Introduction

UK businesses expanding into India face a familiar challenge: navigating a complex regulatory framework while maintaining full operational control. Total trade between the UK and India reached £47.4 billion in the four quarters to Q3 2025, up 11.7% year-on-year, reflecting India's position as one of the fastest-growing markets for British exporters and investors. The signing of the UK-India Comprehensive Economic Partnership Agreement (CEPA) in July 2025 has further strengthened market access, offering UK firms binding FDI protections and access to approximately 40,000 annual government procurement tenders.

A wholly owned subsidiary (WOS) registered as a private limited company under the Companies Act, 2013 is the most common structure for UK businesses seeking permanent establishment in India. Unlike a branch office, which has no separate legal identity, a WOS operates as an independent Indian legal entity — giving the UK parent company 100% control while limiting liability to its shareholding.

In most sectors, India's FDI policy permits 100% foreign ownership under the automatic route, with no prior RBI or government approval required.

This guide walks through what UK businesses need to know:

- FDI eligibility and sector restrictions

- The step-by-step incorporation process, from obtaining DINs to filing the SPICe+ form

- Post-setup compliance covering ROC filings, GST, income tax, and FEMA requirements

- Common pitfalls that delay incorporation

Key Takeaways

- The UK parent company holds 100% share capital through an Indian private limited company

- Most sectors qualify for the automatic FDI route, meaning no RBI approval is required before incorporation

- Incorporation involves obtaining DINs and DSCs for directors, drafting MoA/AoA, and filing via the SPICe+ portal with the Registrar of Companies

- UK corporate documents must be notarised and apostilled through the FCDO before submission to Indian authorities

- Ongoing obligations cover annual ROC filings, statutory audit, GST returns, income tax filings, and FEMA reporting

What Is a Wholly Owned Subsidiary in India?

Under Section 2(87) of the Companies Act, 2013, a subsidiary is a company where the parent controls the composition of the Board of Directors or exercises more than half the total voting power. A wholly owned subsidiary (WOS) is a specific case where the parent holds 100% of the share capital, compared to a regular subsidiary which requires only 51% parent ownership. For UK companies, this structure offers the deepest level of control over Indian operations.

Legal Personality and Liability

Unlike a branch office (an extension of the foreign parent with no separate legal existence), a WOS is an independent Indian legal entity. This means:

- The UK parent's liability is limited to its shareholding

- The WOS can own assets, hire employees, enter contracts, and sue or be sued in its own name

- Day-to-day operations are governed by Indian company law, not UK law

That independence also comes with a structural requirement worth planning for before incorporation.

Nominee Shareholder Requirement

India's Companies Act requires a minimum of two shareholders for a private limited company. UK parent companies typically appoint one nominee shareholder (often a trusted individual or group entity) to satisfy this requirement, whilst maintaining 100% beneficial ownership.

Beneficial ownership declarations must be filed under Section 89 via:

- Form MGT-4 (filed by the nominee shareholder with the company within 30 days)

- Form MGT-5 (filed by the UK parent with the company within 30 days of acquiring beneficial interest)

- Form MGT-6 (filed by the company with the ROC within 30 days of receiving MGT-4 or MGT-5)

Non-compliance penalties: ₹50,000 flat penalty plus ₹200 per day of continuing default (maximum ₹1 lakh per contravention).

Why UK Businesses Are Choosing to Set Up a WOS in India

Strategic Rationale

India's GDP growth is forecast to stay above 6% for at least the next five years — one of the strongest outlooks among G20 economies. That macro momentum alone draws UK investors, but recent trade policy has added a concrete commercial edge.

The UK-India CEPA signed in July 2025 grants UK businesses exclusive "class 2" treatment under the "Make in India" policy when at least 20% of their product or service originates from the UK. In practice, this opens approximately £38 billion worth of Indian government procurement tenders annually to UK firms.

Key Advantages of the WOS Structure

For UK businesses, a WOS offers:

- Full 100% ownership of operations, strategy, and governance — no local joint venture partner required

- Limited liability: the UK parent's financial exposure is capped at its shareholding in the Indian entity

- Ability to hire Indian employees, own local assets, and execute contracts directly as a permanent establishment

- Rights to hold and license intellectual property in India (unavailable to liaison or branch offices)

- Access to the UK-India DTAA, reducing withholding tax on dividends, royalties, and service fees

FDI Routes for UK Investors

These structural advantages are accessible across a wide range of industries. India's FDI policy permits 100% foreign investment under the automatic route in all sectors not listed in Schedule I of the NDI Rules — meaning no prior government approval is needed. This includes:

- IT services and software development

- Manufacturing (all categories)

- Professional services (consulting, accounting, legal)

- E-commerce infrastructure and wholesale trading

- Construction and real estate development

- Telecommunications services

A smaller set of sectors requires government approval before investment can proceed:

- Defence beyond 74% ownership

- Print media covering news and current affairs (26% cap)

- Multi-brand retail trading (51% cap, government approval route)

- Broadcasting and digital media (26% cap for news content)

For restricted sectors, applications are submitted via the Foreign Investment Facilitation Portal (FIFP), administered by the Department for Promotion of Industry and Internal Trade (DPIIT).

How to Set Up a Wholly Owned Subsidiary in India: Step-by-Step

The incorporation process is fully digital via the Ministry of Corporate Affairs (MCA) portal and typically takes 15–30 days once all documents are in order. Working with an experienced setup partner cuts delays considerably. VJM Global has supported 250+ UK businesses through this process, covering apostille coordination, ROC filings, and everything in between.

Minimum Requirements

Before incorporation begins, ensure you have:

- At least two directors (one must be an Indian resident)

- At least two shareholders (the UK parent company plus a nominee)

- No minimum paid-up capital (the Companies (Amendment) Act, 2015 removed the previous ₹1,00,000 requirement)

Step 1: Obtain DIN and DSC for Directors

Each proposed director requires:

- Director Identification Number (DIN) – a unique identifier issued by the MCA

- Digital Signature Certificate (DSC) – required for electronically signing incorporation documents

For UK-resident directors, identity and address proofs (passport, utility bill) must be notarised by a UK notary before submission. They must also be apostilled under the Hague Apostille Convention via the Foreign, Commonwealth and Development Office (FCDO). This step alone can add 2–4 weeks if not planned in advance.

Step 2: Reserve the Company Name

Submit the RUN (Reserve Unique Name) form on the MCA portal. The name must:

- Follow the format: [Trade Name] + [Business Activity] + Private Limited

- Not be identical or similar to existing registered companies

- Not suggest any connection to a government body

Approved names are reserved for 20 days, so timing is critical—ensure all other documents are ready before filing RUN.

Step 3: Prepare and Apostille UK Corporate Documents

The following UK company documents are mandatory:

- Certificate of Incorporation of the UK parent

- Board resolution authorising the Indian subsidiary's formation

- Identity and address proofs of all directors and shareholders

All documents must be:

- Notarised by a UK solicitor or notary

- Apostilled by the UK FCDO

This is the step UK businesses most frequently underestimate. FCDO apostille processing can take several weeks, so initiate this in parallel with DIN/DSC applications.

Step 4: Draft the MoA and AoA

The Memorandum of Association (MoA) sets out the company's objects and scope of business. The Articles of Association (AoA) govern internal management (board meetings, share transfers, director appointments).

Common mistake: Defining objects too narrowly in the MoA. If you later want to expand into adjacent activities, amending the MoA requires a special resolution and ROC filing. At the same time, overly broad objects in restricted sectors can attract regulatory scrutiny — so precision here matters in both directions.

Step 5: File the SPICe+ Form with the ROC

SPICe+ (Simplified Proforma for Incorporating a Company Electronically Plus) is the single integrated incorporation form that simultaneously applies for:

- DIN allotment

- Company name reservation

- PAN (Permanent Account Number)

- TAN (Tax Deduction Account Number)

- GST registration (optional at this stage)

- EPFO/ESIC registrations

- Certificate of Incorporation

The ROC reviews the application and issues a 21-digit alphanumeric Corporate Identity Number (CIN) upon approval.

Step 6: Post-Incorporation Registrations

Once the Certificate of Incorporation is received:

- Open a corporate bank account and deposit initial share capital

- File Form INC-20A (Commencement of Business Certificate) within 180 days

- Appoint a statutory auditor within 30 days under Section 139(6) of the Companies Act, 2013

- Register for GST if turnover will exceed applicable thresholds

- Register with EPFO/ESIC if employee count triggers those thresholds

Post-Incorporation Compliance and Tax Obligations for UK Companies

Ongoing Statutory Compliance

Board meeting requirements (Section 173):

- Minimum four board meetings per year

- Maximum gap of 120 days between consecutive meetings

- First board meeting within 30 days of incorporation

ROC annual filings:

| Filing | Form | Deadline |

|---|---|---|

| Annual financial statements | AOC-4 | Within 30 days of AGM |

| Annual return | MGT-7 | Within 60 days of AGM |

Statutory audit: Required under the Companies Act, 2013. The auditor must be appointed within 30 days of incorporation and reappointed at each AGM.

Many UK companies with an Indian WOS work with firms like VJM Global to manage these ongoing obligations, covering accounting, audit coordination, and ROC filings to avoid late penalties.

Corporate Income Tax Obligations

A WOS incorporated in India is taxed as a domestic Indian company, not a foreign company. Under Section 115BAA of the Income Tax Act, the applicable rate is:

- Base rate: 22%

- Surcharge: 10% (fixed)

- Health and Education Cess: 4%

- Effective rate: approximately 25.17%

Companies opting for Section 115BAA are exempt from Minimum Alternate Tax (MAT). For companies not opting for this regime, MAT applies at 15% of book profits under Section 115JB.

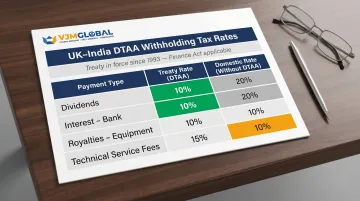

UK-India Double Taxation Avoidance Agreement (DTAA)

These domestic rates don't tell the full story. Where profits flow back to the UK parent — as dividends, interest, or royalties — the UK-India DTAA limits how much India can withhold at source.

The UK-India DTAA, in force since 25 October 1993, caps withholding tax rates on cross-border payments:

| Payment Type | Treaty Rate | Domestic Rate (without DTAA) |

|---|---|---|

| Dividends (general) | 10% | 20% |

| Interest (bank) | 10% | 20% |

| Royalties (equipment use) | 10% | 10% |

| Technical service fees (make available) | 15% | 10% |

To claim treaty benefits, the UK parent must provide a Tax Residency Certificate (TRC) from HMRC and complete Form 10F for the Indian deductor.

FEMA Compliance and Profit Repatriation

Under the Foreign Exchange Management Act (FEMA):

- FC-GPR (Foreign Currency - Gross Provisional Return) must be filed with the RBI within 30 days of share allotment to the UK parent

- The UK parent can repatriate profits (dividends) after paying applicable taxes (10% withholding under DTAA)

- Transfer pricing arrangements between the UK parent and Indian WOS must comply with Section 92 of the Income Tax Act: all intercompany transactions (management fees, royalties, loan interest) must be documented and priced at arm's length. Failure to do so can trigger penalties of up to 2% of the transaction value under Section 271AA.

Additional Compliance Obligations

- Statutory registers must be maintained at the registered office

- Form MBP-1 (director disclosure) must be filed for any material pecuniary interest

- Share certificates must be issued within 60 days of incorporation

- Beneficial ownership declarations (MGT-4, MGT-5, MGT-6) must be filed within 30 days

Common Mistakes UK Businesses Make When Setting Up a WOS in India

Underestimating Document Apostille Timelines

A common assumption is that notarised documents are sufficient — but every corporate and personal document must be both notarised and apostilled via the FCDO. This can add 2–4 weeks if not planned in advance. To avoid delays, initiate apostille processing in parallel with your DIN/DSC applications.

Choosing the Wrong Business Activity Scope in the MoA

Defining business objects too narrowly in the MoA creates problems if you later want to expand into adjacent activities. Amending the MoA requires a special resolution and ROC filing, adding time and cost. Conversely, drafting overly broad objects in restricted sectors may trigger regulatory scrutiny or inadvertently require government approval.

Overlooking Transfer Pricing Compliance

Intercompany charges — management fees, royalties, loan interest — between a UK parent and its Indian WOS are often handled informally. Under India's transfer pricing rules, every such transaction must be documented and priced at arm's length. Non-compliance exposes the WOS to penalties, interest, and tax adjustments during audits.

VJM Global supports this with transfer pricing documentation services, including FAR (Functions, Assets, Risks) analysis, benchmarking studies, and Form 3CEB preparation.

Frequently Asked Questions

What is a wholly owned subsidiary in India?

A WOS is a company incorporated under Indian law in which 100% of the share capital is held by a foreign parent company. It operates as a separate Indian legal entity with limited liability, giving the parent full control over operations.

Does wholly owned subsidiary mean 100% ownership?

Yes, a WOS means the parent company owns the entire share capital. India's Companies Act requires a nominee shareholder to meet the two-shareholder minimum, but beneficial ownership remains 100% with the parent (confirmed via MGT-4, MGT-5, and MGT-6 filings).

How to set up a wholly owned subsidiary in India?

The process runs in three phases: pre-incorporation work (obtaining DINs and DSCs for directors, reserving a company name, apostilling UK corporate documents), filing (drafting the MoA and AoA, submitting the SPICe+ form to the ROC), and post-incorporation registrations (PAN, TAN, GST, bank account, and statutory auditor appointment).

What is an example of a wholly owned subsidiary in India?

Rolls-Royce India Private Limited is a wholly owned subsidiary of Rolls-Royce Holdings plc (UK). Similarly, Barclays Investments & Loans (India) Private Limited operates as a holding entity within the Barclays Group — both incorporated under India's Companies Act.

Can a UK company set up a wholly owned subsidiary in India without prior RBI approval?

In most sectors, yes. UK companies can invest under the automatic FDI route, which does not require prior RBI or government approval—only post-allotment FC-GPR reporting to the RBI is required. Government-approval sectors (defence beyond 74%, print media, multi-brand retail) are the exception.

What are the ongoing compliance requirements for a WOS in India?

Annual ROC filings (AOC-4, MGT-7), statutory audit under the Companies Act, GST and income tax return filings, minimum four board meetings per year, FEMA reporting (FC-GPR), and transfer pricing documentation for intercompany transactions with the UK parent.