That fragmentation creates real complexity. According to Avalara, there are more than 12,000 distinct sales and use tax jurisdictions across the US, each with its own rates, rules, and exemptions. For foreign companies, e-commerce sellers, and multinationals selling into the US market, the exposure is significant: back taxes, penalties, interest, and personal liability for business owners.

This guide walks through the 6 essential steps every business must follow to stay compliant — from identifying where you owe tax to maintaining audit-ready records.

Key Takeaways

- 45 states plus Washington D.C. impose sales tax — there is no federal sales tax

- Nexus (physical or economic) determines whether you must collect and remit in a given state

- The 2018 South Dakota v. Wayfair ruling means online sellers with no US physical presence may still owe tax

- Non-compliance can trigger penalties, interest, and personal liability for business owners

- Following a structured 6-step compliance process, from nexus analysis to recordkeeping, cuts audit risk and back-tax exposure

What Is Sales Tax Compliance in the US?

Sales tax compliance isn't a one-time setup. It's a repeating cycle that restarts as your business grows and changes. Each loop covers:

- Identifying nexus and registering in new states

- Classifying products and calculating the correct rates

- Collecting tax, filing returns, remitting payments, and retaining records

What makes the US system uniquely demanding is its decentralization. VAT systems in the UK, EU, and India apply a national rate with standardized rules. The US has no equivalent. Instead, compliance is determined state by state, jurisdiction by jurisdiction — with rates, exemptions, and filing rules that vary at every level.

Five states have no statewide sales tax at all: Alaska, Delaware, Montana, New Hampshire, and Oregon. Alaska is a partial exception — local municipalities there can still levy their own sales tax. Every other state, plus Washington D.C., sets its own framework independently.

Why Sales Tax Compliance Matters for Your Business

The financial stakes are concrete. California adds a 10% penalty to unpaid tax not remitted on time. Texas applies 5% for tax paid 1–30 days late and 10% for anything beyond 30 days. Those figures compound quickly across multiple states.

Audit exposure compounds the risk further. Research cited by Avalara from Aberdeen Strategy & Research found that 72% of businesses surveyed had been audited in the previous five years, and 38% of audited businesses incurred penalties.

The Risk Grows as You Scale

A business that's compliant at launch can trigger new obligations within months through any of the following:

- Hiring a remote employee in another state

- Storing inventory in a new fulfillment center

- Crossing an economic nexus threshold in a state where they'd never registered

Foreign-owned businesses and companies new to the US market are particularly vulnerable here. The assumption that physical absence equals no tax obligation is no longer valid — and the gap between when nexus is triggered and when a business realizes it can result in years of retroactive liability.

Engaging US-compliant tax professionals before obligations accumulate is considerably less costly than resolving them after the fact. VJM Global's CPAs and cross-border tax advisors specialize in helping international businesses identify and address these obligations before retroactive liabilities take hold.

The 6 Essential Steps for Sales Tax Compliance in the US

These steps form the end-to-end compliance cycle. Each must be revisited as your business adds states, products, sales channels, or team members.

Step 1: Determine Where You Have Sales Tax Nexus

Nexus is the legal connection between your business and a state that creates an obligation to collect and remit sales tax. It comes in two forms:

- Physical nexus — offices, warehouses, employees, or inventory located in a state

- Economic nexus — crossing a state's revenue or transaction threshold, even without any physical presence

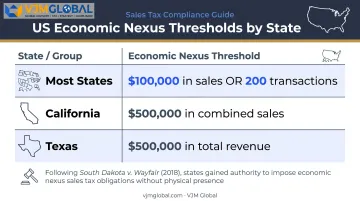

The South Dakota v. Wayfair Supreme Court ruling on June 21, 2018 changed everything. Before that decision, only physical presence could trigger nexus. The Court upheld South Dakota's economic nexus threshold — $100,000 in sales or 200 transactions — and overturned the physical-presence-only rule.

Every state with a sales tax has since adopted its own economic nexus requirements.

Threshold variations matter. The $100,000 or 200-transaction benchmark is widely recognized but not universal:

| State | Economic Nexus Threshold |

|---|---|

| Most states | $100,000 in sales OR 200 transactions |

| California | $500,000 in combined sales |

| Texas | $500,000 in total revenue |

Nexus can also be triggered without obvious signals — through affiliate relationships, marketplace sales (including Amazon FBA inventory storage in some states), remote employees, or click-through arrangements. Businesses must actively monitor all state connections, not just their headquarters location.

Step 2: Register for a Sales Tax Permit

Once nexus exists in a state, you must register with that state's tax authority before collecting any sales tax. Collecting without a permit is a compliance violation — treated the same as not collecting at all.

Each state runs its own registration process, with different forms, fees, and timelines. New York, for example, requires sellers to file for a Certificate of Authority at least 20 days before making taxable sales; operating without one can trigger penalties up to $10,000.

Discovered you should have registered earlier? A Voluntary Disclosure Agreement (VDA) is worth exploring before an audit forces the issue. The MTC Multistate Voluntary Disclosure Program allows businesses to come forward proactively across multiple participating states. In most cases:

- Penalties are waived for the lookback period

- Tax and penalties prior to the lookback period are forgiven

- Many states use a 36-month lookback for sales and use tax (though some use longer periods)

Proactive disclosure is almost always less costly than an audit-triggered assessment.

Step 3: Identify What Products and Services Are Taxable

Nexus tells you where you owe tax. Taxability tells you what you owe it on — and the answer changes by state.

Common exemptions include unprepared groceries, prescription drugs, and long-term residential leases. But an exemption in one state can be fully taxable in another. Businesses must classify every product and service they sell, state by state.

Digital goods and SaaS are particularly variable:

- Connecticut taxes SaaS (computer and data processing services) — at 1% for business use and 6.35% for personal use

- California generally does not tax electronically downloaded software when no tangible media is transferred

- Washington state applies retail sales tax to digital products regardless of delivery method — downloads, streaming, and subscriptions all qualify

For SaaS businesses especially, there is no shortcut. Each state requires its own determination.

Exemption certificates add another layer. When selling to nonprofits, government agencies, or resellers, you must collect a valid exemption certificate at the point of sale and store it properly. During an audit, a missing certificate means full tax liability — even if the buyer was genuinely exempt.

Step 4: Calculate and Collect the Correct Amount of Tax

Not all states calculate tax the same way. The key distinction is sourcing:

- Origin-based states — tax is based on the seller's location. Twelve states use this method, including Arizona, Illinois, Texas, and Pennsylvania. (California is mixed: district taxes follow destination rules.)

- Destination-based states — tax is calculated based on where the buyer receives the goods. This applies to most states and is the standard for most e-commerce transactions.

Remote sellers generally apply destination sourcing when selling into states where they have nexus, using the buyer's delivery address to determine the applicable rate.

Don't overlook use tax. When a business purchases taxable goods from an out-of-state vendor who doesn't charge sales tax, the buyer must self-assess and remit use tax to their own state.

New York makes this explicit: businesses owe use tax on taxable items purchased out-of-state when the seller didn't collect it — including internet, catalog, and phone purchases. This obligation is frequently missed and increasingly audited.

Step 5: File and Remit Sales Tax to Each State

Filing frequency — monthly, quarterly, or annual — is assigned by each state based on your sales volume. Higher-volume sellers typically file monthly; lower-volume sellers may qualify for quarterly or annual filing.

File even when you collected nothing. Most states require a "zero return" confirming that no taxable sales occurred during the period. California and New York both require this — skipping a zero return can trigger penalties identical to a missed filing with tax due.

Common filing deadlines to track:

- Texas: monthly returns due by the 20th of the following month

- New York: quarterly returns due within 20 days after the quarter ends

- Deadlines across states commonly fall on the 15th, 20th, or 25th

Payment is remitted electronically at the same time as filing, through each state's tax portal.

Marketplace facilitator laws affect your obligations. If you sell through Amazon, Etsy, or eBay, those platforms are required to collect and remit sales tax on your behalf in all 45 sales-tax states. Missouri was the last state to implement this, effective January 1, 2023. However, marketplace sales may still need to appear on your own return in some states — and they count toward your economic nexus threshold calculations.

Step 6: Maintain Records and Prepare for Audits

State Departments of Revenue conduct audits periodically, and when they do, you need to produce documentation quickly. The statute of limitations varies by state:

| State | Standard Lookback | Extended Circumstances |

|---|---|---|

| California | 3 years | 8 years if no return was filed |

| New York | 3 years | Longer if exceptions apply |

| Texas | 4 years | Extended if business was unpermitted or fraud is detected |

Core records to retain for the full lookback period:

- Sales invoices and purchase invoices

- Filed returns and payment confirmations

- Exemption certificates (in a centralized, searchable format)

- Bank records confirming remittances cleared

Practical audit-readiness steps:

- Maintain a compliance calendar tracking filing due dates, confirmation numbers, and payment records for every state where you have nexus

- Reconcile bank statements after each remittance to confirm payments were received and posted

- Store exemption certificates in a dedicated system — not a shared drive folder — so they're retrievable by transaction date, buyer, and state

Common Mistakes in US Sales Tax Compliance

Even well-organized businesses stumble on the same compliance traps. Here are the four most common — and the ones with the highest cost when ignored:

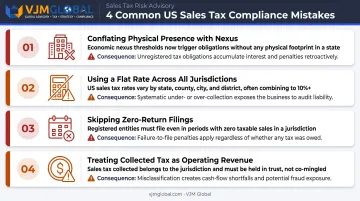

1. Conflating physical presence with nexus. Post-Wayfair, this is no longer valid. Remote sellers and international businesses with purely online operations can trigger nexus in multiple states without a single employee or office on US soil.

2. Using a flat rate across all jurisdictions. With over 12,000 jurisdictions and a mix of origin-based and destination-based sourcing rules, a flat-rate approach will produce both over-collection and under-collection — both of which create compliance problems.

3. Skipping filings when no sales occurred. Businesses registered in a state must file in every period, regardless of whether any sales occurred. This trips up companies that focus compliance effort only on periods with tax owed.

4. Treating collected tax as operating revenue. Sales tax is a trust fund tax — it belongs to the state the moment it's collected. Spending it before remitting exposes business owners to personal financial liability, not just the business entity.

State statutes make this explicit. Under New York Tax Law Section 1133, every person required to collect tax is personally liable for it. California's Section 6829 creates the same responsible-person standard.

Conclusion

US sales tax compliance is structured, repeatable, and manageable — but it demands consistent attention across potentially dozens of jurisdictions. The six steps covered here (nexus determination, registration, taxability classification, rate calculation, filing and remittance, and recordkeeping) form a cycle that must be maintained as business conditions evolve.

For growing businesses, e-commerce sellers, and foreign companies entering the US market, the complexity is real. Obligations can appear quickly and accumulate retroactively.

VJM Global's team of CPAs and cross-border tax advisors supports international businesses at every stage of this process, including:

- Nexus analysis across physical and economic thresholds

- State-by-state registration and account setup

- Taxability classification for products and services

- Ongoing filing and remittance support

Whether you're entering the US market for the first time or catching up on missed obligations, having the right compliance structure in place from the start prevents costly gaps down the line.

Frequently Asked Questions

Is there a sales tax in the USA?

Yes. 45 states plus Washington D.C. impose a statewide sales tax, but there is no federal sales tax — each state sets its own rates, rules, and exemptions independently. The five states with no statewide sales tax are Alaska, Delaware, Montana, New Hampshire, and Oregon, though local jurisdictions in Alaska may still levy their own sales tax.

Do I charge US sales tax to international customers?

The obligation depends on where goods or services are delivered, not where the buyer is based. If a foreign customer receives goods or services in a US state where you have nexus, sales tax may still apply. However, goods physically exported outside the US and destined for delivery abroad are generally not subject to US sales tax.

What is sales tax nexus, and how do I know if I have it?

Nexus is the legal connection between your business and a state that triggers a collection obligation. It can be physical (office, warehouse, employees) or economic (exceeding a state's revenue or transaction threshold). Audit your state connections regularly — nexus can arise through remote employees, affiliate relationships, or marketplace inventory storage, often without the owner's awareness.

What happens if I miss a sales tax filing deadline?

Late filing results in penalties, interest on unpaid tax, and in some cases personal liability for business owners. California adds 10% to unpaid tax; Texas adds 5% for payments 1–30 days late and 10% beyond that. Most states treat a missed zero return identically to a missed filing with tax due.

Do I need to file a sales tax return if I had no sales in a state?

Yes, in most states. Registered businesses must file a zero return confirming no taxable sales occurred during the period. Both California and New York explicitly require this. Failing to file zero returns can result in penalties and may prompt an audit inquiry.

What is the difference between origin-based and destination-based sales tax?

Origin-based states apply the tax rate of the seller's location. Destination-based states — the majority, and the default for most e-commerce — apply the rate based on where the buyer receives the product. Identify which model applies in each state where you have nexus to avoid systematic under- or over-collection.