Introduction

The UK-India trade corridor is moving fast. Bilateral trade in goods and services hit £47.4 billion in the four quarters to Q3 2025, and the UK-India Free Trade Agreement signed in July 2025 is forecast to add £25.5 billion in annual trade on top of that.

The IMF projects India's GDP growth at 6.5% in both 2026 and 2027 — outpacing every other major economy. For British businesses weighing an India entry, the timing has rarely been this clear-cut.

One of the most practical ways to enter that market is through a branch office. It lets you operate under your parent company's identity, conduct commercial activities, and test the Indian market without incorporating a separate entity. You keep full parent company control — no local equity partners required.

This guide covers everything you need to make that move: what a branch office is, whether it suits your business, how to register one, and what compliance looks like once you're up and running.

Key Takeaways

- A branch office is an extension of your UK parent company in India, regulated by the RBI under FEMA 1999—not a separate legal entity.

- UK companies need a net worth of at least USD 100,000 and a 5-year profit track record to qualify.

- Setup involves RBI approval (Form FNC), ROC registration, tax registrations, and bank account opening. Expect 6–10 weeks in total.

- Trading, consultancy, IT services, and research are permitted — retail trading and manufacturing (outside SEZs) are not.

- Annual compliance includes RBI's Annual Activity Certificate (AAC), MCA filing (FC-4), and Indian income tax returns.

What Is a Branch Office in India?

A branch office is an extension of your UK parent company authorised to conduct commercial activities in India. It retains your parent company's legal identity — it is not a separate legal entity. The UK parent remains fully liable for all actions and obligations of the India branch.

Permitted Activities

Under RBI regulations (FEMA Master Direction FED No.10/2015-16), branch offices can undertake:

- Export/import of goods

- Professional and consultancy services

- IT and software development

- Technical support for parent company products

- Research aligned with parent company activities

- Acting as buying/selling agent in India

- Representing foreign airline or shipping companies

Prohibited Activities

Branch offices cannot:

- Engage in retail trading

- Undertake manufacturing outside Special Economic Zones (SEZs)

- Conduct activities unrelated to the parent company's business

These restrictions make it important to choose the right India entry structure from the start. The table below shows how a branch office compares to the two most common alternatives for UK companies.

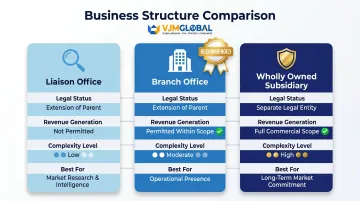

How It Differs from Other Entry Structures

| Structure | Legal Identity | Revenue Generation | Setup Complexity |

|---|---|---|---|

| Liaison Office | Extension of parent | Not permitted | Low |

| Branch Office | Extension of parent | Permitted (defined activities) | Moderate |

| Wholly Owned Subsidiary | Separate legal entity | Full commercial scope | High |

A liaison office suits early-stage market research or relationship building. A wholly owned subsidiary (incorporated under the Companies Act 2013) offers the broadest commercial scope but carries heavier compliance obligations. A branch office occupies the middle ground: operational flexibility without the complexity of incorporating a new Indian entity.

Branch Office vs. Other India Entry Options for UK Companies

Three structures dominate India entry planning for UK companies: Liaison Office, Branch Office, and Wholly Owned Subsidiary. The right choice depends on your operational scope, risk tolerance, and timeline.

Concise Comparison

| Dimension | Liaison Office | Branch Office | Wholly Owned Subsidiary |

|---|---|---|---|

| Revenue Generation | Not permitted | Permitted (within scope) | Fully permitted |

| Liability Exposure | UK parent liable | UK parent liable | Separate legal entity—limited liability |

| Setup Complexity | Low | Moderate | High |

| Ongoing Compliance | Minimal | Moderate | Significant |

| Best For | Market research, relationship building | Operational presence without full incorporation | Long-term commitment, full commercial operations |

Why Choose a Branch Office?

A branch office suits UK companies that want to operate in India without the full commitment of incorporation:

- Faster setup than incorporating a subsidiary

- Lower initial investment and operational overhead

- Full parent company control over India operations

- No local equity partners required

- Flexibility to test the market before making a longer-term commitment

One trade-off to weigh carefully: your UK parent company bears direct liability for all branch office obligations — there is no separate legal shield as there would be with a subsidiary.

Eligibility Criteria and Key Prerequisites for UK Companies

Core Financial Requirements

Your UK parent company must meet two mandatory criteria:

- Net worth of at least USD 100,000 (total paid-up capital and free reserves, less intangible assets, per latest audited balance sheet)

- Profitable track record for the immediately preceding five financial years

Letter of Comfort (LOC) Provision

If your UK subsidiary doesn't independently meet the threshold, a parent or group company that satisfies the criteria can issue a Letter of Comfort. This letter must contain:

- An undertaking to provide necessary financial support

- A statement that the parent/group will meet liabilities if the branch office is unable to

- The latest audited balance sheet of the parent/group company

Approval Routes Under FEMA 1999

Automatic Route — Applies where 100% FDI is permitted. The RBI processes applications via your Authorised Dealer (AD) bank. Most UK companies in IT, consulting, and trading use this route.

Government Route — Required if any of the following apply:

- Restricted sectors: Defence, Telecom, Private Security, Information and Broadcasting

- NGO or non-profit structures

- Applicants from Pakistan, Bangladesh, Sri Lanka, Afghanistan, Iran, China, Hong Kong, or Macau

- Proposed operations in J&K, North East, or Andaman & Nicobar Islands

UK-Specific Documentation: Apostille Requirements

The UK is a signatory to the Hague Apostille Convention (since 1965), and India acceded in 2005. All incorporation and financial documents from the UK must be apostilled (not embassy-notarised). Documents not in English must include certified English translations.

Activities Alignment Check

Your planned India operations must align with RBI's permitted activity categories. If your intended activity falls outside those categories, a branch office is not the appropriate structure. In that case, a liaison office or wholly owned subsidiary may be the better fit.

How to Open a Branch Office in India: Step-by-Step

Opening a branch office in India requires navigating two separate regulatory bodies (RBI and MCA/ROC), tax authorities, and banking compliance — often simultaneously. The five steps below cover the full process, from your first banking appointment through operational status.

Firms like VJM Global, which have guided 250+ UK businesses through this process, can cut delays and reduce documentation errors at each stage.

Process overview:

- Appoint an AD Category-I Bank — Week 1

- Submit Form FNC to RBI — Weeks 1–6

- Register with the Registrar of Companies (ROC) — Weeks 6–9

- Obtain PAN, TAN, and GST registrations — Weeks 9–11

- Open a bank account and complete remaining registrations — Weeks 11–12

Step 1: Appoint an Authorised Dealer (AD) Category-I Bank

Select an AD Category-I Bank in India (a scheduled commercial bank authorised by RBI to handle foreign exchange transactions). This bank:

- Acts as your intermediary with the RBI throughout the process

- Conducts initial KYC and due diligence on your UK parent company

- Will serve as your operational bank for the branch office

The choice of AD bank matters. Banks vary in their processing efficiency and familiarity with UK company applications, so shortlist ones with a documented international client base.

Step 2: Submit Form FNC to the RBI via the AD Bank

Prepare and submit Form FNC (Annex-1) through your chosen AD bank. Mandatory attachments include:

- Certificate of Incorporation from Companies House (apostilled)

- Memorandum and Articles of Association (apostilled)

- Board Resolution authorising the branch establishment

- Audited financial statements for the last 5 years

- Net worth certificate

- KYC of directors/authorised signatories

- Company profile

The AD bank forwards the application to RBI's Central Office Cell in New Delhi for allotment of a Unique Identification Number (UIN), after which the AD bank issues the formal approval letter.

Estimated timeline: 4–6 weeks

Step 3: Register with the Registrar of Companies (ROC)

Within 30 days of receiving RBI approval, file Form FC-1 with the Ministry of Corporate Affairs (MCA) to register the branch office with the relevant state ROC. This yields a Corporate Identity Number (CIN) and is legally required under Section 380(1)(h) of the Companies Act 2013.

Required attachments:

- RBI approval letter

- Parent company incorporation documents

- Details of authorised representative in India

Prescribed filing fee: INR 6,000 (approximately £60) if filed within 30 days. Late filing attracts penalties up to 12x the normal fee — missing this window is one of the most common and costly errors UK companies make.

Estimated timeline: 2–3 weeks

Step 4: Obtain Tax Registrations (PAN, TAN, and GST)

Three registrations are required at this stage:

- PAN (Permanent Account Number): Mandatory for all financial transactions and tax filings. Apply via Form 49AA through NSDL or UTIITSL. Processing: ~10–15 working days.

- TAN (Tax Deduction and Collection Account Number): Required for withholding tax on employee salaries and vendor payments.

- GST (Goods and Services Tax): Required if the branch supplies taxable goods or services in India. Foreign companies with a permanent establishment must register regardless of turnover.

Estimated timeline: 1–2 weeks

Step 5: Open an Indian Bank Account and Complete Remaining Registrations

Open a non-interest-bearing INR current account with the AD bank using the RBI UIN and approval letter.

Additionally complete state-specific registrations as applicable:

- Shops and Establishment Act registration (required in most states)

- Professional Tax registration

- EPF and ESIC registration (if hiring employees)

- Import Export Code (IEC) from DGFT (if involved in cross-border trade of goods)

Total estimated timeline from Step 1 to operational status: 6–10 weeks

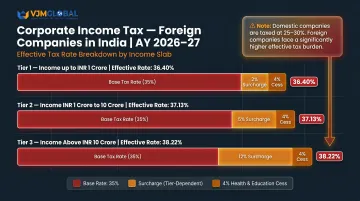

Ongoing Compliance and Tax Obligations for UK Branch Offices in India

Corporate Income Tax

A branch office in India is treated as a Permanent Establishment (PE) of the UK parent company and is subject to Indian corporate income tax on India-sourced income.

Current tax rates for foreign companies (AY 2026-27):

- Base rate: 35%

- Surcharge: 0% (income up to INR 1 crore); 2% (INR 1–10 crore); 5% (above INR 10 crore)

- Health and Education Cess: 4% on tax plus surcharge

- Effective tax rates: 36.40% (up to INR 1 crore) / 37.13% (INR 1–10 crore) / 38.22% (above INR 10 crore)

This is materially higher than the 25–30% base rate for domestic Indian companies.

UK-India Double Taxation Avoidance Agreement (DTAA)

The UK-India DTAA (signed 1993, in force since October 1993) prevents the same income from being taxed twice. Article 7 (Business Profits) is particularly relevant:

- Profits of a UK enterprise are taxable only in the UK unless the enterprise carries on business in India through a permanent establishment.

- If a PE exists (which a branch office does), India may tax profits directly or indirectly attributable to that PE.

- Profits attributable to the PE are calculated as if it were a distinct and separate enterprise operating at arm's length.

- UK companies can claim credit for Indian taxes paid under Article 24 (Elimination of Double Taxation), reducing UK tax liability on the same income.

The DTAA provides meaningful relief, but it doesn't eliminate the need for meticulous compliance in India. Branch offices must maintain a strict annual compliance calendar to stay in good standing with Indian regulators.

Annual Compliance Calendar

1. Annual Activity Certificate (AAC)

- Certified by: Chartered Accountant

- Submitted to: AD bank and Director General of Income Tax (International Taxation), New Delhi

- Reporting period: As at 31 March each year

- Deadline: 30 September annually

- Purpose: Confirms all activities are within RBI-approved scope

2. Form FC-4 (Annual Return to ROC)

- Filed with: Ministry of Corporate Affairs (MCA)

- Deadline: Within 60 days of financial year end (31 May for FY ending 31 March)

- Purpose: Annual return for foreign companies under Section 384(2) of Companies Act 2013

3. Income Tax Return (ITR-6)

- Deadline: 31 October (for companies subject to transfer pricing audit); 30 September (for companies subject to tax audit but not TP audit)

- Purpose: Corporate income tax return for foreign companies

4. GST Returns (if applicable)

- Frequency: Monthly or quarterly, depending on turnover

- Purpose: GST compliance for taxable supplies

Failure to file attracts significant penalties and can jeopardise RBI approval.

Transfer Pricing Compliance

All transactions between the India branch office and UK parent company are subject to Indian transfer pricing regulations and must be conducted at arm's length.

Why this matters: Overpriced intercompany charges — service fees, royalties, or management charges paid to the UK head office — reduce taxable profits in India. Indian tax authorities scrutinise these transactions closely, and any pricing that doesn't reflect market rates triggers adjustments, penalties, and potential double taxation.

Required documentation:

- Form 3CEB: Transfer pricing audit report, due 31 October

- Transfer Pricing Study: Contemporaneous documentation (maintained by Form 3CEB deadline) including:

- FAR analysis (Functions performed, Assets employed, Risks assumed)

- Benchmarking study using comparable companies

- Justification of arm's length pricing

VJM Global prepares Form 3CEB and Transfer Pricing Studies for UK companies operating in India, with 30+ years of experience in international tax compliance and over 250 UK businesses served.

Conclusion

Opening a branch office in India is a well-defined, structured process for UK companies. The eligibility requirements are clear, the two-route approval framework under FEMA is established, and the compliance obligations—while ongoing—are manageable with the right support in place.

The branch office structure offers UK companies a practical middle ground: operational presence in India, ability to generate revenue from permitted activities, full parent company control, and a lower setup burden than incorporating a subsidiary. This makes it particularly well-suited for UK companies at the market-entry or market-testing stage, especially given the growing UK-India trade relationship.

The complexity lies not in the concept but in the documentation, regulatory sequencing, and ongoing compliance. Partnering with an experienced India-based team removes that complexity.

VJM Global has supported 250+ UK businesses through the branch office setup process, from RBI approval through ongoing FEMA and tax compliance—so the regulatory groundwork is handled from day one.

Frequently Asked Questions

What is a branch office of a foreign company?

A branch office is an extension of the foreign parent company (not a separate legal entity), authorised by the RBI to carry out specific commercial activities in India that mirror the parent company's operations. The UK parent retains full liability.

Can a foreign company open a branch in India?

Yes, any foreign company—including UK-registered companies—can open a branch office in India subject to RBI approval under FEMA 1999, provided they meet the net worth (USD 100,000) and profitability (5-year track record) eligibility criteria.

Do branch offices in India require RBI approval?

RBI approval is mandatory for all branch offices in India, obtained by filing Form FNC through an Authorised Dealer Category-I Bank. Most UK companies are eligible under the Automatic Route, processed directly by the AD bank and RBI.

How much does it cost to open a branch office in India?

Setup costs typically range from £1,500–£4,000 (₹150,000–₹400,000), covering:

- ROC registration filing fees: ~£60 (₹6,000)

- Professional fees for RBI and ROC filings: £750–£2,500 (₹75,000–₹250,000)

- Ongoing annual compliance (statutory audit, AAC, ITR, TP documentation): varies by complexity

How to open a branch office in India?

The process runs five steps: appoint an AD Category-I bank → file Form FNC with the RBI → register with ROC (Form FC-1) within 30 days → obtain PAN, TAN, and GST registrations → open a bank account and complete state registrations. Most UK companies are operational within 6–10 weeks.

What are the ongoing compliance requirements for a branch office in India?

Branch offices must file three annual returns: the Annual Activity Certificate (AAC) to RBI by 30 September, Form FC-4 to ROC by 31 May, and Income Tax Return ITR-6 by 30 September (or 31 October if transfer pricing applies). GST returns and transfer pricing documentation (Form 3CEB) are also required where applicable.