Key Takeaways

- VAT operates in 174 countries and is not optional; failing to register when required creates back-tax liability and financial penalties

- Registration thresholds vary by country: £90,000 in the UK, AU$75,000 in Australia — non-resident sellers often face no threshold at all

- India uses GST (not VAT), with mandatory registration for non-resident businesses and e-commerce operators regardless of turnover

- EU businesses can use the One Stop Shop (OSS) to file one consolidated return for all B2C sales across member states

- Penalties range from fixed financial charges to criminal prosecution for deliberate fraud — including in the UK and across EU member states

What Is VAT Compliance and Why Does It Matter?

VAT — Value Added Tax — is a multi-stage consumption tax applied at each point in the supply chain. Unlike US sales tax, which is collected only at the final sale, VAT is charged incrementally. Businesses collect output VAT on their sales and pay input VAT on their purchases. The difference gets remitted to the tax authority. When input VAT exceeds output VAT in a period, a refund is typically owed.

VAT compliance is not a one-time registration. It is an ongoing set of obligations:

- Registering in each jurisdiction where you're required to

- Charging the correct rate on every taxable transaction

- Issuing invoices that meet local legal requirements

- Filing accurate VAT returns by fixed deadlines

- Remitting the correct tax amount to the relevant authority

According to OECD Consumption Tax Trends 2024, VAT and GST averaged 20.8% of total tax revenue across OECD countries in 2022 — making it one of the most significant revenue streams that governments actively protect and monitor.

The Digital Monitoring Shift

Tax authorities are no longer relying solely on periodic self-reporting. An OECD report on e-invoicing found 46% of surveyed tax administrations now systematically collect e-invoice data. Italy's VAT compliance gap fell from €36.3 billion (2017) to €27 billion (2019) after mandatory e-invoicing was introduced — a 26% reduction in three years.

Errors are caught faster now, and omissions are harder to conceal. Accurate invoice data and transaction records need to be built into your systems at initial setup, not treated as an afterthought.

A note on cross-border exposure: The US has no federal VAT system — sales tax applies only at the final sale. But sell goods or services into the EU, UK, or Australia, and VAT obligations in those markets apply regardless of where you're based. Similarly, businesses entering India encounter GST (Goods and Services Tax), India's equivalent multi-stage consumption tax, with its own registration thresholds, return filing cycles, and compliance requirements.

When Must a Business Register for VAT?

Registration thresholds differ significantly by jurisdiction. Here are current thresholds for the markets most relevant to internationally operating businesses:

| Jurisdiction | Threshold (Domestic Sellers) | Non-Resident Sellers |

|---|---|---|

| UK | £90,000 annual turnover | No threshold — register before first taxable sale |

| Australia | AUD $75,000 (AUD $150,000 for non-profits) | Subject to standard rules; register within 21 days |

| Ireland | €42,500 (services) / €85,000 (goods) | No threshold — register regardless of turnover |

| Germany | €25,000 previous year / €100,000 current year (small business exemption) | Stricter rules apply |

| France | €37,500–€85,000 depending on activity type | Register before making taxable supplies |

Thresholds only tell part of the story. Several scenarios trigger registration regardless of sales volume:

- Holding inventory in a foreign country's warehouse

- Importing goods into a new market

- Providing services within a country's borders

- Digital service providers (SaaS, streaming, online courses) selling to consumers — registration is typically required from the first sale, not after crossing a threshold

The Non-Resident Rule

Non-established businesses face stricter requirements in most markets. HMRC is explicit: the UK's £90,000 threshold does not apply to non-established taxable persons. Irish Revenue follows the same principle, requiring foreign sellers to register before making their first taxable supply in Ireland.

Beyond registration itself, some countries require non-resident businesses to appoint a fiscal representative: a locally licensed entity that shares legal responsibility for VAT compliance. The EU VAT Directive permits Member States to impose this requirement. Italy, for example, allows non-established businesses to comply through either direct VAT identification or a fiscal representative.

Registration can take several weeks in some jurisdictions. Starting the process before you begin selling is the only way to avoid non-compliance from day one.

Key VAT Compliance Obligations After Registration

Compliant VAT Invoicing

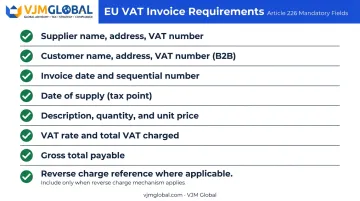

Every taxable transaction requires a VAT-compliant invoice. Under Article 226 of the EU VAT Directive, a compliant invoice must include:

- Supplier's name, address, and VAT registration number

- Customer's name, address, and VAT number (for B2B transactions)

- Invoice date and sequential invoice number

- Date of supply (tax point)

- Description, quantity, and unit price of goods or services

- Applicable VAT rate and total VAT charged

- Gross total payable

- Reference to reverse charge or other special treatments where applicable

Requirements vary by country and transaction type. B2B invoices generally carry stricter requirements than B2C. Some jurisdictions impose specific language requirements, sequential numbering rules, or mandatory invoice formats that must be followed precisely.

Filing VAT Returns

VAT returns are filed monthly, quarterly, or annually depending on the jurisdiction and business size. The filing calculates net VAT liability: output VAT collected minus input VAT paid. The resulting figure is either remitted or claimed as a refund.

E-invoicing mandates are changing the mechanics of compliance across several major jurisdictions:

- Italy: Electronic invoices must be transmitted through the government's SdI exchange system

- France: Mandatory e-invoicing starts 1 September 2026 for French-established companies

- Spain: VERI*FACTU phased deadlines begin in 2026 under Real Decreto 254/2025

Penalties for digital reporting failures are assessed separately from the underlying tax position — meaning a business can owe fines even when the tax itself was calculated and paid correctly. Verify current e-invoicing rules for each country before each filing cycle.

Paying VAT and Maintaining Records

Filing a return and paying the tax are two separate obligations — both must be executed correctly. VAT payments must be made in local currency via approved methods, by deadlines aligned with each return period.

An incorrect payment reference or wrong bank account can cause the payment to be unmatched to the filed return. That counts as a compliance failure even when the underlying tax was calculated correctly.

Record retention requirements also vary, and tax authorities expect records to be immediately available on audit request:

- UK: VAT records must be kept for at least 6 years

- Australia: Most business records must be retained for 5 years

- EU Member States: Retention periods typically range from 5 to 10 years, set individually by each country under the VAT Directive

Records must be produced on request during a tax audit. That includes invoices issued and received, return filings, payment confirmations, and correspondence with tax authorities.

VAT vs. GST: What Businesses Expanding to India Need to Know

India operates a Goods and Services Tax (GST) system rather than a traditional VAT. The structure has three components:

- CGST (Central GST) — applies to intra-state supplies, collected by central government

- SGST (State GST) — applies to intra-state supplies, collected by state government

- IGST (Integrated GST) — applies to inter-state transactions, equal to CGST plus SGST combined

Main GST rate slabs are 5%, 12%, 18%, and 28%, with nil and exempt categories for specific goods and services.

Registration Thresholds and Mandatory Categories

The standard GST registration threshold is INR 20 lakh aggregate annual turnover (INR 10 lakh in special category states). For exclusive goods supply, higher thresholds of INR 40 lakh apply in some cases.

However, several categories must register regardless of turnover under Section 24 of the CGST Act — and this is where many foreign businesses get caught out:

- Non-resident taxable persons making taxable supplies

- E-commerce operators required to collect tax at source

- Businesses involved in inter-state supply of goods or services

- Suppliers of OIDAR services (Online Information and Database Access or Retrieval) to Indian consumers

- Businesses under Reverse Charge Mechanism liability

This means US, UK, and Australian SaaS companies, digital platforms, and e-commerce operators entering India must register for GST from day one — no turnover threshold applies.

India's CGST Act imposes a penalty of INR 10,000 or the tax evaded — whichever is higher for failure to register when legally required. India's CGST Act imposes a penalty of INR 10,000 or the tax evaded — whichever is higher for failure to register when legally required. The European Commission's VAT gap data confirms similar non-compliance costs across comparable indirect tax systems globally.

VJM Global has helped 500+ American, 250+ UK, and 250+ Australian businesses navigate India's GST framework over 30+ years. GST support covers:

- Registration and return filing (GSTR-1, GSTR-3B, GSTR-9/9C)

- Input tax credit (ITC) reconciliation and maximization

- Reverse Charge Mechanism compliance

- Audit certification for businesses above the INR 2 crore threshold

- Representation before GST authorities

Cross-Border VAT Compliance: Selling Internationally

B2B vs. B2C — the Fundamental Distinction

When you sell to a VAT-registered business in another country (B2B), the reverse charge mechanism typically applies. The buyer accounts for VAT in their own country; you don't collect it. When you sell to consumers (B2C), you're generally responsible for charging VAT at the customer's local rate — which can mean registration obligations across multiple jurisdictions at once.

EU Simplification Schemes

The EU offers two schemes that reduce compliance burden for qualifying businesses:

- One Stop Shop (OSS): Allows businesses to file a single VAT return covering all EU B2C sales, rather than registering separately in each member state. The threshold for covered intra-EU B2C sales is €10,000 EU-wide. By end-2024, over 170,000 traders had registered across OSS and IOSS schemes.

- Import One Stop Shop (IOSS): Available for non-EU sellers shipping goods valued under €150 to EU consumers. Simplifies VAT declaration and payment for qualifying distance sales.

These schemes reduce filing burden but don't remove the need for correct product classification, customer location evidence, and compliant invoice records.

The UK, however, sits outside this EU framework entirely. After Brexit, the UK established its own separate VAT rules with no equivalent of the OSS. Overseas sellers shipping goods to UK customers must account for UK VAT directly, often through marketplace liability rules that apply to sales made via online platforms.

Digital Services — No Threshold for Non-Residents

Businesses selling digital services to consumers in most VAT-implementing countries must register and charge local VAT from the first sale — there is no de minimis threshold for non-resident providers. This applies to:

- Software and SaaS subscriptions

- Streaming content and digital media

- Online courses and e-learning platforms

- Any other electronically supplied service

The result is potential registration obligations across dozens of jurisdictions at once, making this one of the most complex compliance scenarios for international digital businesses.

Penalties for VAT Non-Compliance

The financial consequences of non-compliance scale quickly. The table below summarizes key penalties across the three jurisdictions most relevant to businesses with cross-border exposure:

| Jurisdiction | Key Penalty Trigger | Financial Penalty | Criminal Exposure |

|---|---|---|---|

| UK | Late returns accumulate points; 2 (annual), 4 (quarterly), or 5 (monthly) triggers first penalty | £200 fixed penalty per breach + daily interest on late payments | VAT Act 1994 Section 72: unlimited fine or up to 14 years imprisonment |

| Australia | Failure to lodge within 28-day windows | General Interest Charge (compounding daily) on unpaid liabilities | Serious fraud cases referred to the Australian Federal Police |

| India | Non-registration when liable (CGST Section 122) | INR 10,000 or the tax evaded (whichever is higher); Section 47 late fees: INR 100/day, capped at INR 5,000 | Prosecution for willful evasion under CGST Act Section 132 |

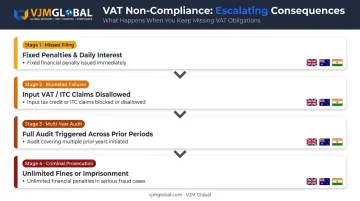

What Persistent Non-Compliance Triggers

Beyond financial penalties, tax authorities can:

- Disallow input VAT or ITC claims entirely

- Conduct full audits covering multiple prior periods

- In serious cases, pursue criminal prosecution

A single missed filing can open a multi-year audit window. Authorities rarely limit their review to the period in question — catching one error often prompts scrutiny of prior returns as well. Resolving issues before they escalate is consistently cheaper and less disruptive than responding to enforcement action.

Practical steps to stay compliant:

- Register before crossing thresholds — or before the first sale where required

- Use accounting systems that track output and input VAT accurately by jurisdiction

- Set calendar reminders for all filing and payment deadlines

- Keep documentation organised and audit-ready at all times

- Work with a specialist compliance advisor when entering new markets

VJM Global supports businesses entering India across each of these steps — from GST registration and return filing through audit certification and ITC optimization.

Frequently Asked Questions

Do I charge VAT to American customers?

The US has no federal VAT system, so American customers are not charged VAT in the way EU or UK customers are. If you're VAT-registered in a VAT-implementing country and exporting goods to the US, the transaction is typically zero-rated — meaning VAT applies at 0%, so you report it but don't collect it from the customer.

What is the difference between VAT and GST?

VAT and GST are both multi-stage consumption taxes collected at each point in the supply chain. The key difference is structural: India uses GST with distinct central (CGST), state (SGST), and integrated (IGST) components, while the EU, UK, and Australia use VAT or a simpler single-rate GST.

How often do businesses need to file VAT returns?

Filing frequency varies by country and sometimes by business size. Most jurisdictions require monthly or quarterly filings, with annual filing available for smaller businesses in some markets. Late filings attract penalties even when the underlying tax has already been paid, so deadlines must be treated as non-negotiable.

Can a business reclaim VAT paid on purchases?

Yes. VAT-registered businesses can offset input VAT — the VAT paid on business purchases — against output VAT collected on sales. If input VAT exceeds output VAT in a given period, the business can usually claim a refund from the tax authority. The reclaim must be supported by compliant purchase invoices.

What happens if a business doesn't register for VAT when required?

Failing to register when legally required creates back-tax liability for all VAT that should have been collected since the trigger date, plus interest and penalties. Tax authorities can also disallow input VAT claims and conduct multi-year audits — with business operations suspended in serious cases.

What must be included on a VAT invoice?

Core requirements include the seller's name, address, and VAT number; buyer's name, address, and VAT number (for B2B); invoice date and sequential number; tax point date; description and quantity of goods or services; the VAT rate applied; total VAT charged; and the gross total. Requirements vary by country and transaction type; always verify local invoice rules in each jurisdiction where you hold a VAT registration.