Introduction

UK businesses are increasingly looking at India as a serious expansion market. Setting up a subsidiary is the preferred route for companies that want a full legal presence, the ability to contract and invoice locally, and direct control over Indian operations. With bilateral trade between the UK and India exceeding £40 billion in 2024—more than double the 2019 figure—India represents one of the UK's most important strategic trade partners in the post-Brexit era.

This guide is for UK-based businesses at any stage of exploring India expansion. It covers:

- Types of Indian subsidiaries and which suits your business

- The step-by-step registration process

- UK-specific document and FDI requirements

- Tax and compliance obligations

- Common mistakes to avoid

Whether you're a fintech startup, a professional services firm, or a manufacturing business, this guide gives you a clear picture of what India entry actually involves.

Key Takeaways

- A subsidiary in India is a separate legal entity where the UK parent holds more than 50% of shares, governed by the Companies Act, 2013

- Most UK businesses incorporate as a Private Limited Company through the SPICe+ form on the MCA portal

- UK incorporation documents from Companies House must be apostilled before submission; at least one Indian-resident director is mandatory

- Setup typically takes 2–4 months, with incorporation costs ranging from £500–£2,000 (plus ongoing annual compliance fees)

- The UK-India DTAA caps withholding tax at 10% on dividends and 10–15% on royalties and technical service fees repatriated to the UK parent

What Is a Subsidiary Company in India?

Legal Definition

A subsidiary is defined under Section 2(87) of the Companies Act, 2013, as a company where the holding or parent company controls the board of directors or holds more than half the total share capital.

The Indian subsidiary is a legally distinct entity from the UK parent, treated as a domestic company for Indian tax purposes. This means your UK parent company is liable only up to its shareholding amount — not the subsidiary's full obligations.

Two Types UK Businesses Can Form

Wholly Owned Subsidiary (WOS):

- UK parent holds 100% of shares

- Only available in sectors permitting 100% Foreign Direct Investment (FDI) under the Automatic Route

- Most common for IT, software, consulting, fintech, and manufacturing businesses

- No Indian partners required

Subsidiary with Shared Ownership:

- UK parent holds more than 50% but less than 100%

- Remaining shares held by Indian individuals or entities

- Often used for joint ventures or sectors with FDI caps

- Allows for strategic local partnerships

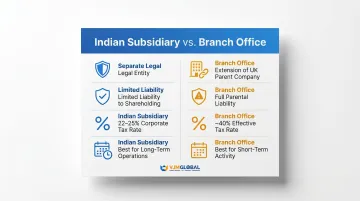

Subsidiary vs. Branch Office

Choosing the right structure has real financial consequences. Here's how they compare:

| Subsidiary | Branch Office | |

|---|---|---|

| Legal status | Separate legal entity | Extension of UK parent |

| Liability | Limited to shareholding | Full parental liability |

| Corporate tax rate | 22–25% (domestic rates) | 35% base rate + surcharge and cess |

| Best for | Long-term India operations | Short-term or limited activity |

For most UK businesses planning a sustained India presence, the subsidiary structure wins on both liability protection and tax efficiency.

Why UK Businesses Are Choosing India for Subsidiary Expansion

UK-India trade exceeded £40 billion in 2024 — double what it was in 2019 — and that momentum is accelerating. According to the UK government's FTA impact assessment, the UK-India Free Trade Agreement is "the biggest and most economically significant new bilateral FTA since leaving the EU." With India's GDP now exceeding £3 trillion and growing at roughly 5% annually, the case for establishing a presence there is hard to ignore.

Beyond market size, the operational fit for UK companies is strong:

- Large English-speaking graduate workforce with deep technical expertise

- Substantially lower operational and labour costs compared to the UK

- Established strength in IT, professional services, and manufacturing — sectors where most UK firms already operate

- Time zone overlap that enables near-24-hour operations when paired with a UK headquarters

UK-India Tax Treaty Benefits

The UK-India Double Tax Avoidance Agreement (DTAA) limits withholding tax on cross-border payments. Under the current treaty rates:

- Dividends: 10% withholding tax

- Royalties: 10–15% (depending on type)

- Technical service fees: 10–15%

These rates ensure that profits flowing back to the UK parent aren't taxed twice — a meaningful advantage over markets without a comparable treaty.

100% FDI Under the Automatic Route

Most sectors UK businesses enter — IT, fintech, consulting, manufacturing, education — permit 100% foreign direct investment under the Automatic Route. No prior government approval is required, simplifying entry considerably compared to markets where regulatory clearance can delay setup by months.

How to Register a Subsidiary in India: Step-by-Step

Registration is governed by the Companies Act, 2013, and filed digitally via the Ministry of Corporate Affairs (MCA) portal. For UK companies, a Private Limited Company (Pvt. Ltd.) is the standard choice — simpler compliance requirements and no minimum paid-up capital make it the right fit for most UK businesses entering India.

Step 1: Choose Your Company Structure

Private Limited Company (recommended for most UK businesses):

- Requires minimum 2 shareholders and 2 directors

- No minimum paid-up capital since the 2015 amendment

- Best suited for small-to-medium UK businesses entering India

- Simpler compliance compared to public companies

Public Limited Company:

- Requires minimum 7 shareholders and 3 directors

- Must comply with SEBI regulations

- Suited only for large businesses planning to raise public capital in India

Step 2: Obtain Digital Signature Certificates (DSC) and Director Identification Numbers (DIN)

All proposed directors must obtain:

- DSC (Digital Signature Certificate): Required for signing all MCA filings electronically

- DIN (Director Identification Number): Allotted through the MCA portal; each director needs a unique DIN before incorporation can proceed

Note for UK nationals: Submit apostilled passport copies and proof of address. This step frequently causes delays if UK documents are not pre-authenticated — sort authentication before starting the DIN application.

Step 3: Reserve the Company Name

Reserve your company name via Part A of the SPICe+ form on the MCA portal:

- Submit two name options

- Names can include the UK parent company's name with "India" appended (e.g., "ABC Solutions India Private Limited")

- Approved name is reserved for 20 days, extendable to 60 days

- Choose a distinctive name that complies with MCA naming guidelines

Step 4: Prepare and Apostille UK Incorporation Documents

Required UK documents:

- Certificate of Incorporation of the UK parent (from Companies House)

- UK parent's Articles of Association

- Board Resolution authorising subsidiary formation

- Memorandum of Association (MoA) and Articles of Association (AoA) drafted to Indian standards

Critical apostille requirement: All UK-origin documents must be apostilled by the FCDO (Foreign, Commonwealth & Development Office) before submission. As a Hague Convention signatory, the UK apostille process is sufficient—Indian Consulate legalisation is not required.

FCDO apostille turnaround times:

- Standard service: up to 15 working days (£45)

- Next-day service: £40

- e-Apostille: 2 days (£35)

Step 5: File the SPICe+ Form on the MCA Portal

SPICe+ is the single-window integrated form covering:

- Company incorporation

- DIN allotment

- PAN/TAN issuance

- GST registration

- Social security registrations (EPFO/ESIC)

On approval, the MCA issues:

- Certificate of Incorporation

- Corporate Identification Number (CIN)

- PAN (Permanent Account Number)

- TAN (Tax Deduction and Collection Account Number)

All in a single integrated output, typically within 2-4 weeks of submission.

Step 6: Complete Post-Incorporation Requirements

Mandatory post-registration actions within strict deadlines:

Within 30 days of incorporation:

- Appoint first auditor

- Hold first Board meeting

- File registered office address with ROC

Within 180 days:

- File Form 20A (Declaration for Commencement of Business)—failure triggers late fees and potential striking off

Ongoing requirements:

- Open corporate bank account in India

- Register for GST if business activities require it

- Establish compliance calendar for monthly/quarterly filings

VJM Global has guided 250+ UK businesses through each of these steps — from DSC procurement and FCDO apostille coordination to SPICe+ filing and post-incorporation compliance. If you'd rather focus on your market entry than the paperwork, their India entry team handles the process from start to finish.

UK-Specific Documents and FDI Requirements You Need to Know

Apostille Requirements for UK Corporate Documents

Which documents must be apostilled:

- Certificate of Incorporation from Companies House

- Memorandum and Articles of Association of the UK parent

- Board Resolution authorising the Indian subsidiary and naming authorised signatories

Documents must be apostilled via the FCDO, not merely notarised by a UK solicitor — this is the single most common administrative bottleneck for UK applicants. Factor FCDO turnaround times into your incorporation timeline. Standard service takes up to 15 working days.

FDI Regulations Under FEMA

Most sectors UK businesses operate in allow 100% FDI under the Automatic Route, meaning no prior RBI or Government of India approval required:

Automatic Route sectors (100% FDI permitted):

- IT and software services

- Fintech and financial technology

- Professional and consulting services

- Manufacturing and industrial production

- Education and training services

Government/Approval Route sectors (restricted or capped):

- Banking and insurance

- Defence and aerospace

- Print media and broadcasting

- Retail trading (conditions apply)

If your sector requires the Approval Route, factor in additional 8-12 weeks for government clearance.

Indian-Resident Director Requirement

At least one director must have been resident in India for 182 or more days in the preceding calendar year, per Section 149(3) of the Companies Act.

Two practical options for UK companies:

Engage a nominee director service — the most common solution for initial setup. Ensure the nominee is genuinely involved rather than purely nominal, as a passive nominee carries compliance risk. Typical cost: ₹1,00,000–2,00,000 annually (approx. £1,000–2,000).

Relocate a UK employee to India — offers more operational control and alignment with your business. This requires an employment visa and residential setup, and the employee must physically reside in India for 182+ days in the calendar year.

Registered Office Requirement

With the director requirement addressed, you also need a physical Indian address registered before operations begin.

A physical address in India must be registered with the ROC within 30 days of incorporation. This address determines state-specific compliance obligations, such as professional tax in Maharashtra or shops and establishments registration.

Practical alternatives for UK companies not ready to lease commercial space:

- Virtual office services

- Co-working spaces with registered office facilities

- Shared office addresses through business centres

VJM & Associates LLP assists UK clients in sourcing registered office addresses across major cities including Noida, Delhi, Mumbai, Bengaluru, Chennai, and Hyderabad.

Tax and Ongoing Compliance Obligations for UK Subsidiaries

Corporate Tax Rates

Your Indian subsidiary, as a domestic entity, faces these corporate tax rates:

| Structure | Rate | Notes |

|---|---|---|

| Subsidiary — turnover up to ₹400 crore | 25% | Standard rate |

| Subsidiary — turnover above ₹400 crore | 30% | Standard rate |

| Subsidiary — reduced rate | 22% | Section 115BAA (certain deductions foregone) |

| Branch office | ~40% effective | 35% base plus surcharge and cess |

This 13–18 percentage point differential is a key financial reason to prefer the subsidiary structure.

Transfer Pricing Obligations

When your Indian subsidiary transacts with its UK parent — through service fees, management charges, or IP licences — all inter-company transactions must be priced at arm's length under Indian transfer pricing rules.

Specific requirements include:

- All international transactions must be documented, regardless of value

- Form 3CEB transfer pricing audit report is mandatory each year

- Cost-centre subsidiaries typically maintain a 15.5–24% profit margin, depending on function and sector

- Recent draft rules propose a uniform 15.5% safe harbour margin for IT services

Transfer pricing documentation must be prepared before filing the annual tax return.

Recurring Compliance Calendar

Monthly obligations:

- TDS (Tax Deducted at Source) deductions and returns

- GST returns (for most businesses)

Quarterly obligations:

- GST returns (for certain taxpayer categories)

- TDS certificates

Annual obligations:

- Statutory audit under the Companies Act

- Income tax return filing

- ROC filings: financial statements and annual return (Form MGT-7)

- Transfer pricing audit (Form 3CEB)

- Annual General Meeting (AGM)

Missing deadlines carries real cost. Late filing penalties include:

- TDS: ₹200 per day (Section 234E)

- GST: ₹100 per day per act (CGST + SGST), capped at ₹5,000

- Form 20A: Escalating fees based on delay; persistent non-filing can lead to the company being struck off

UK-India DTAA Benefits in Detail

To claim DTAA benefits and reduced withholding tax rates, the UK parent must furnish:

- Tax Residency Certificate (TRC) from HMRC

- Form 10F filed electronically with the Indian subsidiary

Without these documents, the Indian subsidiary must apply full domestic withholding tax rates (typically 20% on dividends, 10% on technical fees), which can then only be recovered through a refund application — a lengthy process.

VJM Global supports 250+ UK subsidiaries with accounting, tax compliance, transfer pricing, and back-office services. With 30+ years navigating both Indian and UK tax systems, we help UK management teams stay compliant without building an internal finance function from scratch.

Common Mistakes UK Companies Make When Setting Up in India

Underestimating the Ongoing Compliance Burden

Many UK businesses assume Indian regulatory requirements mirror the UK's lighter-touch regime. In reality, India requires:

- Separate monthly or quarterly filings for GST and TDS

- Multiple labour law registrations (PF, ESI, professional tax) varying by state

- Annual ROC filings with detailed financial statements

- Transfer pricing documentation for all international transactions

Missing any deadline triggers financial penalties and compliance notices. Establish local compliance infrastructure before operations begin — whether through advisors like VJM & Associates LLP or an in-house finance team. Sorting this out after the fact is significantly more costly.

Failing to Apostille UK Documents Correctly or On Time

In practice, apostille errors cause more delays than any other step for UK applicants. Documents notarised by a UK solicitor are insufficient for MCA submission. Only FCDO apostille satisfies the requirement.

Common errors:

- Submitting notarised (but not apostilled) documents

- Using solicitor certification instead of FCDO apostille

- Underestimating FCDO processing times (up to 15 working days for standard service)

Solution: Begin the apostille process immediately after your UK Board Resolution is signed, before starting the Indian incorporation application.

Committing to a Subsidiary Before Validating the India Opportunity

Setting up a subsidiary creates significant ongoing compliance and cost obligations: statutory audits, transfer pricing, GST filings, ROC filings, and more. Winding down a subsidiary is difficult and time-consuming under Indian law.

Consider lighter-touch initial structures:

- Employer of Record (EOR): Hire Indian employees without incorporating a legal entity — VJM & Associates LLP provides PEO services for this structure

- Liaison Office: Limited to market research and liaison activities only (no revenue generation)

- Branch Office: For project-specific work where full subsidiary isn't justified

Reserve the subsidiary structure for once your India business case is validated through initial market testing. The compliance overhead is substantial enough that entering through a lighter structure first is almost always the smarter approach.

Conclusion

Setting up a subsidiary in India involves several interdependent steps. Done in sequence, the full process typically takes 2–4 months:

- Selecting the right corporate structure (Private Limited is standard for most UK entrants)

- Apostilling UK documents for Indian regulatory acceptance

- Appointing an Indian-resident director to satisfy MCA requirements

- Completing SPICe+ registration with MCA

- Establishing ongoing compliance across GST, income tax, labour law, and ROC filings

Careful planning at each stage prevents the delays and penalties that catch unprepared businesses off guard.

India's combination of market size, English-speaking talent, DTAA advantages, and strengthening UK-India commercial ties makes it one of the most compelling expansion destinations for UK businesses.

The regulatory landscape is complex, and missteps in FEMA compliance, transfer pricing, or ROC filings carry real penalties. Working with advisors who understand both UK corporate structures and Indian compliance requirements makes the difference between a smooth market entry and an expensive one. VJM & Associates LLP has guided 250+ UK businesses through this process, from initial structure selection through to ongoing compliance operations.

Frequently Asked Questions

What is a subsidiary company in India?

Under Section 2(87) of the Companies Act, 2013, a subsidiary is a company in which the holding or parent company controls the board of directors or holds more than half the total share capital. It is a separate legal entity from the parent company.

How to register a subsidiary company in India?

Reserve the company name via SPICe+ on the MCA portal, obtain DSC and DIN for directors, file incorporation documents (MoA, AoA, apostilled UK parent documents), and receive the Certificate of Incorporation. The typical timeline is 2–4 months.

How to incorporate a wholly owned subsidiary in India?

A WOS has three core requirements:

- The UK parent must hold 100% of shares

- Only available in sectors permitting 100% FDI under the Automatic Route

- Follows the SPICe+ Private Limited Company process, with at least 2 directors (1 must be an Indian resident)

Are subsidiaries 100% owned?

No, subsidiaries are not always 100% owned. A parent company only needs to hold more than 50% of share capital for the company to qualify as a subsidiary. A company with 100% foreign ownership is specifically termed a Wholly Owned Subsidiary (WOS).

What is a subsidiary company of a foreign company in India?

It is an Indian-incorporated entity (typically a Private Limited Company) in which a foreign parent company holds the majority or all of the shares. Despite foreign ownership, the Indian subsidiary is treated as a domestic company for Indian corporate tax purposes.

How to consolidate a foreign subsidiary in India?

The UK parent must consolidate the Indian subsidiary's audited financial statements into its group accounts under UK GAAP or IFRS. This requires the Indian subsidiary's annual audited accounts and involves currency translation from Indian Rupees to GBP in line with the relevant accounting standard.