Introduction

A UK VAT return is a periodic report filed with HMRC declaring output VAT charged on sales and input VAT paid on purchases. The net difference is either paid to or reclaimed from HMRC.

For Singapore companies selling goods or services in the UK, one misstep in this process can trigger cash flow strain, penalty points, or a costly HMRC compliance review.

This guide is written for Singapore-incorporated businesses — or Singapore-based companies with a UK VAT registration — navigating the UK market. Here's what it covers:

- When you must register for UK VAT

- The step-by-step filing process via HMRC

- How to complete all 9 VAT return boxes correctly

- Common pitfalls for overseas businesses, including reverse charge rules and Making Tax Digital requirements

Key Takeaways

- UK VAT returns are filed electronically via HMRC's Making Tax Digital (MTD) system quarterly, due one month and seven days after each period ends

- Singapore companies must register for UK VAT from their first taxable sale—the £90,000 threshold does not apply to non-UK businesses

- The return comprises 9 boxes; Box 5 (output VAT minus input VAT) determines what you pay or reclaim

- MTD-compatible software is mandatory; paper submissions are not accepted under any circumstances

- Late submissions trigger a points-based penalty system; accumulating 4 points results in a £200 fine

What Is a UK VAT Return?

A UK VAT return is a formal declaration submitted to HMRC reporting the total VAT a business charged on its taxable sales (output VAT) and the VAT it paid on business purchases (input VAT) during a set accounting period (typically three months).

The return calculates your net VAT position. If output VAT exceeds input VAT, you pay the difference to HMRC. If input VAT exceeds output VAT, you reclaim the surplus. Most UK-registered businesses file quarterly, though some use annual accounting schemes.

How UK VAT Differs from Singapore GST

While Singapore's GST and UK VAT operate on the same output-tax-minus-input-tax mechanism, the two systems diverge significantly:

| Feature | UK VAT | Singapore GST |

|---|---|---|

| Standard rate | 20% | 9% (from 1 Jan 2024) |

| Reduced rate | 5% (children's car seats, home energy) | None |

| Zero rate | 0% (most food, children's clothes, exports) | 0% (exports, international services) |

| Registration threshold (domestic) | £90,000 | S$1 million |

| Return format | 9-box return with reverse charge and import VAT fields | Different format, no reverse charge equivalent |

According to IRAS, "In other countries, GST is known as the Value-Added Tax or VAT." The UK's three-tier rate structure and distinct exemptions — covering financial services and property transactions — set it apart from GST. Singapore companies cannot carry their existing GST workflows directly into UK VAT compliance; the 9-box return format alone introduces fields with no GST equivalent.

Do Singapore Companies Need to File UK VAT Returns?

The Non-Established Taxable Person (NETP) Rule

Unlike UK-resident businesses, which register only after annual taxable turnover exceeds £90,000, Singapore companies with no UK establishment must register for VAT from the very first sale of taxable goods or services in the UK. VAT Notice 700/1 states: "The registration threshold for taxable supplies does not apply to you, so you'll have to register for VAT if you make taxable supplies of any value in the UK."

This zero-threshold rule catches many Singapore businesses off guard, particularly those accustomed to Singapore's S$1 million GST registration threshold.

Key Registration Triggers for Singapore Companies

You must register as an NETP if you:

- Store goods in the UK for sale (such as Amazon FBA warehouse stock)

- Sell digital services — software, apps, or e-books — directly to UK consumers

- Provide professional services where the place of supply is the UK

- Import goods into the UK for onward sale

- Ship low-value consignments of £135 or less from outside the UK to UK customers

According to HMRC's guidance on overseas goods, overseas sellers who own goods located in the UK at the point of sale must register for VAT regardless of turnover.

How to Register

Singapore companies register as NETPs through HMRC's online VAT registration portal. You'll need:

- Company details and Singapore registration number

- Description of business activity

- UK turnover estimates

- UK bank account details (or payment arrangements)

HMRC typically issues a UK VAT number within 30 days and confirms your filing frequency (usually quarterly). Registration must be completed within 30 days of making or intending to make your first taxable UK supply.

When You May Not Need to Register

Not every Singapore business selling into the UK needs to register directly. If all your UK sales are business-to-business (B2B) and the UK customer is VAT-registered, the UK customer may account for VAT under the reverse charge mechanism — meaning you don't charge UK VAT. This applies only to specific service categories; you'll need to confirm the place of supply rules for your particular service type. Goods sales generally do not qualify.

Appointing a UK Tax Agent

Working with a UK tax representative is not automatically mandatory for all NETPs, but HMRC has the power under Section 48(1) of the VAT Act 1994 to direct non-EU NETPs to appoint one — and that representative becomes jointly liable for any VAT debts. HMRC exercises this power selectively, so it's worth obtaining advice before assuming no representative is needed.

VJM Global works with Singapore clients on HMRC registration, return filings, and ongoing correspondence, covering both the technical compliance side and the MTD (Making Tax Digital) submission requirements.

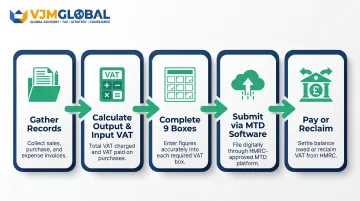

How to File a UK VAT Return: Step-by-Step

All UK VAT returns must be submitted digitally via HMRC's Making Tax Digital (MTD) system using MTD-compatible accounting software (such as QuickBooks, Xero, or Sage). HMRC states: "All VAT registered businesses should now be signed up for Making Tax Digital for VAT." Manual portal submissions are no longer available for most businesses.

Step 1: Gather Your Records for the Period

Collect all:

- Sales invoices (output VAT charged)

- Purchase invoices and receipts (input VAT paid)

- Import VAT statements from HMRC's Customs Declaration Service

- Reverse charge transaction records

Under MTD rules, digital VAT records must be retained for at least six years.

Step 2: Calculate Output and Input VAT

Output VAT: Total VAT charged on all UK taxable sales during the period, applying the correct rate:

- Standard: 20%

- Reduced: 5%

- Zero-rated: 0%

Input VAT: Total recoverable VAT from business purchases. Note: VAT on client entertainment, personal expenses, or non-business use cannot be reclaimed.

Step 3: Complete the 9 VAT Return Boxes

Enter figures into each box (detailed breakdown in next section). Box 5 (net VAT payable or reclaimable) must accurately reflect the difference between Box 3 and Box 4. This is the final amount you'll either pay to HMRC or reclaim.

Step 4: Submit via MTD-Compatible Software

Use your MTD-compatible software to submit electronically to HMRC before the deadline: one month and seven days after the accounting period ends. For example, a period ending 31 March has a deadline of 7 May.

Your software will generate a submission confirmation with a reference number. Save this as proof of filing.

Step 5: Make Payment (or Claim a Refund)

Box 5 determines whether you owe HMRC or are owed a refund.

If Box 5 shows an amount owed: Pay HMRC electronically by the same deadline using:

- Faster Payments (same/next day)

- CHAPS (same day)

- Bacs (3 working days)

Cleared funds must reach HMRC's account by the due date, not just be sent. Singapore companies should account for international transfer times.

If Box 5 shows a net repayment: HMRC will process the refund, typically within 30 days, though compliance checks can delay this.

Understanding the UK VAT Return: The 9 Boxes

The official HMRC guidance (VAT Notice 700/12) defines each box:

Boxes 1 and 2

Box 1 covers total output VAT due on sales and other outputs, including VAT on reverse charge transactions where you receive UK services.

Box 2 applies to VAT on goods acquired in Northern Ireland from EU member states — not relevant for most Singapore companies operating in Great Britain.

Boxes 3 and 4

Box 3 is simply the sum of Box 1 + Box 2 — your total VAT due.

Box 4 captures total input VAT recoverable on purchases. This includes:

- Import VAT under Postponed Import VAT Accounting (PIVA)

- Reverse charge VAT

- VAT on general business costs

Box 5 is the net figure: Box 3 minus Box 4. This is what you either pay to HMRC or reclaim from them.

Boxes 6 and 7

Box 6 is the total value of all sales and outputs (excluding VAT), covering zero-rated, reduced-rated, and out-of-scope supplies.

Box 7 is the total value of all purchases and inputs (excluding VAT), including imports. Singapore companies using PIVA must capture import values here even though no upfront VAT was paid at the border.

Boxes 8 and 9

Both relate specifically to Northern Ireland–EU goods movements and will typically be zero for Singapore companies selling into Great Britain only.

Error Corrections

Two thresholds determine how you correct a VAT error:

- Minor errors (under £10,000, or under £50,000 and below 1% of Box 6) — correct on your next return

- Larger errors — submit a voluntary disclosure using HMRC Form VAT652

Key Considerations and Common Mistakes for Singapore Companies

MTD Compliance and Software Setup

Singapore companies often overlook that standard spreadsheet-based filing or direct HMRC portal submission is not permitted under MTD. VAT Notice 700/21 explicitly states that "cut and paste" is not considered a digital link and is non-compliant.

What you need:

- API-enabled accounting software (Xero, QuickBooks, Sage)

- Or spreadsheets digitally linked to "bridging software" that handles API submission

Confirm your accounting system has active HMRC MTD API integration before your first filing deadline.

Reverse Charge Misapplication

Singapore companies supplying B2B services to UK VAT-registered customers sometimes incorrectly charge UK VAT when the reverse charge should apply instead. This triggers reconciliation problems, error corrections, and customer refunds.

Rule: For most B2B services supplied from overseas, the reverse charge applies—the UK customer accounts for VAT, not the Singapore supplier.

Common triggers for reverse charge errors include:

- Applying standard UK VAT rates to services delivered remotely to UK businesses

- Failing to confirm the UK customer's VAT registration status before invoicing

- Using domestic B2C invoicing templates for B2B cross-border transactions

Import VAT and Postponed Import VAT Accounting (PIVA)

Singapore companies importing goods into the UK should apply for PIVA. It lets you declare and reclaim import VAT on the same VAT return, rather than paying it upfront at the port — preserving working capital that would otherwise be tied up for weeks.

How to access monthly PIVA statements:

- Log in to the Customs Declaration Service (CDS) using your Government Gateway ID

- Statements show total import VAT postponed for the previous month

- Available by the 10th working day of the month

- Accessible for only 6 months—download and retain copies

Skipping PIVA when you qualify means paying import VAT upfront at the port — tying up funds until your next return cycle.

Common Issues with Deadlines and Penalties

Points-Based Penalty System

Since 1 January 2023, HMRC uses a points-based penalty system:

| Filing Frequency | Points Threshold | Penalty at Threshold | Subsequent Late Submissions |

|---|---|---|---|

| Quarterly | 4 points | £200 | £200 each |

| Monthly | 5 points | £200 | £200 each |

| Annual | 2 points | £200 | £200 each |

Each late submission earns one penalty point. Once you reach the threshold, HMRC issues a £200 penalty, with further £200 penalties for each subsequent late submission. Late payment interest also applies from day one of the overdue amount — there is no grace period.

Managing Cross-Border Deadlines

Singapore companies managing multiple filings across time zones should set internal submission deadlines at least two weeks ahead of HMRC deadlines to allow for:

- Internal review

- Currency conversion and international bank transfers (Bacs, the UK bank transfer system, takes 3 working days)

- Time zone differences (UK is 7-8 hours behind Singapore)

Conclusion

Singapore companies with UK VAT obligations need to get several things right from the start:

- Register as a Non-Established Taxable Person (NETP) with HMRC

- Use MTD-compatible software for all VAT records

- Complete the 9-box return accurately each quarter

- Submit electronically by the deadline — one month and seven days after the period ends

- Pay or reclaim the net VAT balance on time

UK VAT compliance for overseas businesses involves real complexity: zero registration thresholds, NETP rules, PIVA, reverse charges, and MTD requirements all differ significantly from Singapore's GST framework.

Working with a cross-border tax specialist like VJM Global — with 30+ years of compliance experience and 250+ UK businesses served — helps Singapore companies stay accurate and avoid costly filing errors.

Frequently Asked Questions

What is a VAT return in the UK?

A UK VAT return is a quarterly (or annual) report filed with HMRC showing the VAT a business charged on sales (output VAT) and paid on purchases (input VAT). The net difference is either paid to or refunded by HMRC.

How do I file a VAT return in the UK?

VAT returns must be submitted electronically using Making Tax Digital (MTD)-compatible software via HMRC's online systems. Businesses log in through the Government Gateway, complete the 9-box return using digital records, and submit before the deadline.

When are VAT returns due and how often must they be submitted in the UK?

Most VAT-registered businesses file quarterly. The deadline for both submission and payment is one month and seven days after the end of the accounting period—for example, a period ending 31 March has a deadline of 7 May.

Who needs to file a VAT return in the UK?

Any VAT-registered business must file returns, even if no VAT is owed or reclaimable. Singapore companies making taxable supplies in the UK must register and file regardless of the £90,000 threshold that applies only to UK-established entities.

Can a Singapore company appoint a tax agent to file UK VAT returns on its behalf?

Singapore companies can appoint a UK-authorised tax agent who registers with HMRC to act on their behalf. The agent can submit returns, communicate with HMRC, and manage compliance obligations — a practical option for companies without in-house UK tax expertise.

What happens if a Singapore company misses the UK VAT return deadline?

Each missed deadline earns one penalty point. Once the threshold is reached (4 points for quarterly filers), a £200 financial penalty is issued, with further £200 penalties for each subsequent late submission. Late payment also accrues daily interest, making timely filing and payment essential.