Introduction

UK VAT compliance has grown substantially more complex in recent years. HMRC now expects businesses to demonstrate documented processes, preventive controls, and digital record-keeping under its Guidelines for Compliance 8 (GfC8), published in September 2024 — not just file returns on time. The stakes have risen: HMRC completed 320,000 compliance checks in 2023-24, a 15% year-on-year increase, with a compliance yield target of £45.4 billion for 2024-25. Late payment interest now runs at the Bank of England base rate plus 2.5%, and the VAT gap has widened to 6.5% (£11.9 billion) in the latest estimate.

Those figures make the cost of getting VAT wrong very real — for businesses of any size.

This guide covers everything VAT-registered UK businesses need to know: core VAT rules, common compliance failures, how to build a GfC8-aligned control framework, and what to expect during an HMRC compliance check. It applies to small traders approaching the £90,000 registration threshold and established companies managing high-volume transactions alike.

Missing deadlines, applying the wrong VAT rate, or failing to maintain Making Tax Digital (MTD) records can trigger penalties from 0% to 100% of potential lost revenue, plus interest.

TLDR: Key Takeaways

- VAT registration is mandatory for UK businesses with taxable turnover above £90,000.

- VAT-registered businesses must charge VAT at the correct rate, file returns (usually quarterly), and pay HMRC on time.

- HMRC's GfC8 guidelines require documented controls, risk ownership, and digital audit trails — not just accurate filing.

- Common failures include incorrect VAT calculations, missed deadlines, poor record-keeping, and misclassified transactions.

- Building a structured VAT control framework is the most effective way to stay compliant and audit-ready.

What Is UK VAT Compliance?

VAT is an indirect tax collected by businesses on behalf of HMRC. VAT compliance means accurately accounting for VAT on all sales and purchases, filing returns correctly, and keeping adequate records.

Compliance today includes meeting governance expectations under Making Tax Digital (MTD). Businesses must keep digital records and submit VAT returns through HMRC-approved software. HMRC's guidance document GfC8 adds a further layer of recommended best practice around process documentation, controls, and accountability.

Mandatory vs. recommended:

- VAT law and MTD rules are legally binding — non-compliance triggers penalties.

- GfC8 is advisory, but HMRC references it when assessing whether a business took "reasonable care" under Schedule 24 FA 2007. Following it provides a documented defence against careless-error penalties.

GfC8 explicitly states: "Following these guidelines may help you to demonstrate that you have taken reasonable care in relation to your VAT compliance."

Who Needs to Register for VAT and What Are the Key Rules?

Registration threshold

Businesses must register for VAT once their VAT-taxable turnover exceeds £90,000 in any rolling 12-month period (increased from £85,000 on 1 April 2024). Voluntary registration is also possible below this threshold — beneficial when you buy more than you sell, want to reclaim input VAT, or need to appear more established.

If your turnover is approaching that threshold, you're far from alone: the UK VAT population stood at 2,330,400 traders in 2024-25, with 234,000 new registrations that year.

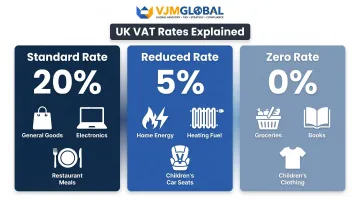

Three UK VAT rates

| Rate | Percentage | Examples |

|---|---|---|

| Standard | 20% | Most goods and services |

| Reduced | 5% | Domestic energy, children's car seats |

| Zero | 0% | Most food, books, children's clothing |

Getting the rate wrong cuts both ways. Treating a zero-rated item as standard-rated means you overcharge customers and hand HMRC more than you owe. Treating a standard-rated item as zero-rated means you underpay HMRC and expose yourself to penalties.

Core obligations

Once registered, you must:

- Charge VAT at the correct rate on all taxable sales

- Keep records of all VAT charged (output tax) and paid (input tax)

- Submit a VAT return (usually every 3 months) through MTD-compliant software

- Pay any VAT owed to HMRC by the due date — the net amount is output tax minus input tax

Common VAT Compliance Mistakes UK Businesses Make

Incorrect VAT treatment on sales or purchases

Applying the wrong VAT rate is one of the most frequent errors, compounding across hundreds or thousands of transactions. "Failure to take reasonable care" now accounts for 31% of the overall UK tax gap, up from 26% in 2019-20 — the largest single contributor.

Missed or late VAT return filing and payment

Late submission triggers a penalty points system (introduced 1 January 2023):

| Filing Frequency | Penalty Point Threshold | Penalty per Late Return |

|---|---|---|

| Annual | 2 | £200 |

| Quarterly | 4 | £200 |

| Monthly | 5 | £200 |

Each late return earns one point; reaching the threshold triggers a £200 penalty, and each subsequent late submission whilst at the threshold incurs a further £200.

Late payment penalties compound quickly:

- Days 0–15: No penalty (grace period)

- Days 16–30: 3% of balance outstanding at day 15

- Days 31+: Additional 3% of balance at day 30, plus 10% per annum calculated daily on the outstanding amount

Incorrectly claiming input VAT

Common input VAT errors include:

- Reclaiming VAT on non-business expenses

- Using invalid or missing VAT invoices

- Claiming back VAT on items specifically blocked from recovery (for example, most business entertainment under Section 24 VATA 1994)

HMRC scrutinises input tax claims closely during compliance checks. Staff entertainment is recoverable, but entertaining clients, customers, or suppliers is not. Mixed events require apportionment between the two.

Poor record-keeping and version control issues

Inadequate records — disorganised invoices, inconsistent data across systems, or spreadsheets without version control — make it impossible to support VAT decisions during an HMRC check. GfC8 specifically warns: "Manual intervention at system interfaces increases the risk of data loss or corruption."

Failure to use MTD-compliant software or processes

Since Making Tax Digital became mandatory for all VAT-registered businesses from 1 April 2022, maintaining manual records or using non-compliant software is itself a compliance failure — even if the VAT figures are correct. HMRC expects an "unbroken chain of digital links" from primary records to the VAT return.

How to Build a Robust VAT Compliance Control Framework

Step 1 — Map and document VAT risks

Identify where VAT errors are most likely to occur across the business:

- Invoicing (wrong rate applied)

- Procurement (invalid supplier invoices)

- Cross-border transactions (import/export VAT treatment)

- Employee expenses (personal vs. business use)

Record these in a structured VAT risk register noting each risk's likelihood, impact, existing controls, and owner. HMRC's Good Practice Guide (GfC8) explicitly requires risks to be "identified and documented."

Step 2 — Design preventive controls

Controls should stop errors at source, not just detect them after the fact:

- Automated VAT code validation in accounting software

- Mandatory drop-down menus instead of free-text entry

- Approval workflows for large purchase orders

- Systematic invoice checks before payment

GfC8 recommends "automated controls over manual controls" because they are "less susceptible to human error or override."

Step 3 — Assign clear ownership

Every VAT-relevant process should have a named owner responsible for its accuracy:

- Supplier onboarding

- Invoice approval

- VAT return preparation

- Error correction

GfC8 states: "Accountability for VAT should be held at an appropriate level of seniority within the business, such as a Director or the Senior Accounting Officer." Documented ownership becomes evidence of good governance during an audit.

Step 4 — Use MTD-compliant software and digital record-keeping

The right MTD-compliant software removes a significant source of manual error from your VAT process. These tools:

- Automate record-keeping to eliminate manual data entry

- Submit returns digitally

- Reduce manual transcription errors

HMRC maintains a digital software directory with options for businesses of different sizes.

Step 5 — Review and test controls regularly

A VAT control framework is not a one-time exercise. Controls should be:

- Tested periodically (quarterly or annually)

- Reviewed when business circumstances change (new markets, payment systems)

- Updated to reflect HMRC guideline changes

As transaction volumes grow or business structures become more complex, internal reviews alone may not be sufficient. Businesses at that stage often find it practical to work with a specialist VAT compliance firm — one that can both stress-test existing controls and manage ongoing filing obligations. VJM Global supports UK businesses with VAT compliance across registration, return preparation, and HMRC compliance checks, drawing on 30+ years of tax advisory experience and a track record with 250+ UK clients.

VAT Compliance Checks: What Triggers Them and How to Prepare

What a VAT compliance check involves

HMRC conducts compliance checks to verify that VAT returns match financial records, VAT refunds are legitimate, and payments are made in full and on time.

The typical process:

- Advance written notice (usually; unannounced visits reserved for suspected fraud)

- On-site visit or correspondence review

- Document inspection (invoices, returns, bank statements)

- Post-check report with findings

HMRC can make unannounced visits where fraud is suspected, but these must generally be authorised by a senior officer.

What triggers a VAT compliance check?

Common triggers include:

- Unusual spikes or drops in VAT liability

- Errors or inconsistencies in previous returns

- Large VAT refund claims relative to turnover

- Industry-specific risk profiles (e.g., e-commerce, construction, hospitality)

- Random selection as part of HMRC's broader compliance programme

HMRC uses the "Connect" data-matching system and a VAT predictive analytics model employing machine learning to identify businesses for review.

What to expect during a VAT compliance check

HMRC officers examine:

- Sales and purchase invoices

- VAT calculations and how VAT codes have been applied

- Bank statements

- Digital records and bookkeeping software

Businesses in sectors with complex VAT rules (mixed supplies, international trade) may face deeper scrutiny.

How to prepare for a VAT compliance check

Practical preparation steps:

- Organise all VAT-related documents (returns, invoices, bank statements) before the visit

- Review recent VAT submissions for errors and proactively disclose any mistakes to HMRC (voluntary disclosure typically reduces penalties)

- Ensure records are accessible and clearly labelled

- Consider having a qualified tax adviser present during the visit

- Have a documented VAT control framework in place — this is strong evidence of good governance

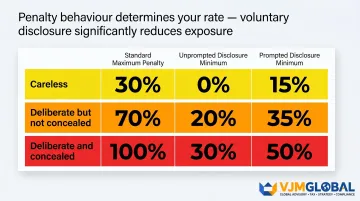

What happens if HMRC finds errors?

The business must pay any outstanding VAT plus interest. Penalties depend on whether the error was careless, deliberate, or concealed:

| Behaviour | Standard (Max) Penalty | Unprompted Disclosure (Min) | Prompted Disclosure (Min) |

|---|---|---|---|

| Careless | 30% | 0% | 15% |

| Deliberate but not concealed | 70% | 20% | 35% |

| Deliberate and concealed | 100% | 30% | 50% |

HMRC can assess VAT going back up to 4 years for innocent errors or 20 years for deliberate non-compliance. Proactive correction under VAT Notice 700/45 is preferable to waiting for a check to uncover issues. This involves adjusting the next return for errors below the relevant threshold — £10,000 or £50,000 depending on turnover.

When to Seek Professional VAT Compliance Support

Professional support adds the most value in these scenarios:

- Approaching or exceeding the £90,000 threshold for the first time

- Complex VAT positions: mixed supplies, imports/exports, partial exemption

- Rapid growth or international expansion requiring scalable compliance infrastructure

- HMRC compliance check notification received

Having a dedicated VAT specialist reduces the risk of costly errors and frees up internal resources. That makes choosing the right partner one of the more consequential decisions in your compliance setup.

What to look for in a VAT compliance partner

Key criteria include:

- Relevant experience across your industry

- Familiarity with HMRC's GfC8 framework and MTD requirements

- Transparent pricing

- Ongoing support (not just one-off filings)

VJM Global has worked with over 250 UK businesses on cross-border tax and compliance matters, including international VAT advisory for companies expanding beyond the UK. With 30+ years of Chartered Accountancy experience and a 95% client retention rate, the firm supports businesses across 15+ industries on registration, return preparation, and HMRC compliance check representation.

Frequently Asked Questions

What is VAT compliance?

VAT compliance means meeting all legal obligations related to Value Added Tax — correctly charging, recording, and remitting VAT to HMRC, filing returns on time, and maintaining adequate digital records in line with Making Tax Digital requirements.

Is VAT mandatory in the UK?

VAT registration is mandatory for businesses with taxable turnover above £90,000 in a 12-month period, but businesses below this threshold can voluntarily register. Once registered, compliance with VAT rules is a legal requirement.

What are the UK VAT rules?

Businesses must charge VAT at the correct rate (20%, 5%, or 0%), keep digital VAT records, submit quarterly returns through MTD-compliant software, and pay any VAT owed to HMRC by the due date.

What are the VAT compliance controls?

VAT compliance controls are the internal systems and checks that ensure VAT is accounted for accurately. Common examples include automated VAT code validation, invoice approval workflows, and regular VAT risk register reviews — all aligned with HMRC's GfC8 guidelines.

What triggers a VAT compliance check?

Common triggers include:

- Unusual changes in VAT liability or unexplained fluctuations

- Errors identified in previously submitted returns

- Large refund claims relative to turnover

- High-risk industry classification or random selection by HMRC

What happens during a VAT compliance check?

HMRC typically notifies the business in advance, then an officer reviews VAT records — invoices, returns, and bank statements — before issuing a report. Any errors found result in repayment of outstanding VAT plus interest, with penalties depending on the nature of the mistake.