Introduction

UK businesses investing in innovation can recover substantial sums through government tax relief — but only if they claim under the correct scheme. In tax year 2023-24, HMRC paid out £7.6 billion across 46,950 R&D claims, demonstrating the significant financial incentive available to qualifying companies.

The SME and RDEC schemes have different eligibility rules, calculation methods, and rates of relief. Claiming under the wrong scheme can result in:

- Underclaiming thousands of pounds in legitimate relief

- Overclaiming and facing HMRC penalties

- Triggering a compliance investigation from an increasingly vigilant tax authority

This guide breaks down both schemes side by side — their eligibility criteria, rates, how the relief is received, and when SMEs might use RDEC instead of the SME scheme. We'll also address the 2024 changes that significantly changed the UK R&D tax relief landscape.

Key Takeaways

- The SME R&D Tax Credit Scheme targets companies with fewer than 500 staff and under €100 million turnover, offering enhanced deductions on qualifying costs

- RDEC (Research and Development Expenditure Credit) serves large companies primarily, but SMEs use it for grant-funded or subcontracted R&D projects

- SME relief delivers enhanced deductions or payable credits; RDEC provides an above-the-line credit treated as taxable income — two structurally distinct mechanisms

- For accounting periods beginning on or after 1 April 2024, both schemes merged into a unified system with a separate ERIS route for R&D-intensive loss-making SMEs

- Choosing the wrong scheme risks forfeiting higher-rate SME relief or triggering HMRC compliance action

SME vs RDEC: Quick Comparison

The table below outlines the key differences at a glance — from eligibility thresholds to effective benefit rates.

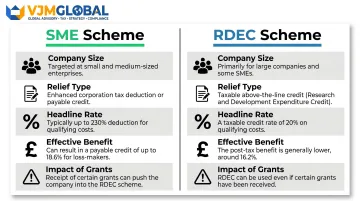

| Dimension | SME Scheme | RDEC Scheme |

|---|---|---|

| Company Size Eligibility | <500 staff AND turnover <€100m (EU-origin threshold) OR assets <€86m | Large companies (exceeding SME thresholds) OR SMEs in specific situations |

| Relief Type | Enhanced deduction or payable credit | Above-the-line expenditure credit (taxable income) |

| Headline Rate (post-April 2023) | 86% additional deduction; 10% credit (14.5% for R&D-intensive) | 20% expenditure credit |

| Effective Benefit | 21.5% (profitable) or 18.6% (loss-making, non-intensive) | 15% (at 25% Corporation Tax rate) |

| Grants/Subsidies Impact | Blocks SME scheme eligibility | No impact on RDEC eligibility |

| Subcontracted R&D | Can claim 65% of unconnected subcontractor costs | Restricted to qualifying bodies, individuals, or partnerships |

One key point: qualifying R&D activities are defined identically under both schemes. The differences lie in who can claim and how the benefit is calculated — not in what R&D qualifies.

What is the SME R&D Tax Credit Scheme?

The SME R&D Tax Credit Scheme is a UK Corporation Tax incentive introduced in 2000 to encourage innovation among smaller businesses. It allows eligible companies to deduct more than 100% of qualifying R&D costs from taxable profits, or claim a payable cash credit if loss-making.

Eligibility criteria:

A company must meet all of the following:

- Fewer than 500 staff

- Either turnover under €100 million OR gross assets under €86 million

One rule that catches many companies out: linked and partner enterprises must be included when calculating these thresholds. The definitions matter here:

- Linked enterprises — where a company holds over 50% of voting rights — require full consolidation of staff, turnover, and balance sheets

- Partner enterprises (25–50% ownership) require proportionate inclusion based on the percentage held

Relief Rates and Benefit Calculation

For expenditure before 1 April 2023:

- Additional 130% deduction (230% total)

- Loss-making companies could surrender losses for a payable credit at 14.5%

For expenditure from 1 April 2023 to 31 March 2024:

- Additional deduction reduced to 86% (186% total)

- Payable credit rate reduced to 10% (or 14.5% for R&D-intensive SMEs meeting the intensity condition)

Real-world benefit (post-April 2023, per £100,000 qualifying expenditure):

- Profit-making companies: 86% × 25% Corporation Tax = £21,500 (21.5%)

- Loss-making companies (non-intensive): 186% × 10% = £18,600 (18.6%)

- Loss-making R&D-intensive SMEs: 186% × 14.5% = £26,970 (~27%)

Qualifying costs include:

- Staff costs (salaries, employer NICs, pension contributions)

- Subcontractor payments (65% of unconnected party costs)

- Externally provided workers

- Consumable items

- Software licences

- Cloud computing costs

- Data licences

- Clinical trial volunteer payments

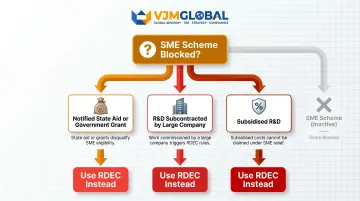

When SMEs Cannot Use This Scheme

The SME scheme is blocked in three scenarios:

- The R&D received a notified State Aid or government grant

- The R&D was subcontracted to the SME by a larger company

- The R&D is subsidised in another way

In these cases, the company must claim through RDEC instead. Grant funding accepted before checking its impact on scheme eligibility can shift a claim from SME rates to the less generous RDEC — so the order of decisions matters.

What is the RDEC Scheme?

RDEC (Research and Development Expenditure Credit) is an above-the-line credit introduced in April 2013 to give large companies a more visible, balance-sheet-friendly way to recognise R&D relief. Unlike the SME scheme's deduction-based approach, RDEC is shown as income in the accounts before being applied against the Corporation Tax liability.

This matters for financial reporting: the R&D benefit appears in pre-tax profit figures rather than being buried in the tax computation.

Eligibility:

RDEC primarily serves large companies exceeding SME thresholds. However, SMEs also use RDEC in specific situations:

- When their R&D project is grant-funded or subsidised by State Aid

- When they're carrying out R&D subcontracted to them by a large company

Note that SMEs contracted by other SMEs cannot claim RDEC for that subcontracted work.

RDEC Rates and Benefit Calculation

For expenditure before 1 April 2023:

- Credit rate: 13% of qualifying expenditure

- Effective benefit: approximately 10.5% after Corporation Tax

For expenditure from 1 April 2023 to 31 March 2024:

- Credit rate: 20%

- Effective benefit: approximately 15% (at 25% CT rate) or 16.2% (at 19% small profits rate)

How the credit is applied:

- First offset against Corporation Tax liability

- Then against other tax liabilities (e.g., VAT)

- Any remaining credit paid out as a cash credit (subject to PAYE cap restrictions)

Qualifying costs under RDEC:

Most standard categories apply — staff, externally provided workers, consumables, software, cloud computing, data licences, clinical trials. However, subcontracted costs are largely excluded unless the subcontractor is:

- A qualifying body (charity, university, health service body, scientific research organisation)

- An individual

- A firm of individuals

This represents a key practical difference from the SME scheme, where subcontractor costs qualify more broadly.

Practical value for SMEs: Even though RDEC's rate is lower than the SME scheme, it's better than no relief at all when the SME scheme is unavailable. In tax year 2023-24, SMEs claimed £795 million through RDEC alongside the £3.6 billion claimed by large companies — showing how widely it is used beyond large companies for grant-funded and subcontracted R&D.

SME vs RDEC: Which Scheme Should You Claim Through?

Companies cannot freely choose the more favourable scheme. The correct route depends on company size, how the R&D project is funded, and the nature of your involvement in the R&D work.

Decision Guide: Determining Your Route

Step 1: Do you meet the SME definition (under 500 staff plus turnover/asset thresholds)?

- No → RDEC

Step 2: Is the R&D project grant-funded or subsidised by State Aid?

- Yes → RDEC (or RDEC for the subsidised portion only)

Step 3: Was the R&D subcontracted to you by a large company?

- Yes → RDEC

If you pass all three checks as an SME with no subsidies or subcontracting constraints → SME Scheme

Split-Claim Scenario

An SME may operate two projects where one is self-funded (SME scheme) and one is grant-funded (RDEC). In this case, both schemes apply simultaneously for the same company in the same accounting period. The qualifying expenditure must be carefully separated between the two routes, with proper documentation supporting each allocation.

Financial Impact of the Decision

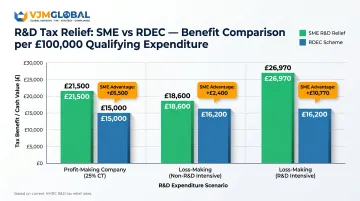

That split matters — because the two schemes produce very different outcomes. Consider £100,000 of qualifying R&D expenditure under post-April 2023 rates:

| Scenario | SME Scheme Benefit | RDEC Benefit | Difference |

|---|---|---|---|

| Profit-making (25% CT) | £21,500 | £15,000 | £6,500 more via SME |

| Loss-making (non-intensive) | £18,600 | £16,200 | £2,400 more via SME |

| Loss-making (R&D-intensive) | £26,970 | £16,200 | £10,770 more via SME |

These gaps scale quickly. A company with £500,000 in qualifying expenditure could forfeit £32,500 in relief by claiming through RDEC when the SME scheme applies. For businesses with complex grant arrangements or split projects, specialist R&D tax advice helps ensure the correct scheme is applied — and that no allowable expenditure is left unclaimed.

The 2024 Update: What Changed?

For accounting periods beginning on or after 1 April 2024, the SME R&D scheme and RDEC merged into a single unified Merged Scheme with a flat 20% expenditure credit rate for most companies.

The old schemes don't disappear overnight, though. Any accounting period starting before 1 April 2024 still falls under the old rules, meaning businesses with live or pending claims must apply the correct scheme to each period.

Enhanced R&D Intensive Support (ERIS)

ERIS replaced the previous intensity condition with a higher-rate route offering an effective 27% benefit. It's available to loss-making SMEs spending at least 30% of their total expenditure on qualifying R&D. The statutory mechanism uses an 86% additional deduction and 14.5% payable credit rate, delivering approximately £27 for every £100 of R&D investment.

Key Implications of 2024 Changes

Subcontracting rules: RDEC-style restrictions (limiting claims to qualifying bodies, individuals, or partnerships) now apply universally under the Merged Scheme. Companies relying heavily on corporate subcontractors will find previously qualifying expenditure now excluded.

Overseas R&D: No longer eligible for relief in most cases, with specific restrictions on payments to overseas contractors and externally provided workers. Northern Ireland-registered SMEs are an exception, retaining broader overseas eligibility.

Intensity threshold: Lowered from 40% to 30%, allowing more loss-making SMEs to qualify for the enhanced 27% rate.

Businesses with accounting periods straddling the April 2024 boundary face the most complexity — expenditure must be split between regimes, with different rates and eligibility rules applied to each portion. Getting this allocation wrong can mean over- or under-claiming relief.

Conclusion

The right scheme comes down to three factors — not whichever rate looks more attractive on paper:

- Company size: SMEs and large companies operate under different eligibility rules

- Funding structure: Grants or subsidised expenditure push claims toward RDEC

- R&D involvement: Whether your company is the claimant or a subcontractor changes everything

SMEs with self-funded, in-house R&D typically benefit most from the SME scheme. Large companies and SMEs with grants or subcontracting arrangements must use RDEC.

With HMRC opening 9,700 compliance checks in 2023-24 and recovering £441 million in tax, scrutiny has intensified dramatically. The SME scheme carries an error rate of 14.6% compared to just 2.8% for RDEC, making correct scheme selection not just about maximising relief but also protecting your compliance position.

Businesses with complex situations — particularly UK subsidiaries of foreign companies or those with mixed funding sources — should take specialist advice before filing. That means reviewing your funding structure, confirming your company size thresholds, and ensuring your claim documentation is watertight before submission.

Frequently Asked Questions

What are R&D tax credits in the UK?

R&D tax credits are a UK government Corporation Tax incentive. Companies can reduce their tax bill or receive a cash payment by claiming relief on qualifying R&D expenditure. Two main schemes — SME and RDEC — applied for periods before April 2024, each with different eligibility rules and rates.

What is the difference between RDEC and SME?

Three core differences separate the schemes:

- Eligibility: SME scheme is based on company size and funding conditions; RDEC applies to large companies and certain SMEs

- Benefit mechanism: SME uses an enhanced deduction; RDEC uses an above-the-line credit

- Relief rate: SME rates are generally higher, though the gap has narrowed since April 2023

What is the R&D tax relief SME scheme?

The SME R&D Tax Relief scheme allows companies with fewer than 500 staff and under €100 million turnover to claim an enhanced deduction on qualifying R&D costs (186% total deduction post-April 2023), or a payable cash credit of 10-14.5% if loss-making.

What is the RDEC tax credit for R&D?

RDEC (Research and Development Expenditure Credit) is an above-the-line credit for large companies and certain SMEs, calculated as a percentage of qualifying R&D expenditure and offset against Corporation Tax. The rate is 20% for expenditure from April 2023, producing an effective 15% benefit at the 25% Corporation Tax rate.

Who is eligible for R&D tax credits?

Any UK-based company subject to Corporation Tax that undertakes qualifying R&D activities in science or technology may be eligible. Which scheme applies — SME, RDEC, or the post-April 2024 Merged Scheme — depends on company size, funding source, and accounting period start date.

What is R&D enhanced deduction?

R&D enhanced deduction is the SME scheme mechanism that lets a company deduct more than the actual cost of R&D from taxable profits. At 186% total deduction, a £100 spend reduces taxable profit by £186. The real R&D benefit is £21.50 — the Corporation Tax saving on the additional 86% enhancement at a 25% rate.