.avif)

If you handle your company’s accounting, understanding how to record an accounts payable journal entry is essential. Every time you receive goods or services on credit, it increases your liabilities. If these transactions are not recorded correctly, it can cause errors in your financial reports, delays in payments, and problems during audits.

This guide will explain how to create accurate accounts payable journal entries, when to record them, how to connect them to vendor accounts, and their effects on your balance sheet and cash flow. Whether you use manual bookkeeping or accounting software, this information will help you keep clear and accurate financial records.

An accounts payable journal entry is a specific financial record that captures transactions related to the money your business owes to suppliers, vendors, or service providers.

It is recorded in your company’s general ledger, which is the central place where all financial activities are tracked and maintained.

Whenever you purchase goods or services on credit, an accounts payable journal entry increases your outstanding liabilities. Conversely, when you make payments to clear those debts, the journal entry reduces the balance owed.

These entries are essential for maintaining accurate financial statements, managing cash flow, and ensuring your business meets its payment obligations on time. Keeping precise accounts payable journal entries helps avoid errors, supports audits, and ensures compliance with accounting standards.

Quick fact: Studies show that nearly 40% of invoices contain errors, highlighting the need for careful journal entry management.

An accounts payable journal entry reflects a company’s obligation to pay for goods or services received on credit. It ensures accurate financial reporting and helps track outstanding liabilities. Properly recorded entries support compliance, audit readiness, and vendor transparency. To maintain clarity, each entry should include the following components:

Including all these components ensures your accounts payable journal entries are complete, accurate, and easy to understand for accounting and audit purposes.

Also Read: Key Differences Between Accounts Payable and Accounts Receivable

Now, let’s look at the different types of accounts payable journal entries you will encounter.

Accounts payable journal entries vary based on the nature of the transaction. Each type captures different stages in the payment cycle, from receiving invoices to settling dues. Accurate recording ensures your books reflect real-time liabilities and helps maintain vendor trust. Below are the most common types of accounts payable journal entries:

When you buy goods or inventory on credit, record the transaction as:

If you return damaged or unwanted inventory to the supplier, use this entry:

When you acquire fixed assets like equipment or furniture on credit, record:

For services such as consultancy or legal work received on credit, use this entry:

When you pay off amounts owed to your creditors, record:

Recording these different types of accounts payable entries correctly will help you maintain accurate financial records and manage your payables efficiently.

Also Read: Understanding the Advantages of Outsourcing Accounts Payable

Timing is crucial. Here’s when you should record these journal entries.

Accurate timing in recording accounts payable journal entries is essential for maintaining clear financial records and ensuring smooth cash flow management. Here are the key scenarios when you should record these entries:

By recording your accounts payable journal entries promptly and accurately in these situations, you can maintain precise financial records, avoid errors, and manage your company’s obligations efficiently.

To help you out, here are some practical examples of how to record these entries.

Recording accounts payable journal entries correctly is essential to keep your financial records accurate. When your business acquires goods or services from a vendor on credit, you need to record these transactions promptly in your accounting system.

There are two main types of accounts payable journal entries: simple and more detailed, depending on the nature of the transaction.

Here are some common examples of accounts payable journal entries to help you understand how to record them:

When you purchase inventory on credit, the entry records the increase in your purchases and your liability to pay the supplier later.

Example:

On March 5, 2025, ABC Traders bought office supplies worth ₹25,000 on credit.

Journal Entry:

If you use a perpetual inventory system, debit the Inventory Account instead of Purchases.

If part of the inventory you purchased is damaged or not needed, and you return it to the supplier, you need to reduce your accounts payable and record the return.

Example:

On March 12, 2025, ABC Traders returned ₹5,000 worth of damaged office supplies to the supplier.

Journal Entry:

When you buy fixed assets like equipment or furniture on credit, the asset account increases while your accounts payable liability also increases.

Example:

On March 15, 2025, ABC Traders purchased office furniture worth ₹50,000 on credit.

Journal Entry:

If you receive professional services such as consulting or legal advice on credit, record the expense and the related liability.

Example:

On March 20, 2025, ABC Traders received consulting services worth ₹15,000 on credit.

Journal Entry:

When you make a payment to settle your accounts payable, the liability decreases, and your cash or bank balance is reduced.

Example:

On March 30, 2025, ABC Traders paid ₹30,000 to its supplier to clear part of its outstanding balance.

Journal Entry:

Suppose your business buys a laptop worth ₹60,000 on credit from a vendor on April 1, 2025. The journal entry would be:

When you pay the vendor on April 10, 2025:

Recording these entries correctly helps you keep your financial data accurate, manage vendor relationships, and maintain compliance with accounting standards.

Also Read: Effective Strategies for Accounts Payable Management

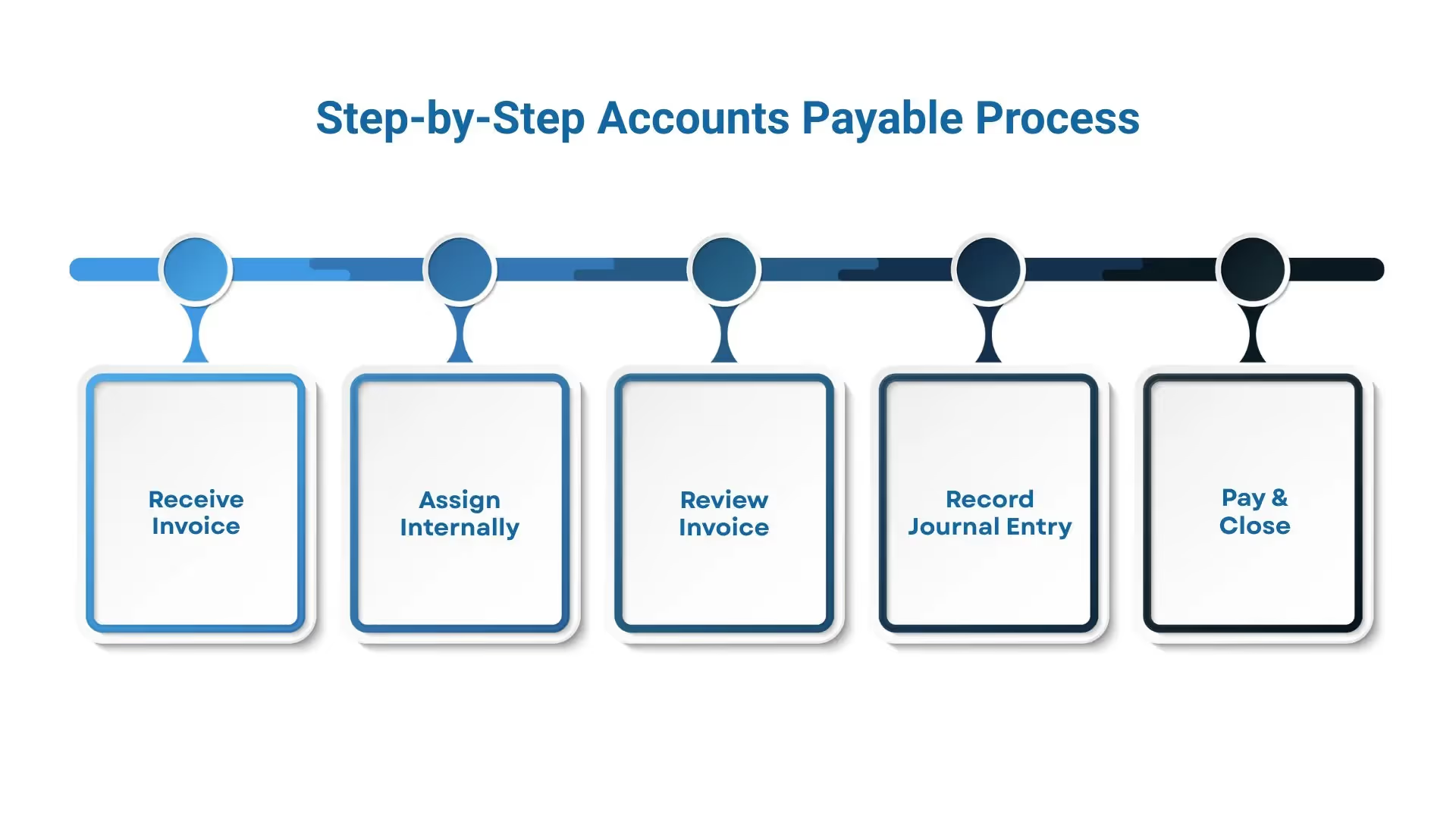

Managing accounts payable involves several important stages; here’s an overview of the process.

Managing accounts payable effectively is essential for maintaining smooth financial operations and strong supplier relationships.

The process varies by company size and structure. In smaller businesses, a single Accounts Payable Manager may handle all steps, while larger organizations often divide responsibilities across departments for greater accuracy and control.

Here’s a detailed guide to the five critical stages of the accounts payable process:

Once the vendor ships goods or provides services, they send you an invoice for payment. Invoices can arrive by email, fax, mail, or through an online portal. It is important to ensure the invoice includes:

Entering the invoice promptly into your accounting system ensures timely tracking and payment, helping you avoid late fees and maintain good vendor relations.

After receiving the invoice, it is assigned internally for verification. Usually, the Accounts Payable team is responsible for:

This step is essential to prevent errors, duplicate payments, or fraud by ensuring only authorized transactions proceed.

Before approval, the invoice is reviewed carefully to confirm that all information is correct. This review includes:

An accurate invoice review ensures your payments are processed without delay and that your accounting records are precise.

Once the invoice passes review, you must record the transaction in your accounting system. This involves:

Making these entries promptly keeps your general ledger accurate and up-to-date, reflecting all outstanding obligations on your balance sheet.

The final step is to pay your vendor on or before the due date. The payment process typically involves:

Once payment is made, you record another journal entry to debit accounts payable and credit your cash or bank account. This closes the payable and updates your records.

Following these stages helps you maintain:

It’s equally important to be aware of common mistakes and how to avoid them. Let's explore in the next section.

Managing accounts payable journal entries accurately is crucial for reliable financial reporting and smooth business operations. However, several common mistakes can occur, leading to errors or delays. Here are some pitfalls to watch out for:

By avoiding these common mistakes, you ensure your accounts payable process runs smoothly and your financial reports remain accurate.

Need expert help to streamline your accounts payable process and avoid costly errors? Partner with VJM Global, experts in accounting and financial solutions who can optimize your bookkeeping, enhance accuracy, and improve compliance.

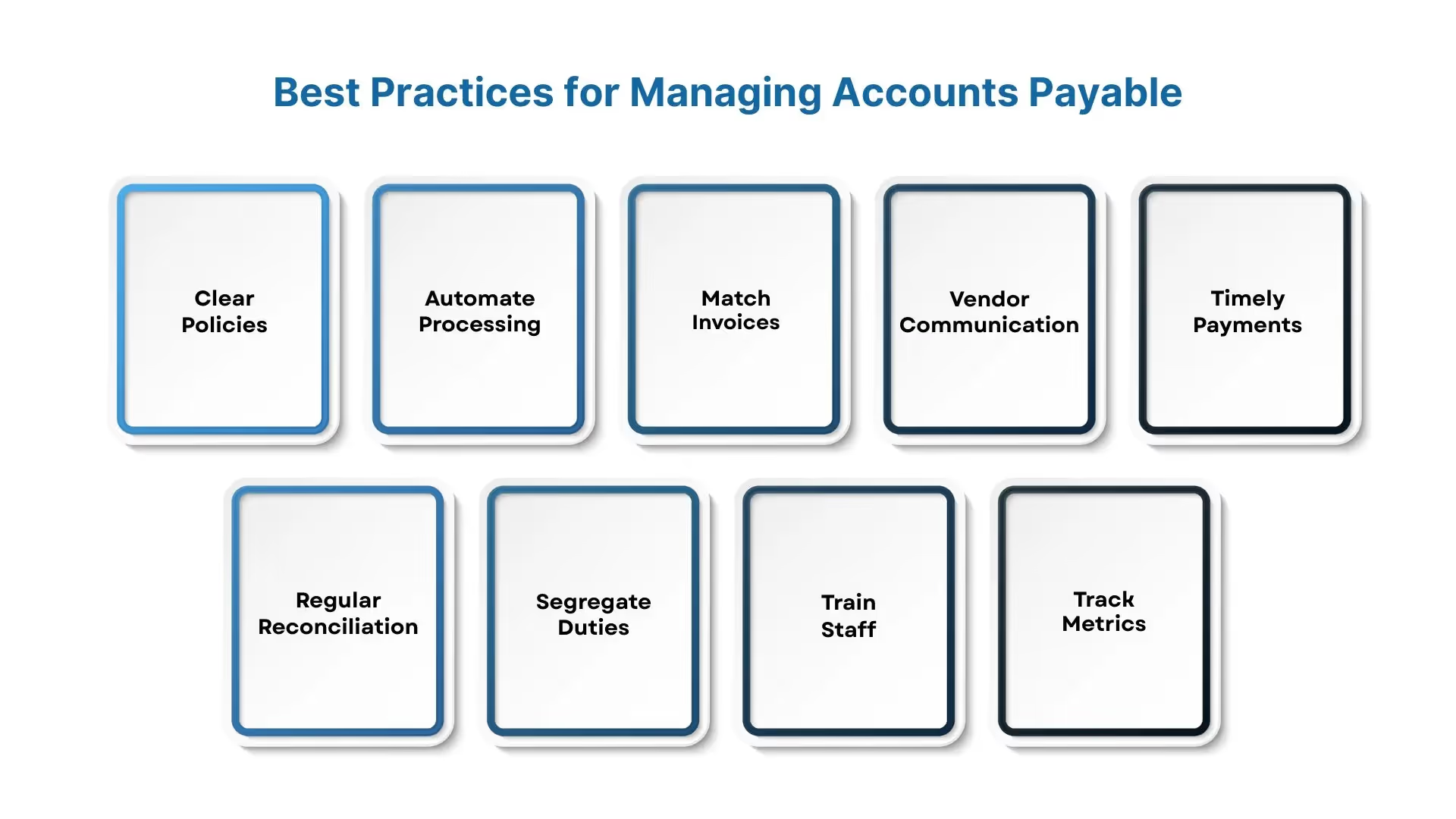

Finally, here are some best practices to keep your accounts payable process running smoothly.

Efficient management of accounts payable is key to maintaining healthy cash flow, strong vendor relationships, and accurate financial records. Here are some proven best practices to help you optimize your accounts payable process:

By following these best practices, your organization can manage accounts payable efficiently, reduce costs, and improve financial accuracy.

Accurate and timely accounts payable journal entries are fundamental to maintaining healthy financial records, managing cash flow effectively, and fostering positive vendor relationships. By understanding the different types of journal entries, following the proper stages in the accounts payable process, and adopting best practices, your business can avoid costly errors and streamline its financial operations.

Get expert support with your accounts payable process by partnering with VJM Global. Our specialized accounting solutions and dedicated team help you improve efficiency, reduce errors, and maintain clear, compliant financial records.

Next Read: Outsourced Accounting as a Service Benefits