation carefully matters.