Introduction

For Singapore-incorporated businesses selling into the UK, there's no £85,000 registration threshold — the moment you make a taxable supply to a UK customer, you're required to register for VAT. From there, you're managing filing deadlines, digital submission rules, and cross-border payments across time zones, all while ensuring cleared funds reach HMRC's account on time.

Missing those deadlines carries real financial consequences: a points-based penalty system that escalates to £200 fines per late return, plus late payment interest currently running at 7.75% per annum.

This guide is written for Singapore-based businesses, e-commerce sellers, and service exporters that are UK VAT-registered or approaching that threshold. It covers:

- Registration rules for non-established businesses

- Quarterly filing deadlines by stagger group

- Making Tax Digital (MTD) submission requirements

- Cross-border payment timing considerations

- The full penalty structure for late filing or payment

TLDR: Key Takeaways

- UK VAT-registered businesses must file returns and pay VAT 1 calendar month and 7 days after the end of each VAT quarter

- Non-established overseas businesses, including Singapore companies, must register from the very first pound of taxable UK sales; the £90,000 domestic threshold does not apply

- All submissions require MTD-compatible software; manual HMRC portal filing is no longer permitted

- Singapore businesses cannot typically use Direct Debit and must allow 5–7 working days for international transfers to clear before the deadline

- Late submissions trigger penalty points, reaching a £200 fine at 4 points for quarterly filers

- Late payments attract 7.75% HMRC interest from day one, plus escalating percentage-based penalties

Do Singapore Businesses Need to Register for UK VAT?

The Zero-Threshold Rule for Non-Established Businesses

UK-established businesses enjoy a VAT registration threshold of £90,000 in taxable turnover. However, this threshold does not apply to non-established taxable persons (NETPs)—Singapore companies making any taxable UK supply must register immediately, regardless of turnover size.

According to HMRC's VAT Notice 700/1, "If you're a non-established taxable person (NETP), the registration threshold for taxable supplies does not apply to you, so you'll have to register for VAT if you make taxable supplies of any value in the UK."

What Constitutes a Taxable Supply?

Singapore businesses trigger UK VAT registration through:

- Inventory held in Amazon FBA warehouses or any UK fulfilment centre triggers registration from the first unit sold

- Goods shipped directly to UK consumers valued at £135 or less require VAT charged at point of sale

- Digital products — software, streaming, e-learning platforms — sold to UK consumers

- Professional services where the customer isn't VAT-registered in the UK and the reverse charge doesn't apply

The Post-Brexit £135 Consignment Rule

Since 2021, Singapore businesses selling goods valued at £135 or less directly to UK customers must charge and account for UK VAT at the point of sale. The one exception: B2B sales where the UK customer provides their VAT registration number, triggering the reverse charge instead.

A separate rule applies to goods already on UK soil. For inventory of any value stored in the UK at point of sale, overseas sellers must register and account for VAT on every sale made directly to customers.

Registration Timeline and Process

Singapore businesses must notify HMRC within 30 days of:

- Making the first taxable supply, or

- Expecting to make a supply in the next 30 days

Once that threshold is crossed, the online registration process requires:

- Business details and Singapore incorporation documents

- UK correspondence address (can be an agent's address)

- Bank account details for repayments

- Estimated taxable turnover

HMRC will assign a VAT registration number and a stagger group during registration. Check your HMRC online account to confirm which quarterly cycle applies to you, as this determines every filing deadline going forward.

UK VAT Return Deadlines: Key Dates by Quarter and Stagger Group

The Universal 1 Month + 7 Days Formula

Both VAT return submission and payment share the same deadline: 1 calendar month and 7 days after the end of the VAT accounting period.

Example: For a period ending 31 March, count forward 1 month (to 30 April) then add 7 days = 7 May deadline.

2025-2026 Deadlines by Stagger Group

HMRC assigns businesses to one of three stagger groups at registration:

Stagger Group 1 (quarters ending March/June/September/December):

- 31 March 2025 → 7 May 2025

- 30 June 2025 → 7 August 2025

- 30 September 2025 → 7 November 2025

- 31 December 2025 → 7 February 2026

Stagger Group 2 (quarters ending January/April/July/October):

- 31 January 2025 → 7 March 2025

- 30 April 2025 → 7 June 2025

- 31 July 2025 → 7 September 2025

- 31 October 2025 → 7 December 2025

Stagger Group 3 (quarters ending February/May/August/November):

- 28 February 2025 → 7 April 2025

- 31 May 2025 → 7 July 2025

- 31 August 2025 → 7 October 2025

- 30 November 2025 → 7 January 2026

Critical: Weekend and Bank Holiday Rule

According to CIOT guidance, VAT return submission deadlines do not move when they fall on weekends or bank holidays—contrary to widespread misinformation online. The deadlines are fixed in law.

For payments: If the 7th falls on a Saturday, Sunday, or UK bank holiday, cleared funds must reach HMRC's account by the last working day before that date. Singapore businesses must account for this rule plus the SGT-to-GMT time difference when planning transfer initiation dates.

Monthly VAT Returns

Businesses that regularly reclaim VAT may benefit from switching to monthly returns. This applies particularly to:

- Singapore exporters of zero-rated goods with consistent VAT reclaim positions

- Businesses where UK import costs regularly exceed output VAT

- Companies prioritizing faster refund cycles and improved cash flow

The same 1 month + 7 days deadline applies, resulting in 12 filing dates per year.

Annual VAT Accounting Scheme

Businesses with taxable turnover up to £1.35 million can use the Annual Accounting Scheme:

- Advance payments: Monthly (10% of estimated liability) or quarterly (25%)

- Annual return deadline: 2 months after accounting year end

- Suitability: Less suitable for Singapore businesses with fluctuating UK revenues or those regularly reclaiming VAT

How to Submit a UK VAT Return from Singapore: MTD Requirements

Making Tax Digital Mandatory Since April 2022

Since April 2022, all VAT-registered businesses—including non-UK-established entities—must keep digital VAT records and submit returns exclusively through HMRC-approved MTD-compatible software. Manual entry via the HMRC portal is no longer available.

Technical Setup for Singapore Businesses

Required steps:

- Obtain UK Government Gateway credentials — this can be completed remotely during VAT registration

- Choose MTD-compatible software from HMRC's approved list (Xero, QuickBooks, Sage, or bridging software all qualify)

- Authorise your software by linking it to HMRC's digital tax account via API

- Configure VAT rate categories — ensure the software correctly handles UK standard-rated (20%), zero-rated (0%), and exempt supplies

Multi-Currency Transaction Challenge

Singapore businesses invoicing in SGD or USD face a unique compliance risk: all transactions must be converted to GBP using acceptable exchange rates.

HMRC permits two methods:

- UK market selling rate at the time of supply

- HMRC's published period rates of exchange

Inconsistent conversion methods are a common trigger for HMRC enquiries on overseas-registered businesses. Pick one method and stick to it — keep a simple rate log within your MTD software showing the source rate, date applied, and transaction reference for each period.

Working with a UK VAT Specialist

Singapore businesses can delegate the entire MTD compliance process to a specialist firm: Government Gateway management, digital record-keeping, software configuration, and return preparation. This eliminates filing errors and missed deadlines without requiring in-house UK tax expertise. VJM Global, which supports 250+ UK-registered businesses, handles this end to end for overseas clients.

Payment Deadlines and Cross-Border Considerations for Singapore Businesses

Cleared Funds Requirement

The payment deadline matches the submission deadline (1 month + 7 days), but HMRC must have cleared funds in their account by that date—not just a payment initiated. Singapore businesses must account for international transfer processing times when planning payment dates.

Payment Methods and Processing Times

| Payment Method | Processing Time | Singapore Business Applicability |

|---|---|---|

| Direct Debit | 3 working days | ❌ Requires UK bank account |

| Faster Payments | Same or next day | ✅ Via UK account or fintech |

| CHAPS | Same working day | ✅ Via UK account, bank fee applies |

| Bacs | 3 working days | ⚠️ International transfers: 3–5 days |

| Corporate credit card | Accepted on payment date | ✅ Non-refundable fee applies |

Recommendation: Initiate international bank transfers at least 5–7 business days before the deadline to allow for clearing time.

HMRC Bank Account Details

For overseas bank accounts (Singapore):

- BIC: BARCGB22

- IBAN: GB36BARC20051773152391

- Bank: Barclays Bank PLC, 1 Churchill Place, London, E14 5HP

- Reference: Your 9-digit VAT registration number (no spaces)

Fintech Solutions for Singapore Businesses

Two fintech options work well for Singapore-based businesses making GBP payments to HMRC:

- Wise Business — Confirmed for HMRC VAT payments via Faster Payments, CHAPS, or Bacs using HMRC's sort code (08 32 00) and account number (11963155). Uses mid-market exchange rates; 50% of payments clear within one hour.

- Airwallex — Provides UK GBP accounts for near-instant GBP transfers, though HMRC-specific payment guidance is absent from their official documentation.

Corporate Credit Card Clarification

HMRC accepts corporate credit cards and corporate debit cards, subject to a non-refundable fee. Personal credit cards are not accepted.

Penalties for Missing UK VAT Deadlines

Points-Based Late Submission Penalty

Introduced January 2023, HMRC's penalty system works as follows:

- Each missed deadline earns 1 penalty point

- Quarterly filers reach the threshold at 4 points

- Upon reaching threshold: £200 fine for that return

- Every subsequent late return: £200 fine

Resetting points: Submit all returns on time for 12 consecutive months (quarterly filers) and clear all outstanding returns from the previous 24 months.

Nil return trap: Even periods with zero UK VAT transactions require timely filing — late nil returns attract penalty points just like any other missed submission.

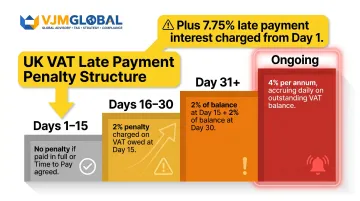

Late Payment Penalty Structure

| Days Overdue | Penalty |

|---|---|

| 1–15 days | No penalty if paid in full or Time to Pay arrangement agreed |

| 16–30 days | 2% of VAT owed at day 15 |

| 31+ days | 2% of day 15 balance + 2% of day 30 balance |

| 31+ days (ongoing) | Daily accruing penalty at 4% per year on outstanding balance |

Late Payment Interest

Interest runs from day 1 of a missed payment deadline at Bank of England base rate + 4%.

Current rate (from 9 January 2026): 7.75%

For Singapore businesses, international bank transfers can take 2–5 working days — factor this lead time into every payment schedule to avoid interest accruing on technically late settlements.

Practical Tips for Singapore Businesses to Stay Compliant

Calendar Management Strategy

- Set deadline alerts in Singapore Standard Time (SGT) at least 10 days before the UK deadline

- Mark all four quarterly deadlines (or 12 monthly deadlines) in advance for the full financial year

- Account for the 7-hour time difference (SGT is 7 hours ahead of GMT, 8 hours ahead of BST)

Real-Time Digital Bookkeeping

Maintain up-to-date UK VAT records throughout each quarter:

- Separate UK-taxable sales from Singapore-domestic and other international activity

- Reconcile multi-currency transactions weekly using consistent GBP conversion rates

- Code transactions correctly (standard-rated, zero-rated, exempt) at point of entry

- Avoid last-minute reconciliation scrambles at period end

Engage a UK-Experienced International Partner

Delegate the entire VAT compliance process to a specialist who understands UK regulations, time zone gaps, multi-currency records, and MTD filing requirements. A UK compliance partner handles:

- VAT return preparation and MTD filing

- Government Gateway setup and maintenance

- HMRC correspondence and enquiry responses

- Multi-currency transaction conversion

- Payment timing coordination

For Singapore businesses, this removes the operational burden of tracking UK deadlines across a 7–8 hour time gap — and eliminates the risk of penalties from late filing or payment.

Frequently Asked Questions

What is the VAT filing deadline in the UK?

The standard deadline is 1 calendar month and 7 days after the end of the VAT accounting period, covering both submission and payment. Payment must clear HMRC's account by that date, not just be initiated. For Singapore businesses, that means initiating international transfers 5–7 working days in advance.

What are the VAT quarters in the UK?

HMRC assigns businesses to one of three stagger groups at registration:

- Group 1: Quarters ending Mar/Jun/Sep/Dec

- Group 2: Quarters ending Jan/Apr/Jul/Oct

- Group 3: Quarters ending Feb/May/Aug/Nov

Check your HMRC online account to confirm your specific cycle, as this determines all your filing deadlines.

When to expect VAT repayment?

HMRC typically processes VAT repayments within 30 days of receiving the return. Singapore businesses that regularly reclaim VAT—such as those importing goods into the UK or selling zero-rated supplies—may benefit from switching to monthly returns to accelerate refund cycles and improve cash flow.

What happens if a VAT return is late?

Late submissions trigger the points-based penalty system: 1 point per late return, with a £200 fine at the threshold of 4 points for quarterly filers. Separate late payment penalties and interest (currently 7.75%) begin accruing from day 1 of a missed payment deadline.

Do you pay VAT on the invoice date or the payment date?

Under the standard VAT accounting method, VAT is accounted for on the invoice date (tax point). Under the Cash Accounting Scheme (available to businesses with turnover up to £1.35 million), VAT is accounted for when payment is received, which is particularly useful for Singapore businesses with longer payment cycles from UK clients.

Who needs to pay VAT in the UK?

Any business making taxable supplies in the UK above the £90,000 registration threshold must register. Critically, non-established overseas businesses (including Singapore companies) must register from the first pound of UK taxable sales, with no minimum threshold exemption.