Introduction

UAE VAT compliance is a mandatory legal and financial obligation for all qualifying businesses operating in or from the UAE, governed by Federal Decree-Law No. 8 of 2017 and administered by the Federal Tax Authority (FTA). Since its introduction on 1 January 2018, the 5% value-added tax has fundamentally changed how businesses structure transactions, maintain records, and report to authorities.

This guide is written for businesses newly entering the UAE market, foreign companies, SMEs, and multinational operators who find the rules difficult to navigate in practice. Common pressure points include registration thresholds, taxable versus exempt supply classification, reverse charge mechanisms, and penalties that exceed AED 10,000 for late registration alone.

The FTA conducted 176,000 field inspections in 2025, an 89% increase from 2024. That enforcement trajectory makes proactive compliance a business priority, not just a legal formality.

This article explains how UAE VAT works, who must register, how returns are filed, and what non-compliance costs. Whether you're a US-based company expanding into Dubai or an Australian services provider assessing your obligations, you'll leave with a practical compliance roadmap — not guesswork.

Key Takeaways

- UAE VAT is charged at 5% on most goods and services, with exports and certain healthcare/education supplies zero-rated (0%)

- Businesses with taxable supplies exceeding AED 375,000 annually must register within 30 days; voluntary registration available from AED 187,500

- Returns are filed quarterly via the FTA portal, with payment due by the 28th of the month following each quarter

- Penalties for non-compliance include AED 1,000 for a first late filing and AED 10,000 for late registration

- Unpaid VAT attracts 14% per annum interest starting April 2026

- Foreign companies operating in the UAE must appoint a local fiscal representative — no registration threshold exemption applies

What Is UAE VAT?

UAE VAT is an indirect consumption tax levied at each stage of the supply chain, from production through distribution, with the final tax burden falling on the end consumer. Introduced on 1 January 2018 under Federal Decree-Law No. 8 of 2017, it was designed to diversify government revenue beyond oil dependency.

The UAE Ministry of Finance confirms the standard rate has held at 5% since implementation, giving the UAE one of the lowest VAT rates globally.

The Federal Tax Authority (FTA) administers the system under implementing regulations set out in Cabinet Decision No. 52 of 2017.

VAT Treatment Categories

Standard-rated (5%): Most goods and services supplied in the UAE carry the standard 5% rate. This includes retail sales, restaurant meals, professional services, telecommunications, and commercial real estate leasing.

Zero-rated (0%): Taxable supplies charged at 0% — businesses can reclaim input VAT on related purchases:

- Exports of goods outside the GCC member states

- International transport and related supplies

- Aircraft and ships of certain specifications

- Investment-grade precious metals (gold, silver of 99%+ purity)

- First supply of newly constructed residential properties (within three years of completion)

- Qualifying healthcare services and related goods

- Qualifying education services and related goods

Exempt supplies: No VAT is charged, and input VAT on related purchases cannot be recovered:

- Most financial services (not charged via explicit fee)

- Sale or lease of residential buildings (except first supply)

- Bare land (land without buildings or civil engineering works)

- Domestic passenger transport within the UAE

VAT vs. Corporate Tax

UAE VAT is transaction-level tax on supplies, not a tax on business profits. This distinction matters: you file separate VAT returns and Corporate Tax returns, maintain separate records, and face different compliance deadlines. A business can be VAT-registered but not subject to Corporate Tax (and vice versa). Both are administered by the FTA but operate under different legal frameworks—VAT under Federal Decree-Law No. 8 of 2017, Corporate Tax under Federal Decree-Law No. 47 of 2022.

UAE VAT Registration: Who Must Register and How

Mandatory Registration

Businesses resident in the UAE whose taxable supplies and imports exceed AED 375,000 in the previous 12 months, or are expected to exceed this threshold within the next 30 days, must apply for VAT registration within 30 days. The FTA states explicitly that this 30-day window starts from the date the threshold is crossed. Missing this deadline triggers a penalty of AED 10,000—an amount many new businesses discover only during their first FTA audit.

Voluntary Registration

Businesses whose taxable supplies or taxable expenses exceed AED 187,500 (measured over the past 12 months or expected within the next 30 days) may choose to register voluntarily. Benefits include:

- Reclaiming input VAT on business purchases and expenses

- Enhanced credibility with suppliers and customers

- Stronger standing when bidding on tenders and government contracts that require VAT-registered vendors

Foreign (Non-Resident) Businesses

No registration threshold applies to non-resident businesses. Any foreign company making taxable supplies in the UAE must register from the first dirham of taxable supply. Non-residents must also appoint a UAE fiscal representative who shares joint and several liability for VAT compliance. The representative must be UAE-resident and FTA-approved.

Single FTA Account Requirement

Once you understand which registration category applies to your business, the next step is managing your FTA account correctly. Businesses already registered for UAE Corporate Tax must use the same FTA portal account for VAT registration. Creating separate FTA accounts is a common and costly error — it creates duplicate compliance obligations and can delay refunds.

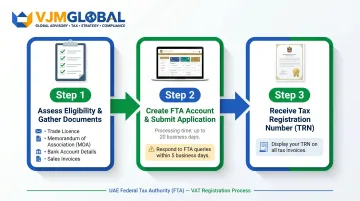

Step 1: Assess Eligibility and Gather Documents

Before applying, assess your taxable supply threshold and prepare required documents:

- Valid trade licence and incorporation certificate

- Memorandum of Association (MOA) or partnership agreement

- Passport and Emirates ID copies for all shareholders and authorised signatories

- UAE bank account details

- Monthly turnover report or declaration letter stating total taxable supplies

- Business flowchart showing supply chain structure

- Sample invoices, contracts, or purchase orders

File formats: PDF or DOC, maximum 15 MB per document.

Step 2: Create an FTA Account and Submit the Application

Register via the FTA e-services portal:

- Create an account using valid Emirates ID or passport

- Complete the VAT registration application with full accuracy

- Upload required documents in the prescribed format

- Submit and note your application reference number

The FTA typically takes up to 20 business days to process applications and may request additional information or clarification. Aim to respond to any FTA queries within 5 business days — unresolved requests can stall your application and push back your effective registration date.

Step 3: Receive Your Tax Registration Number (TRN)

Once approved, you receive a Tax Registration Number (TRN) and VAT registration certificate. After receiving your TRN, take these immediate steps:

- Display your TRN on all tax invoices from the effective registration date

- Update your accounting system and invoice templates to include the TRN

- Inform existing customers of your VAT-registered status

Failure to display your TRN correctly can result in rejected input VAT claims by your customers and penalties of AED 2,500 per non-compliant invoice under the updated penalty regime.

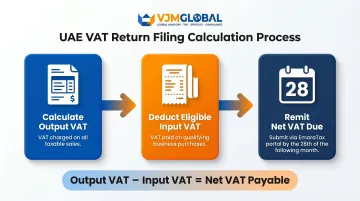

How UAE VAT Returns Are Filed

Every VAT return requires your business to complete four core tasks:

- Report all taxable sales and purchases for the period

- Calculate output VAT collected from customers

- Deduct eligible input VAT paid on business purchases

- Remit the net difference to the FTA

Returns are filed quarterly for most businesses, though the FTA may assign monthly filing to certain large taxpayers.

Returns and payments are due by the 28th of the month following the end of the reporting period. All submissions must be made electronically through the EmaraTax portal. Even businesses with nil activity must file a return for each tax period.

Step 1: Calculate Output VAT

Output VAT is the VAT you charge on taxable supplies made to customers.

Example: If your business invoices AED 500,000 in taxable sales at the standard 5% rate, output VAT = AED 500,000 × 5% = AED 25,000.

Step 2: Determine Eligible Input VAT

Input VAT is the VAT you pay on purchases and expenses related to taxable business activities. Not all input VAT is recoverable — Article 53 of the Executive Regulations blocks specific categories:

- Entertainment costs for non-employees

- Motor vehicles available for personal use

- Employee personal benefits not required for business

- Non-business expenses

To claim any input VAT, you must hold a valid tax invoice showing the supplier's TRN, a description of the goods or services, and the VAT amount stated separately.

Step 3: Submit the Return and Pay the Net VAT Due

Net VAT payable = Output VAT minus eligible input VAT. Submit this amount through the EmaraTax portal by the 28th of the following month.

If input VAT exceeds output VAT, you can carry forward the excess to the next period or apply for a refund. Note that Cabinet Decision amendments effective 1 January 2026 introduce a five-year time limit on excess input VAT refund claims — any refund request must be filed within five years from the end of the relevant tax period.

Ongoing VAT Compliance Obligations

Record-Keeping Requirements

UAE VAT law requires businesses to retain all tax-related records for specified periods:

- General VAT records (invoices, returns, accounting ledgers): 5 years

- Capital asset records: 10 years

- Real estate-related records: 15 years

Records must be stored in a format that allows the FTA to access and audit them. Failure to maintain adequate records triggers penalties starting at AED 1,000 per violation (first offence) and AED 20,000 for repeat violations.

VAT-Compliant Invoicing

Every tax invoice must include:

- Supplier name and TRN

- Buyer details (including TRN if registered)

- Description of goods or services

- VAT-exclusive amount

- VAT amount separately stated

- Total VAT-inclusive value

- Date of supply and invoice number

Missing elements can result in rejected input VAT claims for your customer and penalties for your business. Under Cabinet Decision No. 129 of 2025 (effective 14 April 2026), non-compliant invoices carry a penalty of AED 2,500 each.

VAT Health Checks and Technology

Conducting periodic internal VAT reviews or engaging external VAT health checks helps identify gaps before the FTA does. The FTA's enforcement surge—from 93,000 inspections in 2024 to 176,000 in 2025—means audit risk is rising sharply.

Using FTA-accredited accounting software automates VAT calculations, reduces human error, and positions your business for mandatory e-invoicing.

Ministerial Decision No. 244 of 2025 mandates e-invoicing in phases:

- Pilot phase: July 2026

- Businesses with revenue ≥ AED 50M: Live by January 2027

- All other businesses: Live by July 2027

Businesses must appoint an Accredited Service Provider (ASP) by the applicable deadline or face penalties of AED 5,000 per month. For businesses with operations across multiple jurisdictions, working with advisors who understand both UAE VAT and the tax frameworks of other markets—such as India or the UK—can help ensure nothing falls through the gaps.

VAT Grouping

Two or more UAE businesses under common ownership or control (owning more than 50% of shares or voting rights) can form a VAT group under Article 14 of the Decree-Law. This enables:

- A single consolidated VAT return

- Intra-group transactions treated as outside the scope of VAT

- Simplified compliance for multi-entity structures

VAT grouping rules differ from Corporate Tax grouping rules and the two may not always align—separate applications and approvals are required.

Common UAE VAT Mistakes and Misconceptions

Registration and Threshold Errors

Many businesses fail to monitor turnover against the AED 375,000 threshold continuously, resulting in delayed mandatory registration and exposure to the AED 10,000 late registration penalty.

Free zone misconception: A common error is assuming that free zone entities are automatically exempt from VAT. While goods transfers between Designated Zones may fall outside VAT scope, most service transactions within free zones remain subject to the standard 5% rate. The FTA's Designated Zones Guide clarifies that services supplied within Designated Zones are taxable unless a specific exemption applies.

Incorrect Rate Classification and Input VAT Claims

Misapplying VAT rates—treating a standard-rated supply as zero-rated or exempt—creates both under-reporting and over-claiming risks. Common errors include:

- Claiming input VAT on blocked expenses (entertainment, personal vehicle use)

- Failing to hold valid tax invoices to support input VAT claims

- Recovering VAT on expenses not related to taxable business activities

Input VAT claims must be backed by compliant tax invoices and must relate directly to making taxable supplies.

Reverse Charge Mechanism Misunderstanding

When UAE-registered businesses import goods or services from outside the GCC, the reverse charge mechanism shifts VAT reporting responsibility from the overseas supplier to the UAE buyer. The buyer must self-account for VAT in their own return—reporting it as both output VAT and (where eligible) input VAT.

For fully taxable businesses, this mechanism is cash-flow neutral—you report and recover the same amount. The real risk is ignoring it entirely: many businesses simply pay the foreign supplier without recognising that UAE VAT is still due on their end.

On documentation, a KPMG summary of FTA Public Clarification No. 44 (May 2025) notes that a self-tax invoice is no longer required if you hold a supplier invoice reflecting service details and consideration paid.

Penalty Overview

| Violation | Penalty (from 14 April 2026) |

|---|---|

| Late registration | AED 10,000 |

| Late filing (first offence) | AED 1,000 |

| Late filing (repeat within 24 months) | AED 2,000 |

| Late payment | 14% per annum (monthly calculation) |

| Non-compliant tax invoice | AED 2,500 per invoice |

The updated structure replaces the old compounding monthly interest model (2% + 4%/month) with a flat 14% per annum—reducing cumulative exposure over time, but only if payment is made promptly. Delays still add up quickly.

Frequently Asked Questions

How do you typically handle VAT filing and compliance in the UAE?

VAT filing is managed through the FTA's EmaraTax portal on a quarterly basis. Businesses calculate output VAT collected, deduct eligible input VAT on expenses, and remit the net balance by the 28th of the following month. Most use FTA-accredited accounting software or appoint a tax agent for accuracy.

What are the rules for VAT in UAE?

UAE VAT is set at 5% on most goods and services under Federal Decree-Law No. 8 of 2017. Businesses exceeding AED 375,000 in taxable supplies must register, file periodic returns, issue compliant invoices, maintain records for at least five years, and remit net VAT to the FTA by the 28th of the month following each tax period.

Is VAT mandatory in Dubai?

Yes, VAT applies across all Emirates including Dubai as a federal tax. Businesses in Dubai with taxable supplies exceeding AED 375,000 are legally required to register and comply. Being in a Dubai free zone does not automatically exempt a business from UAE VAT obligations—most services remain subject to the standard 5% rate.

What is the penalty for late VAT filing in the UAE?

The first late filing offence carries a fixed penalty of AED 1,000, rising to AED 2,000 for repeat violations within 24 months. Unpaid VAT also attracts interest of 14% per annum (calculated monthly) under the revised penalty regime effective 14 April 2026, replacing the previous 2% + 4%/month structure.

Can a business voluntarily register for VAT in the UAE?

Yes, businesses whose taxable supplies or expenses exceed AED 187,500 in the past 12 months or are expected to within the next 30 days can voluntarily register. Voluntary registration allows the business to reclaim input VAT on purchases and strengthens credibility with B2B clients and supply chain partners.

What is the reverse charge mechanism in UAE VAT?

The reverse charge mechanism applies when a UAE-registered business receives goods or services from a supplier outside the GCC. Instead of the foreign supplier charging UAE VAT, the UAE buyer self-accounts for it in their own return, reporting it as both output and (where eligible) input VAT.