Introduction

Managing multiple subsidiaries across different jurisdictions is a common challenge for UK parent company directors. Each entity produces its own financial statements, but these individual reports don't reveal the group's true financial health or economic power.

If you control subsidiaries in India, the US, or elsewhere, you're juggling separate balance sheets, profit statements, and compliance obligations — none of which show what the group actually owns or owes as a whole.

Consolidated accounts combine a parent company and all its subsidiaries into one set of financial statements, treating the entire group as a single economic unit. This guide covers when UK law requires them, what they include, key concepts such as goodwill and non-controlling interests, and the common pitfalls to avoid when preparing them.

Key Takeaways

- Consolidated accounts merge a parent company and all subsidiaries into unified financial statements, eliminating internal transactions to show the group's true position

- Section 399 of the Companies Act 2006 requires group accounts unless you meet the small group exemption (£15m turnover, £7.5m balance sheet, or 50 employees) from April 2025

- Key processes include removing intra-group transactions, calculating acquisition goodwill, and recognising minority interests separately

- All subsidiaries under a UK-registered parent must be consolidated, including overseas ones, with only very limited exclusions permitted

What Are Consolidated Accounts?

Consolidated accounts are financial statements that combine the finances of a parent company and all its subsidiaries into a single set of reports. Instead of treating each entity as separate, consolidation presents the group as one economic unit.

Without consolidated accounts, owning three subsidiaries means four separate sets of reports—but no unified view of the group's total resources, debts, or profitability. Consolidated accounts bridge that gap by aggregating everything the parent controls and stripping out internal activity.

Under UK law, these are referred to as "group accounts." The Companies Act 2006, Section 399, requires directors of any parent company to prepare group accounts alongside individual accounts for each entity—both obligations are mandatory, not alternative.

Individual vs. Consolidated Accounts

Individual company accounts remain a legal requirement for each entity under Section 394 of the Companies Act 2006. These are filed at Companies House and show each company's standalone position.

Consolidated accounts go further: they show the group's combined position after removing internal transactions. For example, if the parent lends £500,000 to a subsidiary, that loan appears as an asset in the parent's individual accounts and a liability in the subsidiary's. In the consolidated accounts, both entries are eliminated—because from the group's perspective, you can't owe money to yourself.

The Group as a Single Reporting Entity

Consolidation treats the parent and all subsidiaries as if they were one business. Assets, liabilities, income, and expenses are added together line by line. Transactions between group members—intercompany sales, loans, management charges, or dividends—are stripped out to avoid double-counting.

The result is a set of accounts that reflects only transactions with external parties: customers, suppliers, lenders, and other third parties outside the group.

Applicable Accounting Frameworks

How those eliminations are calculated depends on which accounting framework applies. Two main frameworks govern UK consolidated accounts:

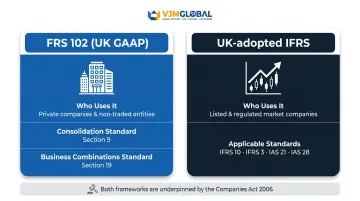

| Framework | Who uses it | Consolidation standard |

|---|---|---|

| FRS 102 (UK GAAP) | Private companies and non-traded entities | Section 9 (consolidation), Section 19 (business combinations) |

| UK-adopted IFRS | Companies with securities on a UK regulated market (mandatory) | IFRS 10, IFRS 3, IAS 21, IAS 28 |

FRS 102 applies to most UK private companies. UK-adopted IFRS is mandatory for listed companies and may be used voluntarily by others. Both frameworks are underpinned by legal requirements in the Companies Act 2006, which apply regardless of the framework chosen.

When Do UK Companies Need to Prepare Consolidated Accounts?

Legal Obligation Under Section 399

Section 399(2) of the Companies Act 2006 places a mandatory duty on directors: if your company is a parent at the end of the financial year, you must prepare group accounts. This applies to all parent companies unless an exemption is available.

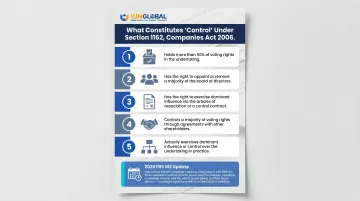

What Constitutes "Control"?

Under Section 1162 of the Companies Act 2006, a company is a parent if it meets any of these criteria:

- Holds more than 50% of voting rights in another entity

- Has the right to appoint or remove a majority of the board of directors

- Exercises dominant influence through the articles or a control contract

- Controls a majority of voting rights through agreements with other shareholders

- Actually exercises dominant influence or manages the subsidiary on a unified basis

Important change from 2026: FRS 102 amendments effective 1 January 2026 align the UK GAAP definition of control with IFRS 10's three-element model: power over the investee, exposure to variable returns, and the ability to use that power to affect those returns. This change applies retrospectively — review your group structure now to identify any investees whose consolidation status may shift.

Small Group Exemption (Updated April 2025)

A group qualifies as "small" and is exempt from preparing consolidated accounts if it meets at least two of these three conditions:

- Aggregate turnover not exceeding £15 million net (£18 million gross)

- Aggregate balance sheet total not exceeding £7.5 million net (£9 million gross)

- Average number of employees not exceeding 50

These thresholds increased by approximately 50% under SI 2024/1303 and apply to financial years beginning on or after 6 April 2025. Early adoption was permitted from 1 January 2024.

Key exclusions: Traded companies, authorised insurance companies, banking companies, e-money issuers, MiFID investment firms, and UCITS management companies cannot claim the small group exemption, regardless of size.

Other Exemptions from Consolidation

Section 400 – Subsidiary exemption: A UK subsidiary is exempt from preparing group accounts if it is already included in a parent's consolidated accounts prepared under IFRS or equivalent, provided those accounts are publicly available and filed with Companies House.

Section 401 – Non-UK parent exemption: Similar exemption available where a non-UK parent prepares consolidated accounts in accordance with UK-adopted IFRS or equivalent standards and makes them publicly available.

Sections 400 and 401 exempt the entire group from consolidation. Section 405 works differently — it allows specific subsidiaries to be excluded from an otherwise consolidated set of accounts. The permitted grounds are:

- Excluded if inclusion would not be material for a true and fair view (note: two or more individually immaterial subsidiaries may be material in aggregate and must be included)

- Excluded where severe long-term restrictions substantially hinder the parent's rights over assets or management

- Excluded where the interest is held exclusively with a view to subsequent disposal

- Excluded in extremely rare cases where obtaining the required information would cause disproportionate expense or delay

The International Angle: Overseas Subsidiaries

One point that catches many directors off guard: if a company is registered in the UK, its overseas subsidiaries — including those in India, the US, or anywhere else — must be included in the consolidated financial statements.

There is no geographic exclusion for foreign subsidiaries under Section 405(1) or FRS 102 Paragraph 9.2. The requirement to consolidate "all subsidiaries" applies worldwide. The only route to exclusion is one of the narrow Section 405 grounds described above.

For UK businesses managing subsidiaries in India, this means local statutory compliance and UK group reporting must run in parallel. VJM Global works with UK parent companies to handle entity-level accounting in India and produce figures ready for inclusion in UK consolidated accounts.

What Is Included in Consolidated Accounts?

A complete set of consolidated financial statements comprises four main statements plus supporting notes:

The Four Core Financial Statements

1. Consolidated Statement of Financial Position (Balance Sheet)

Lists combined group assets, liabilities, and equity at the reporting date. Intra-group balances — such as intercompany loans, receivables, and payables — are eliminated, so only amounts owed to or by external parties appear.

2. Consolidated Statement of Profit or Loss (Income Statement)

Records combined group revenue and expenses for the period, with intra-group sales and purchases removed. For example, if the parent sells £200,000 of goods to a subsidiary, that transaction appears as revenue in the parent's individual accounts and cost of sales in the subsidiary's. In the consolidated statement, both entries are stripped out entirely.

3. Consolidated Statement of Cash Flows

Tracks money moving in and out of the group from operations, investing, and financing activities. Intra-group cash transfers — such as dividends paid by a subsidiary to the parent — are eliminated so only external cash flows remain.

4. Consolidated Statement of Changes in Equity

Captures how retained earnings, share capital, reserves, and other equity components have moved across the group during the period. Dividends paid between group companies are excluded.

Accompanying Notes

FRS 102 (the UK accounting standard) Section 8 and Schedule 1 of the Companies Act 2006 require detailed notes covering:

- Accounting policies applied

- Significant judgements and estimates

- Details of subsidiaries included (names, ownership percentages, principal activities)

- Goodwill recognised on acquisition

- Non-controlling interests

- Related party transactions with external parties

What Gets Eliminated?

Every consolidation removes internal activity to prevent the same transaction being counted twice. Here's what gets cut:

From the balance sheet:

- Intercompany receivables and payables

- Loans between group companies

- Investments in subsidiaries (replaced by the subsidiary's underlying assets and liabilities)

From the profit and loss:

- Intra-group sales and purchases

- Management charges between group entities

- Interest on intercompany loans

- Dividends paid by subsidiaries to the parent

Unrealised profits: If the parent sells inventory to a subsidiary for £100,000 (which cost the parent £80,000) and the subsidiary hasn't yet sold those goods externally, the £20,000 profit is unrealised from the group's perspective. That profit is stripped out of the consolidated inventory value.

Key Concepts Every Beginner Needs to Understand

Intra-Group Eliminations

Intra-group eliminations are central to consolidation. Any transaction between companies within the same group is internal activity that does not represent income or expenditure from the group's perspective.

Why it matters: Including internal transactions would artificially inflate revenue, assets, or liabilities. For example, if the parent sells services to five subsidiaries for £50,000 each, that's £250,000 of internal revenue. In the consolidated accounts, this £250,000 must be removed—because the group hasn't earned anything from external customers.

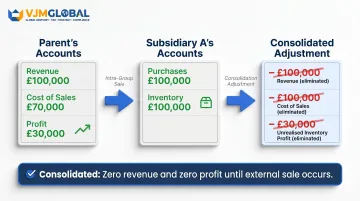

Worked example:

Parent sells goods to Subsidiary A for £100,000. The goods cost the parent £70,000 to produce.

- In the parent's individual accounts: Revenue £100,000, Cost of sales £70,000, Profit £30,000

- In Subsidiary A's individual accounts: Purchases £100,000, Inventory £100,000 (if not yet sold externally)

- Consolidated adjustment: Remove £100,000 from revenue and £100,000 from cost of sales (intercompany sale). Remove £30,000 from inventory value (unrealised profit). The consolidated accounts show zero revenue and zero profit until Subsidiary A sells the goods to an external customer.

Goodwill

Goodwill arises when a parent acquires a subsidiary and pays more than the fair value of its identifiable net assets. It represents the premium paid for intangible factors — such as brand reputation, customer relationships, and workforce expertise — that cannot be separately identified on a balance sheet.

How goodwill is treated under FRS 102 (UK GAAP):

Goodwill is capitalised as an intangible asset and amortised over its useful economic life. If you cannot reliably estimate the useful life, the maximum period is 10 years (FRS 102 Paragraph 19.23).

The FRC retained this amortisation model in its 2024 periodic review, rejecting the IFRS impairment-only approach. The 10-year maximum remains unchanged. Amendments are effective for periods beginning on or after 1 January 2026, with early adoption permitted.

Key changes from 2026:

- Acquisition-related costs (legal fees, advisory costs) must be expensed in the period incurred — not capitalised into goodwill

- Contingent consideration must be measured at fair value, with subsequent changes recognised through profit or loss

How goodwill is treated under UK-adopted IFRS:

Goodwill is recognised at cost less accumulated impairment losses. There is no amortisation. Instead, goodwill must be tested for impairment annually (or more frequently if indicators exist) under IAS 36.

Negative Goodwill (Bargain Purchase)

Negative goodwill arises when the purchase price paid is less than the fair value of the net assets acquired — a bargain purchase.

| Framework | Treatment |

|---|---|

| FRS 102 | Recognised on the balance sheet below goodwill and released systematically to income over the periods expected to benefit |

| IFRS 3 | Recognised immediately as a gain in profit or loss on the acquisition date, after reassessing that all assets and liabilities have been correctly identified |

The treatment difference has a direct impact on reported profit in the year of acquisition.

Non-Controlling Interest (NCI)

When a parent owns less than 100% of a subsidiary, the remaining ownership belongs to outside shareholders. This minority share is called the non-controlling interest.

Example: If the parent owns 80% of Subsidiary B, the other 20% is the NCI.

How NCI is presented:

- Shown within equity on the balance sheet, separately from the parent shareholders' equity

- Split out in the income statement, distinguishing profit attributable to parent shareholders from profit attributable to NCI

Under both FRS 102 (Para 9.20–9.22) and IFRS 10, NCI must be recognised and disclosed separately.

Uniform Accounting Policies

FRS 102 Para 9.17 requires that all entities within the group use the same accounting policies for like transactions and similar events.

Why it matters: If the parent depreciates machinery over 10 years but a subsidiary depreciates similar machinery over 5 years, the group's asset values and profit are inconsistent. Before consolidation, the subsidiary's figures must be adjusted to align with group policy.

If adjustment is impracticable: The differences must be fully disclosed in the notes to the accounts.

Accounting Period Alignment

Group accounts should ideally be prepared to the same period-end date. However, FRS 102 Para 9.16 permits the use of a subsidiary's financial statements with a reporting date up to three months before or after the parent's year-end, provided adjustments are made for significant transactions or events in the intervening period.

Practical application: If a UK parent reports to 31 December but an Indian subsidiary reports to 31 March (the Indian financial year-end), the parent may use the subsidiary's 31 March accounts when consolidating for the year ended 31 December—provided material transactions between April and December are adjusted.

This flexibility is particularly relevant for overseas subsidiaries with different local year-ends.

How to Prepare Consolidated Accounts: A Step-by-Step Overview

Step 1 — Gather and Verify Entity-Level Trial Balances

Before any consolidation work begins, ensure each subsidiary's trial balance is accurate, complete, and reconciled to the same reporting date (or within the permitted three-month window, with adjustments).

Critical checks at this stage:

- Balances agree to underlying ledgers

- Intercompany accounts are reconciled between entities

- All transactions are recorded in the correct period

- Accounting policies align with group policies

Any discrepancy at entity level will cause reconciliation problems across the group. Resolve differences now, not at year-end.

Step 2 — Combine and Eliminate

Start by adding together the assets, liabilities, income, and expenses of the parent and all subsidiaries line by line. Then apply consolidation adjustments to eliminate intra-group activity:

- Remove the parent's investment in each subsidiary against that subsidiary's share capital and reserves

- Eliminate all intra-group balances (receivables, payables, loans)

- Remove intra-group sales, purchases, and other transactions

- Strip out unrealised profits on intra-group transactions

- Calculate goodwill arising on each acquisition

Step 3 — Recognise Goodwill, NCI, and Policy Adjustments

Goodwill is calculated as the fair value of consideration paid, less the fair value of identifiable net assets acquired. Negative goodwill arises where the net assets exceed the purchase price.

Non-controlling interests (NCI) are recognised based on the subsidiary's net assets and profit attributable to minority shareholders, presented separately in equity and profit/loss.

Before finalising the numbers, confirm policy alignment across all entities — consistent depreciation methods, revenue recognition, and other key policies. Adjust any subsidiary figures that deviate from group policy.

Step 4 — Produce the Consolidated Statements

With adjustments complete, prepare the four consolidated statements:

- Consolidated statement of financial position

- Consolidated statement of profit or loss

- Consolidated statement of cash flows

- Consolidated statement of changes in equity

Supporting notes should cover accounting policies, significant judgements, details of subsidiaries, goodwill, NCI, and related party transactions.

Cross-border groups add another layer of complexity. UK parent companies with subsidiaries in India, the US, or Australia must also satisfy local statutory requirements alongside group reporting obligations under FRS 102 or IFRS. VJM Global's accounting outsourcing and advisory services are designed to support exactly that kind of multi-jurisdiction compliance.

Common Challenges When Preparing Consolidated Accounts

Intra-Group Reconciliation Errors

One of the most frequent problems: intercompany balances that do not agree between the parent and subsidiary records.

Example: The parent records a loan to Subsidiary C of £150,000, but Subsidiary C records a loan from the parent of £145,000. The £5,000 mismatch must be investigated and resolved before consolidation can be completed.

Root causes:

- Timing differences (transactions recorded in different periods)

- Foreign exchange differences (if balances are in different currencies)

- Unrecorded transactions (one side records, the other does not)

- Errors in posting or allocation

Best practice: Reconcile intercompany accounts throughout the year, not just at year-end. Monthly or quarterly reconciliation catches errors early and reduces year-end workload.

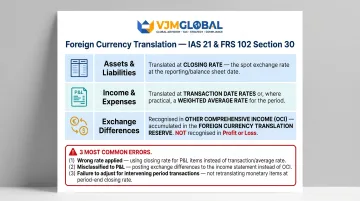

Multi-Currency Complexity

Groups with subsidiaries operating in different currencies must translate each subsidiary's results into the group's presentation currency (typically GBP for UK groups).

Translation rules under IAS 21 (IFRS) and FRS 102 Section 30:

- Assets and liabilities: Translated at the closing rate (the exchange rate at the reporting date)

- Income and expenses: Translated at the exchange rates at the dates of the transactions (or a weighted average rate for the period as a practical approximation)

- Exchange differences: All resulting translation differences are recognised in other comprehensive income (OCI) and accumulated in the foreign currency translation reserve, not in profit or loss

Common errors:

- Using the wrong rate (e.g., closing rate for income, or average rate for assets)

- Misclassifying translation differences as profit/loss instead of OCI

- Failing to adjust for significant transactions in the intervening period (when using the three-month reporting date rule)

Impact: Errors in rate application or classification can materially distort group equity figures and misstate profit or loss.

Over-Reliance on Manual Processes

Currency translation complexity compounds when the underlying consolidation process itself is manual. Consolidating accounts using spreadsheets alone introduces multiple risks:

- Multiple team members editing different versions of the same file simultaneously

- Broken formula links, incorrect cell references, or accidentally deleted rows

- No audit trail recording who changed what and when

- Errors buried deep in complex formulas across multiple tabs

Best practice: Professional accounting software or outsourced consolidation support reduces these risks by automating calculations, maintaining audit trails, and enforcing controls.

For UK groups managing international subsidiaries, outsourcing consolidation work to specialists — such as VJM Global — gives you structured support across trial balance preparation, currency translation, consolidation adjustments, and year-end reporting under UK GAAP or IFRS. This is particularly useful where in-house teams lack capacity during reporting periods.

Frequently Asked Questions

What is a consolidated account?

A consolidated account (or consolidated financial statement) is a combined set of financial reports that presents a parent company and all its subsidiaries as a single economic unit. Internal transactions between group members are eliminated to show the group's true financial position and performance.

Do I need to prepare consolidated accounts in the UK?

Under Section 399 of the Companies Act 2006, a UK-registered parent company must prepare consolidated accounts unless it qualifies for an exemption. The most common route out is the small group exemption — see the size threshold question below for the current figures effective from April 2025.

What are the three types of consolidation?

Three consolidation methods are used in UK reporting:

- Acquisition (purchase) accounting — the most common method, applied when one entity acquires control of another; recognises goodwill and fair values

- Merger accounting — available under FRS 102 for specific group reconstructions where no party acquires the other; not permitted under IFRS

- Equity method accounting — used for associates and joint ventures where significant influence exists but full control does not

What are the current size thresholds for the small group exemption in the UK?

From 6 April 2025, a group qualifies as small if it meets at least 2 of these 3 conditions: turnover not exceeding £15 million, balance sheet total not exceeding £7.5 million, and average employee count not exceeding 50. These figures represent an approximately 50% increase under SI 2024/1303.

Can overseas subsidiaries be excluded from UK consolidated accounts?

Generally, no. If a company is registered in the UK and is a parent, it must include all subsidiaries it controls in the consolidation, including those based overseas in India, the US, Europe, or elsewhere. Limited exclusions apply where a subsidiary is immaterial, held exclusively for resale, or subject to severe long-term restrictions on the parent's rights.