Introduction

India's GDP grew 6.5% in FY2024/25, keeping it the fastest-growing major economy in the world. Yet UK companies ranked only 12th among FDI equity sources in FY2024-25, contributing £795 million — a signal that many UK firms are either routing investments through third countries or missing the opportunity entirely.

For those ready to enter directly, the first decision is also one of the most consequential: choosing the right legal structure. Get it wrong, and you risk delayed operations, ongoing compliance headaches, or exposing your parent company to liability it didn't anticipate.

India's regulatory framework spans multiple governing bodies — the Ministry of Corporate Affairs (MCA), the Reserve Bank of India (RBI), and FEMA authorities — each with distinct rules for foreign-owned entities. This guide covers which structure suits your activities, what each option requires, and how to complete the setup process correctly.

Key Takeaways

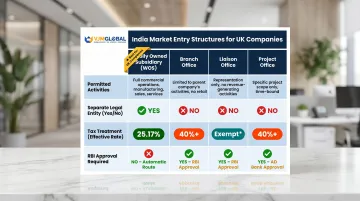

- UK companies can enter India as a Wholly Owned Subsidiary (WOS), Branch Office, Liaison Office, or Project Office, each with distinct permitted activities and compliance obligations

- A WOS (typically a Private Limited Company) offers the most flexibility, lowest tax rate (~25.17% effective), and limited liability protection

- Setup requires MCA and RBI approvals under FEMA, plus PAN, TAN, and GST registrations

- The UK-India DTAA reduces withholding tax on dividends, interest, and royalties compared to standard rates

- Typical timeline: 4-6 weeks for a WOS; Branch Offices take longer due to mandatory RBI approval

Your Entry Options: Legal Structures for UK Companies in India

India offers four main entry routes for foreign companies: Wholly Owned Subsidiary, Branch Office, Liaison Office, and Project Office. The right choice depends on your intended business activities, liability tolerance, and long-term goals.

Wholly Owned Subsidiary (WOS)

A WOS is a Private Limited Company incorporated under the Indian Companies Act, 2013. It functions as a separate legal entity from the UK parent, limiting parental liability to the extent of shareholding.

Key advantages:

- 100% FDI permitted in most sectors under the automatic route — no prior RBI approval needed

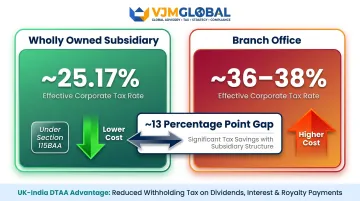

- Lower tax rate: Effective corporate tax of approximately 25.17% under Section 115BAA, versus 36–38% for Branch Offices

- Broad operational scope: Can invoice Indian clients, hire locally, undertake manufacturing, and operate indefinitely

- Stronger local credibility: Indian clients and partners consistently prefer dealing with registered local entities over foreign branches

100% foreign ownership is permitted under DPIIT's Consolidated FDI Policy across most sectors, though some industries (discussed below) have caps or require government approval.

Branch Office

A Branch Office is an extension of the UK parent — not a separate legal entity. It's permitted to carry out activities such as import/export, professional services, IT services, and acting as a buying/selling agent.

Key limitations:

- Requires prior RBI approval under FEMA, typically adding 4–8 weeks

- Higher tax burden: Taxed as a foreign company at an effective rate of 36.4–38.22%

- Cannot undertake manufacturing or retail trading

- Parent liability: The UK parent remains fully liable for the Branch's obligations

Branch Offices suit UK companies with limited, specific activities and no intent to generate substantial local revenue.

For companies that need even lighter-touch representation — or are tied to a single contract — two further structures are available.

Liaison Office and Project Office

A Liaison Office (also called a Representative Office) is restricted to market research, liaison, and communication activities — it cannot earn revenue in India. A Project Office is temporary, tied to a specific contract, and suitable for infrastructure or construction projects funded by inward remittance.

Comparison Table: Legal Structures

| Structure | Permitted Activities | Separate Legal Entity? | Tax Treatment | RBI Approval Required? |

|---|---|---|---|---|

| Wholly Owned Subsidiary | All commercial activities (trading, manufacturing, services) | Yes | Domestic company: ~25.17% effective rate | No (for most sectors under automatic route) |

| Branch Office | Import/export, professional services, IT, agency work | No | Foreign company: ~36–38% effective rate | Yes |

| Liaison Office | Market research, liaison, communication only — no revenue | No | Not applicable (no income permitted) | Yes |

| Project Office | Execution of specific project contract only | No | Foreign company: ~36–38% effective rate | No (if contract funded by inward remittance) |

For UK companies planning to invoice Indian clients, hire locally at scale, or operate long-term, a WOS is almost always the right structure. VJM Global has guided over 250 UK businesses through India market entry — in most cases, the WOS route delivered faster setup, lower ongoing tax costs, and fewer operational restrictions than any alternative.

Why UK Companies Are Choosing India for Expansion

India presents a compelling business case for UK companies. Bilateral trade between the UK and India reached £47.2 billion in the four quarters to Q2 2025—a 15.2% increase from the prior year. The UK-India Comprehensive Economic and Trade Agreement (CETA), signed in July 2025, aims to double bilateral trade to USD 100 billion by 2030 through 99% tariff elimination on India's export lines.

Despite this momentum, UK FDI into India totalled just USD 795 million in FY2024-25, ranking the UK 12th among source countries—well behind Singapore (USD 14.9 billion), Mauritius, and the US. Cumulative UK investment since 2000 stands at USD 36.13 billion (6th largest), suggesting many UK firms are routing investments through intermediary jurisdictions rather than investing directly.

Sectors attracting UK investment:

- Financial services and fintech — India's UPI and GST Network infrastructure creates openings for UK fintech and insurance firms

- Technology and IT services — large English-speaking talent pool with lower operational costs

- Manufacturing — government incentives under Production Linked Incentive (PLI) schemes

- Healthcare and pharmaceuticals — growing middle class and expanding healthcare access

- Retail and consumer goods — rising disposable incomes in Tier 2 and Tier 3 cities

FDI route considerations:

Most sectors permit 100% FDI under the automatic route. However, certain sectors require government approval or have caps:

- Defence: 74% automatic; up to 100% via government route for modern technology access

- Insurance: 100% automatic route (liberalised February 2026); LIC capped at 20%

- Pharmaceuticals (brownfield): 74% automatic; beyond requires government approval

- Print and digital news media: 26% cap, government approval required

- Banking (private sector): 74% automatic, subject to RBI guidelines

These caps and approval requirements vary by sub-sector and change periodically — getting the route classification wrong at incorporation can create costly restructuring later. VJM Global conducts sector-specific FDI route verification for every UK client before initiating incorporation to prevent exactly that.

How to Set Up a Wholly Owned Subsidiary in India: Step-by-Step

Setting up a WOS involves pre-incorporation steps (obtaining Director Identification Numbers and Digital Signature Certificates), MCA filings, and post-incorporation registrations. The entire process typically takes 4-6 weeks with proper documentation.

Step 1: Obtain Director Identification Number (DIN) and Digital Signature Certificate (DSC)

Every proposed director of the Indian company—including UK-based directors—must obtain:

- DIN: A unique identification number issued by the MCA

- DSC: A digital signature required for filing e-forms on the MCA portal (valid for 1-2 years)

Critical requirement many UK companies overlook: At least one director must be a resident of India, defined as someone who has stayed in India for at least 182 days in the preceding calendar year. The 182 days need not be consecutive.

Documents required for DSC:

- Passport-size photograph

- Self-attested address proof

- Self-attested PAN card

UK companies without a local hire must either appoint a qualified resident director or use a professional nominee director service until a full-time local hire is in place.

Step 2: Name Approval via RUN (Reserve Unique Name) Application

The company name must be submitted through the MCA's RUN portal for approval. Applicants can propose up to two names per application. The reserved name is valid for 20 days from approval.

Name requirements:

- Must reflect the business activity

- Cannot be identical to existing registered companies or trademarks

- Must comply with the Companies (Incorporation) Rules, 2014

- Cannot contain words suggesting government patronage without permission

Step 3: Incorporation Filing (SPICe+ Form) with MCA

The SPICe+ (Simplified Proforma for Incorporating a Company Electronically) form handles multiple registrations simultaneously:

- Company incorporation (CIN allocation)

- PAN (Permanent Account Number)

- TAN (Tax Deduction Account Number)

- EPFO (Employee Provident Fund Organisation)

- ESIC (Employee State Insurance Corporation)

- GST registration (optional at this stage)

Required documents:

- Memorandum of Association (MoA) and Articles of Association (AoA)

- Passport copies and address proof for all directors (foreign directors' documents must be notarised and authenticated)

- Board resolution from the UK parent company authorising the Indian entity setup

- Proof of registered office address in India (rental agreement or ownership documents)

- Subscriber details and share subscription information

Step 4: RBI Reporting under FEMA (Foreign Exchange Management Act)

While a WOS in most sectors does not require prior RBI approval under the automatic FDI route, the UK parent company must report the inward remittance (share capital transfer) to the RBI within 30 days of receipt.

Filing requirement: Form FC-GPR (Foreign Currency – Gross Provisional Return) must be filed through the RBI's FIRMS portal within 30 days from the date of share allotment.

Non-compliance penalties:

- Late filing attracts a fee of 0.05% of the amount involved per month of delay or ₹1,000 per month (whichever is higher), capped at ₹10 lakh

- Failure to pay triggers compounding proceedings with penalties up to 3 times the sum involved under FEMA Section 13

Step 5: Post-Incorporation Registrations and Bank Account Opening

After receiving the Certificate of Incorporation, the company must complete several post-incorporation steps:

Mandatory registrations:

- Open an Indian bank account: Required to deposit share capital within 180 days of incorporation

- GST registration: Mandatory if annual turnover exceeds ₹20 lakh (services) or ₹40 lakh (goods) in normal states

- Import Export Code (IEC): Required if the company will engage in import/export

- Shops and Establishments Act registration: Required in the state of operation (varies by state)

- Professional Tax registration: Applicable in certain states if employing staff

E-invoicing: Mandatory for taxpayers with aggregate turnover exceeding ₹5 crore, effective from 1 August 2023.

VJM Global provides end-to-end support across every step of this process — from DIN/DSC coordination and SPICe+ filing to FC-GPR submissions and post-incorporation registrations. Support includes:

- GST registration with analysis of business nature, supply types, and registration category

- Bank account opening coordination

- IEC registration support

- Ongoing secretarial compliance and statutory register maintenance

Key Regulatory and Compliance Requirements for UK Companies in India

FEMA (Foreign Exchange Management Act)

FEMA governs all cross-border capital flows. UK companies must ensure compliance for:

- Equity investments: FC-GPR filing within 30 days of share allotment

- Inter-company loans: Subject to External Commercial Borrowing (ECB) guidelines

- Royalties and technical fees: Must comply with DTAA provisions and transfer pricing rules

- Dividend repatriation: Subject to 15% withholding tax under UK-India DTAA (unless lower rate applies)

Non-compliance can result in penalties up to 3 times the sum involved or ₹2 lakh (if amount not quantifiable), plus ₹5,000 per day for continuing contraventions.

Companies Act, 2013 Ongoing Compliance

Indian subsidiaries must meet strict annual compliance requirements:

| Obligation | Form/Requirement | Deadline | Penalty for Non-Compliance |

|---|---|---|---|

| Financial statements filing | AOC-4 | Within 30 days of AGM | Up to ₹10 lakh for company; ₹1–5 lakh for directors |

| Annual return filing | MGT-7 | Within 60 days of AGM | Up to ₹5 lakh for company; ₹50,000–5 lakh for directors |

| Annual General Meeting (AGM) | AGM | Within 6 months of financial year end (by 30 September) | Late fee: ₹100/day |

| Board meetings | Minimum 4 per year | Maximum 120-day gap between meetings | ₹1 lakh for company; ₹25,000 for directors |

Statutory audit: Annual financial statements must be audited by a Chartered Accountant registered with the Institute of Chartered Accountants of India (ICAI).

VJM Global supports UK-owned Indian subsidiaries with AOC-4 and MGT-7 filings, statutory audit coordination, and maintenance of statutory registers.

Indian Tax Landscape

Corporate income tax rates (AY 2026-27):

| Entity Type | Tax Regime | Effective Rate |

|---|---|---|

| Domestic company (WOS) | Section 115BAA (concessional) | ~25.17% |

| Domestic company | Standard rate | Up to ~34.94% |

| Foreign company (Branch Office) | Standard rate | ~36.4-38.22% |

The approximately 13 percentage-point gap between the WOS effective rate (~25.17%) and the Branch Office effective rate (~36–38%) gives WOS entities a clear tax cost advantage over Branch Offices — worth factoring into your entity structure decision.

UK-India Double Taxation Avoidance Agreement (DTAA):

The UK-India DTAA (entered into force 26 October 1993) reduces withholding tax rates on cross-border payments:

| Payment Type | Treaty Rate |

|---|---|

| Dividends | 15% |

| Interest (general) | 15% |

| Interest (banking/export credit) | 10% or 0% |

| Royalties (general) | 15% |

| Royalties (industrial equipment) | 10% |

| Fees for Technical Services | 15% |

VJM Global advises UK companies on structuring dividend repatriation, royalty payments, and intercompany loan interest to minimise withholding tax obligations under the DTAA.

Transfer Pricing Regulations

Transactions between the UK parent and the Indian subsidiary are classified as "international transactions" and must be priced at arm's length. The Indian subsidiary must:

- File Form 3CEB annually: Required when aggregate value of international transactions exceeds ₹1 crore

- Prepare Transfer Pricing documentation: Including a Functional, Asset, and Risk (FAR) analysis and benchmarking study

- Maintain contemporaneous documentation: To support arm's length pricing in case of tax authority scrutiny

VJM Global prepares Transfer Pricing studies and Form 3CEB filings for UK parent–Indian subsidiary transactions, conducting FAR analysis and benchmarking against industry data to mitigate tax controversy risk.

GST Compliance

The Indian subsidiary must:

- Register for GST if turnover exceeds ₹20 lakh (services) or ₹40 lakh (goods) in normal states

- File monthly/quarterly returns: GSTR-1 (outward supplies), GSTR-3B (summary return)

- Comply with e-invoicing if turnover exceeds ₹5 crore

VJM Global provides ongoing GST compliance support, including registration, return filing, and e-invoicing compliance.

Common Mistakes and Misconceptions When UK Companies Set Up in India

Mistake 1: All Sectors Are Open to 100% FDI Under Automatic Route

While the automatic route covers most sectors, several industries require government approval or have FDI caps:

- Defence: 74% FDI permitted automatically; beyond that requires government approval

- Pharmaceuticals (brownfield): 74% automatic; exceeding this threshold requires government approval

- Print and digital news media: 26% cap, government approval required

- Banking: 74% automatic (subject to RBI guidelines)

UK companies that assume blanket automatic route eligibility without sector-specific due diligence face rejected applications or void incorporations. VJM Global conducts FDI route verification for every client before initiating the incorporation process.

Mistake 2: Failing to Appoint a Resident Indian Director Before Incorporation

The most common operational mistake: attempting to proceed with only UK-based directors. Indian law requires at least one director who has stayed in India for 182+ days in the preceding calendar year.

This requirement leads to incorporation filing rejections. UK companies must either hire a local director before filing or use a professional nominee director service until a permanent local hire is in place. A third option — appointing an existing India-based employee to the board — works well for companies that already have in-country staff.

Mistake 3: Underestimating the Compliance Burden

UK companies often underestimate how different Indian compliance timelines and procedures are from the UK:

- Hard deadlines: AOC-4 due within 30 days of AGM; MGT-7 within 60 days

- Financial penalties: ₹100/day for late filings, plus statutory penalties up to ₹10 lakh

- Director disqualification risk: Non-filing for 3 consecutive years can disqualify directors

Working with an India-experienced professional services firm from Day 1 reduces this risk. VJM Global's compliance calendar management keeps filing deadlines on track — so UK companies avoid penalties before they become a problem.

Frequently Asked Questions

Can a UK company own 100% of its Indian subsidiary?

Yes, 100% foreign ownership (FDI) is permitted under the automatic route in most sectors. The subsidiary is classified as a wholly owned subsidiary under Indian company law. The UK parent must report the investment to RBI via FC-GPR within 30 days of share allotment.

What is the minimum capital required to register a company in India as a UK business?

There is no statutory minimum paid-up capital requirement for a Private Limited Company under the Companies Act, 2013 (the previous ₹1 lakh requirement was removed in 2015). However, practical considerations—visa applications, bank accounts, operational costs—often lead foreign companies to start with modest initial capital.

How long does it take to set up an Indian subsidiary or branch office for a UK company?

A WOS typically takes 4–6 weeks from document submission to incorporation certificate, plus an additional 2–4 weeks for GST registration and bank account opening. Branch Offices take longer — mandatory RBI approval adds another 4–8 weeks.

Does the Indian subsidiary need a local (Indian resident) director?

Yes, at least one director must be a resident of India, defined as someone present in India for at least 182 days in the preceding calendar year. UK companies must arrange for a qualified resident director before filing for incorporation—either through local hiring or professional nominee director services.

What taxes does a UK company's Indian subsidiary pay?

The subsidiary pays Indian corporate tax at an effective rate of approximately 25.17% under Section 115BAA. The UK-India DTAA provides relief from double taxation on dividends (15% withholding), interest (10–15%), and royalties (10–15%).

Is a branch office or a subsidiary better for a UK company entering India?

For most UK companies, a subsidiary (WOS) is the stronger choice — it offers limited liability protection, lower tax rates (~25% vs ~36–38%), greater operational flexibility, and is viewed more favourably by Indian clients and partners. A branch office suits companies with limited, specific activities and no intent to generate substantial local revenue.

Ready to establish your UK company's presence in India? VJM Global has assisted over 250 UK businesses with India market entry, providing full-cycle support from entity selection through ongoing compliance. Contact VJM Global at info@vjmglobal.com or +91 9891576441 to discuss your India expansion strategy with our team of Chartered Accountants and business setup specialists.