Introduction

Most Singapore businesses entering the UK assume VAT registration only kicks in after £90,000 in revenue — the same way GST thresholds work at home. That assumption is wrong, and it's an expensive one to make.

Non-Established Taxable Persons (NETPs) — any business without a UK physical presence — must register for VAT from their very first taxable sale, with no revenue threshold. Getting this wrong means backdated VAT liabilities, late registration penalties of up to 15%, and a compliance backlog that can stall your UK operations before they start.

This guide covers who qualifies as an NETP, when registration is required, how to register, and what ongoing compliance looks like for Singapore businesses selling into the UK.

Key Takeaways

- UK VAT registration threshold is £90,000 in taxable turnover (rolling 12 months) — but doesn't apply to most Singapore businesses

- Singapore companies classified as NETPs must register from their first taxable UK sale, regardless of size

- Standard UK VAT rate is 20%; registered businesses charge it on sales, file quarterly digital returns, reclaim input VAT, and maintain compliant records

- Voluntary registration can make sense if you have significant UK input costs or sell primarily to VAT-registered B2B customers

What is UK VAT? Key Basics for Singapore Businesses

VAT (Value Added Tax) is a consumption tax applied at each stage of the supply chain in the UK. Unlike Singapore's 9% GST, UK VAT is charged at 20% on most goods and services — a rate that's been in place since January 2011. VAT has operated in the UK since 1973 and represents one of the government's largest revenue sources, generating £179.6 billion in 2025-26 — equivalent to 14.6% of all receipts.

The Three UK VAT Rates

The UK applies three distinct VAT rates:

- Standard rate (20%): Most goods and services, including professional services, electronics, and most retail items

- Reduced rate (5%): Children's car seats, home energy, installation of energy-saving materials

- Zero rate (0%): Most food, books, newspapers, children's clothing and shoes, exported goods, most public transport

One distinction within these categories matters specifically for registration: zero-rated sales count toward your taxable turnover, while VAT-exempt sales — financial services, insurance, education, and healthcare — do not.

How VAT Works for Singapore Businesses

VAT-registered businesses collect VAT from UK customers on behalf of HMRC and can reclaim VAT paid on their own business inputs. This input/output mechanism means you're acting as a tax collector, not absorbing the 20% cost yourself. VAT paid on eligible business expenses offsets the VAT you collect, so the net impact on your margin depends on your cost structure — not the headline rate alone.

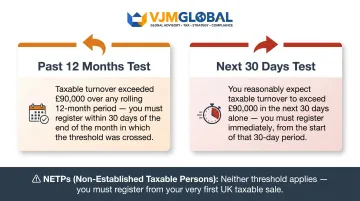

The UK VAT Registration Threshold Explained

The current UK VAT registration threshold is £90,000 in taxable turnover within any rolling 12-month period, effective from 1 April 2024 (increased from £85,000). The deregistration threshold sits at £88,000 — if your taxable turnover drops below this level, you can cancel your VAT registration.

Two Registration Triggers

Two separate tests can trigger a registration obligation:

- Past 12 months (backward-looking): Taxable turnover exceeded £90,000 — register within 30 days of the end of that month

- Next 30 days (forward-looking): You expect turnover to exceed £90,000 within the next 30 days alone — register immediately by the end of that period

Example: If on 1 May you sign a £100,000 contract to be paid end of May, you must apply by 30 May.

What Counts as Taxable Turnover

Includes:

- Standard-rated, reduced-rated, and zero-rated sales

- Goods hired or loaned to customers

- Business goods used for personal reasons

- Reverse charge services received from abroad

Excludes:

- VAT-exempt sales (financial services, education, insurance)

- Out-of-scope supplies

- Capital assets like buildings, equipment, vehicles

Understanding what falls inside and outside these categories matters — especially for Singapore businesses supplying digital services or physical goods to UK customers, where classification directly determines whether you've crossed the threshold at all.

For context, at a USD-PPP equivalent of ~$132,500, the UK threshold is the third-highest among OECD countries — nearly twice the OECD average. Many smaller Singapore exporters may remain below it, but those scaling quickly should monitor their rolling 12-month turnover closely.

The NETP Rule: Why the Threshold May Not Apply to Your Singapore Business

If your company has no UK branch, office, or fixed establishment, HMRC classifies you as a Non-Established Taxable Person (NETP). NETPs must register for UK VAT from their very first taxable supply to UK customers — the £90,000 threshold does not apply.

HMRC's official guidance leaves no ambiguity: "You must register (regardless of taxable turnover) if all of the following are true: you're based outside the UK; your business is based outside the UK; you supply any goods or services to the UK (or expect to in the next 30 days)."

Common Singapore Business Scenarios

- E-commerce (physical goods to UK consumers): Register as NETP from your first sale — no minimum threshold.

- Digital services (SaaS, apps, media): Register from first sale unless all customers are UK VAT-registered businesses using reverse charge.

- Professional services (consulting, marketing, IT): Registration depends on who you're selling to — B2B or B2C. See the reverse charge section below for details.

The Reverse Charge Mechanism

The reverse charge rule determines whether you or your UK customer handles VAT:

- Selling to a UK VAT-registered business (B2B): The UK customer accounts for VAT directly — you do not need to register as long as all your UK customers are VAT-registered.

- Selling to UK consumers or non-VAT-registered businesses (B2C): You must register for UK VAT and charge it directly on each sale.

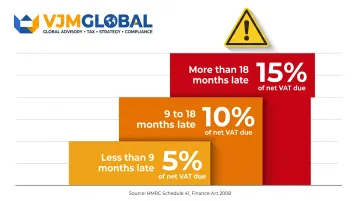

Penalties for Non-Compliance

Failure to register when required triggers serious consequences. HMRC can demand VAT on all past sales from the date registration should have begun, plus late registration penalties under Schedule 41 of the Finance Act 2008:

- Less than 9 months late: 5% of net VAT due

- 9 to 18 months late: 10% of net VAT due

- More than 18 months late: 15% of net VAT due

What Singapore Businesses Must Do After UK VAT Registration

Charging and Invoicing

From your effective registration date, every applicable sale to a UK customer must include VAT at the correct rate. VAT invoices must display:

- Your VAT registration number

- The VAT amount charged

- The applicable rate

Singapore businesses selling in SGD or USD must convert amounts to GBP for VAT purposes.

Making Tax Digital (MTD) Compliance

Since April 2022, all VAT-registered businesses must keep digital records and file returns via MTD-compatible software. VAT returns are due quarterly. You cannot use HMRC's direct portal; software with API integration is required to submit returns.

MTD-compatible options include:

- Xero, QuickBooks, Sage

- Specialized VAT software with bridging capabilities

- HMRC maintains a searchable tool for finding compatible software

Reclaiming Input VAT

VAT-registered Singapore businesses can reclaim UK VAT paid on UK-sourced business expenses. This offsets a meaningful portion of compliance costs. Qualifying expenses include:

- Supplier costs and professional service fees

- UK event registrations and business travel

- Office or venue hire in the UK

Personal expenses and non-business costs don't qualify for reclaim.

Managing these obligations from Singapore — without in-house UK tax expertise — is where many businesses hit friction. VJM Global's international tax compliance team handles everything from initial registration through quarterly MTD filing. Having supported 250+ UK businesses, the firm helps international companies meet HMRC requirements without building a dedicated compliance function in-house.

Should Singapore Businesses Consider Voluntary VAT Registration?

Singapore businesses with UK taxable turnover below £90,000 (or NETPs who haven't yet made their first UK taxable supply) can voluntarily register for UK VAT. This makes strategic sense in specific scenarios:

When voluntary registration benefits you:

- You have significant UK-sourced costs and want to reclaim VAT paid

- You primarily sell to UK VAT-registered businesses who can reclaim the VAT you charge them — your price doesn't effectively increase for them

The compliance trade-off:

- Quarterly VAT returns with MTD-compatible software

- VAT invoicing requirements on all UK sales

- Administrative burden and potential accounting costs

If your UK customers are mostly end consumers or non-VAT-registered buyers, adding 20% VAT makes you less price-competitive against UK-established suppliers — a meaningful disadvantage worth factoring in.

Weigh reclaimable input VAT against your compliance costs and any pricing impact before deciding. For most Singapore businesses, the numbers make this straightforward to model, but the right answer depends on your customer mix and margins.

How to Register for UK VAT as a Singapore Business

Mandatory vs. Voluntary Registration Process

Registration is completed online through HMRC's VAT registration service. Singapore businesses register as NETPs.

Information required:

- Business details and nature of UK supplies

- Expected UK taxable turnover

- Bank details for any VAT refunds

- Company registration number and tax reference

Once registered, HMRC issues a VAT registration number and effective registration date.

Post-Registration Steps

- Appoint a VAT agent or fiscal representative if needed — HMRC can direct NETPs from countries without mutual assistance arrangements to do so, and the appointed representative becomes jointly and severally liable for any VAT debts.

- Set up MTD-compatible accounting software before your first quarterly filing deadline.

- Update invoicing templates to display your UK VAT number on all applicable invoices.

- Track your rolling 12-month UK taxable turnover to stay ahead of the £90,000 threshold.

Frequently Asked Questions

What is the UK VAT threshold?

The current UK VAT registration threshold is £90,000 in taxable turnover over any rolling 12-month period. This threshold applies to UK-established businesses. Singapore businesses classified as NETPs must register from their first taxable UK sale.

Is VAT registration mandatory in the UK?

Registration is mandatory once a UK-based business exceeds the £90,000 threshold, or immediately for non-UK businesses (NETPs) making any taxable supply in the UK. Failure to register when required results in backdated VAT liability and penalties.

Is the UK VAT threshold based on turnover or profit?

The £90,000 threshold is based on taxable turnover — the total value of VAT-able sales — not profit. This includes zero-rated supplies but excludes VAT-exempt sales.

Is VAT still 20% in the UK?

The standard UK VAT rate is 20%, unchanged since January 2011. A reduced rate of 5% applies to certain goods such as home energy, while a 0% zero rate covers most food and children's clothing.

Who is exempt from VAT in the UK?

Businesses selling only VAT-exempt goods or services — such as financial services, insurance, education, or healthcare — don't need to register. Singapore businesses selling even partially taxable supplies to UK customers will likely need to register, as NETPs can claim exemption only when all supplies are zero-rated.

What happens if I temporarily go over the VAT threshold?

UK-established businesses can apply to HMRC for a registration exception if the breach was temporary and turnover is expected to fall below £88,000 — HMRC will then either grant the exception or proceed with registration. This route is not available to NETPs like Singapore businesses, who must register from their first taxable supply regardless of circumstances.