GSTR-9/9C现已开放2024-25财年申报。这些表格已更新,以解决现有表格的缺陷。在这一行中,GSTN发布了常见问题解答的详细清单。GSTN发布的常见问题解答以及解释和示例如下所示。这些常见问题解答将帮助纳税人更好地了解GSTR-9/9C的各种表格。

常见问题解答:

1。GSTR 9/9C 何时启用 2024-25 财年的申报?

- 一旦提交了2024-25财年所有到期的GSTR 1和GSTR 3B,GSTR-9/9C将启用。

- 在 2024-25 财年任何 GSTR 1 和 GSTR 3B 待处理的情况下,将不启用 GSTR 9。

- GSTR 9中表4,5,6,8和9的所有相关单元格将根据GSTR-1/ 1A/ IFF或GSTR 2B或GSTR 3B中提供的信息自动填充。

2。GSTR 9 的表 8A 中应自动填充什么值?

- 2024-25财年GSTR 9的表8A按以下方式计算了ITC:

- 对2024-25财年GSTR 2B中出现的2024-25财年所有入境供应的ITC;

- 应包括2025年4月至2025年10月期间在明年2025-26年的GSTR 2B中出现的2024-25财年的发票;以及

- 应不包括2024年4月至2024年10月期间出现在GSTR 2B中的上一2023-24财年的发票。

3.在 IMS 仪表板上采取的操作会对 GSTR-9 产生任何影响吗?

- IMS 对 GSTR 9 没有直接影响。

- 只有构成 GSTR-2B 一部分的文件才能构成 2024-25 财年 GSTR 9 的一部分。

4。GSTR 9表4/5中的汽车价值总量是否会考虑通过GSTR 1A增加/修改的供应?

- 表4载有 “应纳税财政年度内预付款、进出供应的详细情况”;

- 表5包含 “在财政年度内无需纳税的对外和流入供应的详细信息”

- 是的,从 2024-25 财年起,在 GSTR 9 表4、5中,通过GSTR 1A增加/修改的供应量将与 GSTR-1 和 IFF 一起考虑汽车总量。

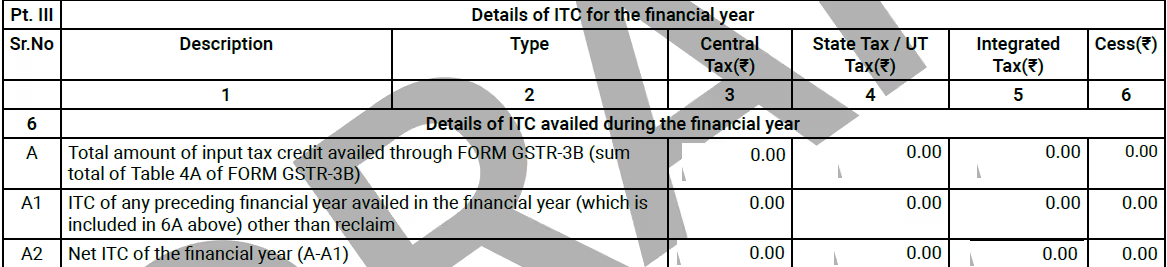

5。什么是表 6A1,需要申报的金额是多少?

- 2024-25财年GSTR 9的表6A1列出了接收方在本财年(2024-25年)至指定时间段内申报的上一财年(2023-24年)的国际贸易法案。

- 此类 ITC 已包含在 GSTR-3B 年内提供的 ITC 中。

- 但是,根据第37/37A条在本财年(2024-25年)收回的有关2023-24财年或之前任何其他财政年度的任何国际贸易中心都不会在GSTR 9的表6A1中报告。

- 因此,表6A2中该财政年度的净国际贸易中心是本财年(2024-25年)的国际贸易中心净额。

- 由于表 6A1 中排除了上一财年的国际贸易协定,因此在 2023-24 财年之前,它不会像 GSTR-9 那样,在 GSTR 9 的表 6J 中造成差异。

6。由于标签自2024-25财年以来已更改,表6M的报告是否有任何变化?

- 表 6M 表示 “通过 ITC-01、ITC-02 和 ITC-02A(GSTR-3B 和 TRAN 表格除外)获得的 ITC

- 对表 6M 的标签更改使其与通知表格的说明保持一致。但是,这种标签变更不会对报告产生任何影响。

7。是否可以在 Excel 中下载表 8A?

- 对于在线表8A中自动填充的金额,发票方面的详细信息在GSTR 9仪表板的Excel表格中以 “下载表8A文档详情” 的形式提供。

- 纳税人可以下载并参考发票/DN/CN,金额将根据该发票自动填充到在线表8A中。

8。无论如何,在 GSTR-9 的表 8A 中自动填充的 ITC 和 Excel 中反映的 ITC 是否有所不同?

- 是的。在以下情况下,根据在 Excel 中下载的表 8A,ITC 和 GSTR-9 表 8A 中反映的 2024-25 财年的 ITC 可能会有所不同:

- RCM 涵盖的对外供应将出现在表 8A Excel 中,但不会出现在自动填充的数字中。

- 外向供应报告为正常费用,后来修订为RCM,将在表8A Excel中反映为B2B和B2BA。但是,该金额不应构成自动填充的ITC的一部分;

- 对外供应,其中收件人和供应商属于不同的州,但同一个州的采购订单是供应商州,因此需要收取商品及服务税和商品及服务税。

- 由于PoS规则,该记录不符合ITC的资格。

- 对外供应从2024-25财年修改为2025-26财年,然后将出现在表8A Excel中(Excel表格的B2B部分),但不会出现在在线表8A中

- 对外供应从 2025-26 财年修改为 2024-2,5 财年,然后将出现在表 8A Excel(Excel 表单的 B2BA 部分)中,并将在线出现在表 8A 中

- 因此,在 GSTR-9 的表 8A 中自动填充 ITC 是正确的。但是,由于上述各点,表8A Excel中可能还有一些其他记录。

9。供应商是否会对GSTR 1/1A/IFF进行任何修改,ITC的变更会自动填充到我的GSTR 9表8A(Excel和Online)中?

- 是的,如果修订后的供应与2024-25财年有关,则GSTR 1/1A/IFF中表8A中的汽车总量的任何修正案都将与修订后的记录相同。

- 例如。

- 发票日期:2025 年 3 月 30 日;

- GSTR-1 申报月份:2025 年 4 月;

- 因为这是2024-25财年的合格记录。因此,根据表8A(Excel和Online),国际贸易中心将出现同样的情况。

例如。

- 对此类记录的修正:2025年5月的GSTR 1;

- 发票日期更改为 2025 年 4 月 30 日;

- 现在,该文件与2025-26财年有关,因此不考虑将其纳入2024-25财年GSTR 9的表8A(在线)。

- 但是,该记录将继续出现在2024-25财年GSTR 9的表8A Excel(B2B部分)中。

10。在 2025 年 10 月之前的下一个财年的 GSTR-1 中报告的当前财年的发票,那么它将如何自动填充到表 8A 中?

- 在这种情况下,收款人将本财政年度的发票/DN/CN自动填充到2024-25财年的表8A中,此前收款人将以ITC的身份填写相应纳税期的GSTR 3B,由收款人在其GSTR 3 B中申报。

- 例如:

- 2024-25 财年的发票在 2025 年 5 月的 GSTR-1 中报告;

- 此类发票应构成符合条件的ITC的收款人GSTR 2B的一部分;

- 纳税人提交 2025 年 5 月 GSR 3B 后,此类发票将自动填充到 2024-25 财年 GSTR 9 的表 8A 中

11。GSTR 9 的表 8C 是什么?

- 表8C包含当前财年的ITC数据,该数据将在下一个财年在规定的时间段内提供。

- 该表不包括在2024-25财年申请并在2024-25财年撤销并在下一财年收回的任何ITC。

- 因此,它仅包含当前财年(2024-25年)未兑现的ITC,该国际贸易法在下一财年的GSTR 3B中申报的截至指定时间段。

12。表8C是否会列出在财年(2024-25财年)申领和撤销并在下一个财年(2025-26年)收回的ITC?

- 不,不应在2024-25财年GSTR 9的表8C中报告此类回收的ITC。

- 例如。

- 国际贸易委员会于2025年3月提出索赔(GSTR 3B的表4A5),并于2025年3月撤销了同样的索赔(GSTR 3B的表4B2),因为货物尚未到达工厂。

- 现在,在2025年4月,该ITC将在GSTR 3B的表4A5中收回。

- 此类ITC将在2024-25财年GSTR 9的表6B和表7H中报告。

- 表 6B:内向供应(进口和入境供应除外,但包括从经济特区获得的服务)

- 表 7H:本财政年度ITC撤销和不符合资格的ITC的详细信息-其他撤销

- 表8A将包含相应的ITC,表8B也将根据2024-25财年GSTR 9的表6B自动填充。

- 因此,表 8D 中没有区别。

- 因此,不应在表8C中报告此类ITC,因为这将造成表8D中的不匹配。此回收应仅在表 13 中报告。

13。在什么情况下,应在GSTR 9的表8C中报告ITC?

- 只有在以下情况下才会在表8C中报告金额:

- 与2024-25财年相关的ITC是GSTR 2B的一部分,已自动填写在GSTR9的表8A中,但在2024-25财年收款人尚未申报,在指定时间段之前,该ITC首次在下一财年(2025-26年)GSTR 3B的表4A5中申报。

- 供应商在 2025 年 4 月 25 日至 2025 年 10 月的 GSTR 1 中报告的 2024-25 财年的发票。因此,该ITC首次出现在下一财年(2025-26年)GSTR 3B的表4A5中。

- 例如。

- 购买商品:2025 年 1 月;

- 但是,他未能在2025年1月申请国际贸易委员会;

- 此类ITC是在2025年5月申请的。

- 此类国际贸易中心将反映在表8C中

- 例如。

- 购买商品:2025年1月;

- 供应商在 2025 年 4 月的 GSTR-1 中报告了此类发票;

- 收款人在 2025 年 4 月的 GSTR 3B 中申请了此类ITC;

- 此类ITC将自动填充到2024-25财年GSTR 9的表8A中,该表已于明年在指定时间段内首次申报;

- 此类ITC将在2024-25财年GSTR 9的表8C和表13中报告。

14。商品已在24-25财年进口,但是在2025-26财年国际贸易法委员会已经考虑了GSTR 9中将如何报告这一情况。

- 此类ITC将在新插入的表8H1(下一个财政年度用于商品进口的IGST抵免)中报告,而不会在GSTR 9的表6E(商品进口(包括来自经济特区的供应))中报告。

- 在表8G中报告商品进口时支付的IGST;

- ITC声称将在下一财年在表8H1中报告;

- 该ITC将在24-25年的GSTR 9的表13中报告。

15。由于GSTR 3B中已插入负负债表,因此在2024-25财年GSTR 9表9中的应纳税额中自动填充了哪个值?

- 应纳税列取自GSTR 3B,取自净负债。

- 如果GSTR 3B表6.1中报告的负债为正(总额减去负负债),则此类正净纳税负债将自动填充到表9的应纳税额项下。

- 但是,如果表 6.1 中的净金额显示为负数,则表 9 的应纳税额列下不会自动填充任何金额。

- 此外,GSTR 9表9中的应纳税列保持可编辑状态,因此,如果需要,纳税人可以更改该值。

16。表 12 和表 13 的标签变更是否会对报告产生任何变化?

- 与之前的任何财政年度相比,表12和表13标签的变更对报告没有任何区别。

- 表12列出了下一个财政年度(2024-25年)逆转的国贸中心数据。

- 表13列出了下一个财政年度可用的财政年度(2024-25年)的国际贸易中心。

17。在2024-25财年GSTR 9的表17中是否有其他便利设施可以提交HSN的详细信息?

- GSTN现已为下载名为 “下载GSTR 1/1A HSN详细信息的表12” 的额外Excel表格提供了便利;

- 这样的 excel 汇总了 GSTR-1 表 12 的详细信息;

- 此类excel表中的其他表格还以GSTR 9表17的格式提供了数据。

- 这将便于纳税人使用下载文件并在2024-25财年的GSTR 9表17中报告相同的内容。

18。如果 FY24-25 的 RCM 下的商品及服务税以 FY25-26 的 GSTR3B 支付。应在2024-25财年或2025-26财年的GSTR 9中报告RCM的负债和ITC吗?

- 上述RCM交易的RCM负债和ITC应在2025-26财年的 GSTR-9 中报告。

- 解释——正如CBIC在2019年7月3日的新闻稿中澄清的那样,RCM负债可能会在支付当年进行报告,并附上适用的利息(如果有)。

- 上述新闻稿的相关摘录-

“g) 在2018-19财政年度支付的2017-18财政年度的反向收费:许多纳税人要求澄清2017-18财年按反向收费缴纳但在2018-19财年缴纳的税款的相应栏目或表格。值得注意的是,由于付款是在2018-19财年支付的,因此此类税款的进项税抵免只能在2018-19财年提供。因此,此类详细信息不会在2017-18财年的年度申报表中公布,而将在2018-19财年的年度申报表中公布。如果此次调整导致营业额的计算有任何差异,则可以在对账表(GSTR-9C 表格)中报告同样的差异,并说明理由”

结论:

GSTR-9 和 GSTR-9C 是必不可少的申报表,因为它们汇总了全年提交的所有商品及服务税申报表,因此需要与账簿进行比较。GSTR-9 和 9C 是进行任何更正和披露任何其他信息的最后机会。必须强调的是,纳税人无法选择修改这些表格。因此,建议纳税人寻求专业指导,以确保GSTR-9/9C中提供准确的信息。在V J M Global,我们是一支由商品及服务税专家组成的团队,随时准备协助您正确申报GSTR-9/9C。