Standard Operating Procedure to be followed in case of non-filers of returns includes best judgement assessment by proper officer for nonfillnig of GSTR 3B with in due dates.

Every taxpayer is liable to make payment ofGoods and Service Tax (“GST”), alongwith filing of return in form GSTR-3B, onmonthly basis by 20th of the following Month. If taxpayer fails tofurnish GSTR-3B by such due date then he is mandatorily required to pay latefee of INR 20/INR 50 per day. GST Portal will auto-populate the penalty forlate filing in GSTR-3B of following month.

Further, if taxpayer fails to furnish GSTR-3B for continuous period of 2 months then jurisdictional Assessing Officer may cancel GST registration of such taxpayer after following principle of Natural Justice.

Despite of stringent provisions, Departmentis still adopting various measures to regularize the filing of GST return. VideCircular 129/48/2019-GST dated 24th December, 2019, department has prescribedthe “StandardOperating Procedure to be followed in case of non-filers of returns”.

RelevantProvisions of GST Law:

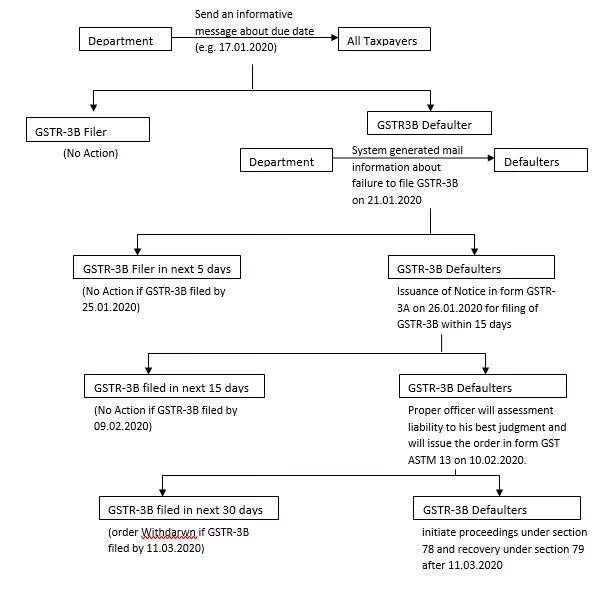

Procedureto be followed in case of Non-filer of returns

Step 1: Asystem generated message would be sent to all the registered persons 3 daysbefore the due date to nudge them about filing of the return for the tax periodby the due date.

Step2: After expiryof due date of furnishing GSTR-3B, a system generated mail will be sent to alldefaulters informing them about their failure to furnish return by due date.Copy of the same will be sent to authorized personnel andproprietor/Partner/Karta/Director.

Step3: 5 days afterexpiry of due date to furnish GSTR-3B, notice under section 46 of CGST Act readwith Rule 68 in form GSTR-3A will be sent to persons who fails to furnishGSTR-3B. Such notice will require him to furnish such return within 15 days.

Step 4 If defaulter fails to furnish GSTR-3B within 15 days of issuance of GSTR-3A, then proper officer may proceed to assess tax liability of such person under section 62 of CGST Act (i.e., to the best of his judgment). While assessing tax liability, proper officer will take into account all material available to him* and would issue an order in form GST ASMT-13. Summary of such order will be uploaded in form GST DRC-07.

*Details of sales outward furnished in form GSTR-1, details of inward supply auto-populated in form GSTR-2A, information available through e-waybill portal or information collected through any other source such as inspection

Step5: If defaulterfurnishes return in form GSTR-3B within 30 days of service of order in form GSTASMT-13 then such order shall be deemed to be withdrawn. However, in case offailure, proper officer may initiate proceedings under section 78 and recoveryunder section 79 of the CGST Act.

Step6: Indeserving cases, based on the facts of the case, the Commissioner may opt forprovisional attachment under section 83 of the CGST Act before issuance of FORMGST ASMT-13 to protect revenue.

Step 7: Proper officer would initiate action under section 29(2) CGST Act for cancellation of registration if registered person fails to furnish GSTR-3B for consecutive period of 6 months.

Read More Important Points to be considered for GSTR-3B return under GST.