Introduction

UK finance teams managing Indian subsidiaries face a critical challenge: India's audit season isn't simply a foreign version of familiar UK compliance. The framework is structurally different, with distinct deadlines, multiple concurrent audit obligations, and penalties that escalate quickly when mishandled.

Under Indian law, every company incorporated in India must undergo an annual statutory audit — including wholly-owned UK subsidiaries with zero revenue. The Indian financial year runs April 1 to March 31, and audit season creates a concentrated compliance window from April through September, culminating in the 30 September AGM deadline.

UK companies that treat this as a local formality handled entirely by the Indian team routinely miss critical cross-border documentation requirements that only HQ can provide. The consequences are concrete: ₹100 per day in uncapped late fees, up to ₹2 lakh in adjudication penalties, and potential five-year director disqualifications.

This guide is for UK-based companies operating Indian subsidiaries, branches, or liaison offices. It explains when India's audit season runs, what types of audits apply, what you must prepare, and what commonly goes wrong.

Key Takeaways

- India's financial year runs April 1 to March 31, with audit season spanning April–September and a statutory audit AGM deadline of 30th September

- Every Indian-registered entity must complete a statutory audit under the Companies Act, regardless of turnover or profitability—no UK group audit substitutes for this requirement

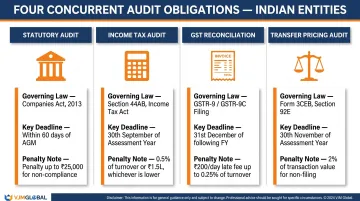

- UK companies face four concurrent obligations: statutory audit, income tax audit, GST reconciliation, and transfer pricing audit

- Audit readiness is year-round: maintain clean books monthly, reconcile GST returns, and keep transfer pricing documentation up to date

- UK HQ involvement is mandatory for success—intercompany agreements, transfer pricing studies, and board approvals all require active UK participation

How India's Audit System Differs From What UK Companies Are Used To

Fixed Financial Year and Separate Regulatory Framework

India's financial year runs April 1 to March 31 under both the Companies Act 2013 and the Income Tax Act 1961. While this coincidentally mirrors the UK tax year, private companies cannot change this period to align with a UK parent's calendar year. **Your UK statutory audit does not satisfy Indian compliance requirements**—Indian law requires a standalone audit conducted by an ICAI-registered Chartered Accountant and filed separately with the Registrar of Companies.

Under Section 141 of the Companies Act 2013, only practicing Chartered Accountants registered with the ICAI may serve as statutory auditors. UK-registered auditors — ICAEW or ACCA members — cannot sign off on Indian statutory audits, though they can coordinate with the Indian auditor for group consolidation.

Multi-Layer Audit Obligations

Unlike the UK where a single audit report satisfies most regulatory needs, Indian companies may simultaneously owe:

- Statutory audit under the Companies Act 2013

- Tax audit under Section 44AB of the Income Tax Act (if turnover thresholds are met)

- GST reconciliation via GSTR-9 and GSTR-9C (self-certified)

- Transfer pricing audit (Form 3CEB) for international transactions with related parties

Each carries distinct deadlines, prescribed forms, and penalty structures. Missing one triggers a cascade of compliance failures.

Cross-Border Complexity Unique to UK Subsidiaries

Transactions between the Indian entity and its UK parent must be documented at arm's length under India's transfer pricing regulations. This requires:

- Formal intercompany agreements for every transaction type (management fees, royalties, loans, shared services)

- Transfer pricing study justifying the pricing methodology

- Master File documentation if group revenue exceeds ₹500 crore

- Form 3CEB certification by a Chartered Accountant

FEMA/RBI compliance for foreign investment inflows must also be verifiable at audit through filings like FC-GPR, FC-TRS, and the annual FLA return. This level of cross-border coordination — between UK HQ, the Indian finance team, and multiple regulators — is where firms like VJM Global add the most practical value, managing the Indian compliance side so it doesn't fall entirely on the UK team to track.

Types of Audits UK Companies Must Complete in India

Operating in India means navigating four distinct audit requirements — each with its own deadlines, thresholds, and penalties. Here is what UK companies need to account for.

Statutory Audit (Companies Act 2013)

Every company incorporated in India — including wholly-owned UK subsidiaries, zero-revenue entities, and dormant companies — must undergo an annual statutory audit under Section 139 of the Companies Act 2013.

Key deadlines:

- AGM must be held by 30th September for March 31 year-end (Section 96)

- Form AOC-4 (audited financial statements) due 30 days post-AGM (Section 137)

- Form MGT-7 (annual return) due 60 days post-AGM (Section 92)

Penalties for non-compliance:

| Penalty Type | Amount | Basis |

|---|---|---|

| Additional fee (Section 403) | ₹ 100/day, uncapped | Automatic for late filing |

| Adjudication penalty (Sections 92(5)/137(3)) | Company: up to ₹ 2 lakh; Officers: up to ₹ 50,000 each | Enforcement action |

| Director disqualification (Section 164(2)) | 5-year ban from directorship | After 3 consecutive years of non-filing |

Income Tax Audit (Section 44AB)

This audit is triggered by turnover — the thresholds differ depending on how your Indian entity processes transactions:

| Business Type | Threshold | Condition |

|---|---|---|

| General business | ₹ 1 crore | Standard threshold |

| Digital business | ₹ 10 crore | If 95%+ transactions are digital/banking channels |

| Professionals | ₹ 50 lakh | Gross receipts |

Forms required:

- Form 3CA or 3CB (audit report)

- Form 3CD (statement of particulars)

Deadline: 30th September (standard) or 31st October (if transfer pricing applies)

Penalty: 0.5% of turnover/receipts, maximum ₹ 1.5 lakh (Section 271B)

GST Reconciliation

The mandatory GST audit by CA/CMA was removed effective 1st August 2021 — but the reconciliation obligation remains. UK-owned entities must align GSTR-1 (outward supplies), GSTR-3B (summary return), and books of accounts before the statutory audit is finalised.

Required filings:

- GSTR-9 (annual return): Due 31st December of the following year

- GSTR-9C (self-certified reconciliation): Mandatory if turnover exceeds ₹5 crore; due 31st December

Late fee: ₹200/day (₹100 CGST + ₹100 SGST), maximum 0.50% of turnover

Mismatches between these returns trigger notices and delay audit sign-offs. Monthly reconciliation of GSTR-1 vs GSTR-3B vs books throughout the year — rather than a year-end scramble — is the most reliable way to avoid this.

Transfer Pricing Audit (Form 3CEB)

If your Indian entity has any international transaction with its UK parent or related parties — management fees, royalties, intercompany loans, software licensing, or back-office services — a Transfer Pricing audit is mandatory.

Documentation requirements (Rule 10D):

- Ownership structure and organisational chart

- MNE group profile and business description

- Nature and terms of international transactions

- Functional analysis (functions, assets, risks of each party)

- Comparability analysis and pricing methodology

- Supporting agreements, communications, and market research

Detailed documentation threshold: International transactions exceeding ₹ 1 crore

Master File threshold (Rule 10DA): Group revenue exceeds ₹ 500 crore AND international transactions exceed ₹ 50 crore (or intangibles exceed ₹ 10 crore)

Deadline: 31st October of the assessment year

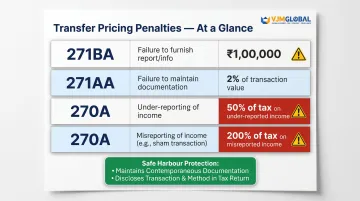

Penalties:

| Section | Trigger | Amount |

|---|---|---|

| 271BA | Failure to furnish Form 3CEB | ₹ 1 lakh |

| 271AA | Failure to maintain documentation or incorrect information | 2% of arm's length price per transaction |

| 270A | Under-reporting income (TP adjustment) | 50% of tax on under-reported income |

| 270A | Misreporting income (undisclosed transaction) | 200% of tax on misreported income |

Critical safe harbour: TP adjustments are not considered under-reporting if you maintained documentation per Section 92D, declared transactions, and disclosed all material facts. This makes contemporaneous documentation (prepared at the time of the transaction) essential insurance against escalating penalties.

This is where missing documentation from UK HQ most frequently causes delays. VJM Global works directly with the UK parent to gather functional analysis data, draft intercompany agreements, and manage the Form 3CEB certification — so the Indian entity is not chasing paperwork at year-end.

India's Audit Season Timeline: Key Dates UK Companies Must Track

April: Audit Planning & Book Closure Begins

Immediately after the 31st March year-end, the audit preparation cycle begins. Auditors are formally engaged, client assistance schedules issued, and management must begin closing the books. For UK companies, this is when the Indian team should initiate dialogue with UK HQ about intercompany transactions and any outstanding documentation—including transfer pricing studies, intercompany agreements, and board resolutions.

May–June: Interim Fieldwork & Book Finalisation

During this phase, two workstreams run in parallel:

- Auditors conduct walkthroughs of key processes, test transactions from the first 9-10 months, and review GST and TDS compliance

- Management finalises year-end accounts, completes bank and vendor reconciliations, and books all provisions and depreciation

Delayed book closure at this stage is the single most common cause of audit overruns for foreign-owned entities. Keeping reconciled books throughout the year — rather than scrambling at year-end — is what separates smooth audits from costly ones.

July: Audit Fieldwork

Auditors now run substantive testing: verifying balances, vouching transactions, reviewing board minutes, and examining related-party transactions. Query volumes can be high during this phase. UK companies must ensure their Indian finance team has prompt access to all documentation and can respond to auditor queries within agreed turnaround times.

August: Finalisation & Board Approval

The draft auditor's report is reviewed and finalised. Before the AGM can proceed, the Board of Directors must formally approve the financial statements. Key actions at this stage include:

- Circulating draft financials to all directors in advance

- Briefing UK-based directors on any India-specific disclosures

- Scheduling the board meeting with enough lead time before the AGM deadline

September: AGM & Regulatory Filing Deadlines

30th September: AGM deadline for companies with March 31 year-end (Section 96)

Post-AGM deadlines:

- Form AOC-4 due within 30 days (approximately 29-30 October)

- Form MGT-7 due within 60 days (approximately 29 November)

Missing these deadlines triggers the penalty structure outlined above, including uncapped additional fees and potential director disqualification.

Also in September/October:

- Tax audit report due 30th September (or 31st October if transfer pricing applies)

- Form 3CEB (transfer pricing report) due 31st October

A Step-by-Step Audit Preparation Checklist for UK Companies

Maintain Clean, Reconciled Books Throughout the Year

Audit readiness requires year-round discipline, not a last-minute sprint. UK-owned entities should:

- Close books monthly

- Reconcile GST returns (GSTR-1 vs GSTR-3B vs books) every month

- Flag unusual or large transactions at the time they occur, not at year-end

- Schedule quarterly check-ins between UK HQ finance teams and the Indian accounting team

Monthly reconciliation protocols typically cover verifying that GSTR-1 matches GSTR-3B and books, reconciling input tax credit against supplier invoices, reversing ineligible ITC with interest where applicable, and confirming TDS deductions are deposited on time.

Document All Intercompany Transactions With the UK Parent

Every transaction between the Indian entity and its UK parent or group companies must be supported by:

- Formal intercompany agreement

- Proper invoicing

- Transfer pricing study

Transaction types requiring documentation:

- Management fees and shared service charges

- Software licensing fees

- Royalties

- Intercompany loans and guarantees

- Reimbursements

- Purchase/sale of goods or services

UK finance teams are often the only people who can provide this documentation, and delays from HQ are the most common audit bottleneck. Start this process in April, not July.

Ensure TDS and GST Compliance Is Current Before Audit Begins

Auditors will verify:

TDS compliance:

- Correct calculation on salaries, vendor payments, rent, and professional fees

- Timely deposit

- Quarterly TDS returns filed

GST compliance:

- Returns fully reconciled with books

- GSTR-1 vs GSTR-3B alignment

- Input tax credit eligibility verified

Any TDS default or GST mismatch must be resolved before the audit can conclude. Unresolved issues typically trigger interest charges and can delay sign-off by several weeks.

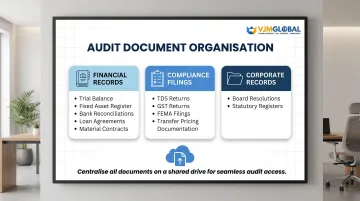

Prepare a Complete Document Repository

Organise documents into three categories before fieldwork begins:

Financial Records:

- Trial balance and general ledger

- Fixed asset register with depreciation schedules

- Bank reconciliations (all accounts)

- Loan agreements and repayment schedules

- Material contracts with UK parent or third parties

Compliance Filings:

- TDS returns and certificates

- GST returns (GSTR-1, GSTR-3B, GSTR-9)

- FEMA filings: FC-GPR (foreign investment reporting), FC-TRS (share transfer reporting), APR (annual performance report)

- Transfer pricing documentation (Local File, Master File if applicable)

Corporate Records:

- Board resolutions and minutes

- Statutory registers (members, directors, charges)

Store these in an accessible shared drive or document management system so the audit team can retrieve them without chasing individuals.

Appoint a Dedicated Internal Audit Liaison

Designate one person on the Indian finance team as the single point of contact for the statutory auditor. For UK-owned companies where HQ involvement is needed, this liaison must have:

- Authority to escalate queries to the UK team quickly

- Access to a shared query tracker to monitor outstanding items

- Clear turnaround time commitments from UK HQ

Where an internal liaison isn't available, firms like VJM Global can fill this role — managing audit checklists, responding to queries, and coordinating between the Indian team and UK headquarters.

Engage Your Statutory Auditor Early and Share a Timeline

Don't wait until May or June to formally engage your Indian auditors. Brief them in April on:

- Significant events from the financial year (new products, acquisitions, intercompany restructuring, key personnel changes)

- Realistic timeline with milestones

- Any anticipated documentation challenges

Early engagement allows auditors to flag documentation gaps before fieldwork begins, reducing the risk of delayed sign-off or regulatory penalties.

Common Mistakes UK Companies Make During India's Audit Season

Assuming the UK Audit Covers or Satisfies Indian Requirements

Many UK finance teams assume that because the Indian entity is consolidated into the UK group audit, no separate Indian filing is needed. That assumption is wrong.

Indian law requires a standalone statutory audit filed with the ROC, conducted by an ICAI-registered Chartered Accountant under Indian Accounting Standards (Ind AS or Indian GAAP). No group-level audit — however thorough — substitutes for this obligation.

Leaving Transfer Pricing Documentation to the Last Minute

Transfer pricing documentation requires months of preparation and significant inputs from the UK parent:

- Pricing policies and justification

- Group financials for Master File

- Functional analysis of the UK entity (functions, assets, risks)

- Intercompany agreements with proper terms

- Comparability analysis using Indian databases

UK companies that start this process after the field audit has begun routinely face:

- Late filings beyond the 31st October deadline

- Auditor qualifications on the financial statements

- Transfer pricing penalty under Section 271AA (2% of the arm's length price)

- Under-reporting penalty under Section 270A (50–200% of tax on under-reported or misreported income)

VJM Global's transfer pricing services start with Q1 planning, collecting functional analysis data from the UK parent early and drafting intercompany agreements before transactions occur rather than retrospectively at year-end.

Treating India's Audit as Purely the Indian Team's Responsibility

Transfer pricing is just one area where UK HQ input is non-negotiable. Across the audit process as a whole, the Indian finance team handles execution — but critical decisions and documentation must come from the UK side.

While the Indian finance team handles day-to-day execution, UK HQ's involvement is essential for:

- Approving intercompany transaction terms

- Providing group-level documentation for transfer pricing (Master File, group structure, functional analysis of UK entity)

- Authorising board resolutions

- Confirming availability of UK-based directors for AGM board meetings

- Responding promptly to auditor queries that touch on UK operations

- Providing FEMA-related documentation (FC-GPR, APR) when the UK parent has made FDI

Lack of UK engagement is the single biggest factor behind audit delays for foreign-owned Indian entities. Establish clear escalation protocols and response time commitments between the Indian team and UK HQ before audit season begins.

Frequently Asked Questions

What is the accounting period in India?

India's financial year runs from April 1 to March 31 each year, as mandated under the Companies Act 2013 and the Income Tax Act. Unlike the UK where companies may choose a different year-end, Indian companies must follow this fixed period with very limited exceptions.

Is a statutory audit mandatory for a UK-owned Indian subsidiary even if it has no revenue?

Yes. Every company incorporated in India—including dormant or pre-revenue entities—must undergo a statutory audit under Section 139 of the Companies Act 2013. There are no turnover-based exemptions for statutory audit, unlike the tax audit which is threshold-triggered.

What is the difference between a statutory audit and a tax audit in India?

A statutory audit verifies compliance with the Companies Act and is mandatory for all Indian companies regardless of turnover. A tax audit under Section 44AB applies only when turnover exceeds Rs 1 crore (or Rs 10 crore for digital businesses) and focuses on income tax reporting accuracy.

When is the transfer pricing audit deadline in India?

The Transfer Pricing Audit report (Form 3CEB) must be filed by 31st October of the assessment year. The Central Board of Direct Taxes has historically issued extension notifications for specific years, so confirm whether one applies to the current assessment year.

Can UK companies use their UK auditors for the Indian subsidiary's statutory audit?

No. Indian law requires the statutory auditor to be a Chartered Accountant registered with the Institute of Chartered Accountants of India (ICAI). UK auditors are not eligible to conduct Indian statutory audits, though they may coordinate with the Indian auditor for group consolidation purposes.

What penalties apply if an Indian statutory audit is not completed on time?

Late filings attract Rs 100/day in additional fees (uncapped), adjudication penalties up to Rs 2 lakh for the company and Rs 50,000 per officer, and potential director disqualification after three consecutive years of non-filing. For UK-owned subsidiaries, non-compliance can also affect FEMA standing and future FDI reporting obligations.

India's audit season demands year-round coordination between your UK headquarters and Indian operations. VJM Global's audit and compliance services help UK companies manage statutory audit, tax audit, GST reconciliation, and transfer pricing obligations through a single point of contact. With 30+ years of experience serving 250+ UK businesses, we know where cross-border audit preparation breaks down — and how to prevent it.

Contact VJM Global at info@vjmglobal.com or +91 9891576441 to discuss your India audit preparation strategy.